green bonds: an alternative source of financing in the era

TRANSCRIPT

Master’sDegreein

ManagementAccountingAndFinance

FinalThesis

GreenBonds:

analternativesourceoffinancingintheEraofClimateChange

SupervisorCh.Prof.GloriaGardenalAssistantsupervisorCh.Prof.FedericoBeltrameGraduandNicolòRossittoMatricolationnumber852523AcademicYear2019/2020

CONTENTS

INTRODUCTION..................................................................................................................................................1

1.CHAPTER:CLIMATECHANGE.................................................................................................................4

1.1RiodeJaneiro1992...............................................................................................................................5

1.2KyotoProtocol........................................................................................................................................6

1.3DevelopmentaftertheKyotoProtocol:TheSternReview..................................................7

1.4TheCopenhagenAgreement.............................................................................................................8

1.5TheCOP21(ParisAgreement)........................................................................................................9

1.5.1TheINDCs.......................................................................................................................................10

1.6SustainableDevelopmentGoals(SDGs).....................................................................................13

1.7MitigationandAdaptation...............................................................................................................15

1.7.1EnergySector................................................................................................................................18

1.7.1.1GSEIncentive........................................................................................................................20

1.8.ClimateChangeandCOVID-19......................................................................................................21

2.CHAPTER:CLIMATEFINANCE..............................................................................................................25

2.1Low-CarbonEconomyTransition.................................................................................................26

2.2ClimateFinanceActors......................................................................................................................30

2.2.1PublicFinanceActors................................................................................................................32

2.2.1.1FinancingSustainableGrowthandTheGreenDeal............................................33

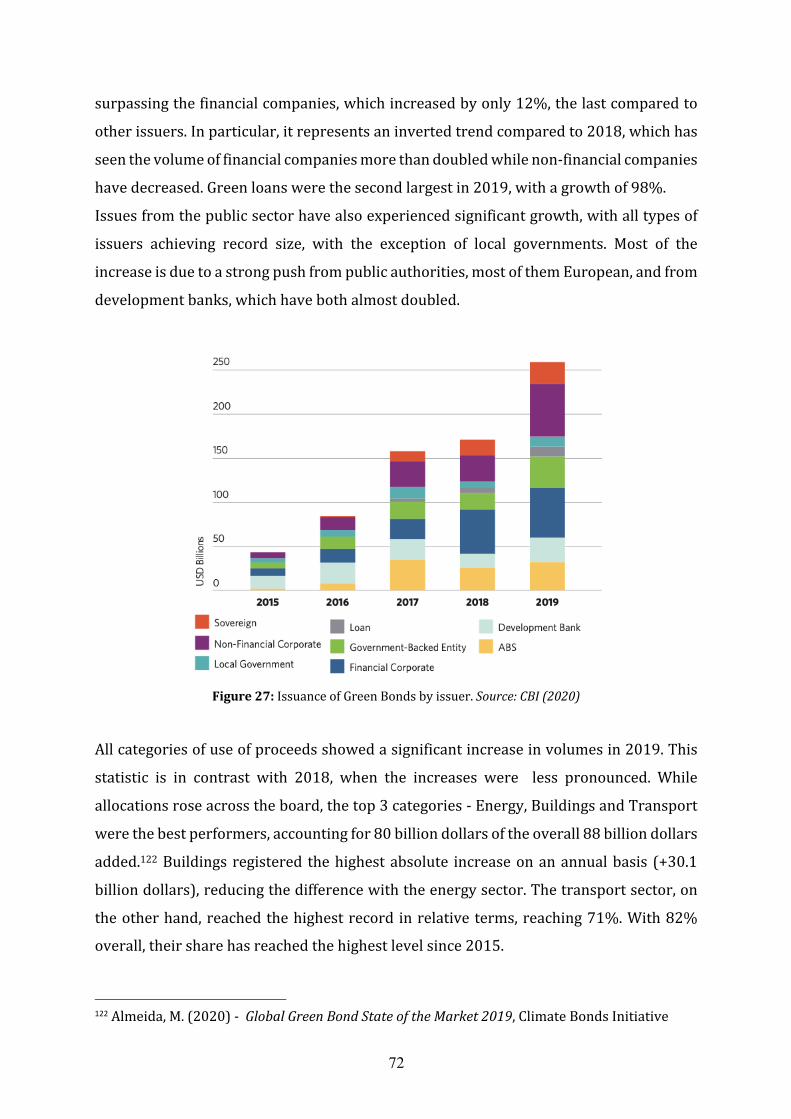

2.2.2PrivateFinanceActors..............................................................................................................37

2.2.3TheimportanceofPublicandPrivaterelationship......................................................38

2.2.3.1BlendedFinance..................................................................................................................39

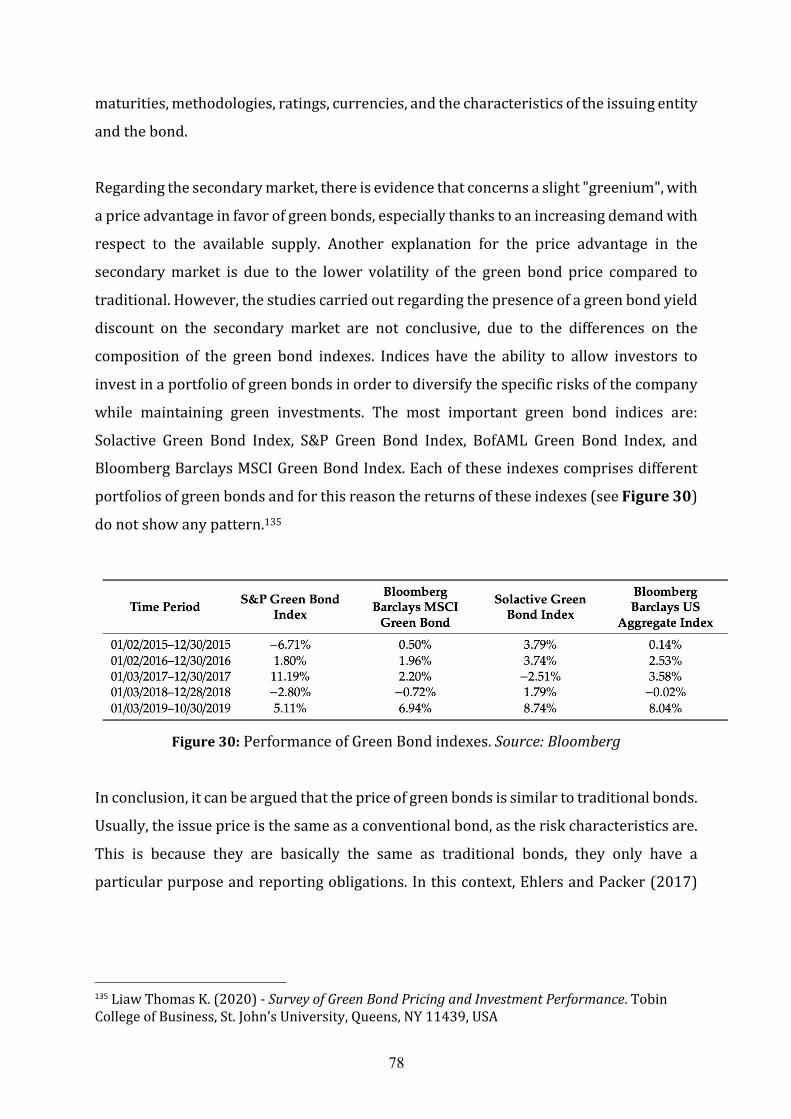

2.3ClimateFinanceInstruments..........................................................................................................43

2.3.1FinancialInstrumentstoRaiseFunds................................................................................44

2.3.1.1GreenBonds..........................................................................................................................45

2.3.1.2ClimatePolicyPerformanceBonds.............................................................................45

2.3.1.3CatastropheBonds.............................................................................................................47

2.3.1.4DebtforClimateSwaps....................................................................................................49

2.3.2FinancialInstrumentstoDeployFunds............................................................................51

2.3.2.1CapitalInstruments...........................................................................................................51

2.3.2.1.1DebtFinance.................................................................................................................52

2.3.2.1.1EquityFinance.............................................................................................................53

2.3.2.2RiskManagementInstruments.....................................................................................55

2.4SustainableFinanceandCovid-19...............................................................................................56

3.CHAPTER:GREENBONDS.......................................................................................................................59

3.1WhatisaBond......................................................................................................................................59

3.2TheGreenBonds..................................................................................................................................61

3.2.1GreenBondsPrinciplesandClimateBondsStandard................................................63

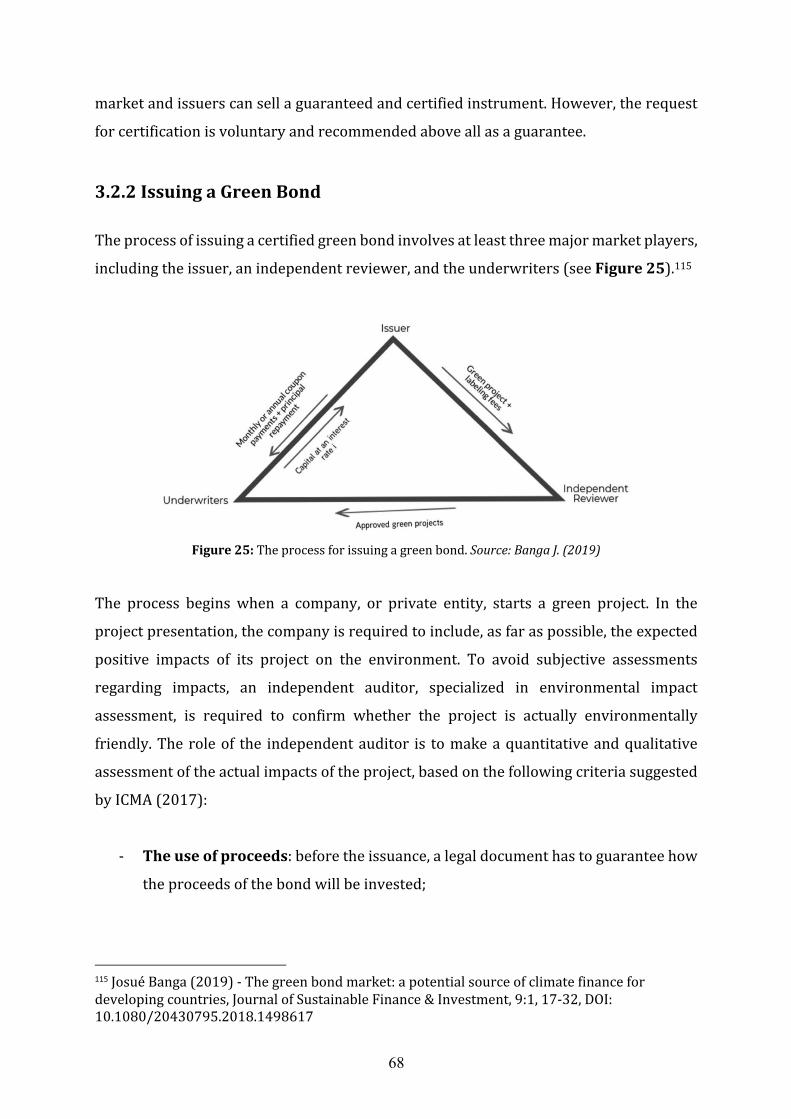

3.2.2IssuingaGreenBond.................................................................................................................68

3.3GreenBondMarket.............................................................................................................................69

3.3.1Developmentofthelastyears...............................................................................................70

3.4CharacteristicsofGreenBonds......................................................................................................74

3.4.1The“greenium”ofGreenBonds...........................................................................................76

3.5GreenBondMarketinItaly.............................................................................................................79

3.5.1ExampleofGreenBond–EnelS.p.A...................................................................................80

4.CHAPTER:GREENBONDS:ANALTERNATIVESOURCEOFFINANCING?AN

EMPIRICALEVIDENCE...................................................................................................................................84

4.1ProjectFinance.....................................................................................................................................84

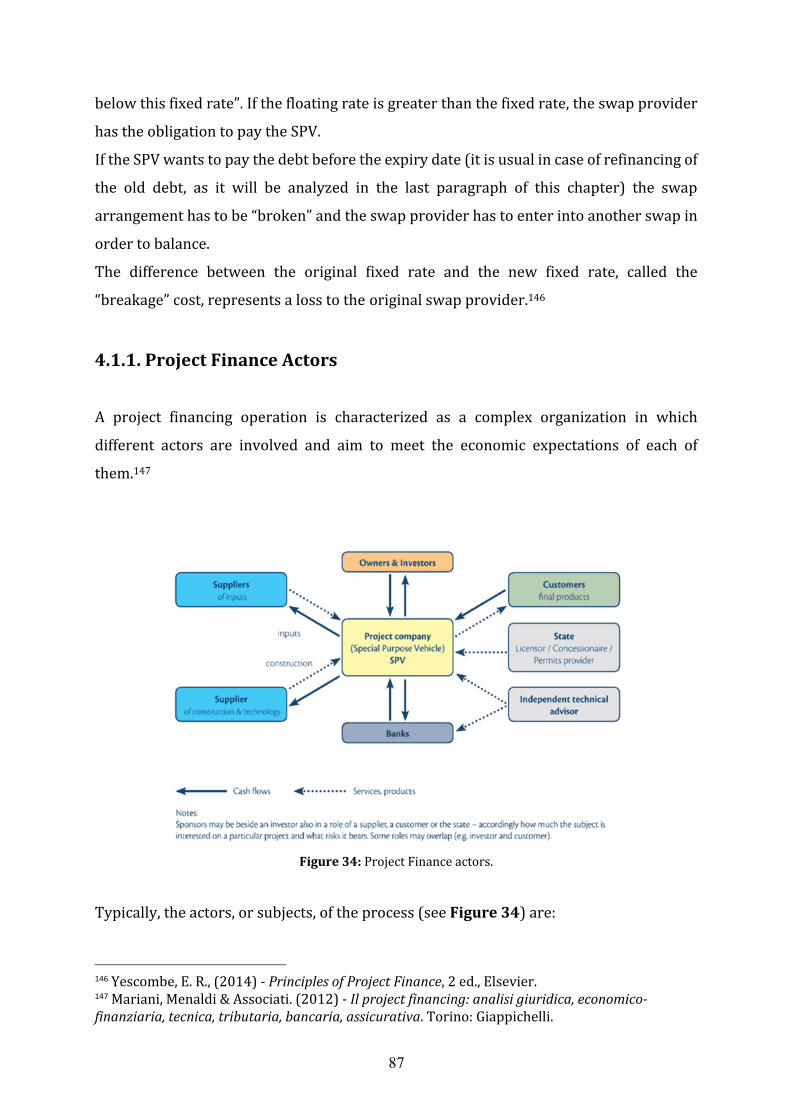

4.1.1.ProjectFinanceActors.............................................................................................................87

4.1.2TypicalProjectFinanceTransaction..................................................................................90

4.1.3ProjectValuation.........................................................................................................................92

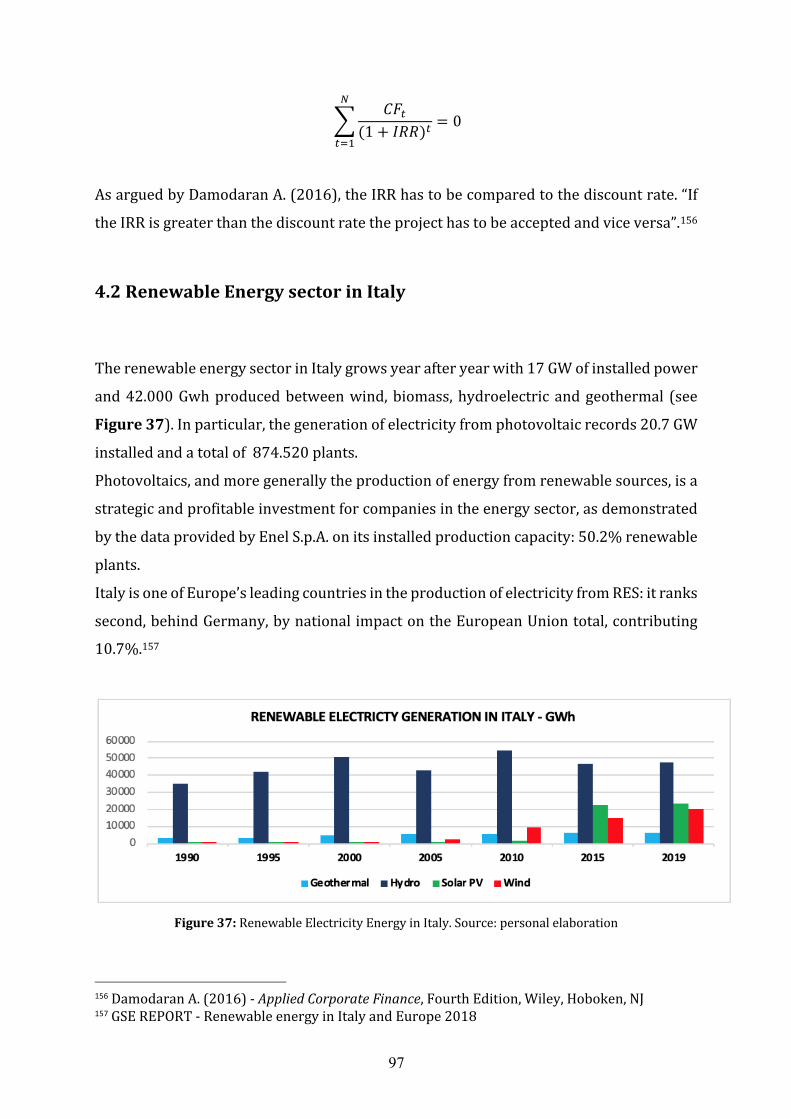

4.2RenewableEnergysectorinItaly.................................................................................................97

4.3GreenBondsvsProjectFinance:anempiricalevidence.................................................100

4.3.1LiteratureReview....................................................................................................................100

4.3.2EmpiricalAnalysis...................................................................................................................103

4.3.2.1Methodology......................................................................................................................104

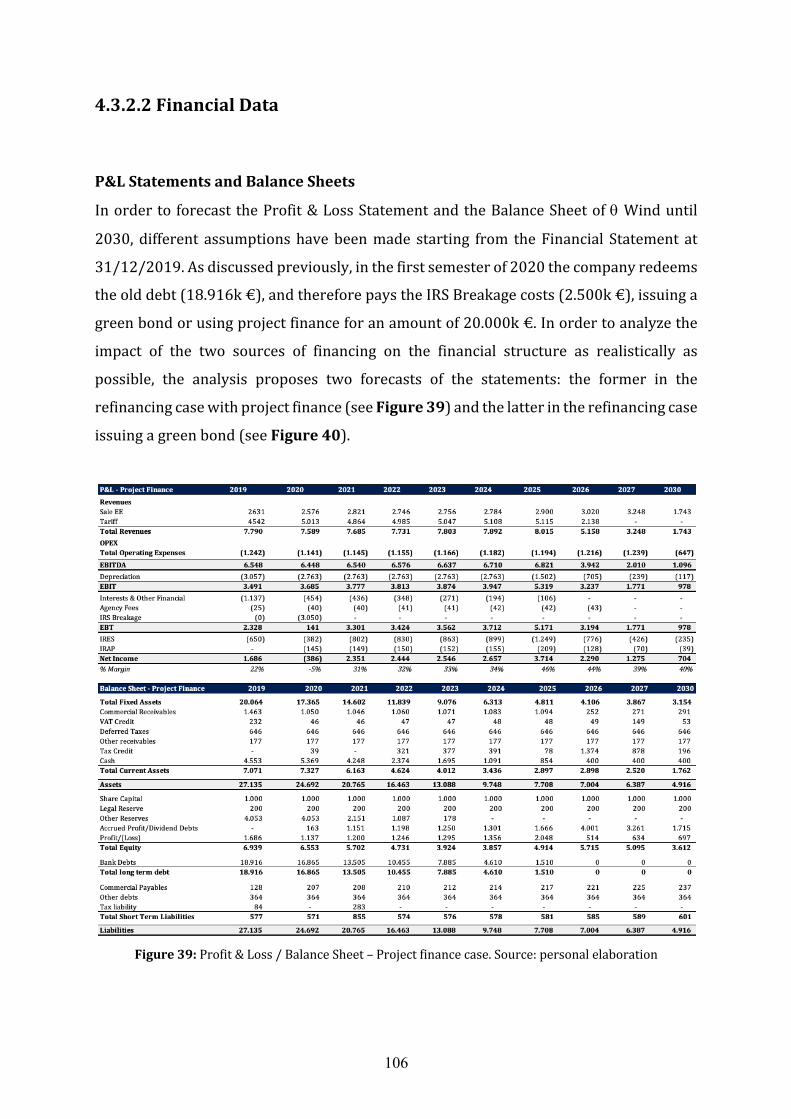

4.3.2.2FinancialData....................................................................................................................106

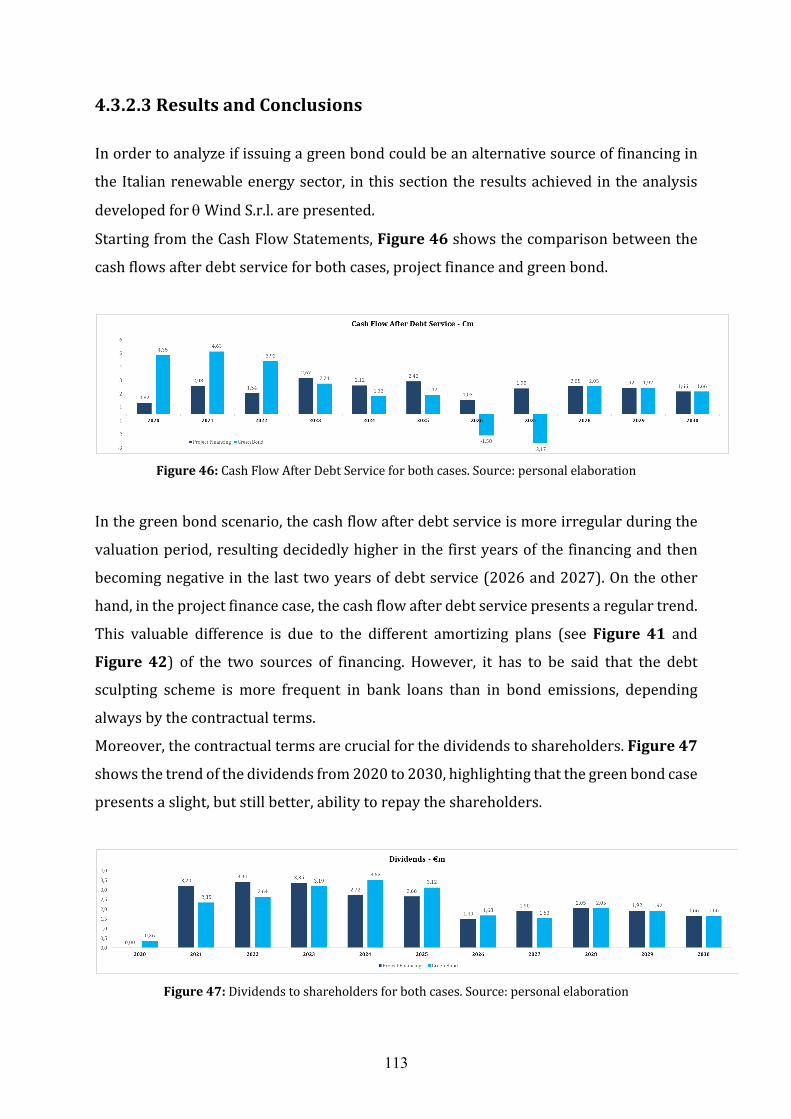

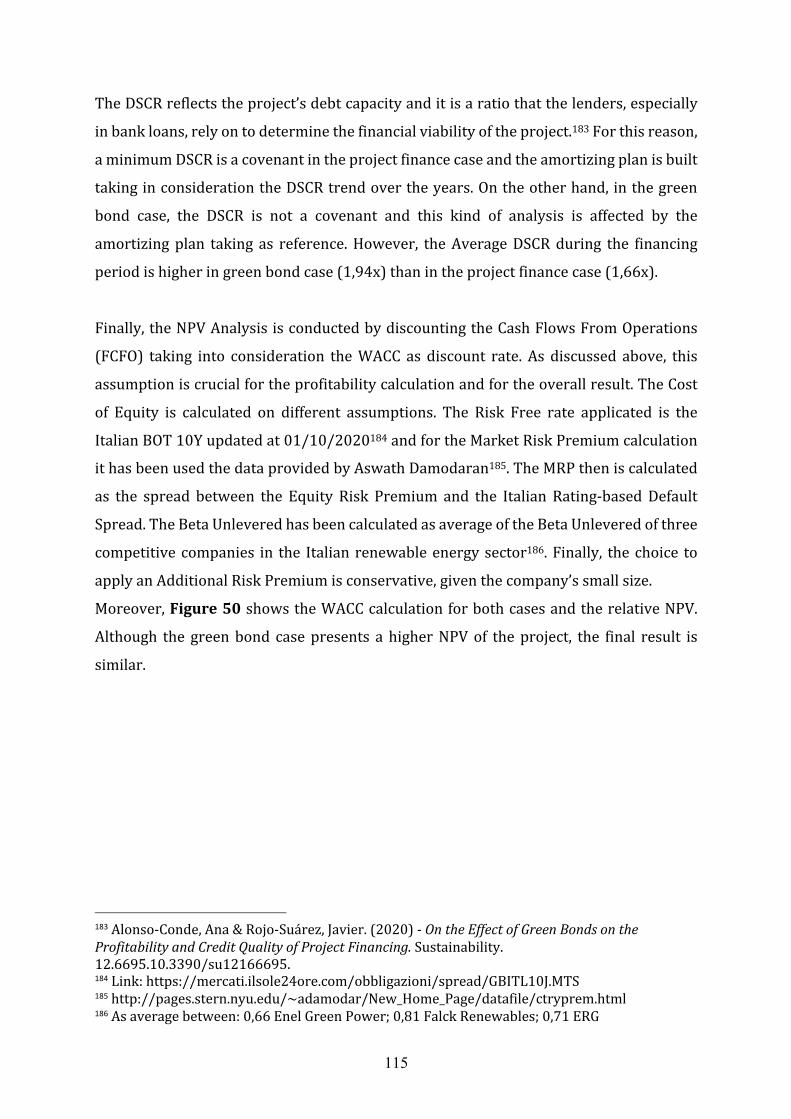

4.3.2.3ResultsandConclusions...............................................................................................113

CONCLUSIONS................................................................................................................................................117

REFERENCES...................................................................................................................................................121

1

INTRODUCTION Attheendof2007agroupofSwedishpensionfundshadtheintuitiontoinvestinclimate

friendlyprojects.Theydidnotknowhowtoinvestingreenprojectsandtheyaskedtothe

WorldBankforsupport.Ayearlater,in2008,theWorldBankissueditsfirstgreenbond,

introducinganewtoolinthemarketthatallowedfinancialinvestorsandprojectstojoin

forcesagainstclimatechange.

Theobjectof this thesis is tostudyandshed lightonan innovative tool:greenbonds.

Climatechangeisthereasonbehindthebirthofthesenewgreenfinancialinstruments,

highlighting the global need of stimulating financial investors towards environmental

sustainability projects, thus avoiding the need to allocate resources on projects that

producehighCO2emissionsandgreenhousegases.

The purpose of green bonds is therefore a kind ofwin-win strategy,where investors

increasetheirprofitsand,atthesametime,individualgovernmentsareabletocomply

with theParisAgreement guidelines. In this context, energy industryplays a key role

againstclimatechange.Infact,theenergytransitionaimstoshiftfromfossilfuel-centered

energytoacarbon-neutralone,basedprimarilyonrenewablesources.Renewableenergy

isplacedatthefoundationofthethesis,highlightinghowtheissuanceofgreenbondscan

facilitatetheenergytransitioninItaly.

After having extensively studied climate change, climate finance and green bonds in

general,theobjectiveofthisthesisistoanalyzewhethertheissuanceofagreenbondin

the renewable energy market can be a viable alternative to conventional sources of

financing used in Italy such as project finance, from a shareholder perspective. In

particular,theanalysisisconductedonthedebtrefinancingofahypotheticalcompany

that has awind farm located in Italy as its core asset. Through the construction of a

financial model, the 10-year financial statements forecast of the company will be

proposed,assumingtwodifferentscenarios:thefirstonewitharefinancingusingproject

financeandthesecondoneissuingagreenbond.Theproposedanalysisdoesnotaimat

statingageneralandunivocalresultbutrathertofosterfurtherfutureresearchonthe

topic.

2

Themotivation behind this thesis is the desire of inspiring the new generations to a

greater sensitivity around climate change, trying to combine both economic and

environmentalinterests.Climatechangeisnowanacknowledgedproblem,asitisthekey

roleplayedbyeconomicsandfinanceinthefutureofourplanet.TheCovid-19pandemic

crisismustbeconsideredasawake-upcall. In fact, ithasshownthathumansarenot

invincibleand,onthecontrary,theyarevulnerablewithoutacommonglobaleffort.Inthe

financial field, green bonds represent the viable way to move from the profit

maximizationparadigmtoamoresustainableandfairerfuture.Thesymbolthatthose

instrumentsrepresent insectorswhereprofitmaximizationhasalwaysbeenthemain

goalisthemainreasonbehindthisresearch.

Thestructureofthisthesisisdesignedtograduallyintroducegreenbonds,starting,as

mentioned above, from its roots in climate change, exploring similar instruments of

climatefinanceandfinallydemonstratingempiricallyhowtheycanbeaviablealternative

toprojectfinanceintherenewableenergymarketinItaly.

Thechapterswillbeorganizedasfollows.

Chapter 1 introduces the climate change issue, highlighting themain global warming

causes. The chapter is focused on howmodern society has dealtwith climate change

throughouthistory,fromthefirstconferenceinRiodeJaneiroin1992,throughtheKyoto

Protocolin1997,theCopenhagenAgreementin2009,andfinallywiththemostimportant

agreement,theParisAgreementin2015.Thefinalpartofthechapterisdedicatedtothe

description of the SDGs (Sustainable Development Goals) and the importance of the

energysectorinthefightagainstclimatechange.Inaddition,afinalparagraphdiscusses

therelationshipbetweenclimatechangeandtheCovid-19pandemic.

Chapter2isdedicatedtothedescriptionofclimatefinance.Inparticular,thefirstpartof

the chapter focuses on the low-carbon transition, highlighting the public and private

actors in climate finance and how the relationship between public and private is

fundamentalintheenergytransition.Thesecondpartofthechapterfocusesonclimate

finance instruments, fromthe instrumentstoraise funds(GreenBonds,ClimatePolicy

PerformanceBonds,CatastropheBondsandDebtforClimateSwaps)totheinstruments

todistributefunds(CapitalInstrumentsandRiskManagementInstruments).Finally,the

finalpartdiscussestheconsequencesofclimatefinanceaftertheCovid-19pandemic.

3

Chapter 3 is entirely focused on describing green bonds, highlighting how these

innovativeinstrumentswork.Inaddition,itoutlinestheGreenBondPrinciplesandthe

GreenBondStandards,whicharethekeyelementsinthegreenbondsclassificationand

categorization.Moreover,thedevelopmentsinrecentyearshaveshowedhowtheiruse

has grown exponentially in the current decade. Finally, the last part of the chapter is

dedicatedtothecharacteristicsofgreenbonds,theso-called"greenium"andafinalfocus

onthegreenbondmarketinItaly,supportedbytheexampleofthegreenbondissuedby

EnelS.p.A.

Chapter4proposesanempiricalanalysisabouttheissuanceofagreenbond.Inparticular,

asdescribedabove,theanalysiscomparesthedebtrefinancingofahypotheticalcompany

operatingintherenewableenergymarketinItalywiththeuseofprojectfinanceandthe

issuanceofagreenbond.Theproposedanalysisisconstructedfromthepointofviewof

the project shareholders/sponsors, obtaining a final NPV (Net Present Value) of the

projectforbothcases.

Theliteratureonthetopichasprovedtobestill fledglingasconfirmedbyCondeetal.

(2020).Theirworkistakenasareferencetodeveloptheanalysisofthisthesis.

Therefore, the chapter is structured by introducing the project finance instrument,

currently the most widely used source of financing in Italy in the renewable energy

market.AfterabriefdescriptionofthecurrentmarketsituationinItaly,withparticular

regardtotheincentivesystem,thelastpartwillbededicatedtotheempiricalanalysis

describedabove.

4

1.CHAPTER:CLIMATECHANGE

ClimateChangesurroundsusandwecannotavoidit.Itisoneofthemajorchallengesof

ourcenturyanditisemergingasoneofthegreatestchallengesofoursociety1.Itiswell

established that climatic variations are themost important threat of themodern age,

consideringthatitseffectsaffectthehumansociety,theeconomiesandthedestinyof

ourplanet.Thecausesof theso-called “GlobalWarming”are relativelyeasy todefine.

Studiesandacademicresearchagreethathumansareconstantlyinfluencingbothclimate

and the temperature of the Earth by burning fossil fuels, this being one of the most

important causes of global warming. The process of burning fossil fuels has the

consequencetoaddenormousamountofgreenhousegasestotheatmosphere,sustaining

andincreasingthegreenhouseeffectandtheglobalwarming.

AccordingtoKaddoandJameelR.(2016),greenhousegasesarethemaincontributorsto

climatechange.Theyareveryefficientintrappingheatintotheatmospheregenerating

thegreenhouseeffect.SolarenergyisabsorbedbytheEarth’ssurfaceandthenreflected

backtotheatmosphereasheat.Astheheatgoesouttospace,greenhousegasesabsorba

partoftheheat.Afterthat,theyradiatetheheatbacktotheearth’ssurface,toanother

greenhousegasmolecule,ortospace.

ThemainconcernforscientistsistheemissionofCO2sinceitisabout75%ofthetotal

globalemissionofgreenhousegases(Burghilaetal.,2015).

The increasing urbanization and industrialization led to the chaotic consumption of

naturalresources,severepollution,naturaldisastersandanirreversibleimbalanceofthe

Earth’s system2.Greenhousegasesare considered themainhuman-induceddriversof

climatechange3.Amongthegasesthatcontributetosustainthegreenhouseeffect(like

carbon dioxide, methane and nitrous oxide), carbon dioxide is certainly the most

dominant causeof thiskindof change, representing the75%ofglobal emissions.The

concentrationofCO2isrisingasaresultoffossilfuelburning4.

1 Burghilaetal.(2015)-ClimateChangeEffects–What’sNext?,AgricultureandAgriculturalScienceProcedia6,405–412 2 Burghilaetal.(2015)-ClimateChangeEffects–What’sNext?,AgricultureandAgriculturalScienceProcedia6,405–412 3 OECD(2008)-AnnualReport2008 4 AmericanMeteorologicalSociety(2008)-WeatherAnalysisandForecastingCommittee2008AnnualReport

5

On a daily basis, the process of climate change is represented as the increase in

temperature that affects populations all over the world, altering social systems,

economiesandtheenvironmentaroundus.Veryhotorcoldwaves,periodsofdrought,

hurricanes,floodsandfiresareputtingfoodsafetyinseriousdangerand,atthesametime,

ourhomesandourcities,ourcompaniesandourhealth.

Inthisparticularscenario,itisinterestingtoreflectonhowthemodernsocietyhasdealt

withtheevidenceofclimatechange,startingfromtherecognitionofthethreatstothe

creationofnewwaysoffundinggreenprojects,pointingoutthatclimatefinancehasa

centralroleonthisbattleagainstclimatechange.

1.1RiodeJaneiro1992

Atthebeginningof1800,thefirststudiesabouttheimportanceoftheatmosphereandits

connectionwiththeclimatewerecarriedout.

Therealbreakthroughwasin1970,whentheWorldMeteorologicalOrganization(WMO)

started to study the connection between human activities, CO2 and the growth of

temperatureontheplanet.TheconnectionswereconfirmedandfinallytheWMOissued

the IPCC (International Panel on Climate Change) in 1988. Its goalwas to summarize

scientificevidenceonclimatechangeandtopartiallyreassessgovernmentalcontrolover

theclimatechangeissue.Afterthefirststudies,theworriesaboutgreenhousegasesand

theirconnectionwiththetemperatureoftheplanetwereconfirmedandtheFramework

ConventiononClimateChange(FCCC)wasestablishedinMay1992inRiodeJaneiro.The

Conventionwasnotanend-pointbutratherthestartofanongoingprocess,thebeginning

oftheguidelinestofighttheglobalwarming.Inparticular,Article2representsthemain

objectiveoftheconference:“Stabilizegreenhousegasemissionsintheatmosphereatalevel

thatwouldpreventdangerousanthropogenicinterferencewiththeclimatesystem”5.

TheconferenceinRiowasalsoimportantbecauseitlaunchedanewwayofinteracting

between developed and developing countries. Indeed, specific commitments for

industrializedcountriesandtheformerEasternBlocweredefined:theyhadto“takethe

lead” in the GHG (greenhouse gases) emission reduction and advanced reporting6.

5 UNFCCC(1992)-Article2,RiodeJaneiro3-14June1992 6UNFCCC(1992)-Article4.2,RiodeJaneiro3-14June1992

6

Moreover,industrializedcountriesexcludingtheformerEasternBlochadtoprovide“new

andadditional”financialresourcesneededtocovercostsofreportingobligationsaswell

asmitigationandadaptationactivitiescostssupportedbydevelopingcountries7.In1994

morethan50statesapprovedtheUNFCCCandit finallyenteredintoforce.TheIPCC’s

secondassessmentreportin1996underlinedthefactthatclimatechangemitigationwas

anecessity8.

1.2KyotoProtocol

During1997inKyoto,Japan,160countriesoftheUFCCC9(UnitedFrameworkConvention

on Climate Change) adopted the Kyoto Protocol, which established legal limits for

industrializedcountriesonemissionsofcarbondioxideandother“greenhousegases”10.

ThecomplexityoftheKyotoProtocolreflectedtheeconomicandsocialissuesraisedby

climatechange11. Inparticular, theprotocolaimedto“reduceemissionsofgreenhouse

gasesindevelopedcountriesandtheglobalemissionstargetwas5,2%belowthe1990

leveltobeachievedoverthe2008-2012”12.

Infact,theart.3par.1oftheprotocolstatesthattheoverallreductionshouldbeatleast

5percent13.

TheKyotoProtocolalsoprovidedapossibilityforcountriestouseasystemof flexible

mechanismsfortheacquisitionofemissioncredits.

Thefirstmechanismwascalled“CleanDevelopmentMechanism”(CDM)anditallowed

industrializedcountriesandeconomiesintransitiontoimplementprojectsindeveloping

countries that produce environmental benefits in terms of reducing greenhouse gas

emissions,inordertoachieveemissioncredits.

7UNFCCC(1992)-Article4.3,RiodeJaneiro3-14June1992 8Bodansky,D(2001)-TheHistoryoftheGlobalClimateChangeRegime,Internationalrelationsandglobalclimatechange 9UnitedFrameworkConventiononClimateChange(1992)-openedforsignatureJune41992,S.Treaty,DOCno.102-38,1992 10ClareBreidenichetal.(1998)-TheAmericanJournalofInternationalLaw,Vol.92,No.2(Apr.,1998),pp.315-331 11ChamberofCommerceandIndustryofWA(1999)-TheKyotoProtocolAndGreenhouseGasEmissions 12WigleyT(2008)-GeophysicalResearchLetters,Vol.25,No.13,Pages2285-2288,July1,199813UNFCCC(1998)-KyotoProtocoltotheUnitedNationsFrameworkonClimateChange

7

The second mechanism, called “Joined Implementation” (JI), allowed industrialized

countries and economies in transition to implement projects for the reduction of

greenhousegasemissions inanothercountryof thesamegroupand touse the linked

creditsjointlywiththehostcountry.

Thethirdandlastmechanismwascalled“EmissionTrading”(ET)anditconsistedinthe

possibility for industrialized countries and economies in transition to “trade” the

emissioncredits. Inotherwords,acountrywhichreduces theemissionofgreenhouse

gasesmore than the objective can exchange that credits to other countrieswhich are

unabletoachievethoseobjectives,maintainingtheoverallbalance.14

ThemostimportantconditionoftheProtocolstatedthat,inorderfortheagreementto

come into force, it had tobe ratifiedbyno less than55 signatory states among those

producing at least 55% of pollutant emissions. This last conditionwas achieved only

during2004,whenRussiasignedtheagreement.

1.3DevelopmentaftertheKyotoProtocol:TheSternReview

After the first meetings organized and studies produced to mitigate the emission of

greenhousegasesand,ingeneral,climatechange,aparticularlyinsightfulresearch(and

thefollowingbook,“Ablueprintforasaferplanet”)wastheSternreview,publishedin

2006byNicolasStern,helpingthecommunitytounderstandtherealrisksoftheclimate

change.

ThegeneralopinionbeforetheSternReviewwasthattheoverallcostsofmitigatingthe

actionsagainsttheclimatechangeweretoohighand,consequently,thecostofclimate

changewasunderestimated.Infact,Stern,afteralifelivedalongsidepoorpeopleinorder

tocombatglobalpoverty,in2006,withthesupportoftheBritaingovernment,showed

withhisreviewthat“costsofclimatechangewouldbehigherthanthecostsofreducing

GHGemissionsand,asaconsequence,strongpoliticalinitiativeswereunavoidableandwere

needed as soon as possible”15. Stern’s approach had little to do with the pessimistic

environmentalismwaytoactthat,tryingtoraiseawarenessthroughshock,alltoooften

leads to resignation. The centralmessagewas simple: the risks are enormous (social,

14 EuropeanCommission(2005)-TheKyotoProtocol 15 SternN.(2007)-Theeconomicsofclimatechange.TheSternreview,CambridgeUniversityPress,Cambridge

8

economic andenvironmental)but it ispossible to contain themsignificantly ifweact

quicklyanddecisively.Thewatchwordisone:investing.

Moreover,inApril2008Sternsaidthattheseverityofhisstudieswereconfirmedbythe

2007 IPCC report. That report showed that thepresenceof greenhouse gases such as

methane,carbondioxideandnitrousoxideintheatmospherehadbeenrisingfrom1800

untiltoday16.TheyadmittedthatintheSternReview"(…)weunderestimatedtherisksand

weunderestimatedthedamageassociatedwiththeriseintemperature.Weunderestimated

the probabilities of temperature increases". In 2008, Stern said also that, since climate

changewasgoingfasterthanexpected,“thecostofreducingcarbonwouldbeevenhigher,

byabout2%ofGDPinsteadof1%intheoriginalreport”.17

1.4TheCopenhagenAgreement

On December 19 2009, the Copenhagen Conference ended with a result far below

expectations.Despitethepresenceofoverahundredheadsofstateandgovernment,the

climate summit did not succeed in creating a global agreement to replace the Kyoto

Protocol,whichwasgoingtoexpiredin2012.Withoutanagreement,the190member

countries of the UNFCCC postponed negotiations to 2010 and, as a conclusion of the

conference,abroadagreementonthetargetsforreducing2020greenhouseeffectwas

achieved: the Copenhagen Agreement. The Copenhagen Agreement was a 5 page

documentthatrecognizedclimatechangeas"oneofthegreatestchallengesofourtimes"

andstressedtheneedtolimittheincreaseinglobaltemperaturebelow2°C.Thetextdid

not containmandatory obligations but invited the industrialized countries to indicate

their reduction targets and developing countries to indicate the actions that were

intendedtobeputintopracticeinordertolimittheexpectedemissionsgrowthinthe

next ten years. On 31 January 2010, the deadline set for joining the agreement, 55

countrieshad formally adhered to thedocument, indicating their plans and reduction

targets.

16SolomonS.etal(2007)-Climatechange2007.ThePhysicalScienceBasis.ContributionofWorkingGroup,totheFourthassessmentreportoftheIntergovernmentalPanelonClimateChange,CambridgeUniversityPress,Cambridge,NewYork 17 Jowit,Juliette;Wintour,Patrick(2008)-Costoftacklingglobalclimatechangehasdoubled,warnsStern,TheGuardian.London.

9

On the other hand, the indications presented were far below what was considered

necessaryby the international scientificcommunityandwouldhavenotpreventedan

increaseintheglobaltemperatureabove3°C.Forthisreason,thatagreementrepresents

only an intermediate stage to be quickly surpassed by far more ambitious goals and

commitments.Until2015,theregulationstocombatclimatechangewerededicatedonly

tofewstates,leavingtheotherswithoutrulesorguidelines.In2015,duringCOP21,anew

fundamentalagreementbetweennationswassigned,aswewillseeinthenextparagraph.

1.5TheCOP21(ParisAgreement)

During2015intheClimateChangeConferenceofPartiesheldinParis,theso-calledCOP21,

197 countries reached a common political agreement: the Paris Agreement. This

agreementhasbeenfundamentalinthefightagainstglobalclimatechangeandagainst

theimpactsgeneratedbyglobalwarming,recognizingthat"climatechangerepresentsan

urgentandpotentiallyirreversiblethreattohumansocietiesandtotheplanet"18.Oneyear

later, on5October2016, the threshold for the entry into force of the agreementwas

achieved.TheParisAgreemententeredintoforceon4November2016,thirtydaysafter

thedateonwhichatleast55PartiestotheConvention(accountingintotalforatleastan

estimated55%ofthetotalglobalgreenhousegasemissions)depositedtheirinstruments

ofratification,acceptance,approvaloraccession19.

Thestatesalreadyinvolvedintheprevioustreatiesacknowledgedthattheeffortofafew

nations was no longer enough and a common commitment was needed to limit the

emissionsofgreenhousegases.Infact,theParisAgreementrepresentedthelargestglobal

effortwiththeaimof involvingallthenationsoftheworldinthefightagainstclimate

change,withparticularattentiontodevelopingcountries,declaringthatclimatechange

wasthegreatestthreattothefutureofourplanet.

Inparticular,thepartiescommittedtotransformtheirdevelopmenttrajectoriessothat

theysettheworldonacoursetowardssustainabledevelopment,aimingatlimitingglobal

warmingto1.5°to2°degreesabovepre-industriallevels.

18 IPCC(2020)-Link:https://www.ipcc.ch/sr15/faq/faq-chapter-1/ 19 UNCC(2015)-ParisAgreement–StatusofRatification,link:https://unfccc.int/process/the-parisagreement/status-of-ratification

10

ThroughtheParisAgreement,thepartiesalsoagreedtoalong-termgoaltoincreasethe

abilitytoadapttotheadverseimpactsofclimatechangeandfosterclimateresilienceand

low greenhouse gas emissions development, in amanner that does not threaten food

production.Additionally,theyagreedtoworktowards“makingfinanceflowsconsistent

with a pathway towards low greenhouse gas emissions and climate-resilient

development”20.

The heads of Governments also understood the need to reach the global peak of

greenhousegasemissionsassoonaspossibleinordertoproceedinthefuturewithrapid

reductions depending on the available technologies, achieving a balance between

emissionsandremovalsbysinksofgreenhousegasesinthesecondhalfofthiscentury.

Infact,asstatedbyUNFCCC,“itisunderstoodthepeakingofemissionswilltakelongerfor

developingcountries,andthatemissionreductionsareundertakenonthebasisofequity,

andinthecontextofsustainabledevelopmentandeffortstoeradicatepoverty,whichare

criticaldevelopmentprioritiesformanydevelopingcountries”.21

Theagreementisdividedintodifferentareas,inordertomeetthesechallenginggoals.In

particular, the areas are adaptation, loss and damage,mitigation, finance, technology,

capacitybuildingandreportingandaccounting.Moreover, theCOP21proposedanew

transparencyframework,fosteringthefinancialandtechnicalinnovationinordertohelp

developingcountriesinmitigatingthedisruptiveconsequencesofclimatechange.

Moreover,itpromotedthefavorableconditionsforatransitionfromfossilfuelstoward

renewableenergysources.

Finally,theagreementstressedtheimportanceofthecommitmentmadein2009during

theCOP15inCopenhagenbydevelopedcountriesto"jointlymobilize$100billionayear

until2020"todevelopingcountriesformitigationandadaptationactions.

1.5.1TheINDCs

Inorder topursue these long-termobjectives,art.4of theagreementstates thateach

country has to prepare, communicate and maintain a list of activities and binding

20UNCC(2017)-NationallyDeterminedContributions(NDCs),link:https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement/nationally-determined-contributions-ndcs#eq-1 21UNCC(2017)-NationallyDeterminedContributions(NDCs)

11

commitments to be implemented post-2020: the so-called Intended Nationally

DeterminedContributions(INDCs),whicharecalledNationallyDeterminedContributions

(NDCs)once theagreementhasbeenapprovedandratified. “Theseplansare the first

instrument throughwhich governments communicate at international level the steps

theyintendtotaketocombatclimatechangeintheirterritories”.22

Sofar,notallthepartiesratifyingtheagreementhavealsodepositedtheirNDCs:only189

outof197nations,whichratifiedtheagreementhavedoneit,whilesomeothercountries

haveonlydepositedtheINDCs.

Moreover,inparagraphs9,11and13itisstatedthat“governmentswillhavetoincrease

their efforts not only to achieve the objective of the agreement and to communicate

supplementary updates every five years, but also operate in the field of transparent

reportingoftheiremissionsandtheprogressofimplementationprocesses”.23

Indeed,theagreementstatesthatactionplansmustbedrawnupinaccordancewiththe

principleofequity,takingintoaccounttheinternalcapacitiesandcircumstancesofeach

nation,thusensuringthateachcountryplaysitspart.Theymustalsobeasambitiousas

possibleindirectingtheprocessofdecarbonizingcarbon-intensivesectors.

As described in art. 14, countries must report on the progress made internally with

respect to theirNDCs and the long-termobjectives of the agreement every five years

startingfrom2023:thisprocedureiscalled"globalstocktake".24

Thekeyquestion iswhether thecommitmentsandobjectiveswithin theNDCswillbe

sufficienttomaintainalevelofglobalwarmingbelow2°Cby2030.

Theanswer, asdescribedbyCAT (ClimateActionTracker), isnegative.Theemissions

reductionstargetsputforwardintheINDCs,iffullyimplemented,areprojectedtoleadto

aglobalwarmingofaround2.7°C(2.2-3.4°C)(or,inprobabilisticterms,arelikelytolimit

warmingtobelow3°C)by2100.25Thisconstitutesanincreaseof0.4°CsinceDecember

2014,beforeanyINDCswereformallysubmitted.

22 UNCC(2015)-link:https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement/nationally-determined-contributions-ndcs 23UNCC(2015)-TheParisAgreement,link:https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement24WorldResearchInstitute(2015)-WhatisanINDC?25 JefferyL.etal.(2015)-ClimateActionTrackerUpdate,link:https://climateactiontracker.org/documents/44/CAT_2015-12-08_2.7degCNotEnough_CATUpdate.pdf

12

Thefigurebelow(seeFigure1) showsthetrendsthat theemissionsshould followin

ordertomaintainthewarmingbelowthe2°C.

Figure1:GHGemissionindifferentscenarios.Source:CAT(2015)

The effortsmadewith the INDCs showa substantial improvement from the scenarios

beforethestartof the INDCprocess.However, the impactof these INDCs isstillmuch

lowerthanthatrequiredtolimitheatingto1,5°Corlessthan2°C.

RegardingtheParisAgreement,arelevantdecisionbytheUShasbeentakenduring2017.

On August 4 (2017), the Trump administration handed the UnitedNations an official

noticethattheUnitedStatesintendedtoterminatefromtheParisAgreementassoonas

itwaslegallyadmissibletodoso.Theformalnoticeofwithdrawalcouldnotbesubmitted

untiltheagreementwasinforcefor3yearsfortheUnitedStates(4November2019).On

4November,theUnitedStatesGovernmentdepositeditsnoticeofwithdrawalwiththe

Secretary-GeneraloftheUnitedNations,thedepositaryoftheagreement.

ThewithdrawaloftheUnitedStates,thesecondmostpollutingcountryintheworld,

fromtheParisAgreementriskstounderminetheinternationaleffortstocombatclimate

change.ThedatapublishedbytheWorldBank,accordingtowhich"theimpactof

extremenaturaldisastersisequivalenttoagloballossof520billiondollarsinannual

consumptionandannuallyforcesabout26millionpeopletopoverty"26,showsthatclimate

26 TheWorldBank(2016)-link:https://www.worldbank.org/en/news/press-release/2016/11/14/natural-disasters-force-26-million-people-into-poverty-and-cost-520bn-in-losses-every-year-new-world-bank-analysis-finds

13

challengesneedamultilateralapproachandcannotfocusonsimplisticandnational

responses.Thenewtechnologiesarereadytodirectthecurrentenergyandproduction

inaverygreendirection.However,suchdimensionscannotbeseparatedfromastrong

politicalleadershipcapableofovercominggeographicalandideologicaldifferences.

WithouttheUnitedStates,thisleadershipgap,evenifitcanbefilled,isboundtobefelt.

Moreover,inFebruary2021thePresidentJoeBidenreenteredtheUnitedStatesinthe

ParisAgreement,fewhoursafterhisinauguration.

However, theParisAgreementhighlights theeconomicand financial field as a central

actorforthefightagainsttheclimatechange.Article2.1coftheAgreementcommitsthe

partiesto"makingfinanceflowsconsistentwithapathtowardslowergreenhousegas

emissionsandaclimate-resilientdevelopment".27

Aswewillseeinthenextchapters,thefundsrequiredtomeetthethresholdof2°Care

large,andtherearemanystudiestoestimatethemshowingdifferentresults.

Theresearchersagreed that thegapbetweenclimate-friendly finance flowsand those

needed to achieve the climate stabilization objective is large but technology and

innovationarereadytolimitit.28

1.6SustainableDevelopmentGoals(SDGs)

InSeptember2015,inNewYork,morethan150internationalleadersmetattheUnited

Nationstocontributetoglobaldevelopment,promotinghumanwell-beingandprotect

theenvironment.TheStatesendorsedtheSustainableDevelopmentAgenda2030,whose

essential elements are the 17 Sustainable Development Goals (SDGs) (see Figure 2)

together with 169 sub-objectives, which aim to end poverty, combat inequality and

supportsocialandeconomicdevelopment.Inaddition,itincludesaspectsoffundamental

importanceforsustainabledevelopmentsuchastheoppositiontoclimatechangeandthe

sustainmentofpeacefulsocietiesbytheyear2030.After2yearsofpublicconsultations

aroundtheworld,the17SustainableDevelopmentGoalscameintoforceon1January

2016. The SDGs replaced theMillenniumDevelopment Goals (MDGs) bymerging the

27 UnitedNations(2015)-TheParisAgreement,link:https://unfccc.int/sites/default/files/english_paris_agreement.pdf#page=5 28 StephenPeake&PaulEkins(2016)-ExploringthefinancialandinvestmentimplicationsoftheParisAgreement,ClimatePolicy

14

agendasofdevelopmentandenvironment29andthedifferencebetweenSDGsandMDGs

is that the latter make no distinction between developed and developing countries,

coveringallstateswithoutdistinction.Inparticular,theobjectives,whichareinterlinked

and indivisible, balance the three dimensions of sustainable development: economic

growth,socialinclusionandenvironmentalprotection,byextendingAgenda2030from

the social dimension of the MDGs to the other two dimensions, economic and

environmental.

Figure2:TheSDGs.Source:UnitedNations

TheSDGsarebasedonthefive“P”s:People,Planet,Prosperity,PeaceandPartnership.In

this particular framework, the focus on finance is crucial. The financial dimension,

comprehensive and consistentwith the achievement of the SDGs,was outlined in the

AddisAbabaActionPlan.SignedinJuly2015bythe193membercountriesoftheUnited

Nationsat theThird InternationalConferenceonFinancing forDevelopment, theplan

identifiesmorethanahundredconcretemeasurestomeeteconomicchallenges,aswell

associalandenvironmentalissuesfacedbytheworld.Thepriorityofactionatnational

levelishighlightedwiththedevelopmentoffavorableandcoherentpolicies,favoringalso

29 MagdalenaBexell&KristinaJonsson(2017)-ResponsibilityandtheUnitedNations’SustainableDevelopmentGoals,ForumforDevelopmentStudies,44:1,13-29

15

the role of the private sector. About this last aspect, the document emphasizes the

importancetoaligntheprivateinvestmentstotheattainmentoftheSDGs.Countriesare

invitedtoputinplaceappropriatemeasurestocombatbothevasionandillicitfinancial

flows. As we will see in the next chapters, the health crisis caused by the COVID-19

pandemichasradicallychangedtheplanofaction.Inparticular,itiscrucialtoanalyzethe

Financing for Sustainable Development Report 2020, edited by the United Nations in

collaboration with 60 agencies of the Inter-Agency Task Force on Financing for

Development, which brings together ONU agencies and international partner

organizations.Thedocument,publishedon4April2020,preparedinthelightofthevery

serious economic, social and health crisis caused by the COVID-19 pandemic, calls

governments toactwithappropriatemeasures to respond to immediateneedsand to

preventaglobaldebtcrisiswithpotentiallydevastatingconsequences.

1.7MitigationandAdaptation

All actions aimed at reducing the amount of greenhouse gases in the atmosphere are

included in theconceptof "mitigation".Acting in thisdirection is crucial,because it is

precisely by emitting an excessive amount of these gases - whose atmospheric

concentration has no precedent in the last 800 thousand years - thatwe are causing

climatechange.Theonlyeffectivewayforreducingtheconcentrationofgreenhousegases

intheatmosphereistoemitless.Inotherwords,to"mitigate"thequantitiesproduced.It

is,however,asolutionthat isassimpleto identifyas it isdifficulttoput intopractice,

becausetheemissionofgreenhousegases,andinparticularCO2,isatthebasisofalmost

allhumanactivities.

Inordertoavoidthemostseriousconsequencesofclimatechange,thecountriesofthe

UnitedNationsFrameworkConventiononClimateChange(UNFCCC)agreedtolimitthe

increaseinoverallaveragesurfacetemperaturecomparedtothepre-industrialperiodto

below2°C.Inordertoachievethisobjective,globalgreenhousegasemissionsmustpeak

asquicklyaspossibleandthereforedecreaserapidly.By2050,globalemissionsmustbe

reducedby50%comparedto1990levels,andbytheendofthecentury,carbonneutrality

mustbeachieved.

Regardingthegreenhousegasemissionsbyeconomicsectors(seeFigure3),theprimary

sources of emissions are the process of burning fossil fuel for electricity and heat

16

generation (25%), followed by industry (21%), transportation (14%), other energy

(10%),buildings(6%).Finally,agriculture,forestry,andotherlandusescontributetothe

24%ofgreenhousegasemissions.

Figure3:Greenhousegasemissionsbyeconomicsectors.Source:Statista

Inthisparticularscenario,theenergysectorrepresentsafundamentalprocesstolimit

GHG(greenhousegases)emissions,followedbyagriculture,forestryandotherlanduse

(AFOLU)30.Asa civil society,wehave twooptions to follow inorder to “mitigate” the

greenhousegasemissionintheenergysector.Ononehand,energyconsumptioncanbe

reducedbyinvestinginenergyefficiency.Ontheotherhand,itiscrucialtoreplacefossil

fuels with "clean" energy sources, in particularwith renewable energy, such as solar

panelsorwind,whichproduceenergyusingthenaturalresourcesoftheEarth(suchas

sunlight, wind, but also the flow of rivers and the motion of waves). Focusing on

renewablesources,currentlyrelegatedtoasecondrole,meansproducingenergywithout

emittinggreenhousegases,andtherefore"mitigating"globalemissions.

30 Smithetal.,(2014)-Agriculture,ForestryandOtherLandUse(AFOLU).In:ClimateChange2014:MitigationofClimateChange.ContributionofWorkingGroupIIItotheFifthAssessmentReportoftheIntergovernmentalPanelonClimateChange,CambridgeUniversityPress,Cambridge,UnitedKingdomandNewYork,NY,USA.

17

Indeed,severalEuropeaninitiativesaimtoreducegreenhousegasemissions.Afterthe

achievementoftheKyotoProtocoltargetsfortheperiodfrom2008to2012,theEUhas

adopted legislation to foster the use of renewable energies, such as wind, solar,

hydroelectric and biomass, and to improve the energy efficiency of a wide range of

appliancesandequipment.TheEUalso intends tosupport thedevelopmentofcarbon

captureandstoragetechnologiestotrapandstoreCO2frompowerplantsandotherlarge

installations.

However,astheInternationalEnergyAgency(IEA)estimated,around“USD3.5trillion

yearlyinenergysectorinvestmentswouldbenecessarybetween2016and2050inorder

tomaintaintherisingoftemperaturebelow2°C”.31

Theotherconceptcloselyconnectedto“mitigation”istheneedto"adapt"toachanging

climate.Inpractice,thismeansminimizingtheimpactofclimatechangeonthewell-being

ofcitizens,thesupplyofresourcesandthestabilityofecosystems.“Adaptation”hasbeen

definedbytheIntergovernmentalPanelonClimateChange(IPCC)asthe“adjustmentsin

practices,processesorstructureswhichcanmoderateoroffsetthepotentialdamageortake

advantageforopportunitiescreatedbyagivenchangeinclimate”.32

Climate change affects many aspects of our society and, in order to manage its

consequences,itwillbeessentialtointegrateadaptationpoliciesineverysector.Atthe

basisofthisconcept,therearealltheconsequencesthatclimatechangehasonagriculture

andlivestock(drought,desertification)andonfishing(meltingglaciers,acidificationof

theoceans)whichareonlyapartoftheproblemsthatfuturegenerationswillhavetoface,

togetherwithotherfundamentalissuessuchaspoverty,lackoffoodsecurityandwater

scarcity.Inaddition,urbanandengineeringchallengeswillhavetobefacedinorderto

preventcitiessuchasVenice,NewYorkorCairofromsufferingtheeffectsofrisingsea

levels.

Inthisframework,theroleofinnovationiscrucial,becauseitallowsfindingmoreefficient

technologies forenergyconversion,or tousealternativesourcesofenergy,orevento

31 IEA(2019);Link:https://www.iea.org/reports/the-critical-role-of-buildings 32 IPCC(2018)-GlobalWarmingof1.5°C.AnIPCCSpecialReportontheimpactsofglobalwarmingof1.5°Cabovepre-industriallevelsandrelatedglobalgreenhousegasemissionpathways,inthecontextofstrengtheningtheglobalresponsetothethreatofclimatechange,sustainabledevelopment,andeffortstoeradicatepoverty

18

capture and store CO2. The following areas may cover these and other mitigation

activities33:

- Energy

- Transportation

- Buildings

- Industry

- Agriculture

- ForestryandOtherLandUse

Asitwillbeshowedinthenextchapters,therenewableenergysectorhasbecomecrucial

forthemitigationagainstclimatechangeandoneoftherolesofpublicfinanceistofoster

the investments in this growing sector. Indeed, for the purposes of this research, the

energysectorwillbethesectorthatwillbetakenasexampletomitigateclimatechange,

highlighting inparticulartheEuropean(orCommunity)policiesthat fostertheenergy

transitionfromfossil-basedenergytowardsrenewableenergy.

1.7.1EnergySector

Energysupplyisthemaincauseofglobalgreenhousegasemissionswith35%ofthetotal:

itsgrowthacceleratedfrom1.7%peryearfrom1990to2000to3.1%peryearfrom2000

to2010.34

ComplyingwiththeParisAgreementwouldmeanprogressivelyreducingtheuseoffossil

fuelstozerobytheendof2100,sincetheyareresponsibleforabout70%ofgreenhouse

gasemissionsand,combined,meetabout86%ofenergydemand.Moreover,asstatedby

IRENA (2019), “the energy production sector offers amultitude of options for reducing

emissions: improvingenergyefficiencyandusingsourcesthatreduceemissions fromfuel

33 Link:https://archive.ipcc.ch/pdf/reports-nonUN-translations/italian/ar4-wg3-spm.pdf 34 IPCC(2014)

19

extraction,energyconversion,transmissionanddistributionsystems,ornewlow-emission

energyproductiontechnologiessuchasrenewableandnuclear”.35

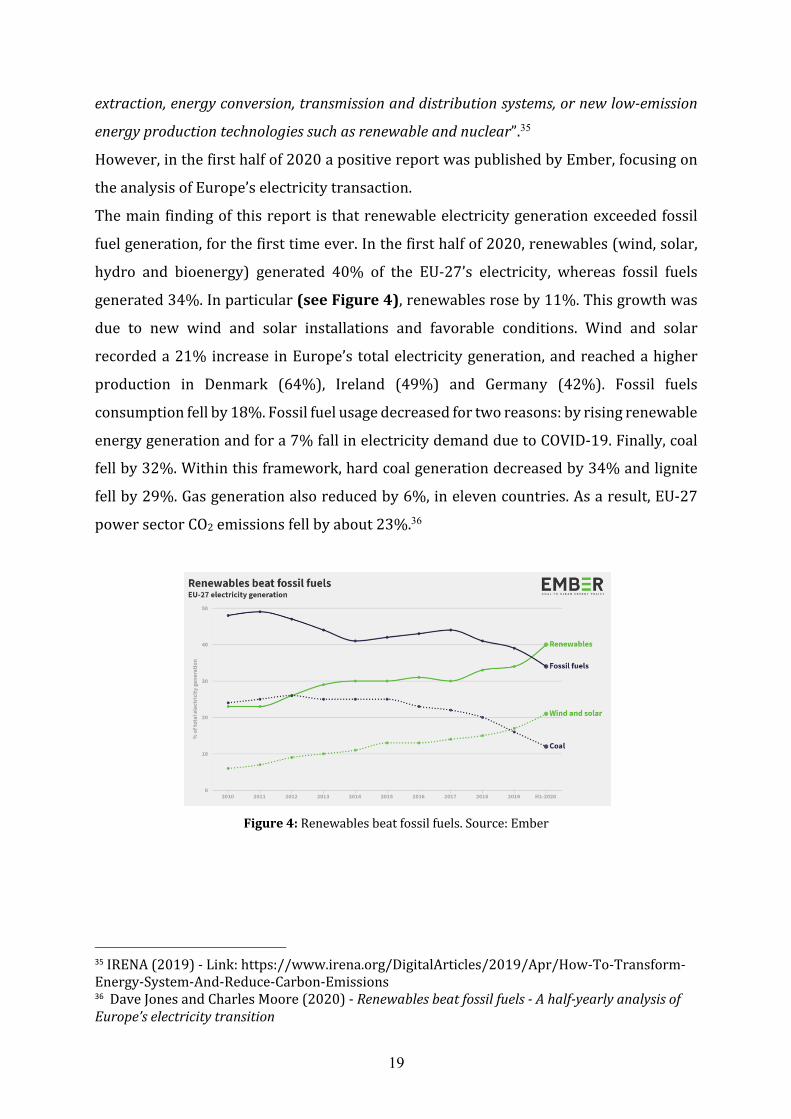

However,inthefirsthalfof2020apositivereportwaspublishedbyEmber,focusingon

theanalysisofEurope’selectricitytransaction.

Themainfindingofthisreport isthatrenewableelectricitygenerationexceededfossil

fuelgeneration,forthefirsttimeever.Inthefirsthalfof2020,renewables(wind,solar,

hydro and bioenergy) generated 40% of the EU-27’s electricity, whereas fossil fuels

generated34%.Inparticular(seeFigure4),renewablesroseby11%.Thisgrowthwas

due to new wind and solar installations and favorable conditions. Wind and solar

recordeda21%increase inEurope’s totalelectricitygeneration,andreachedahigher

production in Denmark (64%), Ireland (49%) and Germany (42%). Fossil fuels

consumptionfellby18%.Fossilfuelusagedecreasedfortworeasons:byrisingrenewable

energygenerationandfora7%fallinelectricitydemandduetoCOVID-19.Finally,coal

fellby32%.Withinthisframework,hardcoalgenerationdecreasedby34%andlignite

fellby29%.Gasgenerationalsoreducedby6%,inelevencountries.Asaresult,EU-27

powersectorCO2emissionsfellbyabout23%.36

Figure4:Renewablesbeatfossilfuels.Source:Ember

35 IRENA(2019)-Link:https://www.irena.org/DigitalArticles/2019/Apr/How-To-Transform-Energy-System-And-Reduce-Carbon-Emissions 36 DaveJonesandCharlesMoore(2020)-Renewablesbeatfossilfuels-Ahalf-yearlyanalysisofEurope’selectricitytransition

20

1.7.1.1GSEIncentive

The energy transaction towards a renewable and sustainable future passes through

market-based instrumentssuchassubsidiesoremissiontaxes,controlovertheuseof

specificfuels,theperformancetobesupportedorthemaximumemissionsgranted.

One of the examples of the energy transition to renewable energy in Italy is the

mechanism of incentives managed by the company GSE S.p.a. (Gestore dei Servizi

Energetici).

ThecompanyisanItalianlimitedcompany,whollycontrolledbytheMinistryofEconomy

andFinance thatcarriesout its tasks inaccordancewith thestrategicandoperational

guidelinesdefinedbytheMinistryofEconomicDevelopment.37

TheGSEplaysacentralroleinthepromotionanddevelopmentofrenewablesourcesin

Italy. The main activity is the promotion, also through the provision of economic

incentives,ofelectricityproducedfromrenewablesources.

In particular, it acquires and redistributes energy from renewable sources into the

market.Itprovidesincentivesforproduction,itverifiesthatthesameproductiontakes

placeaccording to regulationsandprovides theGreenCertificates.TheGSEalsodeals

withthemonitoringofrenewableenergywiththegoalofachievingthetargetsset for

2020. It is responsible for providing data and technical advice to institutions, public

administrationsandoperatorsinthesectorinordertoencouragethedisseminationof

sustainableenergysources.38

In2018,morethan1GWofadditionalrenewableenergypowerwasinstalledinItaly.450

MWarerepresentedbysolarphotovoltaics.

Moreover,Enarray(2019)suggeststhat“thankstoover113TWhofenergyproducedfrom

renewable sources, Italy has exceeded, in 2018 and for the fifth consecutive year, the

thresholdof17%ofconsumptionsatisfiedbyrenewables”.39

37 Link:https://www.gse.it/en/company 38 Link:https://www.gse.it/en/company 39 Enerray(2019)-2018RenewableenergystatisticsinItaly,Link:https://www.enerray.com/blog/renewable-energy-statistics-italy-2018/

21

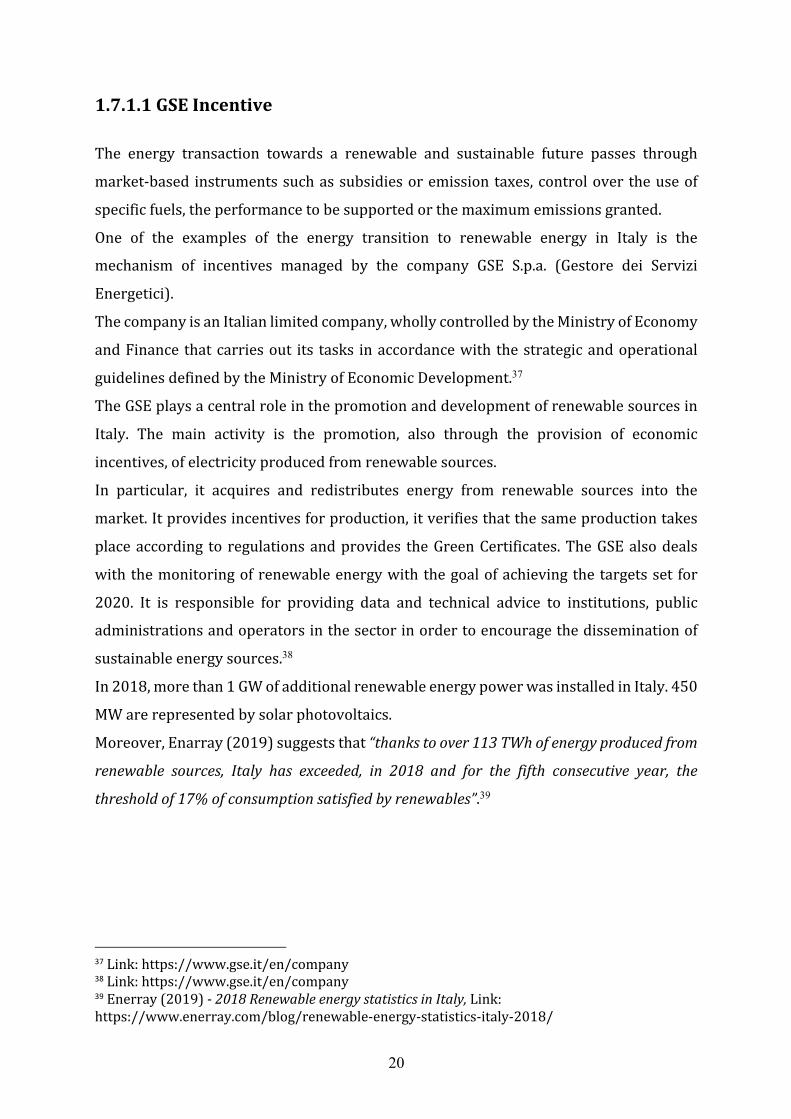

Figure5:EvolutionofphotovoltaicplantsinItaly.Source:Enerray

The Italian promotion and feed-in tariff system for renewable energy sources is

characterizedbyamultiplicityofmechanismsthathavefollowedovertheyearsinalogic

ofprogressivemarketorientationandreductionof the incentive level in linewith the

decrease of generation costs40 (see Figure 5). The FiT program Conto Energia41,

operating in Italy since the end of 2005, guaranteed a significant growth in the

photovoltaicsectorduringitsoperations,especiallybetween2011and2012.

1.8.ClimateChangeandCOVID-19

OnMarch11,2020, theWorldHealthOrganizationdeclared theCOVID-19outbreaka

pandemic.AsdefinedbytheU.S.DepartmentofHealthandHumanServices(2020),“data

from China have indicated that older adults, particularly those with serious underlying

40 Enerray(2019)-2018RenewableenergystatisticsinItaly,Link:https://www.enerray.com/blog/renewable-energy-statistics-italy-2018/ 41 Link:https://www.gse.it/servizi-per-te/fotovoltaico/conto-energia

22

healthconditions,areathigherriskforsevereCOVID-19–associatedillnessanddeaththan

areyoungerpeople”.42

COVID-19 pandemic has radically changed people’s lives around the world. The

consequencesoflockdownsinvariouscountrieshaveshown,probablyasneverbefore,

that human society is vulnerable. A constantly changing situation that has forced all

sectorslinkedtohumanactivitytorethinkproduction,socialandeconomicprocesses.

Climatechangehasalsobeenaffectedby theCOVID-19pandemicand theSustainable

DevelopmentGoalsReport2020wellframesthecurrentandfutureconsequencesofthe

pandemic.

Ingeneral,theannualSustainableDevelopmentGoalsReportprovidesanoverviewofthe

world’simplementationeffortstodate,highlightingareasofprogressandareaswhere

moreactionneedstobetakentoensurenooneisleftbehind.Asdescribedbythereport,

“the COVID-19 pandemic has unleashed an unprecedented crisis, causing further

disruptiontotheprogressofSDGs,withtheworld’spoorestandmostvulnerableaffected

themost”43 (United Nations, 2020). Using the latest data and estimates, this annual

stocktakingreportonprogressacrossthe17Goalsshowsthatitisthepoorestandmost

vulnerable– including children,olderpersons,personswithdisabilities,migrants and

refugees–whoarebeinghitthehardestbytheeffectsoftheCOVID-19pandemic.Women

arealsobearingtheheaviestbruntofthepandemic’seffects.

Fromanenvironmentalpointofview,lockdownrestrictionshavehadpositiveeffectson

GHGemissions.However,theseeffectsarecalculatedintheshorttermanditis

necessarytoanalyzetheeffectsinthemedium-longterm.AccordingtoForsteretal.

(2020),“theclimateeffectoftheimmediateCOVID-19relatedrestrictionsiscloseto

negligibleandlastingeffects,ifany,willonlyarisefromtherecoverystrategyadoptedin

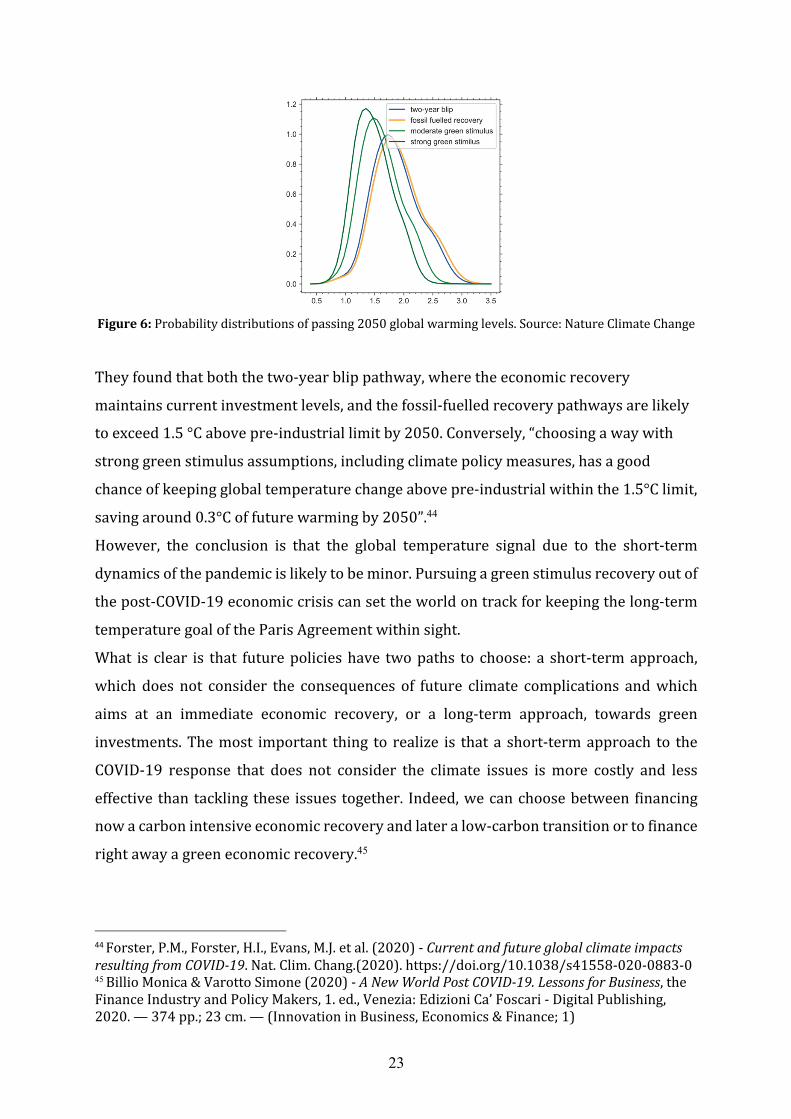

themediumterm”.Intheiranalysis,theystudiedtheeffectofdifferentscenarios,

includingafossil-fuelledrecoveryandtwodifferentscenariosofgreenstimulus(see

Figure6).

42 U.S.DepartmentofHealthandHumanServices-CentersforDiseaseControlandPrevention(2020)-SevereOutcomesAmongPatientswithCoronavirusDisease2019(COVID-19)—UnitedStates,February12–March16,202043 UnitedNations(2020)-TheSustainableDevelopmentGoalsReport2020

23

Figure6:Probabilitydistributionsofpassing2050globalwarminglevels.Source:NatureClimateChange

Theyfoundthatboththetwo-yearblippathway,wheretheeconomicrecovery

maintainscurrentinvestmentlevels,andthefossil-fuelledrecoverypathwaysarelikely

toexceed1.5°Cabovepre-industriallimitby2050.Conversely,“choosingawaywith

stronggreenstimulusassumptions,includingclimatepolicymeasures,hasagood

chanceofkeepingglobaltemperaturechangeabovepre-industrialwithinthe1.5°Climit,

savingaround0.3°Coffuturewarmingby2050”.44

However, the conclusion is that the global temperature signal due to the short-term

dynamicsofthepandemicislikelytobeminor.Pursuingagreenstimulusrecoveryoutof

thepost-COVID-19economiccrisiscansettheworldontrackforkeepingthelong-term

temperaturegoaloftheParisAgreementwithinsight.

What is clear is that futurepolicieshave twopaths to choose: a short-termapproach,

which does not consider the consequences of future climate complications andwhich

aims at an immediate economic recovery, or a long-term approach, towards green

investments.Themost important thing to realize is thata short-termapproach to the

COVID-19 response that does not consider the climate issues ismore costly and less

effectivethantacklingthese issuestogether. Indeed,wecanchoosebetweenfinancing

nowacarbonintensiveeconomicrecoveryandlateralow-carbontransitionortofinance

rightawayagreeneconomicrecovery.45

44 Forster,P.M.,Forster,H.I.,Evans,M.J.etal.(2020)-CurrentandfutureglobalclimateimpactsresultingfromCOVID-19.Nat.Clim.Chang.(2020).https://doi.org/10.1038/s41558-020-0883-0 45 BillioMonica&VarottoSimone(2020)-ANewWorldPostCOVID-19.LessonsforBusiness,theFinanceIndustryandPolicyMakers,1.ed.,Venezia:EdizioniCa’Foscari-DigitalPublishing,2020.—374pp.;23cm.—(InnovationinBusiness,Economics&Finance;1)

24

AccordingtoBattiston,BillioandMonasterolo(2020), “reinforcingthesocio-economic

resilienceagainstfuturepandemicscallsforrecoverymeasuresthatarefullyalignedto

theobjectivesoftheEUGreenDeal”,asitwillbeshowedinthenextchapters.Tackling

theseobjectivestogetherismorecosteffectivethanaddressingtheCOVID-19crisiswith

short-termmeasures.Remarkably,becauseoftheinter-connectednessbetweenclimate

risk,pandemicriskandfinancialrisk(Monasterolo,Billio,Battiston,2020),thismaybe

actuallytheonlyfeasiblewaytobuildresiliencetofuturecrises.Theeconomicresponse

toCOVIDshouldrathertakeplacewithinaframeworkofhardconstraintsongreenhouse

gasemissions.Suitablepoliciesexist,butplausibly require to implement international

cooperation.46

46 BardsleyN.(2020),AvoidingaGreatDepressionintheEraofClimateChange

25

2.CHAPTER:CLIMATEFINANCE

Climate change is not just an environmental issue. It is an issue of global economic

importancethatconcernstheprospectsforgrowth,theexitfrompovertyindeveloping

countries, a careful use of resources to avoid penalizing future generations. In this

complexframework,theworldoffinanceplaysadecisiverole.

Climate finance is defined by the United Nations Framework Convention on Climate

Change(UNFCCC)tobe“local,national,ortransnationalfinancing—drawnfrompublic,

private, and alternative sources of financing — that seeks to support mitigation and

adaptation actions that will address climate change.” It is about investments that

governments,corporations,andhouseholdshave“toundertaketotransitiontheworld’s

economytoalow-carbonpath,toreducegreenhousegasconcentrationslevels,andtobuild

resilienceofcountries toclimatechange”.47Formitigation,climate finance isneeded in

ordertofosterlarge-scaleinvestmentsandtoreduceemissions.Itisequallyfundamental

foradaptationbecausenewfinancialresourcesareneededtoreducetheeffectsofclimate

change.

Alongwiththegoalsof“pursuingeffortstolimitthetemperatureincreaseto1.5°Cabove

pre-industriallevels”and“increasingtheabilitytoadapttotheadverseimpactsofclimate

change,”Article2oftheParisAgreementrecognizedthat“financeflows”areessentialto

achievethese longstandinggoalsof“lowgreenhousegasemissionsandclimate-resilient

development”48(COP21,2015).Moreover,theUNFCCC’sStandingCommitteeonFinance

(SCF) takes a comprehensive view of climate finance, defining it as finance aimed at

“reducingemissions,andenhancingsinksofgreenhousegasesandatreducingvulnerability

of, and maintaining and increasing the resilience of, human and ecological systems to

negativeclimatechangeimpacts”49.Morespecifically,climatefinancetypicallyconsistsof

grants,loans,equityintheformofpurchasedshares,anddebtrelief.IntheSCF’sBiennial

47 HongH.,KarolyiG.A.,ScheinkmanJ.A.(2020)-ClimateFinance,ReviewofFinancialStudies48 WhitleyS,ThwaitesJ,WrightH,OttC(2018)-MakingFinanceConsistentwithClimateGoals:InsightsforOperationalisingArticle2.1coftheUNFCCCParisAgreement.OverseasDevelopmentInstitute,London49 SCF(2014)-UNFCCCStandingCommitteeonFinance:2014BiennialAssessmentandOverviewofClimateFinanceFlowsReport.UNFCCCBonn.

26

AssessmentandOverviewofClimateFinanceFlows,isstatedthat“totalglobalfundingin

2016wascalculatedtobeUSD681billion,asahigh-boundestimate,anincreaseof17%

overtheprevioustwoyears,withmostofthegrowthoccurringinnewprivateinvestments

inrenewableenergyprojects”50.

However, literature on climate investment and finance is very poor, quantitative

informationislimitedandincomplete,asistheaccountingsystem.Thecrucialproblemis

that capital monitoring and verification systems invested in green projects at an

internationallevelhavenotbeensharedandimplementedyet.Thus,theavailabledata

areoftenobtainedusingdifferentmethodologiesdependingontheprojects.Forexample,

data referred to mitigation and adaptation costs changing with the policy and

technologicaldevelopmentconsideredintheanalysis.

2.1Low-CarbonEconomyTransition

Thetransitiontoa low-carboneconomywillrequire further investment inthecoming

decades and will require that the efforts, especially financial, of the recent years are

definitelystrengthened.Wearestillatthebeginningofthetransitionfromahigh-carbon

economytoalow-carboneconomy.Transformingourenergysystemwilltaketimeanda

significantamountofcapitalanditwillalsorequireclosecoordinationamongthreekey

elements:policy,technologyandcapital.

According to the International Energy Agency (IAE, 2010), “$10.5 trillion in global

incrementalinvestmentsinlow-carbonenergytechnologiesandenergyefficiencyby2030

will be necessary”. This estimate is across all sectors, including power, transport,

residentialandcommercialbuildingequipment,andindustrialsectors,inordertolimit

global temperature increases to 2 C°, the threshold that the United Nations

Intergovernmental Panel on Climate Change has identified as necessary for “avoiding

catastrophicclimatechange.”51

Moreover, the energy transition is affected by the problem of world overpopulation,

whichgrewfrom3billionpeopleatthebeginningofthe20thcenturyto7billionpeople

at thebeginningof the21stcentury.Theshockcausedby thescarcityof fossilenergy

50 SCF.(2018)-SummaryandRecommendationsbytheStandingCommitteeonFinanceonthe2018BiennialAssessmentandOverviewofClimateFinanceFlows.UNFCCCBonn.51 GoldmanSachs(2010)-OpportunitiesandChallengesoftheEmergingCleanEnergyIndustry

27

sources, in the absence of alternative energy sources, will drastically reduce world

agriculturalproductionresultinginfoodshockfortheworldpopulation.

Tounderstandtheclimatefinanceflowsoverthepastyearsandamountofinvestments

neededtoreachtheParisAgreementtargets,threedifferentanalysiswillbeshowed:IEA,

IRENAandClimatePolicyInitiativeanalysis.

According to IEA, clean-energy investments, in particular solar andwindpower, have

beengrowingrapidlyinrecentyears52.Forexample,in2015,investmentsinrenewable

energyamountedtomorethan300billionperyear.However,consideringfossilenergy

investments,theystilldominatetheenergyindustry.

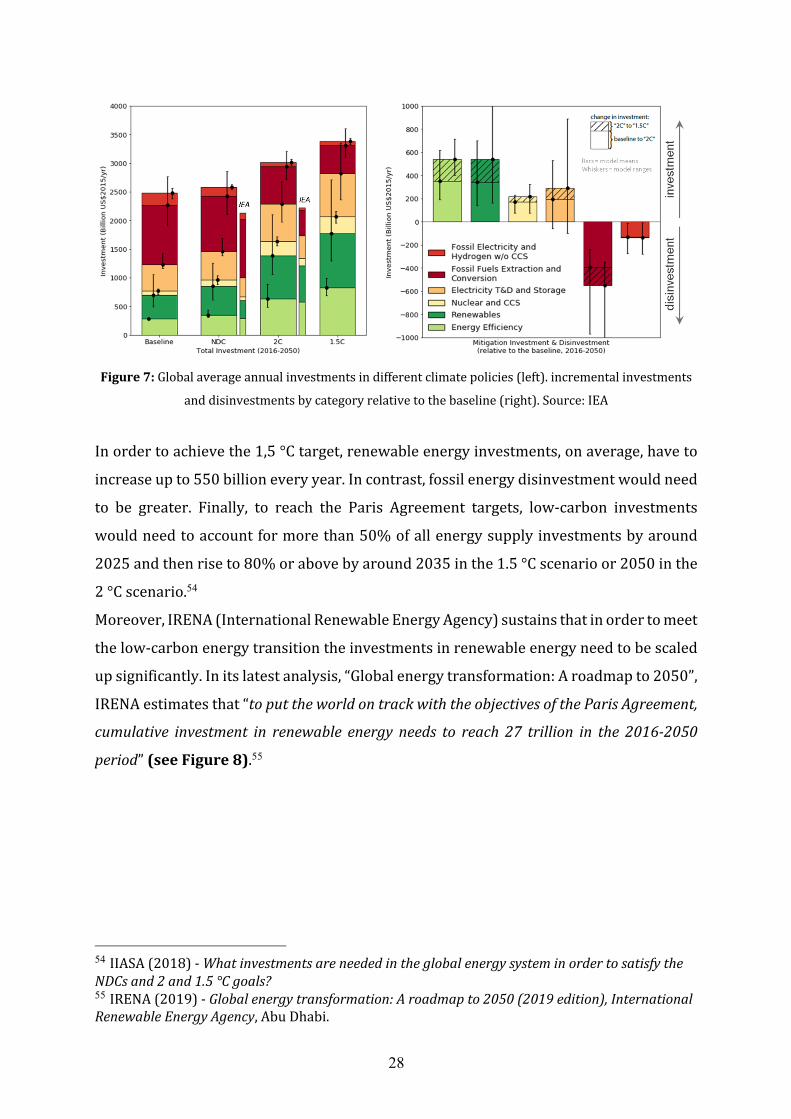

ToachievetheambitioustargetsoftheParisAgreement,animportanteffortintermsof

investmentinrenewablesandenergyefficiency,combinedwithrapiddisinvestmentsof

fossilfuels,willbenecessary.Theimpactoffutureenergyandclimatepoliciesontotal

energy investments depends on the nature of the policies (see Figure 7). The NDC

scenariowould likely only necessitate amarginal increase in total future investments

globally. In contrast, according to most models, “more aggressive policies promoting

decarbonizationthroughaglobalenergysystemtransformation(‘2C’and‘1.5C’scenarios)

willrequireamarkedincrease”.53

52 OECD/IEA(2016)-WorldEnergyInvestment2016.(OrganisationforEconomicCo-operationandDevelopment(OECD),InternationalEnergyAgency(IEA),201653 McCollum,D.L.etal(2018)-EnergyinvestmentneedsforfulfillingtheParisAgreementandachievingtheSustainableDevelopmentGoals.NatureEnergy3,589-599,doi:10.1038/s41560-018-0179-z(2018)

28

Figure7:Globalaverageannualinvestmentsindifferentclimatepolicies(left).incrementalinvestments

anddisinvestmentsbycategoryrelativetothebaseline(right).Source:IEA

Inordertoachievethe1,5°Ctarget,renewableenergyinvestments,onaverage,haveto

increaseupto550billioneveryyear.Incontrast,fossilenergydisinvestmentwouldneed

to be greater. Finally, to reach the Paris Agreement targets, low-carbon investments

wouldneedtoaccountformorethan50%ofallenergysupplyinvestmentsbyaround

2025andthenriseto80%orabovebyaround2035inthe1.5°Cscenarioor2050inthe

2°Cscenario.54

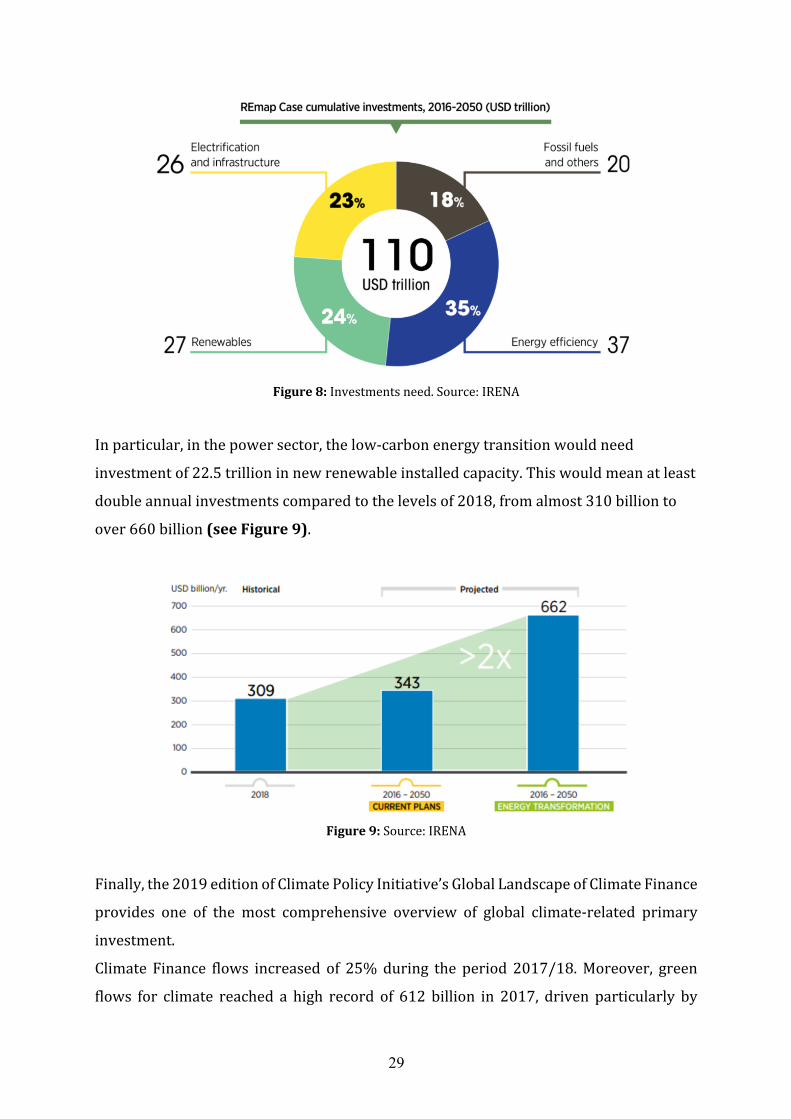

Moreover,IRENA(InternationalRenewableEnergyAgency)sustainsthatinordertomeet

thelow-carbonenergytransitiontheinvestmentsinrenewableenergyneedtobescaled

upsignificantly.Initslatestanalysis,“Globalenergytransformation:Aroadmapto2050”,

IRENAestimatesthat“toputtheworldontrackwiththeobjectivesoftheParisAgreement,

cumulative investment in renewable energy needs to reach 27 trillion in the 2016-2050

period”(seeFigure8).55

54 IIASA(2018)-WhatinvestmentsareneededintheglobalenergysysteminordertosatisfytheNDCsand2and1.5°Cgoals?55 IRENA(2019)-Globalenergytransformation:Aroadmapto2050(2019edition),InternationalRenewableEnergyAgency,AbuDhabi.

29

Figure8:Investmentsneed.Source:IRENA

Inparticular,inthepowersector,thelow-carbonenergytransitionwouldneed

investmentof22.5trillioninnewrenewableinstalledcapacity.Thiswouldmeanatleast

doubleannualinvestmentscomparedtothelevelsof2018,fromalmost310billionto

over660billion(seeFigure9).

Figure9:Source:IRENA

Finally,the2019editionofClimatePolicyInitiative’sGlobalLandscapeofClimateFinance

provides one of the most comprehensive overview of global climate-related primary

investment.

Climate Finance flows increased of 25%during the period 2017/18.Moreover, green

flows for climate reached a high record of 612 billion in 2017, driven particularly by

30

renewableenergycapacityadditions inChina, theU.S., and India, aswell as increased

publiccommitmentstolanduseandenergyefficiencyandthiswasfollowedbyan11%

dropin2018to546billion(seeFigure10).56

Figure10:Globalclimatefinanceflows2013-2018.Source:CPIReport

However,asdescribedbythereport,climatefinancehasreachedrecordlevelsbutnot

enoughwithrespecttowhatisneededundera1.5Cscenario.Estimatesoftheinvestment

required to achieve the low-carbon transition range from 1.6 trillion to 3.8 trillion

annually between 2016 and 205057, while the Global Commission on Adaptation58

estimatescostsof180billionannuallyfrom2020to2030.

2.2ClimateFinanceActors

AfterdescribingtheinvestmentsnecessaryfortheLow-CarbonEconomyTransition,itis

importanttounderstandwhotheactorsofclimatefinanceareandwhatroletheyhavein

theglobalcontext.

Twocategoriesofactorsarerecognizedatinternationallevel:publicactorsandprivate

actors. The first category comprises governments and their agencies, the so-called

“Development Finance Institutions” (DFIs) (national, multilateral and bilateral) and

56 CPI(2019)-GlobalLandscapeofClimateFinance2019[BarbaraBuchner,AlexClark,AngelaFalconer,RobMacquarie,ChaviMeattle,RowenaTolentino,CooperWetherbee].ClimatePolicyInitiative,London.57 IPCC(2018)-GlobalWarmingof1.5°C.AnIPCCSpecialReportontheimpactsofglobalwarmingof1.5°Cabovepre-industriallevelsandrelatedglobalgreenhousegasemissionpathways,inthecontextofstrengtheningtheglobalresponsetothethreatofclimatechange,sustainabledevelopment,andeffortstoeradicatepoverty58 GCA(2019)

31

climate funds. The second category is private actors: project developers, commercial

banks,financialorganizationsandintermediaries,multinationalcorporations,smalland

medium-sizedenterprises,cooperatives,entrepreneursandhouseholds,privateequiters

and venture capitalists and private institutional investors (pension funds, insurance

companies,foundations,etc.).

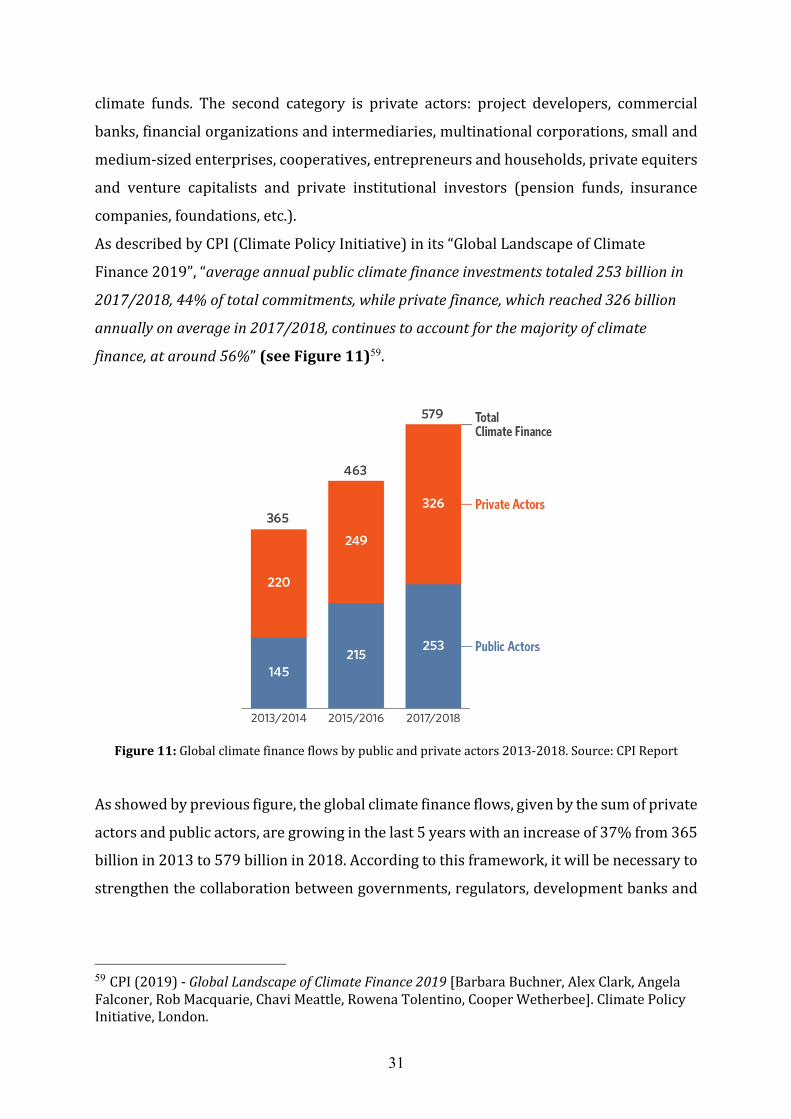

AsdescribedbyCPI(ClimatePolicyInitiative)inits“GlobalLandscapeofClimate

Finance2019”,“averageannualpublicclimatefinanceinvestmentstotaled253billionin

2017/2018,44%oftotalcommitments,whileprivatefinance,whichreached326billion

annuallyonaveragein2017/2018,continuestoaccountforthemajorityofclimate

finance,ataround56%”(seeFigure11)59.

Figure11:Globalclimatefinanceflowsbypublicandprivateactors2013-2018.Source:CPIReport

Asshowedbypreviousfigure,theglobalclimatefinanceflows,givenbythesumofprivate

actorsandpublicactors,aregrowinginthelast5yearswithanincreaseof37%from365

billionin2013to579billionin2018.Accordingtothisframework,itwillbenecessaryto

strengthenthecollaborationbetweengovernments,regulators,developmentbanksand

59 CPI(2019)-GlobalLandscapeofClimateFinance2019[BarbaraBuchner,AlexClark,AngelaFalconer,RobMacquarie,ChaviMeattle,RowenaTolentino,CooperWetherbee].ClimatePolicyInitiative,London.

32

private investors in order to match all financing with climate and sustainable

developmentgoals(SDGs).

2.2.1PublicFinanceActors

As described before, the definition of public finance actors includes governments and

theiragencies,theDevelopmentFinanceInstitutions(national,multilateralandbilateral)

andclimatefunds.

Investmentsbypublicactorsincreasedof18%,from215billionannuallyin2015to253

billionin2018.

DFIsprovide themajorityofpublic finance investments, contributingwith213billion

annually, compared to 194 billion in 2015/2016. Bilateral andmultilateral DFIs have

continuedincreasinginvestments(seeFigure12)by47%and24%,respectively.Finally,

Government Budgets and Agencies doubled the financing up to 42 billion in 2018,

contributingfor15%ofpublicflows.ClimatefundsincreasedannualfinancingtoUSD3.2

billionin2017/2018,43%morewithrespectto2015/2016.60

Figure12:PublicSourcesandIntermediariesofClimateFinance(USDbillion).Source:CPI

Inthisframework,publicactorscanoperateintwodifferentways:throughpublicfinance

methodsorpublicpolicy.Thefirstwayisadirectfinancingfrompublicinterventions,by

governmentsorfirmsownedbythestate.Examplesofpublicfinancearegrants, loans

andbonds,debtbonds,equityinvestments.

60 CPI(2019)-GlobalLandscapeofClimateFinance2019[BarbaraBuchner,AlexClark,AngelaFalconer,RobMacquarie,ChaviMeattle,RowenaTolentino,CooperWetherbee].ClimatePolicyInitiative,London.

33

Incontrast,publicpolicymethodsofferdifferentsourcestofinanceclimateprojects.In

thisway,apublicactorshouldcreateincentivesthatareattractivetoprivateinvestors.

Examplesofpublicpolicyareregulatoryandfiscalpolicies,suchastheEuropeanGreen

DealandtheFinancingSustainableGrowthissuedbytheEuropeanCommission.

2.2.1.1FinancingSustainableGrowthandTheGreenDeal

TheEUvisionontheroleof finance insustainabledevelopment isrepresentedby the

implementationofthe“ActionPlan”andthe“EuropeanGreenDeal”.

On8March2018, theEuropeanCommission issued theFinancingSustainableGrowth

(ActionPlan) inorder to finance sustainable growth. Inparticular, thepurposeof the

“ActionPlan”istoimplementafinancialsysteminordertosupporttheEuropeanUnion’s

activities on climate and sustainable development. The Plan represented a key step

towards the implementation of the Paris Agreement and the UN Agenda 2030 for

SustainableDevelopmentandcontributestothesustainabledevelopmentobjectivesset

outintheCommissionCommunication"Europe’ssustainablefuture:nextsteps.European

actioninfavourofsustainability".

ThePlanaimstomeetthreechallenges:

- orientinginvestmentflowstowardssustainabilitytoachievegreengrowth;

- integratingsustainabilityintoriskmanagement;

- fosteringtransparencyandlong-termvisionineconomicandfinancialactivities.

Thesethreeobjectivesarefollowedbytenspecificactionsthatshouldfacilitatetoachieve

them:

1) establishinganEUclassificationsystemforsustainableactivities,

2) creatingstandardsandlabelsforgreenfinancialproducts,

3) fosteringinvestmentinsustainableproducts,

4) incorporatingsustainabilitywhenprovidingfinancialadvice,

34

5) developingsustainabilitybenchmark,

6) anewsystemofratingsbasedonsustainabilityfactors,

7) clarifyingdutiesofinstitutionalinvestorsandassetmanagers,

8) incorporatingsustainabilityinprudentialrequirements,

9) strengtheningsustainabilitydisclosureandaccountingrule-making,

10) fostering sustainable corporate governance and attenuating short-termism in

capitalmarkets.

Inparticular,forthepurposeofthisresearch,thecreationofEUGreenBondsstandards

andlabelsforgreenfinancialproductsiscrucial.Basedonthefinalreportandusability

guideoftheTechnicalExpertGroup(TEG),theCommissionisexploringthedevelopment

ofavoluntaryEUGreenBondStandard.Moreover,theCommissionisworkingonanEU

Ecolabel for retail investment products. The extension of the Ecolabel framework to

financialproducts,bywayofaCommissionDecision,isexpectedforQ32021.61

ThepolicyareasoftheActionPlanare:

- Environment:first,withregardtothemitigationofclimatechange,aswellasthe

wider environment and the risks associated with it. Climate change and the

response to it by the public sector and society in general have led to the

identificationofnewsourcesoffinancialriskthattheregulatoryandsupervisory

communityispayingmoreattentionto;

- Social and governance: where the hottest issues are equity, inclusiveness,

working conditions and relationships, investment in human capital and

community.

61 EuropeanCommission(2020)-Renewedsustainablefinancestrategyandimplementationoftheactionplanonfinancingsustainablegrowth

35

In 2019, the European Commission President Ursula von der Leyen has promised to

strengthenEUclimatepolicy62.SheproposedaEuropeanClimateLawthat“wouldrequire

theEUtobecomeclimateneutralby2050,makingEuropethefirstcontinenttoreachthis

goal.Thestepstogettotheclimateneutralityrequireacomprehensivepolicy,comprising

climate, energy, environmental, industrial, economic and social aspects of this

unprecedentedprocess.ThisiswhattheEuropeanGreenDealisabout.”63

Concretely, the European Green Deal represents a “strategy”, a series ofmeasures of

differentnature,includingnewlawsandinvestmentsthatwillbeimplementedinthenext

thirtyyears.At themoment, theCommissionhasmadepreciseplans for the first two

years,themostimportantonebeingthesetupofastructurecapableofsupportingsuch

anambitiousproject.TheGreenDealwillbefundedwithalargeamountofpublicand

privatemoney.Inthefirsttenyears,theobjectivewillbetomobilizeabout1000billion

tofinanceit,moreorless100billionperyear.

Themainobjectiveistolimittheincreaseinglobalwarming,whichhastoremainwithin

1.5°Ccomparedtothepre-industrialyears,accordingtotheestimatesoftheIPCC.To

meetthistarget,theEuropeanUnionhascommitteditselftoputtozeroitsnetpollutant

emissionsby2050,andtomeetintermediatetargetsfor2030and2040.Fromthismain

objective,aseriesofconsequentmorespecificmovesshouldderive(seeFigure13).

62 vonderLeyen,Ursula(2019)-AUnionthatstrivesformore:MyagendaforEurope,PoliticalGuidelinesfortheNextEuropeanCommission2019-2024 63 GrégoryClaeys,SimoneTagliapietraandGeorgZachmann(2019)-HowtomaketheEuropeanGreenDealwork

36

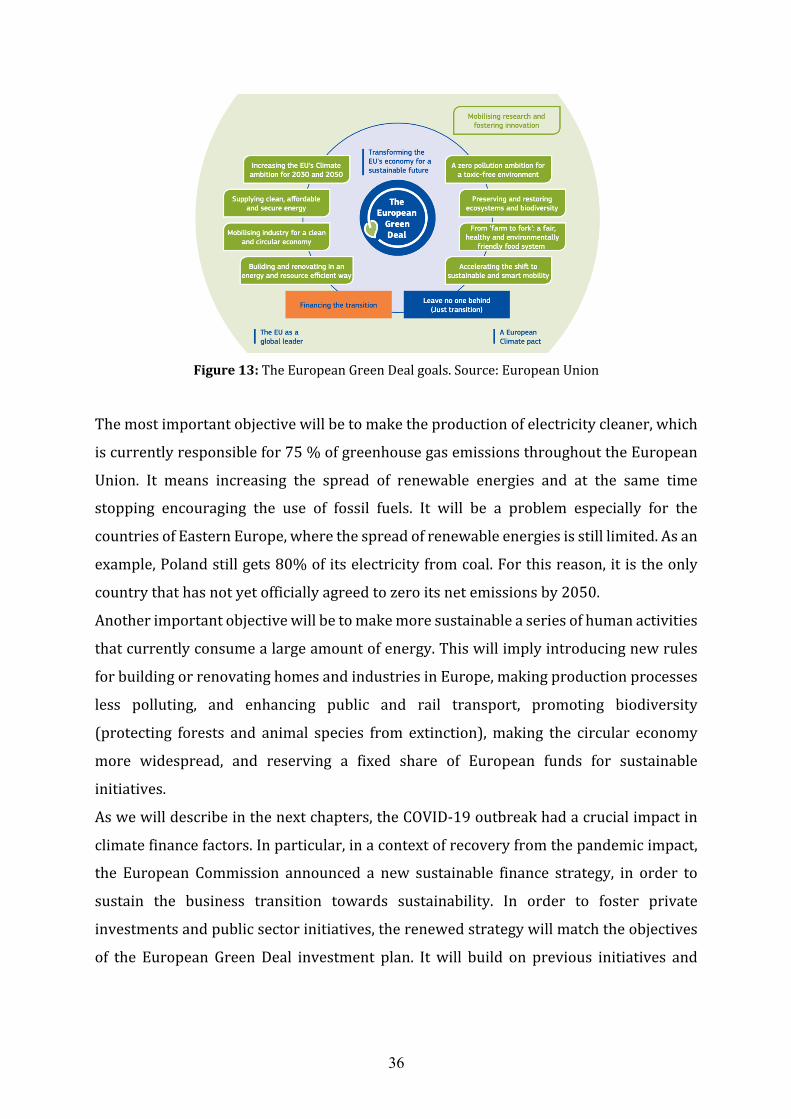

Figure13:TheEuropeanGreenDealgoals.Source:EuropeanUnion

Themostimportantobjectivewillbetomaketheproductionofelectricitycleaner,which

iscurrentlyresponsiblefor75%ofgreenhousegasemissionsthroughouttheEuropean

Union. It means increasing the spread of renewable energies and at the same time

stopping encouraging the use of fossil fuels. It will be a problem especially for the

countriesofEasternEurope,wherethespreadofrenewableenergiesisstilllimited.Asan

example,Polandstillgets80%ofitselectricityfromcoal.Forthisreason,itistheonly

countrythathasnotyetofficiallyagreedtozeroitsnetemissionsby2050.

Anotherimportantobjectivewillbetomakemoresustainableaseriesofhumanactivities

thatcurrentlyconsumealargeamountofenergy.Thiswillimplyintroducingnewrules

forbuildingorrenovatinghomesandindustriesinEurope,makingproductionprocesses

less polluting, and enhancing public and rail transport, promoting biodiversity

(protecting forests and animal species from extinction),making the circular economy

more widespread, and reserving a fixed share of European funds for sustainable

initiatives.

Aswewilldescribeinthenextchapters,theCOVID-19outbreakhadacrucialimpactin

climatefinancefactors.Inparticular,inacontextofrecoveryfromthepandemicimpact,

the European Commission announced a new sustainable finance strategy, in order to

sustain the business transition towards sustainability. In order to foster private

investmentsandpublicsectorinitiatives,therenewedstrategywillmatchtheobjectives

of the European Green Deal investment plan. Itwill build on previous initiatives and

37

reports,suchastheactionplanonfinancingsustainablegrowthandthereportsofthe

TechnicalExpertGrouponSustainableFinance(TEG).64

2.2.2PrivateFinanceActors

Thedefinitionofprivateactorscompriseshouseholds,non-financialcorporations,banks

(financial institutions), institutional investors (asset managers, insurance companies)

andprivateequity,venturecapitalandinfrastructurefunds.

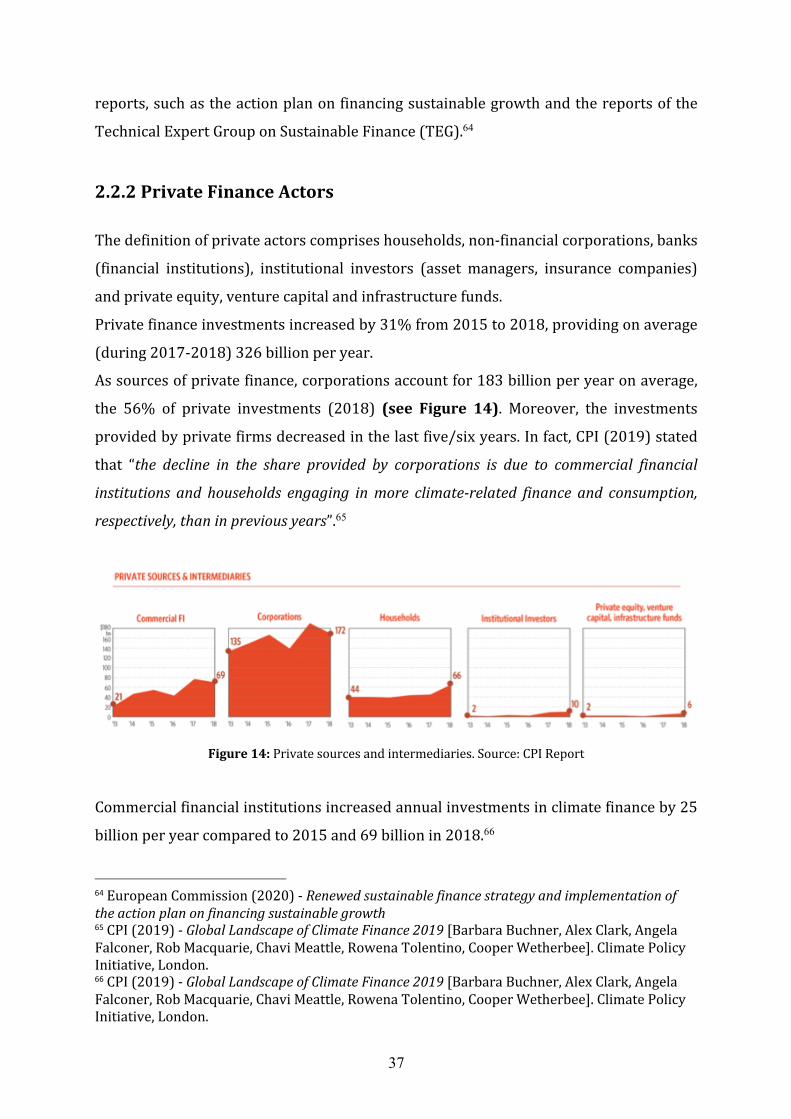

Privatefinanceinvestmentsincreasedby31%from2015to2018,providingonaverage

(during2017-2018)326billionperyear.

Assourcesofprivatefinance,corporationsaccountfor183billionperyearonaverage,

the 56% of private investments (2018) (see Figure 14). Moreover, the investments

providedbyprivatefirmsdecreasedinthelastfive/sixyears.Infact,CPI(2019)stated

that “the decline in the share provided by corporations is due to commercial financial

institutions and households engaging inmore climate-related finance and consumption,

respectively,thaninpreviousyears”.65

Figure14:Privatesourcesandintermediaries.Source:CPIReport

Commercialfinancialinstitutionsincreasedannualinvestmentsinclimatefinanceby25

billionperyearcomparedto2015and69billionin2018.66

64 EuropeanCommission(2020)-Renewedsustainablefinancestrategyandimplementationoftheactionplanonfinancingsustainablegrowth 65 CPI(2019)-GlobalLandscapeofClimateFinance2019[BarbaraBuchner,AlexClark,AngelaFalconer,RobMacquarie,ChaviMeattle,RowenaTolentino,CooperWetherbee].ClimatePolicyInitiative,London. 66 CPI(2019)-GlobalLandscapeofClimateFinance2019[BarbaraBuchner,AlexClark,AngelaFalconer,RobMacquarie,ChaviMeattle,RowenaTolentino,CooperWetherbee].ClimatePolicyInitiative,London.

38

Thegrowthofinvestmentsbybanksreflectsthetransitiontosustainabilityinfinancial

markets,inparticularforrenewableenergies,whichrepresent93%ofbankinvestments

in climate finance during 2017-2018. Although investments in renewable energy are

growing,themajorityofbankinvestmentsarerepresentedbyloans(650billion)tofossil

fuelcompanies67.

Althoughtheygobeyondthescopeofdirectprojectfinance,thesefiguresindicatethat

commerciallendersstillhavetoimplementamajorshiftininvestmentstrategytoalign

theirfinancingactivitieswithdecarbonizationpathwaysundertheParisAgreement.68

Finally,aswecanseeinthelastgraph,privateequity,venturecapitalandinfrastructure

fundsdoubledtheirinvestmentsinthelast5years,from2billionof2013to6billionof

2018.Alsointhissector,75%oftheinvestmentsareaddressedtorenewableenergies.

Thisrapidincreaseshowsthegrowthofrenewableenergymarketsandalowerperceived

risksamonginternationalinvestors.

2.2.3TheimportanceofPublicandPrivaterelationship

Aspreviouslyshowed,themajorityofinvestmentsintheclimatefinancesectoraremade

byprivateactors.Asaconsequence,theprivatesectorplaysacentralroleinfinancing

mitigationandadaptationactionsinmostcountries.

Theprivatesector,however,tendstoinvest incountrieswithawell-developedcapital

market,whereregulationisclearandwheretherearelowtransactioncostsandstable

prices,i.e.countrieswithlowcountryandcurrencyrisks.Suchrisksarefrequentlyhigh

in developing countries, where there is a high need for investment, especially in

adaptationactions.Public interventionbynationaland internationalgovernmentsand

bankstoencourageprivateinvestmentisthereforecrucial.

Appropriate policies and common actions between public and private sectors allow

mobilizingfinancialresourcesandhumancapitalandtocreateanenvironmentsuitable

for attracting private investment through a clear and stable regulatory framework.

Finally,risk-sharingthroughpublic-privaterelationshipsisveryimportant,especiallyin

67 RAN,Banktracketal.(2019)-BankingonClimateChange–fossilfuelfinancereportcard2019relationsandglobalclimatechange68 CPI(2019)-GlobalLandscapeofClimateFinance2019[BarbaraBuchner,AlexClark,AngelaFalconer,RobMacquarie,ChaviMeattle,RowenaTolentino,CooperWetherbee].ClimatePolicyInitiative,London.

39

thecaseofgreeninvestments,whichoftenrequiresubstantialinitialfundingandsuffer

fromamoreuncertainandlongerreturnoninvestment.