max ginsburg, - luc.sinegre.free.frluc.sinegre.free.fr/psi/sujetsynthesedebt.pdf · ! 1! epreuve...

TRANSCRIPT

1

EPREUVE TYPE CENTRALE-SUPELEC 4 HEURES Vous rédigerez en anglais et en 500 mots environ une synthèse des documents proposés. Vous indiquerez avec précision à la fin de votre synthèse le nombre de mots qu’elle comporte. Un écart de 10% en plus ou en moins sera accepté. Votre travail comportera un titre comptabilisé dans le nombre de mots.

Ce sujet propose les 4 documents suivants :

− Un tableau de Max Ginsburg ; − Un extrait du livre Payback (Debt and the Shadow Side of Wealth) de Margaret Atwood, publié en

2008; − “The Story of Our Time”, article paru en avril 2013 dans The New York Times ; − “After austerity, what?”, article paru le 4 mai 2013 dans The Economist.

Document 1

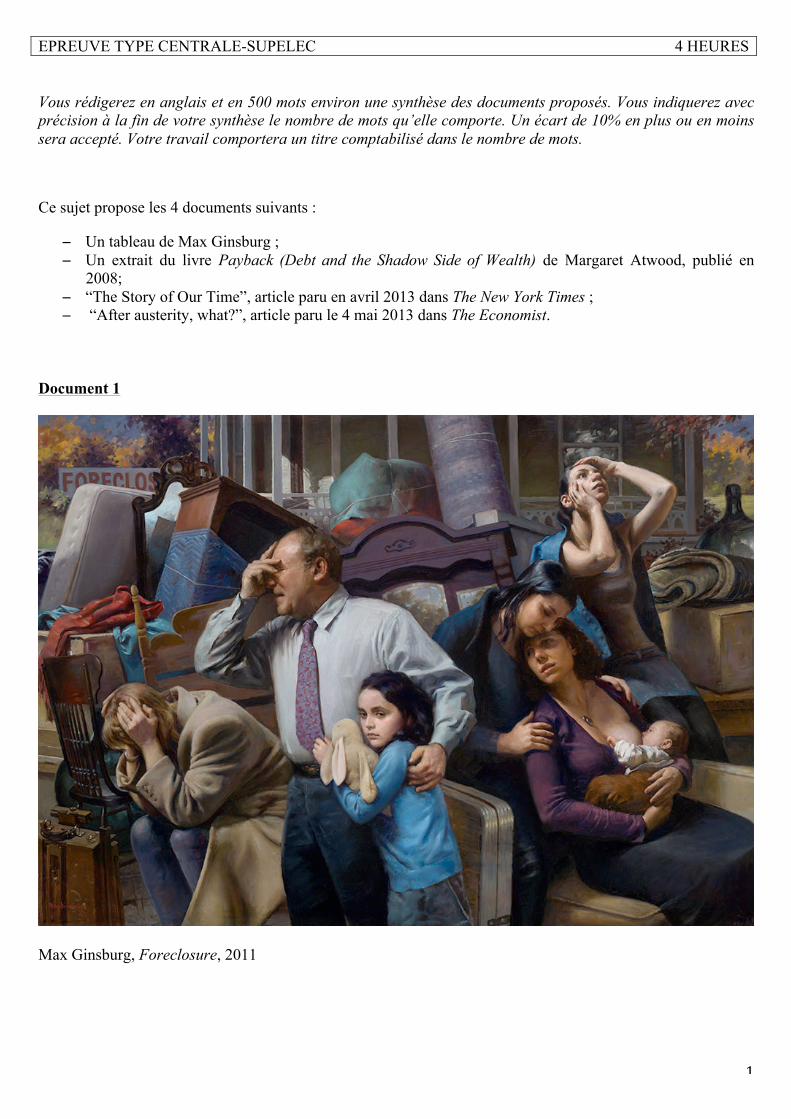

Max Ginsburg, Foreclosure, 2011

2

Document 2

Debt as plot Without memory, there is no debt. Put another way: without story, there is no debt. A story is a string of actions occurring over time – one damn thing after another, as we glibly say in creative writing classes – and debt happens as a result of actions occurring over time. Therefore, any debt involves a plot line: how you got into debt, what you did, said, and thought while you we're in there, and then, - depending on whether the ending is to be happy or sad - how your got out of debt, or else how you got further and further into it until you became overwhelmed by it, and sank from view. The hidden metaphors are revealing: we get "into" debt, as if into a prison, swamp, or well, possibly a bed; we get "out" of it, as if coming into the open air or climbing out of a hole. If we are "overwhelmed" by debt, the image is possibly that of a foundering ship, with the sea and the waves pouring inexorably on top of us as we flail and choke. All of this sounds dramatic, with much physical activity: jumping in, leaping or clambering out, thrashing around, drowning. Metaphorically, the debt plot line is a far cry from the glum actuality, in which the debtor sits at a desk fiddling around with numbers on a screen, or shuffles past-due bills in the hope that they will go away, or paces the room wondering how he can possibly extricate himself from the fiscal molasses. In our minds - as reflected in our own language - debt is a mental or spiritual non-place, like the Hell described by Christopher Marlowe's Mephistopheles when Faust asks him why he's not in Hell but right there in the same room as Faust. "Why, this is Hell, nor am I out of it," says Mephistopheles. He carries Hell around with him like a private climate: he's in it and it's in him. Substitute "debt" and you can see that, in the way we talk about it, debt is the same kind of placeless place. "Why, this is Debt, nor am I out of it," the beleaguered debtor might similarly declaim. Which makes the whole idea of debt - especially massive and hopeless debt - sound brave and noble and interesting rather than merely squalid, and gives it a larger-than-life tragic air. Could it be that some people get into debt because, like speeding on a motorbike, it ads an adrenaline hit to their otherwise humdrum lives? When the bailiffs are knocking at the door and the lights go off because you didn't pay the hydro and the bank's threatening to foreclose, at least you can't complain of ennui. Scientists tell us that rats, if deprived of toys and fellow rats, will give themselves painful electric shocks rather than endure prolonged boredom. Even this electric shock self-torture can provide some pleasure, it seems: the anticipation of torment is exciting in itself, and there's the thrill that accompanies risky behaviour. But more importantly, rats will do almost anything to create events for themselves in an otherwise eventless time-space. So will people: we not only like our plots, we need our plots, and to some extent we are our plots. A story-of-my-life without a story is not a life. Margaret Atwood, Payback (Debt and the Shadow Side of Wealth), 2008 Document 3

The Story of Our Time

Those of us who have spent years arguing against premature fiscal austerity have just had a good two weeks. Academic studies that supposedly justified austerity have lost credibility; hard-liners in the European Commission and elsewhere have softened their rhetoric. The tone of the conversation has definitely changed. My sense, however, is that many people still don’t understand what this is all about. So this seems like a good time to offer a sort of refresher on the nature of our economic woes, and why this remains a very bad time for spending cuts. Let’s start with what may be the most crucial thing to understand: the economy is not like an individual family. Families earn what they can, and spend as much as they think prudent; spending and earning opportunities are two different things. In the economy as a whole, however, income and spending are interdependent: my spending is your income, and your spending is my income. If both of us slash spending at the same time, both of our incomes will fall too. And that’s what happened after the financial crisis of 2008. Many people suddenly cut spending, either because they chose to or because their creditors forced them to; meanwhile, not many people were able or willing to

3

spend more. The result was a plunge in incomes that also caused a plunge in employment, creating the depression that persists to this day. Why did spending plunge? Mainly because of a burst housing bubble and an overhang of private-sector debt — but if you ask me, people talk too much about what went wrong during the boom years and not enough about what we should be doing now. For no matter how lurid the excesses of the past, there’s no good reason that we should pay for them with year after year of mass unemployment. So what could we do to reduce unemployment? The answer is, this is a time for above-normal government spending, to sustain the economy until the private sector is willing to spend again. The crucial point is that under current conditions, the government is not, repeat not, in competition with the private sector. Government spending doesn’t divert resources away from private uses; it puts unemployed resources to work. Government borrowing doesn’t crowd out private investment; it mobilizes funds that would otherwise go unused. Now, just to be clear, this is not a case for more government spending and larger budget deficits under all circumstances — and the claim that people like me always want bigger deficits is just false. For the economy isn’t always like this — in fact, situations like the one we’re in are fairly rare. By all means let’s try to reduce deficits and bring down government indebtedness once normal conditions return and the economy is no longer depressed. But right now we’re still dealing with the aftermath of a once-in-three-generations financial crisis. This is no time for austerity. O.K., I’ve just given you a story, but why should you believe it? There are, after all, people who insist that the real problem is on the economy’s supply side: that workers lack the skills they need, or that unemployment insurance has destroyed the incentive to work, or that the looming menace of universal health care is preventing hiring, or whatever. How do we know that they’re wrong? Well, I could go on at length on this topic, but just look at the predictions the two sides in this debate have made. People like me predicted right from the start that large budget deficits would have little effect on interest rates, that large-scale “money printing” by the Fed (not a good description of actual Fed policy, but never mind) wouldn’t be inflationary, that austerity policies would lead to terrible economic downturns. The other side jeered, insisting that interest rates would skyrocket and that austerity would actually lead to economic expansion. Ask bond traders, or the suffering populations of Spain, Portugal and so on, how it actually turned out. Is the story really that simple, and would it really be that easy to end the scourge of unemployment? Yes — but powerful people don’t want to believe it. Some of them have a visceral sense that suffering is good, that we must pay a price for past sins (even if the sinners then and the sufferers now are very different groups of people). Some of them see the crisis as an opportunity to dismantle the social safety net. And just about everyone in the policy elite takes cues from a wealthy minority that isn’t actually feeling much pain. What has happened now, however, is that the drive for austerity has lost its intellectual fig leaf, and stands exposed as the expression of prejudice, opportunism and class interest it always was. And maybe, just maybe, that sudden exposure will give us a chance to start doing something about the depression we’re in. By Paul Krugman, The New York Times, April 28th, 2013 Document 4 Charlemagne After austerity, what? LIKE France’s François Hollande a year ago, Italy’s Enrico Letta rushed to Berlin immediately after taking power, and with a similar message: Italy would respect fiscal discipline, but Europe must do more to promote growth. “If Europe stands only for negative news, for austerity, then we’ll see more of these movements against Europe,” he told Angela Merkel. Italy’s new prime minister did not explain how he would pay for expensive promises to cut taxes and expand welfare. Nor did he spell out exactly what he wanted Europe to do. What is clear is that the backlash against austerity has become intense: even Ireland’s president, Michael Higgins, has joined in. The big danger is that, in the clamour for relief from self-destructive policies, countries will give up on the painful structural reforms they need. For all the hopeful signs of “rebalancing” within the euro zone, the economies of southern Europe are still

4

shrinking. Europe’s single market belies its name when smaller firms in southern Europe must pay far higher interest for loans than German competitors, if they can get credit at all. Forecasts by the European Commission, due this week, will be gloomy. On the eve of Labour Day, Eurostat reported that unemployment in the euro zone had risen to 12.1%. In Greece and Spain, three out of five people under 25 are now jobless. Austerity has also suffered a double academic blow. IMF economists admitted that the recessionary impact of austerity was more severe than they thought. Then economists at the University of Massachusetts, Amherst, found mistakes and questioned the data and assumptions in a piece of research by Kenneth Rogoff and Carmen Reinhart suggesting that a country’s growth slows down markedly once its public debt rises above 90% of GDP. José Manuel Barroso, president of the European Commission, made a half-admission of defeat when he said austerity was reaching its limits. “A policy, to be successful, not only has to be properly designed; it has to have the minimum of political and social support.” Or as Mr Letta put it more pithily to the Italian parliament, “budget consolidation alone will kill Italy.” What might replace the current policy is less clear. The obvious trade-off is to go more slowly on deficit-cutting and faster on structural reforms, especially when political capital is limited. The IMF pushed for such a mix from the outset. It would be especially sensible for such countries as Italy and Portugal, which stopped growing long before the euro crisis: in effect, they are suffering the bust without ever having enjoyed the boom. Yet austerity is not about to end. For countries in bail-out programmes, less of it means asking creditors for bigger loans (or a debt write-off). And nobody seriously suggests fiscal stimulus: the only question is how far deficit-cutting should be slowed. The commission (with Germany’s nod) has become readier to allow countries to delay meeting fiscal targets in the face of recession. The Netherlands should get another year, Spain another two. Even Mr Letta says he still wants to bring Italy’s deficit below 3% of GDP this year. That would release Italy from the EU’s “excessive deficit procedure” and, to an extent, from German tutelage. France will be a test-case. It is likely to get another year to meet its target, in exchange for a promise of more structural reforms. In June EU leaders will discuss the idea of countries signing binding “contracts” for reform, perhaps backed by the offer of more money. Yet shifting the focus may be harder than it looks. “Structural reform” is a broad term. Each country needs a different mix. Enacting legislation is not the same as implementing it. Reforms tend to increase short-term pain, while the benefits do not come through immediately. The OECD, a rich-world think-tank, argues that troubled euro-zone countries have made the most progress in enacting reform. Even so, several have a lot more to do to make labour and product markets more flexible, to boost productivity and to create efficient public administration. Structural reforms are hard to measure. But one fact is telling: unit-labour costs in southern Europe are falling, yet even in the region’s worst post-war slump inflation has mostly been higher than in Germany. This amounts to a double assault on citizens: they have not only lost jobs and benefits, but are seeing higher prices. Governments have found it easier to cut deficits than take on obstreperous unions and vested business interests. Take Greece: it has cut deficits more than anyone else, but only this week, in the sixth year of recession, did it pass a law to allow incompetent civil servants to be fired more easily. Or look at Italy: its technocratic prime minister, Mario Monti, forced through more austerity, but his plan to simplify the sacking of workers was watered down. One underlying problem is dysfunctional politics: countries that got into trouble because they could not reform in the good times are still struggling in bad ones. The north must reform too Keynes’s dictum that the time for austerity is during a boom, not a bust, also applies to structural reform. But crisis is often needed to force change. The case for relaxing austerity should not hide the need for big reform. And reform should not be limited to the euro-zone periphery. Germany can do more, even without a spending spree. Just liberalising Sunday shopping could boost domestic demand. Across Europe, deepening the single market, particularly in services, would help kindle growth. Fixing the euro zone’s banks so they can resume lending also requires Germany to stop blocking the creation of a full banking union. And this means being ready to share the risks of other countries’ banks. Without this, Germany faces an even bigger risk: that the euro zone collapses because political resentment pulls it apart. Rules alone will kill Europe. The Economist, May 4th 2013