article final ver 1

TRANSCRIPT

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 1/18

Crude Oil - End Product Linkages in the European

Petroleum Markets

Szymon Wlazlowski∗

Aston Business School, Aston Triangle, Birmingham B4 7ET, UK

E-mail address: [email protected]

Abstract

Crude oil prices were found to have a significant impact on retail petroleum product pricesand were shown to affect inflation and other key economic indicators. This article analyses the

former link in the European Union (EU) within a multi-national and multi-product framework.The results indicate that the old EU countries from North-West Europe are well integrated inthe global petroleum markets, while the Mediterranean and Eastern European countries dependon the low-quality Russian oils. Furthermore, while product prices in the North West Europeare driven by the world benchmark crudes, countries with easy access to Russian oil are in thebi-directional relationship with its prices.

JEL Classification: Q410, C220, D400.

Keywords: Oil Markets, Price Transmission, Europe.

1 Introduction

1.1 Motivation

Modelling the impact of crude oil prices on retail petroleum product prices continues to receive

significant attention in the applied literature (see Meyer & Cramon-Taubadel (2004) and Frey &

Manera (2005) for recent literature reviews). However, some important questions about the details

of this transmission mechanism are still left unanswered - in particular the type of crude oil driving

the downstream prices and cross-product and cross-national patterns in transmission.

These seemingly trivial details are of some significance also outside the field of energy economics.

In particular, recent proposals for inclusion of crude oil prices in macroeconomic inflation targeting

models - Krichenel (2005) - should be implemented with care, as the results could be potentially

∗I am grateful to the Editors, the anonymous referee, Dr Monica Giulietti, Dr Jane Binner, and Bj orn Hagstromerall at Aston University and Prof Costas Milas at Keele University. The usual disclaimer applies.

1

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 2/18

misleading if the wrong kind of crude oil is assumed to affect inflation or, ironically, consumer prices

drive endogenous crude oil prices.

So far, the researchers assumed that downstream product prices and macroeconomic indicators

follow only one of the two most acclaimed benchmarks - WTI or Brent, and that the crude oil prices

are not affected by the local market conditions (i.e. they are exogenous). This simplification could

be challenged for several reasons.

Firstly, one has to remember that the benchmarks offer just a snapshot of a complicated market

which is supplied with hundreds different varieties of crude oil - Energy Intelligence Group (2004).1

The popular benchmarks - Brent and WTI, are both rather niche products - their outputs are

respectively 0.68% and 1.77% of the global production.2 Given the above, those crudes are not

commonly used in the EU refineries. Furthermore, those benchmark crudes represent the high-

quality segment of the market, whereas the global crude oil market is increasingly comprised of lower

quality crudes. This process could be only strengthen by the closure of old, easy-to-access, high-

quality fields and the technological progress allowing to tap reservoirs of heavy crudes (such as steam

flooding - Bahree & Gold (2006)).

Secondly, examining from the demand side, the crude oil - end product link is far from being

straightforward enough to be proxied by one benchmark crude. During the refining process, the

quality of the crude determines the mix of end products, each of which has different market demand

and price. Figure 1 adapted from Natural Resources Canada (2005) presents the product yields for

different qualities of crudes. The most important point is that refining high-quality crudes results in

greater share of high-quality and high-margin products.3 Furthermore, conversely to the tendencies

in the crude oil supply, the demand for high-quality, low-sulphur crudes is steadily increasing as they

1Every crude can uniquely differentiated by its quality parameters, among which density and sulphur content arethe most important. Light and heavy refer to the density as measured in degrees API . Sweet and sour refer to thesulphur content. As defined by OPEC (2005):

• crudes with API> 35◦ are light , 26◦ <API< 35◦ are medium and API< 26◦ are heavy ;

• crudes are considered to be sweet when the sulphur content does not exceed 0.5% and sour otherwise.Based on such criteria, McQuilling Services, LLC (2006) distinguishes over 500 different crudes.

2Author’s calculations, based on Eni SpA (2006) and Montepeque (2005).3For a more detailed overview of yields during topping and cracking phases see Platt’s (1999).

2

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 3/18

Figure 1: Comparison of Refinery Yields by Crude Quality. Source: Natural Resources Canada(2005).

allow refineries to meet the stricter environmental regulations - Platt’s (2006).

Needless to say, the price of every crude is uniquely set by the changing forces of supply and

demand and can fluctuate - Bacon & Tordo (2005) and Energy Information Agency (1999). To-

gether with prices, transportation costs and technical constraints, the quality parameters directly

influence refineries’ choices of inputs (see van den Berg, Kapusta, Ooms & Smith (2003) for a sample

discussion), which in turn affects the end prices of a wide array of products. The final result of this

process determines which varieties of crude oil are used for refining. Oil companies could choose a

well known global benchmark crude(s) (which are however supply constrained), local crude(s) or a

combination of both.

Energy economists and macroeconomists usually assume that the choice could be simplified by

assuming that oil companies use only Brent or WTI - the best known crudes for which price data is

readily available, disregarding the complexities described above. However, when one combines the

notion that different varieties of crude oil can be used to produce the same products with the fact

that prices of different qualities of crudes often diverge for long spells it is clear that the proxying the

crude oil - product link with one global benchmark might be an oversimplification. The probability

and extent of resulting error depend on the differences between prices of different crudes and for

how long they diverge. While this varies on a case by case basis, to illustrate the importance of the

question posed in this article, it is enough to say that the divergence can be substantial - Energy

Intelligence Group (2004) reports that it reaches such levels that European Brent oil is actually

3

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 4/18

transported all the way to the United States for refining.

1.2 Literature

As pointed out by Lanza, Giovannini & Manera (2003), the specific economic literature on the topic

of crude oil - end product linkages is not very large. Furthermore, it is geared either to financial

markets or to testing for asymmetries in price relationships. Since the latter is of little importance

for the purposes of this article, we shall focus on the former strand of the literature.

Gjolberg & Johnsen (1999) analyse the existence of a long-run relationship between monthly

prices of benchmark crude oil (Brent) and end products (premium leaded petrol, naphtha, jet fuel,

gas oil and light / heavy fuel oils quoted in North-Western Europe, FOB, cargoes) over the period

January 1992 - August 1998. The results support the existence of a relationship between crude oils

and end products which can be effectively used for hedging purposes.

Adrangi, Chatrath, Raffiee & D Ripple (2001) also focus on one crude only (Alaska North Slope)

and its relationship with one product (US West Coast diesel). The results obtained using VARs and

a bivariate GARCH model indicate the presence of uni-directional relationship between the prices,

but the paper contains no discussion about the choice of the crude and possibility that other crudes

can drive the product prices.

Asche, Gjolberg & Volker (2003) use a multivariate VAR to test for the relationship between

Brent oil and several end products. The results indicate that the Brent oil is weakly exogenous, but

no discussion of possible impact of other crudes is presented.

Lanza et al. (2003) compared the prices of ten different kinds of crude oils and prices of fourteen

end products worldwide (i.e. in Mediterranean, North West Europe, Latin America and North

America regions) over the period 1994-2002. This analysis was geared towards explaining prices of

local crudes with the help of the prices of petroleum products and benchmark crudes. The results of

the cointegrating analysis indicate that the differences in quality of crude oil varieties determine their

behaviour - crudes similar to the global benchmarks return more quickly to their long-run values,

4

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 5/18

compared to the crudes of significantly different quality.

Arpa, Gnan & Antoinette (2005) analyse transmission between logs of weekly prices of crude oil

and three end products (heating oil, diesel oil, and unleaded petrol) in 25 EU countries for the period

January 1996 - June 2005 (old EU-15) and May 2004 - June 2005 (new EU-10). The purpose of the

exercise was to compare the impacts of oil price shocks on the product prices across the EU markets.

However, the authors did not present any information on:

• kind of crude oil used;

• the role of exchange rates.

Furthermore, the focus of the article is on pass-through estimates (i.e. long run impact of crude oil

prices on retail prices) obtained using the transformation proposed by Bewley & Fiebig (1990). Given

the disadvantages of this technique (poor small-sample properties and extreme estimate problem)

pointed out in Bewley & Fiebig (1990, p. 349), the results should be treated with caution.

This article attempts to contribute to the discussion about the importance of the right choice of

crude oil. The problem is analysed from a slightly different angle - instead of analysing products and

crudes out of context, the purpose is to analyse the relationship between crude oils and end products

in the multi-national and multi-product setting. This should allow us to verify if the quality of

the crude oil plays any role in the price transmission and establish cross-national and cross-product

transmission patterns.

2 Empirical Analysis

2.1 Data

Data used involves three sets of weekly series:

• USD prices of Brent, WTI and Urals crude oils (denoted xBrentt , xWTI

t , and xUralst );

• k-th country’s net-of-taxes retail prices for:

5

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 6/18

– EURO-95 unleaded petrol (y(ULP,k)t );

– Diesel oil (y(DO,k)t );

– heating oil (y(HO,k)t );

– lead replacement petrol (Super) (y(SUPER,k)t );

– LPG (y(LPG,k)t );

– two kinds of fuel oils (low and high sulphur) (y(RFO−1,k)t and y(RFO−2,k)

t );

• exchange rates between k-th country’s local currency and USD, necessary as crude oil prices

are quoted in USD (exkt ).

The choice of three crudes analysed was inspired by Hagstromer & Wlazlowski (2007), which found

these crudes to price-lead the global markets and by Platt’s (2006) which presented a discussion of

importance of Urals crudes for the European market.

Retail prices were obtained from the OilBulletin published by the European Commission for 25

EU countries. A short description of the products analysed is presented in Table 1.

Table 1: Products Analysed. Source: Platt’s (1999).Product Usage Source PropertiesUnleaded petrol Motor spirit Crude Oil High margin motor spiritDiesel oil Motor spirit Crude Oil – –Heating oil Heating Crude Oil Similar to diesel, lower qualityLPG Motor spirit,

cookingNatural Gas /Crude Oil

When used as motor fuel is referred to asautogas, less commonly used for cooking

Fuel oil Heat / Elec-

tricity

Crude oil Heaviest commercial fuel that can be ob-

tained from the crude oilLRP Motor Spirit Crude Oil Lead replacement petrol, banned in

some EU countries

The length of period covered differs on the country and product basis. The longest sample for

the EU-15 countries stretches4 back to January 1994, while the data for the EU-10 countries5 starts

in mid-2004. All series end in December 2005.

4Austria, Belgium, Denmark, Germany, Finland, France, Great Britain, Greece, Ireland, Italy, Luxembourg, theNetherlands, Portugal, Spain, and Sweden.

5Cyprus, the Czech Republic, Estonia, Hungary, Lithuania, Latvia, Malta, Poland, Slovenia, Slovakia.

6

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 7/18

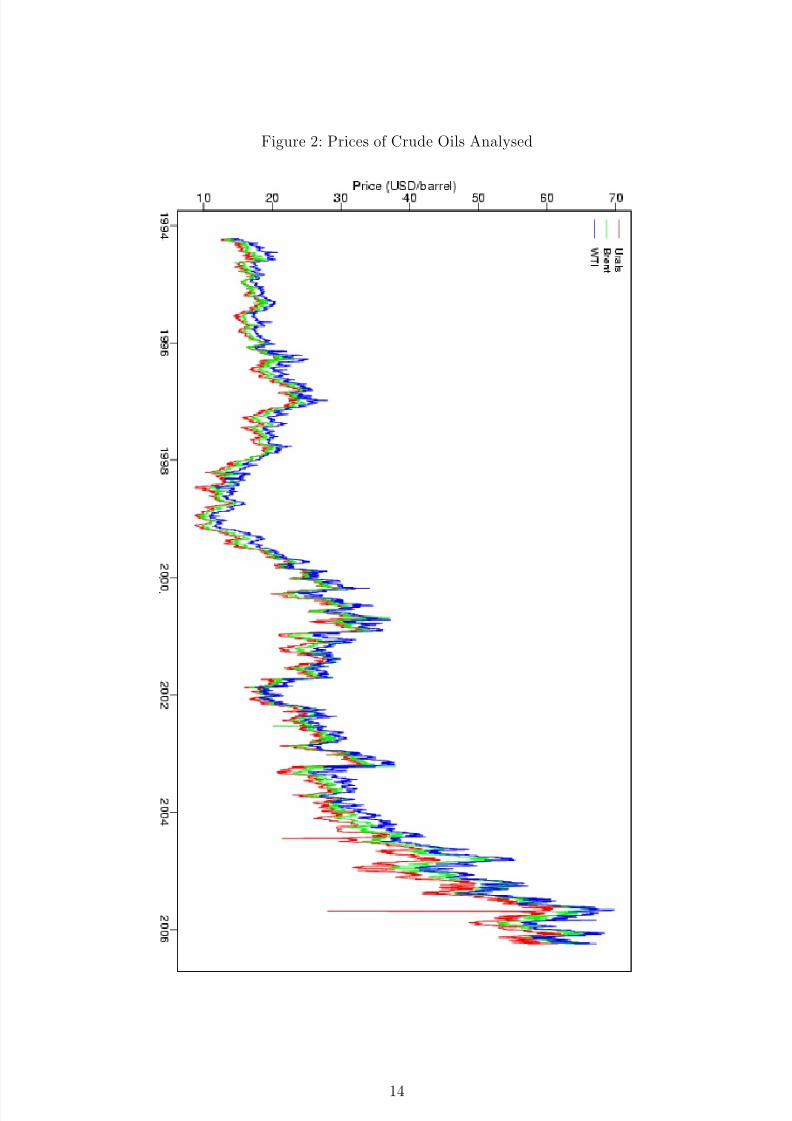

The prices of crude oils analysed in this article represent different geographical segments of the

global oil market with WTI being the global benchmark, usually used in the USA, Brent being the

most popular crude in the North-West Europe and Urals crude being the most popular Russian oil

extracted near Caucasus mountains and transported via the Bosphorus Strait to the Mediterranean

region - Platt’s (2006).

Furthermore, the crudes are of different quality, with Brent and WTI representing the high end of

the spectrum and Urals being low quality crude. The details of those crudes are presented in Table

2. The prices of crudes analysed are presented in Figure 2.

Table 2: Crude Oils Analysed. Source: Platt’s (2007).

Crude Country of origin API Sulphur ContentWTI USA 38◦-40◦ / light 0.3% / sweet

Brent North West Europe 38◦ / light 0.45% / sweetUrals FSU 31◦-33◦ / medium 1.3% / sour

Data on the exchange rates between local EU currencies and USD at relevant times were obtained

from DataStream. The data follow the official exchange up till the introduction of Euro (January

2002), after which the exchange rate follows the EUR/USD exchange rate. The quotes were taken

for the same (or the earliest available) day as the crude oil data. The prices expressed in Euro were

converted to the original currencies using fixed parities established by the European Central Bank.

Using the standard ADF tests, all series were found to be integrated of order one.6

2.2 Cointegration, Endogeneity

Since the series in question are integrated of order one, they have to be analysed in the cointegrating

framework - Maddala & Kim (1999). Only when a common stochastic trend between the series

in question exists, the possibility of spurious regression is rejected and an economically valid link

between crude oil and end product prices can be identified.

As specified by Engle & Granger (1987), cointegration implies an error correction model mecha-

nism, which describes short and long run responses of prices to external shocks and allows for testing

6Detailed results for so many series would require a large amount of space, so the results of the tests are notreported here - they can be provided by the author.

7

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 8/18

for endogeneity of the variables. Intuitively, variables that do react to shocks in other variables

should be modelled on the left-hand side, while those which remain exogenous (determined outside

the system), should be treated as explanatory and the model should be conditioned upon them.

As the first step in the analysis, the following cointegrating equation was estimated for every of

crude oil-product pair:

ln(y( j,k)t ) = α(k,l,j) + β (k,l,j)ln(xl) + γ (k,l,j)ln(exk) + t (1)

where:

• j stands for product;

• k stands for country;

• l stands for crude oil.

For every equation, the Phillips-Perron Z α test for cointegration was conducted, under the null

hypothesis of no cointegration, the long truncation parameter (n/30) and a constant.7 For product-

crude pairs for which the null of no cointegration was rejected at 5%, the following VAR(p) model

was estimated:

B(L)zt = zt − Φ1zt−1 − . . .− Φ pzt−p = t (2)

where:

• B(L)zt is the lag polynomial;

• zt = (ln(y(Product,Country)t ), ln(xCrude), ln(exCountry)) is the column vector of the variables (per

country, per product for all analysed crudes);

• t is the disturbance vector.

7Z α test is similar to typical ADF tests, i.e. it is also based on residuals from level estimation. However it has

slower rate of divergence and better small-sample properties, i.e. higher power - Phillips & Ouliaris (1990).

8

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 9/18

The VAR model was used to confirm the results of the test for cointegration with the help of

eigenvalue and trace tests - i.e. rejection of the null of r = 0 and failure to reject r ≤ 1 and r ≤ 2.

This should be interpreted as a confirmation that the relationship between retail prices, crude oil

prices and exchange rate is not spurious.

The only remaining part is to establish the direction of the transmission and its properties. As

the next step, (2) was transformed into the VECM model.

∆zt = Πzt−1 − p−1

i=1

Γi∆zt−i + t (3)

where:

• Π = B(1);

• Γi = − p

i+i Γi.

For the purposes of this study specified in the Section 1 it is necessary to examine the properties

of the Π matrix, which contains the information about the dynamic stability of the system. After

ascertaining the presence of one cointegrating vector in the system, the matrix in question can be

normalised and re-written as Π = αβ . In this setting, β contains the cointegrating vector and α

represents the speed of adjustment from the errors (β zt−1) towards the long-run equilibrium. If the

coefficient is zero in the particular equation, that variable is considered to be weakly exogenous, i.e.

determined outside the system and setting the retail prices.

In order to test the hypothesis of weak exogeneity of the crude oils, the α vector was constrained

to have zero values for crude oil and the exchange rate and then the χ2 tests were performed. The

results are depicted in Figures 3-6. The colours indicate the cases when the null of exogeneity of a

given crude oil and exchange rate was rejected.8

8Markets with no data are marked as NAs, while those for which the null of no-cointegration was not rejected are

marked as spurious.

9

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 10/18

3 Discussion of Results

The results indicate that within the EU, the national markets could be generally split into three major

groups: East, Mediterranean and North-West. This intuitively reflects the state of the infrastructure

and geographical accessibility to different crudes and transportation routes (for landlocked countries).

Furthermore, at the product level, the results could be divided into two groups - those for popular

and requiring high-quality crude products (unleaded petrol, diesel and low-sulphur fuel oil) and those

for niche products which could be obtained from lower quality crudes (leaded petrol, high-sulphur

fuel oil and heating oil). LPG seems to behave in a different manner from the other products which

might reflect the fact that it is often obtained from natural gas in addition to crude oil.

3.1 Long Run Relationship

The results of the Phillips-Perron Z α and Johansen procedure indicate that the product prices in the

old EU-15 countries in the North-West Europe are in a long-run relationship with prices of all crude

oils. This indicates that those markets are well integrated with the global energy markets and the

infrastructure (pipelines, tanker off-loading ports, etc.).

Conversely, product prices in the new-EU countries do not have a long run relationship with

crude oil markets (this applies mainly to diesel and unleaded petrol) or are in the relationship only

with the low-quality Russian crude oil. This seems to be confirmed by the results obtained for

less-environmentally-friendly products (high sulphur oils) which are easier to obtain from low-quality

products. Failure to reject the null of no cointegration in some cases might be due either to short

samples (unfortunately, earlier data is not available), or to the fact that on those markets prices

are still heavily regulated and controlled by the state-owned monopolies. The situation from the

countries in the Mediterranean is more complicated - in many cases they are cointegrated only with

Ural oil, as this crude can be readily transported from Russia.

In terms of different products, the common wisdom is also confirmed - the most popular products

follow crude oil prices quite closely, while less popular, lower quality products are either linked to

10

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 11/18

low quality crude (Urals) or do not cointegrate at all.

3.2 Endogeneity of Crudes

Results of the tests for the null of crude oil and the exchange rate exogeneity are also intuitive. Brent

and WTI are global high quality crudes, which lead the global markets and are commonly used as

reference worldwide. As such they are exogenous in all markets in which they are cointegrated with

retail products.

The results for Ural crude are more surprising and possibly of some importance to energy

economists and policy makers. The failure to reject the null of exogeneity of Ural crude indicates

that prices of that crude are influenced by the retail prices and those series are in bi-directional

relationship. This indicates that local retail market condition do play an important role in local

crude oil markets. Given that, any simplification based on the assumption that upstream prices can

be perfectly proxied by global benchmarks should be treated with caution. Perhaps of even greater

importance is the fact that macro-models involving local product prices (such as inflation models)

should be revisited and the bi-directional feedback crude oil - retail products should be taken into

account.

4 Conclusions and Suggestions for Further Research

The results obtained indicate that the crude oil - retail product linkages present in the EU energy

markets are far from being simple and uniform. In particular, they confirm the common wisdom

that those linkages depend on availability of crude oil and that for some local crudes the relationship

might be bi-directional.

Obviously, the results should be further confirmed with the help of higher-frequency data, possibly

split between local wholesale markets and other transmission tiers. In particular, the analysis of

transmission involving some middle pricing tiers (global spot and national wholesale) could shed

even more light on this interesting issue. Accordingly, more sophisticated models (in particular those

11

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 12/18

involving all products being modelled in a single framework) should be utilised.

References

Adrangi, B., Chatrath, A., Raffiee, K. & D Ripple, R. (2001), ‘Alaska north slope crude oil price andthe behavior of diesel prices in california’, Energy Economics 23(1), 29–42.

Arpa, M., Gnan, E. & Antoinette, M. (2005), ‘Oil price shock, energy prices and inflation - acomparison of austria and the eu’.

Asche, F., Gjolberg, O. & Volker, T. (2003), ‘Price relationships in the petroleum market: an analysisof crude oil and refined product prices’, Energy Economics 25(3), 289–301.

Bacon, R. & Tordo, S. (2005), ‘Crude oil price differentials and differences in oil qualities: A statisticalanalysis’.

Bahree, B. & Gold, R. (2006), ‘Saudi heavy oil may help in global energy crunch’, The Wall Street Journal Europe 24(111), 1–2.

Bewley, R. & Fiebig, D. (1990), ‘Why are long-run parameter estimates so disparate?’, The Review

of Economics and Statistics 72(2), 345–349.

Energy Information Agency (1999), ‘Price changes in the gasoline market: Are midwestern gasolineprices downward sticky?’, DOE (626), 55+.

Energy Intelligence Group (2004), The International Crude Oil Market Handbook , Energy IntelligenceGroup.

Engle, R. & Granger, C. (1987), ‘Cointegration and error correction: Representation estimation andtesting’, Econometrica 55(2), 251–276.

Eni SpA (2006), World oil & gas review 2006, Technical report, Eni SpA.

Frey, G. & Manera, M. (2005), Econometric models of asymmetric price transmission, WorkingPapers 2005.100, Fondazione Eni Enrico Mattei.

Gjolberg, O. & Johnsen, T. (1999), ‘Risk management in the oil industry: can information on long-run equilibrium prices be utilized?’, Energy Economics 21(6), 517–527.

Hagstromer, B. & Wlazlowski, S. (2007), ‘Causality in crude oil markets’, Aston University Working Papers.

Krichenel, N. (2005), ‘Simultaneous equations model for world crude oil and natural gas markets.imf workig paper: African department’, International Monetary Fund. February .

Lanza, A., Giovannini, M. & Manera, M. (2003), Oil and product price dynamics in internationalpetroleum markets, Technical report, Fondazione Eni Enrico Mattei.

Maddala, G. & Kim, I. (1999), Unit Roots, Cointegration, and Structural Change, Cambridge Uni-versity Press.

McQuilling Services, LLC (2006), Imo 13h marpol regulation, Commercial offer, McQuilling Services,LLC. available at www.meglobaloil.com/MARPOL.pdf.

Meyer, J. & Cramon-Taubadel, S. v. (2004), ‘Asymmetric price transmission: A survey’, Journal of

Agricultural Economics 55(3), 581–611.

12

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 13/18

Montepeque, J. (2005), ‘Sour crude pricing: A pressing global issue’, Middle East Economic Survey .

Natural Resources Canada (2005), Overview of the canadian downstream petroleum industry, Tech-nical report, Oil Division, Natural Resources Canada.

OPEC (2005), ‘Monthly oil market report august 2005’.

Phillips, P. C. B. & Ouliaris, S. (1990), ‘Asymptotic properties of residual based tests for cointegra-

tion’, Econometrica 58(1), 165–93.

Platt’s (1999), ‘Platt’s oil guide to specifications’.

Platt’s (2006), ‘Crude oil price discovery turns sour’, Platt’s Energy Economist .

Platt’s (2007), ‘Methodology and specifications guide - crude oil’.

van den Berg, F., Kapusta, S., Ooms, A. & Smith, A. (2003), ‘Fouling and compatibility of crudesas basis for a new crude selection strategy’, Petroleum Science and Technology 21(3), 557–568.

13

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 14/18

Figure 2: Prices of Crude Oils Analysed

14

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 15/18

Figure 3: Unleaded Petrol and Diesel - Endogeneity

15

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 16/18

Figure 4: Leaded Petrol and Heating Oil - Endogeneity

16

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 17/18

Figure 5: Fuel Oil - Endogeneity

17

8/3/2019 Article Final Ver 1

http://slidepdf.com/reader/full/article-final-ver-1 18/18

Figure 6: LPG - Endogeneity