formation - fatca application aux fonds et sociétés de ... · de gestion du secteur immobilier...

TRANSCRIPT

Formation - FATCA Application aux fonds et sociétés de gestion du secteur immobilier

28 novembre 2014

www.landwell.fr

PwC

Sommaire

• Qu’est ce que FATCA ? • Les accords inter-gouvernementaux en de mise en

œuvre de FATCA (les « IGA ») • Le cadre juridique de FATCA • L’IGA France --- Etats-Unis • Les obligations FATCA en France • Le secteur de l’Asset Management • Les spécificités immobilières • Annexes

www.landwell.fr

Qu’est ce que FATCA ?

3

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• Lutter contre l’évasion fiscale des contribuables américains détenant des avoirs financiers à l’étranger

• S’inscrire dans un contexte international favorable: G20 Londres, liste OCDE des paradis fiscaux, …

• Financer la restauration des finances publiques américaines dans le cadre des politiques de relance

Les études menées par l’IRS confirment que plus l’IRS fait appel à des tiers pour recouper ses informations, plus le taux de fraude fiscale des contribuables US est faible

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Qu’est ce que FATCA ?

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Qu’est ce que FATCA ?

• Genèse : Dispositif légal américain adopté en Mars 2010 à portée extraterritoriale

• Objet : Lutte contre l’évasion fiscale des contribuables américains détenant des actifs /comptes financiers gérés à l’étranger

• Mode opératoire:

- Obtenir des informations des agents financiers étrangers pour les confronter aux déclarations fiscales spontanées des US persons

- Des obligations crées par la loi Fatca et reprises par un contrat entre les institutions financières Non-américaines (« Foreign Financial Institutions » ou FFI) et l’IRS

◦ Identifier les titulaires de comptes/d’avoirs US persons à l’administration fiscale américaine (l’IRS).

◦ Reporting annuels des avoirs détenus et des revenus perçus par les US persons

◦ Application une retenue à la source de 30%

• Entrée en vigueur : 1er juillet 2014

Divider

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

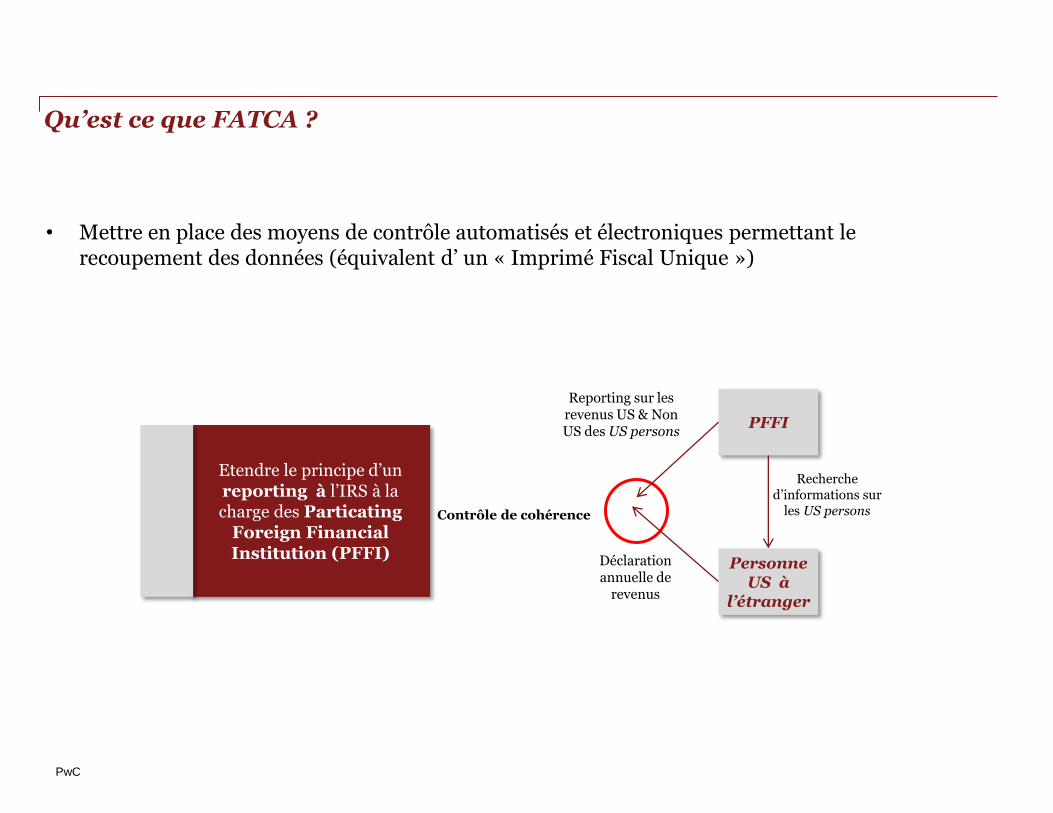

PFFI

Déclaration annuelle de

revenus

Reporting sur les revenus US & Non US des US persons

Recherche d’informations sur

les US persons

Personne US à

l’étranger

• Mettre en place des moyens de contrôle automatisés et électroniques permettant le recoupement des données (équivalent d’ un « Imprimé Fiscal Unique »)

Contrôle de cohérence

Etendre le principe d’un reporting à l’IRS à la charge des Particating

Foreign Financial Institution (PFFI)

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Qu’est ce que FATCA ?

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

•Un mécanisme visant à lutter contre l’évasion fiscale des personnes US percevant des revenus et détenant des avoir à l’étranger

Centralisation des déclarations des PFFIs

La finalité: un contrôle de cohérence entre les déclarations des contribuables US et les éléments transmis par les institutions financières non US participantes (PFFI)

concernant les revenus et les avoirs de ces contribuables

PFFI

PFFI PFFI

PFFI

PFFI

PFFI

PFFI

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Qu’est ce que FATCA ?

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Qu’est ce que FATCA ?

• Sanction prévue :

1. Retenue à la source appliquée par les agents financiers Américains en cas de paiement reçu dans un compte ouvert dans un FFI non-conforme à Fatca

2. Retenue à la source devant être appliquée par un FFI

◦ (i) sur les revenus perçus par ses clients récalcitrants -titulaires de comptes

◦ (ii) sur les paiements adressés à des FFIs non-conformes à Fatca

un dispositif d’une grande efficacité

• Evolution de l’approche unilatérale américaine :

- Souhait des Etats-Unis de créer une dynamique de collaboration, actée par une convention, avec autant d’Etats-partenaires que possible

- Souhait d’un certain nombres d’Etats de collaborer, moyennant un engagement réciproque , des Etats-Unis

Divider

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• 18 mars 2010 : Hire Act

• 7 juin 2011 : L’AFG adresse un courrier à l’IRS sur les problématiques liés à l’organisation de la gestion en

France

• 8 février 2012 : Publication du projet de réglementation

• 18 février 2012 : 5 Etats , dont la France, font une déclaration commune relative à une approche intergouvernementale de Fatca

• 26 juillet 2012 : Publication du modèle #1 d’accord avec 5 Etats pour l’application de Fatca

• 12 septembre 2012 : Signature du 1er IGA (USA et le RU)

• 8 novembre 2012 : Les USA annoncent des négociations d’IGA avec plus de 50 Etats

• 6 décembre 2012 : La Commission européenne publie un « Plan d’action pour renforcer la lutte contre la fraude et l’évasion fiscales »

• 19 avril 2013 : les ministres des finances du G20 approuvent l’échange automatique d‘informations et demandent à l’OCDE de préparer un modèle standardisé

• Été 2013 : concertation DGFIP/ secteur financier sur le cahier des charges du reporting Fatca

• 14 novembre 2013 : Signature de l’IGA France-USA

• 12 décembre 2013: Réunion ASPIM/AFG/DGFIP sur l’application de FATCA aux fonds immobiliers

• 8 août 2014: Publication d’une loi de finances rectificative qui contient des dispositions d’application de Fatca

• 29 octobre 2014: Adoption par 51 Etats de l’OCDE d’un modèle de traité d’échanges automatisés d’informations fiscales (Common Reporting Standard)

Qu’est ce que FATCA ?

www.landwell.fr

Les accords inter-gouvernementaux en de mise en œuvre de FATCA (les « IGA »)

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Les accords inter-gouvernementaux en vue de mettre en place FATCA et d’améliorer le reporting fiscal international (les « IGA »)

• Structure d’un IGA

- Le corpus du traité

◦ Définitions, définition des obligations d’échanges d’informations, périodicité et modalités des échanges d’informations, …

- Annexe 1: Le processus de due diligence pour l’identification de « l’américanité » des personnes physiques et des entités

- Processus distinct pour les comptes-clients ouverts au 1er juillet 2014 et ceux ouverts après

◦ ‘Stock’ de comptes-clients au 1er juillet 2014: Définition du processus de due diligences attendu

◦ Nouveaux comptes-clients ouverts à partir du 1er juillet 2014: Nouvelles procédures à mettre en œuvre de façon pérenne

- Annexe 2 : Liste des types d’institutions financières considérées comme exonérées, réputées conformes ou bénéficiant d’un régime « allégé » (« Non-Reporting FIs/Deemed compliant ») et liste des produits financiers exonérés

• Portée territoriale

• l’IGA France/Etats-Unis ne s’appliquera pas aux succursales à l’étranger des FFI français

• Application aux succursales en France de FFI étrangers (même si l’état du siège n’a pas signé d’IGA)

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

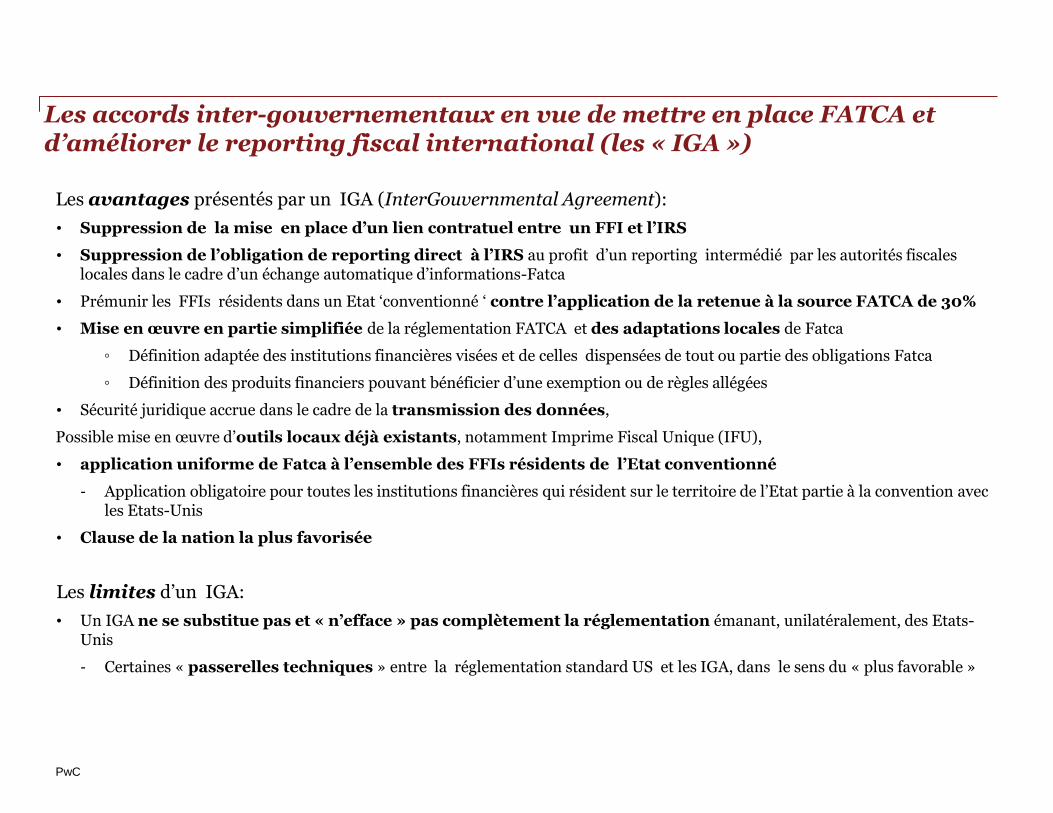

Les accords inter-gouvernementaux en vue de mettre en place FATCA et d’améliorer le reporting fiscal international (les « IGA »)

Les avantages présentés par un IGA (InterGouvernmental Agreement):

• Suppression de la mise en place d’un lien contratuel entre un FFI et l’IRS

• Suppression de l’obligation de reporting direct à l’IRS au profit d’un reporting intermédié par les autorités fiscales locales dans le cadre d’un échange automatique d’informations-Fatca

• Prémunir les FFIs résidents dans un Etat ‘conventionné ‘ contre l’application de la retenue à la source FATCA de 30%

• Mise en œuvre en partie simplifiée de la réglementation FATCA et des adaptations locales de Fatca

◦ Définition adaptée des institutions financières visées et de celles dispensées de tout ou partie des obligations Fatca

◦ Définition des produits financiers pouvant bénéficier d’une exemption ou de règles allégées

• Sécurité juridique accrue dans le cadre de la transmission des données,

Possible mise en œuvre d’outils locaux déjà existants, notamment Imprime Fiscal Unique (IFU),

• application uniforme de Fatca à l’ensemble des FFIs résidents de l’Etat conventionné

- Application obligatoire pour toutes les institutions financières qui résident sur le territoire de l’Etat partie à la convention avec les Etats-Unis

• Clause de la nation la plus favorisée

Les limites d’un IGA:

• Un IGA ne se substitue pas et « n’efface » pas complètement la réglementation émanant, unilatéralement, des Etats-Unis

- Certaines « passerelles techniques » entre la réglementation standard US et les IGA, dans le sens du « plus favorable »

Divider

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

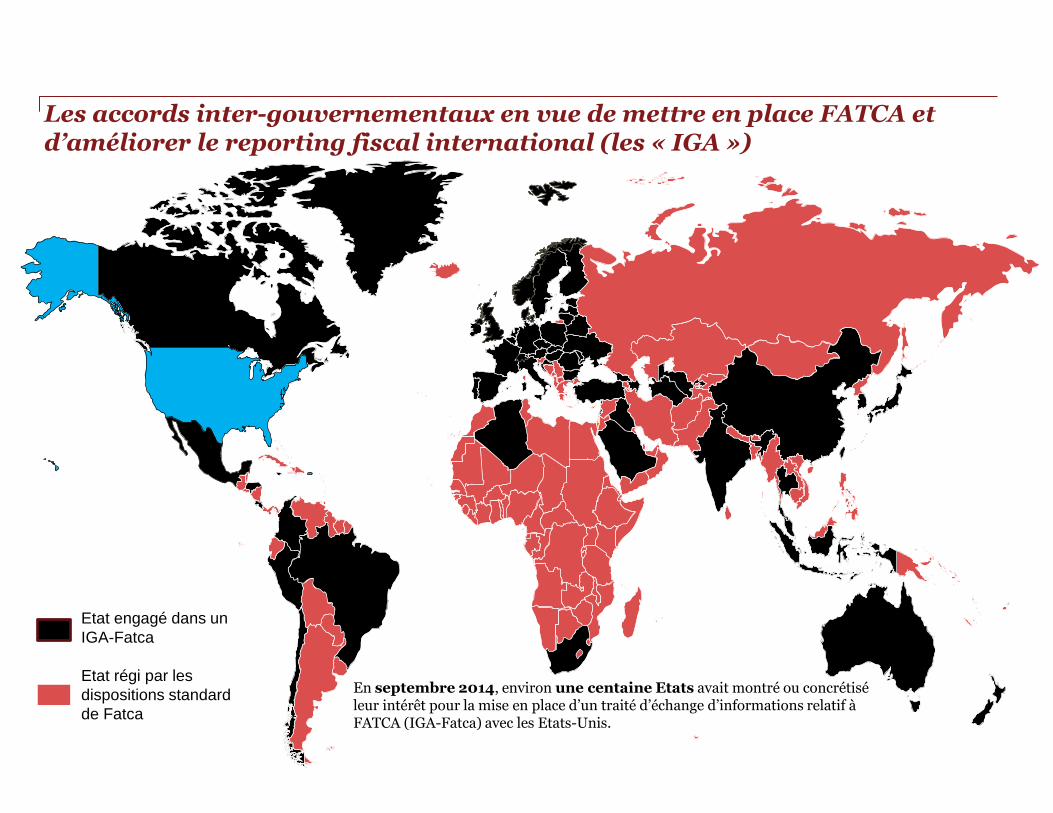

Etat engagé dans un

IGA-Fatca

Etat régi par les

dispositions standard

de Fatca

En septembre 2014, environ une centaine Etats avait montré ou concrétisé leur intérêt pour la mise en place d’un traité d’échange d’informations relatif à FATCA (IGA-Fatca) avec les Etats-Unis.

Les accords inter-gouvernementaux en vue de mettre en place FATCA et d’améliorer le reporting fiscal international (les « IGA »)

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Les accords inter-gouvernementaux en vue de mettre en place FATCA et d’améliorer le reporting fiscal international (les « IGA »)

• Etats signataires d’un IGA-Fatca (novembre 2014):

Afrique du Sud, Allemagne, Australie, Autriche*, Belgique, Bermudes*, Canada, Caïmans, Chili*, Costa Rica, Danemark, Estonie, Espagne, Finlande, France, Gibraltar, Guernesey, Hongrie, Honduras, Île de Man, Îles Vierges britanniques, Irlande, Israël, Italie, Jamaïque, Japon*, Jersey, Liechtenstein, Luxembourg, Malte, Maurice, Mexique, Norvège, Nouvelle-Zélande, Pays-Bas, Royaume-Uni, Slovénie, Suisse*

• Les Etats suivants, bien que n’ayant pas encore signé d’IGA, peuvent être considérés comme inclus dans la liste des signataires :

Algérie, Anguilla, Antigua-et-Barbuda, Arabie Saoudite, Arménie*, Azerbaïdjan, Bahamas, Bahreïn, Barbade, Bélarusse, Brésil, Bulgarie, Cap Vert, Chine, Colombie, Corée du Sud, Croatie, Curaçao, Chypre, la Dominique, République Dominicaine, Émirats Arabes Unis, Géorgie, Groënland, Grenade, Guyane, Haïti, Hong Kong*, Inde, Indonésie, Irak*, Kosovo, Koweït, Malaisie, Moldavie*, Monténégro, Nicaragua*, Lituanie, Ouzbékistan, Panama, Paraguay*, Pérou, Pologne, Portugal, Qatar, Roumanie, Saint-Kitts-et-Nevis, Sainte-Lucie, Saint-Vincent-et-les Grenadines, Serbie, Seychelles, Saint-Marin*, Singapour, République Slovaque, Suède, Taiwan*, République Tchèque, Thaïlande, Turquie, Turkménistan, Îles Turques et Caïques, Ukraine.

• Les pays en gras sont signataires ou négocient des IGA de modèle 2.

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

www.landwell.fr

Le cadre juridique de FATCA

Les dispositions standards de FATCA

Hiring Incentives to Restore Employment Act (‘HIRE’ Act), 18 mars 2010 codifié au chapitre 4 (sections 1471 through 1474) du code fiscal US

contient les dispositions sur du Foreign Account Tax Compliance Act (FATCA)

Treasury Regulations §1.1471 - §1.1474

Refonte du régime Qualified Intermediary (Q.I.) (établissements de crédit)

Cadre juridique de FATCA

BANQUES DEPOSITAIRES /

FIDUCIAIRES

FONDS ET

SOCIETES DE GESTION

ASSUREURS

Les acteurs du secteur financier visés, dans le dispositif FATCA-standard:

Détenir des actifs financiers pour le compte de tiers

Entités recevant des dépôts dans l’exercice normal d’une activité bancaire ou similaire

Transactions sur certaines classes d’actifs financiers; gestion de portefeuille; opérations d'investissement, d'administration

Assureur proposant des produits d’assurance s ayant une cash value

HOLDINGS et CENTRES DE TRESORERIE

14 novembre 2013: Signature d’un accord (I.G.A.) entre la France et les Etats-Unis

Transposition de FATCA en France, ainsi rendu obligatoire pour l’ensemble des entités financières résidentes en France

Toutes les entités Françaises du secteur financier visé

les succursales en France de sociétés étrangères du secteur financier visé

Réciprocité des échanges d’informations avec les Etats-Unis

Protection des institutions financières contre l’application, à leur niveau, de la retenue à la source FATCA de 30% (sauf infraction significative)

Entrée en vigueur

Adoption de certaines mesures d’application de l’I.G.A.

1ere loi de finances rectificative pour 2014

Habilitation légale et obligation des institutions financières de fournir et déclarer les informations nécessaires aux échanges internationaux automatiques d'informations à des fins fiscales

200€ d’amende par compte déclarable comportant une ou plusieurs informations omises ou erronées, sauf manquement dû à client ou de la personne concernée

Cahier des charges informatiques du format de reporting (projet)

Instruction fiscale: en attente

Cadre juridique de FATCA Dispositions Françaises

DISPOSITIONS DU CGI CONCERNANT FATCA

Article 1649 AC du CGI –(loi de finances rectificative pour 2014, loi n°2014-891 du 08.08.2014) -« Les teneurs de compte, les organismes d'assurance et assimilés et toute autre institution financière mentionnent, sur une déclaration déposée dans des conditions et délais fixés par décret, les informations requises pour l'application des conventions conclues par la France permettant un échange automatique d'informations à des fins fiscales. Ces informations peuvent notamment concerner tout revenu de capitaux mobiliers ainsi que les soldes des comptes et la valeur de rachat des bons ou contrats de capitalisation et placements de même nature.

Afin de satisfaire aux obligations mentionnées au premier alinéa, ils mettent en œuvre, y compris au moyen de traitements de données à caractère personnel, les diligences nécessaires en matière d'identification et de déclaration des comptes, des paiements et des personnes.

Ces traitements éventuels sont soumis à la loi n° 78-17 du 6 janvier 1978 relative à l'informatique, aux fichiers et aux libertés.»

Cette disposition légitime les institutions financières à opérer des traitements automatisés afin d'identifier les contribuables visés et les comptes concernés dans le cadre de leur obligation déclarative,

Il donne ainsi un fondement légal aux diligences d'identification des contribuables et des comptes visés que les institutions financières sont amenées à accomplir dans le cadre de l'échange automatique d'informations, notamment en procédant à des traitements automatisés de données à caractère nominatif.

Ces traitements sont soumis à la loi 78-17 du 6 janvier 1978 relative à l'informatique, aux fichiers et aux libertés

Article 1736 du CGI « I.-5. Tout manquement à l'obligation déclarative prévue à l'article 1649 AC est sanctionné par une amende fiscale de 200 € par compte déclarable comportant une ou plusieurs informations omises ou erronées.

Toutefois, la sanction mentionnée au premier alinéa du présent 5 n'est pas applicable lorsque le teneur de compte, l'organisme d'assurance et assimilé ou l'institution financière concernée établit que ce manquement résulte d'un refus du client ou de la personne concernée de lui transmettre les informations requises et qu'il a informé de ce manquement l'administration des impôts. »

Cadre juridique de FATCA Dispositions Françaises

www.landwell.fr

L’IGA France --- Etats-Unis

Les obligations FATCA en France

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• Par un processus de due diligence précisé par l’IGA, identifier • les personnes physiques Américaines • … et les entités substantiellement détenues par des Américains

=> Comptes-clients pré-existants au 1er juillet 2014 =>… et toute nouvelle ouverture de compte-client depuis le 1er juillet 2014 (1er janvier 2015 pour les comptes détenus par les entités)

• Qualité de l’ information, de la documentation et des données • Identifier le statut-Fatca des relations d’affaires/partenaires financiers/contreparties: PFFI, NPFFI, DC

FFI, NFFE, …

• Reporting annuel sur l’ensemble des comptes Américains identifiés lors du processus de Due diligence

• Reporting des paiements effectués au profit de NPFFIs

Les obligations-FATCA en France

(3) Obligations de

Reporting

(2) Obligations de

Due diligence

• S’enregistrer sur le site de l’IRS • S’enregistrer en tant que groupe-Fatca, le cas échéant • Avant le 22 décembre 2014, dernier délai • Pour les entités financières visées et non-éligibles à un statut allégé

(1) Obligation de

s’enregistrer

auprès de l’IRS

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

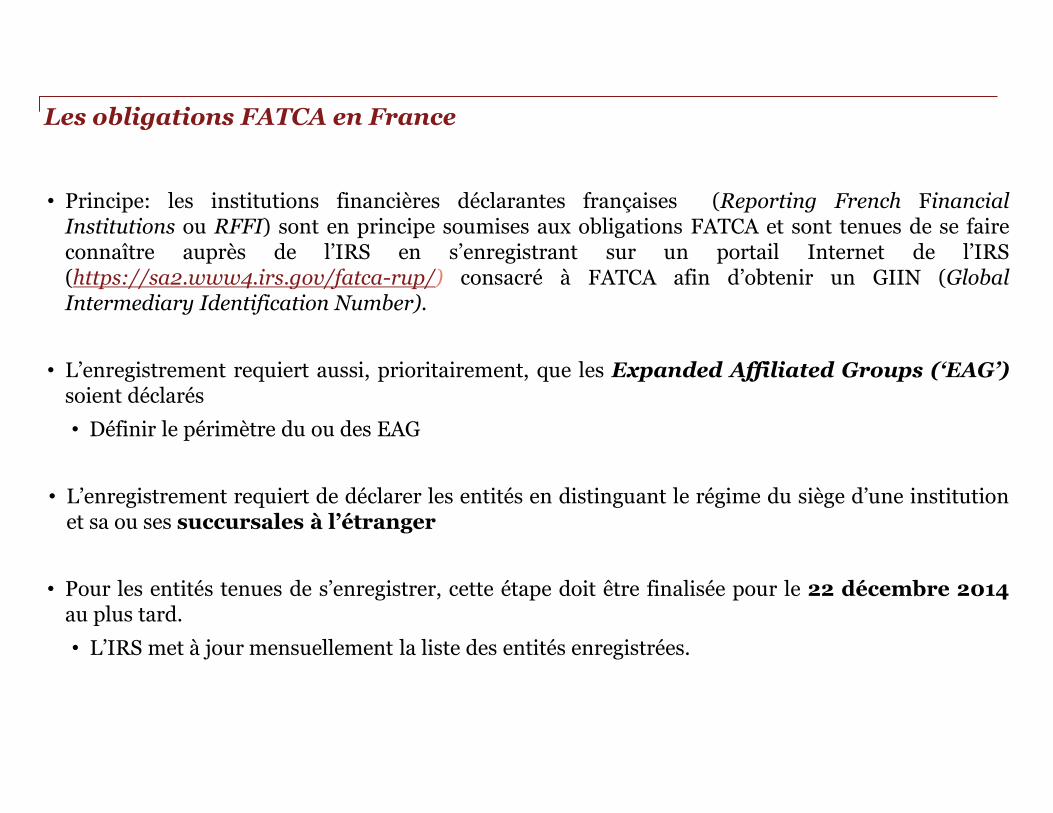

• Principe: les institutions financières déclarantes françaises (Reporting French Financial Institutions ou RFFI) sont en principe soumises aux obligations FATCA et sont tenues de se faire connaître auprès de l’IRS en s’enregistrant sur un portail Internet de l’IRS (https://sa2.www4.irs.gov/fatca-rup/) consacré à FATCA afin d’obtenir un GIIN (Global Intermediary Identification Number).

• L’enregistrement requiert aussi, prioritairement, que les Expanded Affiliated Groups (‘EAG’) soient déclarés

• Définir le périmètre du ou des EAG

• L’enregistrement requiert de déclarer les entités en distinguant le régime du siège d’une institution et sa ou ses succursales à l’étranger

• Pour les entités tenues de s’enregistrer, cette étape doit être finalisée pour le 22 décembre 2014 au plus tard.

• L’IRS met à jour mensuellement la liste des entités enregistrées.

Les obligations FATCA en France

Les obligations FATCA en France

EAG

• Mécanisme permettant a priori de simplifier la mise en place du FATCA

• Groupe construit selon le critère suivant: lien de détention/intérêt supérieur à

50% (droits en capital ET droits de vote)

• Portée du groupe FATCA: ► La déclaration d’existence et composition du groupe est centralisée

► La tête de groupe peut prendre une responsabilité de supervision des

procédures FATCA mises en place par les membres de son groupe

• Les membres du groupe conservent individuellement leurs

obligations/responsabilités de due dilligence, de reporting et de retenue à la

source, chacun selon ses dispositions-FATCA nationales

• ! Risque de contagion entre entités membre d’un groupe si l’une d’elle

n’est plus en conformité

Expanded Affilated Group

« Groupe Etendu d’Affiliés »

Section 1471 (e), 1504 IRC

• La notion de Groupe-FATCA (« Expanded Affiliated Group », EAG ) inclut l’ensemble des entités détenues directement ou indirectement à plus de 50 % en valeur ET en droit de vote

• Même en étant membre d’un EAG, chaque entité conserve le reste des obligations FATCA: identification, retenue à la source et reporting

• Lorsque l’on crée un EAG, il est nécessaire de désigner un « "Lead FFI" »

• Processus coordonné d’entrée au régime FATCA

Désignation d’un « Lead FFI »

Le "Lead FFI" s’engage personnellement à être un PFFI ou DCFFI

Le "Lead FFI" doit notifier à l’IRS les nouveaux membres et les membres sortants.

Le "Lead FFI" devra fournir certaines informations sur les membres (eg activités menées, statut préexistant QI, NFFE, …)

• Un point de contact unique pour tous les membres

Le "Lead FFI" peut désigner d’autres membres du groupe comme point de contact d’un « sous-groupe » particulier (ex : pays ou ligne de métier).

Responsabilité particulière en matière de communication avec l’IRS sur la certification Deemed Compliant FFI.

« "Lead FFI" »

• Différents rôles sont prévus au sein des groupes :

Rôle de Lead FFI : procédure coordonnée de mise en place du FATCA dans le groupe

Rôle du Point of Contact - FFI : point de contact central avec l’IRS pour le groupe FFI

Rôle du Compliance FFI : surveillance du respect de la conformité de la réglementation FATCA

Les obligations FATCA en France

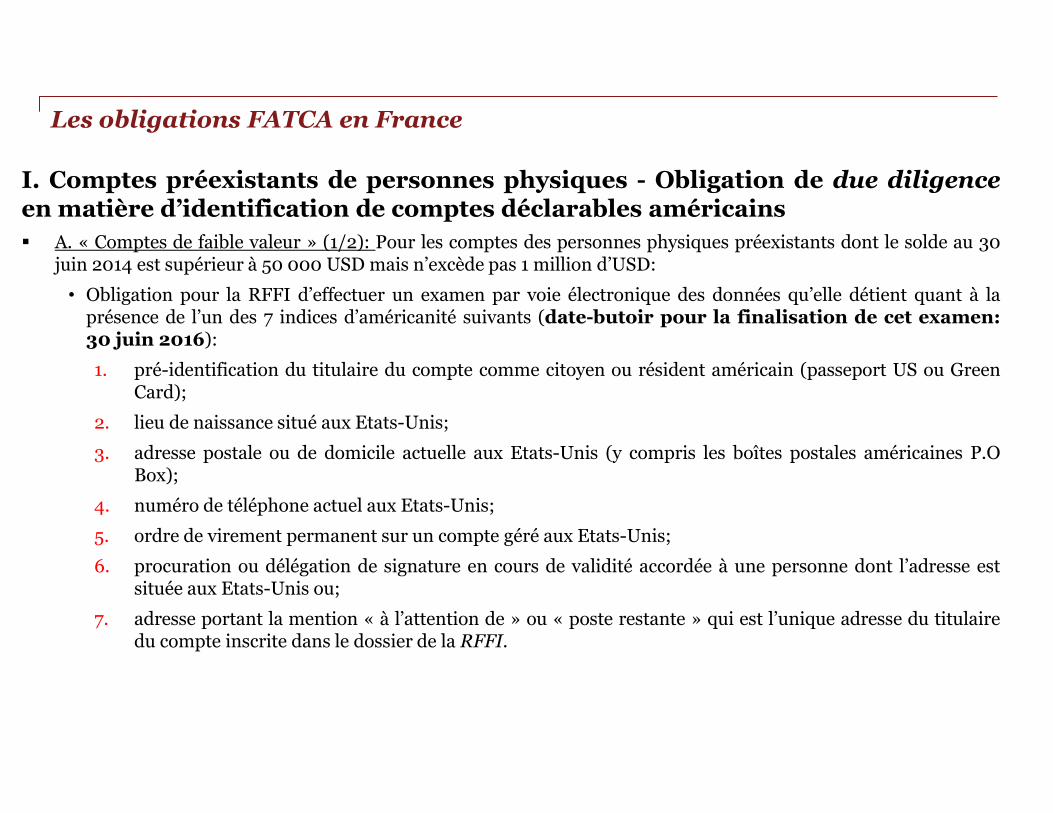

I. Comptes préexistants de personnes physiques - Obligation de due diligence en matière d’identification de comptes déclarables américains

A. « Comptes de faible valeur » (1/2): Pour les comptes des personnes physiques préexistants dont le solde au 30 juin 2014 est supérieur à 50 000 USD mais n’excède pas 1 million d’USD:

• Obligation pour la RFFI d’effectuer un examen par voie électronique des données qu’elle détient quant à la présence de l’un des 7 indices d’américanité suivants (date-butoir pour la finalisation de cet examen: 30 juin 2016):

1. pré-identification du titulaire du compte comme citoyen ou résident américain (passeport US ou Green Card);

2. lieu de naissance situé aux Etats-Unis;

3. adresse postale ou de domicile actuelle aux Etats-Unis (y compris les boîtes postales américaines P.O Box);

4. numéro de téléphone actuel aux Etats-Unis;

5. ordre de virement permanent sur un compte géré aux Etats-Unis;

6. procuration ou délégation de signature en cours de validité accordée à une personne dont l’adresse est située aux Etats-Unis ou;

7. adresse portant la mention « à l’attention de » ou « poste restante » qui est l’unique adresse du titulaire du compte inscrite dans le dossier de la RFFI.

Les obligations FATCA en France

I. Comptes préexistants de personnes physiques - Obligation de due diligence en matière d’identification de comptes déclarables américains

A. « Comptes de faible valeur » (2/2): Pour les comptes des personnes physiques préexistants dont le solde au 30 juin 2014 est supérieur à 50 000 USD mais n’excède pas 1 million d’USD:

• En cas d’absence d’indices d’américanité pour ces comptes aucune nouvelle démarche n’est requise jusqu’à ce qu’un changement de circonstance ne se produise (apparition d’un indice d’américanité ou évolution du compte en compte à valeur élevée) ce qui nécessite la mise en place par la RFFI d’une veille permanente sur ces comptes. Si au 30 juin 2014 un compte préexistant n’est pas à valeur élevé mais le devient au dernier jour de 2015 ou de toute année civile ultérieure, la RFFI doit appliquer les procédures d’examen approfondi (cf. description page suivante) dans les six mois qui suivent le dernier jour de l’année civile au cours de laquelle le compte devient compte de valeur élevée.

• En présence d’au moins un indice d’américanité, la RFFI doit considérer le compte comme compte déclarable américain sauf transmission dans certains cas spécifiques par le titulaire de compte de documents probants justifiant qu’il n’est pas citoyen ou résident américain. Le compte sera réputé être un compte déclarable américain toutes les années suivantes sauf si le titulaire cesse d’être une personne américaine déterminée.

Les obligations FATCA en France

I. Comptes préexistants de personnes physiques - Obligation de due diligence en matière d’identification de comptes déclarables américains

B. « Comptes à valeur élevée» (1/2) : Pour les comptes des personnes physiques préexistants dont le solde excède 1 million de dollars au 30 juin 2014 ou au 31 décembre 2015 ou de toute année suivante:

• Obligation pour la RFFI d’effectuer un examen par voie électronique des données qu’elle détient quant à la présence de l’un des 7 indices d’américanité précités (date-butoir pour la finalisation de cet examen: 30 juin 2015).

• Obligation pour la RFFI d’effectuer des recherches dans les dossiers papier. La RFFI ne pourra s’affranchir de cette obligation que si elle a pu réaliser un examen électronique de l’ensemble des indices d’américanité (à l’exception du lieu de naissance aux Etats-Unis) et que les résultats de cet examen sont probants. Dans le cas contraire, la RFFI devra effectuer des recherches dans ses dossiers au cours des cinq années précédentes sur d’éventuels indices d’américanité.

• Obligation pour la RFFI de traiter comme compte déclarable américain tout compte de valeur élevé confié à un chargé de clientèle (y compris les éventuels comptes financiers qui sont groupés avec un tel compte de valeur élevé) si le chargé de compte sait que le titulaire du compte est une personne américaine déterminée. A ce titre, la RFFI est tenue de mettre en œuvre des procédures garantissant que les chargés de clientèle identifient tout changement de circonstances en relation avec un compte (cas typique d’une nouvelle adresse postale aux Etats-Unis) qui ferait que le compte devienne un compte déclarable américain.

Ces obligations constituent les procédures d’examen approfondi définies dans l’IGA pour les comptes de valeur élevée.

Les obligations FATCA en France

I. Comptes préexistants de personnes physiques - Obligation de due diligence en matière d’identification de comptes déclarables américains

« Comptes à valeur élevée» (2/2) : Pour les comptes des personnes physiques préexistants dont le solde excède 1 million de dollars au 30 juin 2014 ou au 31 décembre 2015 ou de toute année suivante:

• En cas d’absence d’indices d’américanité pour ces comptes, aucune nouvelle démarche n’est requise jusqu’à ce qu’un changement de circonstance ne se produise (apparition d’un indice d’américanité) ce qui nécessite la mise en place par la RFFI d’une veille permanente sur ces comptes.

• En présence d’au moins un indice d’américanité, la RFFI doit considérer le compte comme compte déclarable américain sauf transmission dans certains cas spécifiques par le titulaire de compte de documents probants justifiant qu’il n’est pas citoyen ou résidant américain. Le compte sera réputé être un compte déclarable américain toutes les années suivantes sauf si le titulaire cesse d’être une personne américaine déterminée.

Les obligations FATCA en France

II. Nouveaux comptes de personnes physiques - Obligation de due diligence en

matière d’identification de comptes déclarables américains

« Nouveaux comptes de personnes physiques»: comptes de personnes physiques ouverts à partir du 1er juillet 2014

• Possibilité de dispenser les comptes de dépôt dont le solde à la fin de l’année civile n’excède pas 50 000 USD.

• Pour les autres comptes, la RFFI doit obtenir lors de l’ouverture de compte (ou dans les 90 jours suivant la fin de l’année civile durant laquelle les conditions de dispense ci-dessus ne sont plus remplies pour le compte), une autocertification, laquelle peut faire partie des documents d’ouverture de compte, qui lui permette de déterminer si le titulaire du compte réside aux Etats-Unis à des fins fiscales et confirmer la vraisemblance de l’autocertification en s’appuyant sur des renseignements/documents recueillis à l’ouverture de compte dans le cadre des procédures LAB et KYC.

• Obligation pour la RFFI de traiter comme compte déclarable américain tout nouveau compte dont l’autocertification établit que le titulaire réside aux Etats-Unis à des fins fiscales et d’obtenir du titulaire de compte un formulaire W-9 avec indication de son TIN.

• A défaut de pouvoir obtenir de la part du titulaire du compte une autocertification valide à l’ouverture de compte, la RFFI doit considérer le compte comme un compte déclarable américain.

Les obligations FATCA en France

III. Comptes préexistants d’entités - Obligation de due diligence en matière

d’identification de comptes déclarables américains (1/2)

• Les comptes d’entités préexistantes dont le solde n’excède pas 250 000 USD au 30 juin 2014 n’ont pas à être examinés tant que le solde n’excède pas 1 million d’USD.

• Obligation de la RFFI d’examiner les comptes d’entités préexistantes dont le solde excède 250 000 USD au 30 juin 2014 (date-butoir de l’examen: 30 juin 2016) et tout compte dont le solde n’excède pas 250 000 USD au 30 juin 2014 mais dépasse le seuil de 1 million d’USD au dernier jour de 2015 ou de toute année civile ultérieure (date-butoir de l’examen: dans les six mois qui suivent le dernier jour de l’année civile au cours de laquelle le solde du compte a été supérieur à 1 million d’USD)

• L’examen consiste à:

déterminer si au regard de renseignements obtenus à des fins réglementaires (LAB/KYC) l’entité est une personne américaine déterminée (par exemple si le lieu de constitution ou de création ou l’adresse est aux Etats-Unis). Dans ce cas, le compte est considéré comme compte déclarable et un formulaire W-9 doit être obtenu sauf si la RFFI détermine avec une certitude suffisante sur la base de renseignements en sa possession ou qui sont accessibles au public que le titulaire de compte n’est pas une personne américaine déterminée;

déterminer si au regard de renseignements obtenus à des fins réglementaires (LAB/KYC) l’entité est une Institution financière non américaine. Dans ce cas, ou si la RFFI est en mesure de vérifier le GIIN de l’entité, le compte n’est pas considéré comme compte déclarable américain;

déterminer si, notamment en l’absence de GIIN, l’institution financière est non participante. Dans ce cas le compte n’est pas un compte déclarable américain mais les paiements effectués doivent faire l’objet d’un reporting spécifique.

Les obligations FATCA en France

III. Comptes préexistants d’entités - Obligation de due diligence en

matière d’identification de comptes déclarables américains (2/2)

Si au regard de renseignements obtenus à des fins réglementaires (LAB/KYC) l’entité n’est ni une personne américaine ni une institution financière , déterminer (i) si le titulaire du compte est une entité contrôlée, (ii) si le titulaire du compte est une NFFE passive et (iii) si l’une des personnes ayant le contrôle de l’entité titulaire du compte est un citoyen ou un résident américain.

Les obligations FATCA en France

« US-owned Foreign

Entitites »

Entités Etrangères Non

Financières / NFFE (société, partnership …

US-owned >25%

• Une « US-owned Foreign Entity » est une entité étrangère dont un ou plusieurs américains (PP ou PM) détiennent un pourcentage substantiel (i.e. >25% directement ou indirectement des droits aux bénéfices ou au capital)

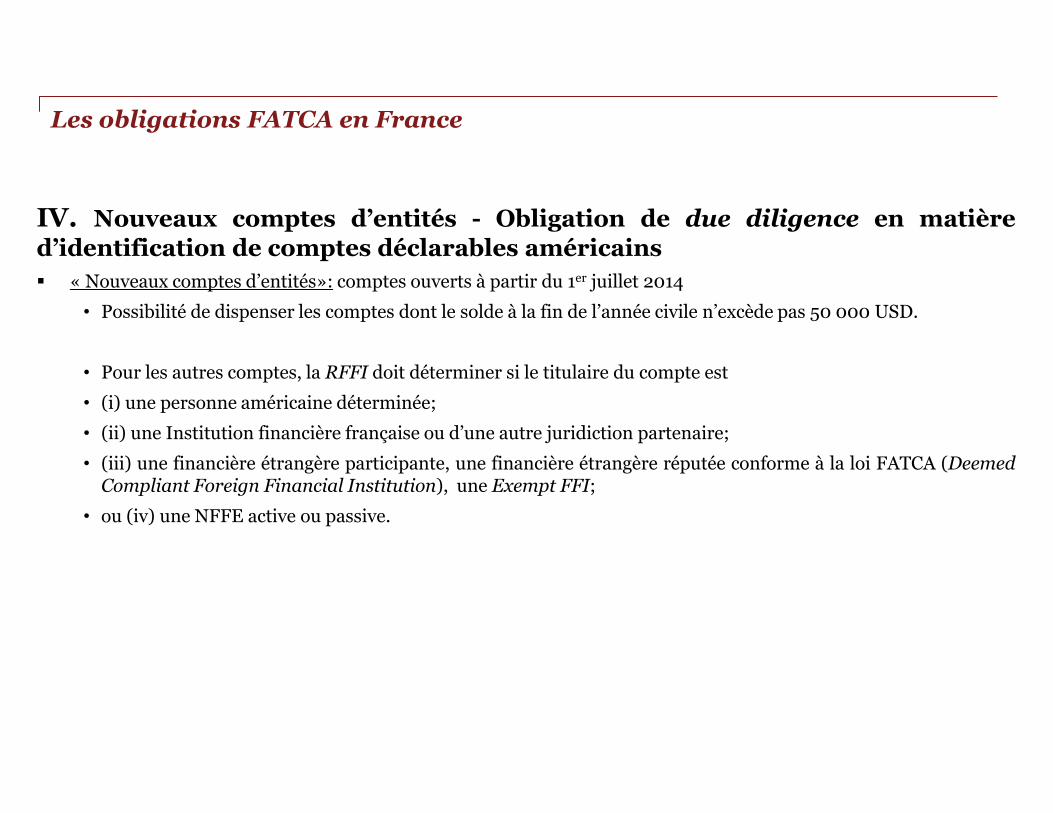

IV. Nouveaux comptes d’entités - Obligation de due diligence en matière

d’identification de comptes déclarables américains

« Nouveaux comptes d’entités»: comptes ouverts à partir du 1er juillet 2014

• Possibilité de dispenser les comptes dont le solde à la fin de l’année civile n’excède pas 50 000 USD.

• Pour les autres comptes, la RFFI doit déterminer si le titulaire du compte est

• (i) une personne américaine déterminée;

• (ii) une Institution financière française ou d’une autre juridiction partenaire;

• (iii) une financière étrangère participante, une financière étrangère réputée conforme à la loi FATCA (Deemed Compliant Foreign Financial Institution), une Exempt FFI;

• ou (iv) une NFFE active ou passive.

Les obligations FATCA en France

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Personnes physiques

Recalcitrant US Non-US

Exempted beneficial

owner

Entités

US NFFEs

Participating FFI

Deemed Compliant/

Non reporting FI

Non-participating

FFI

Passive NFFEs

Active NFFEs

Non-US owned

US owned

FFI

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Les obligations FATCA en France

Participating FFI FFI ayant passé un accord avec l’IRS ou résident d’un Etat conventionné avec les Etats-Unis (IGA)

Non Participating FFI FFI résident d’un Etat non-conventionné et n’ayant pas passé d’accord avec l’IRS

Deemed Compliant FFI / Non-reporting FFI FFI éligible à un statut allégé et faisant application de ce régime

Exempted beneficial owner Certaines entités de droit public, certaines organisations internationales, certains fonds de pension, …

L’obligation de reporting: obtenir et transmettre les renseignements concernant les comptes déclarables dans des délais et selon des modalités prédéfinis

Informations devant être transmises à la DGFIP Année fiscale de référence pour le

reporting

(1) - Personnes physiques US: nom, adresse, TIN le cas échéant (obligatoire à compter du 1er janvier

2017). Pour les comptes préexistants dont le solde n’excède pas au 30 juin 2014 la valeur de 50

000 USD, possibilité de les exclure de la déclaration.

- Personnes morales non US détenues par des personnes US: nom, adresse, TIN (le cas échéant) de

l’entité et de chacune des personnes US. Pour les comptes préexistants dont le solde n’excède

pas au 30 juin 2014 la valeur de 250 000 USD, possibilité de les exclure de la déclaration

(2) Le numéro de compte (ou équivalent fonctionnel)

(3) Nom et numéro GIIN de l’institution financière déclarante française

(4) Le solde du compte à la fin de l’année civile considérée ou, si compte clos durant l’année de

référence, immédiatement avant la date de clôture.

2014

(informations à transmettre à Bercy début

2015 )

(1)+(2)+(3)+(4)+

(5-A) Dans le cas d’un compte conservateur, le montant brut total des intérêts, des dividendes et des

autres revenus produits par les actifs détenus sur le compte

(6) Dans le cas d’un compte de dépôt, le montant brut total des intérêts versés sur le compte

(7) Pour les autres types de comptes, le montant brut total versé au titulaire du compte ou portés à

son crédit

(8) Nom de chaque Institution financière non participante à laquelle la RFFI a fait des paiements

ainsi que le montant total de ces paiements

2015

(informations à transmettre à Bercy début

2016 )

(1)+(2)+(3)+(4)+ (5-A) + (6) + (7) + (8)

(5-B) Le produit brut total de la vente ou du rachat d’un bien versé ou crédité sur le compte

2016

(informations à transmettre à Bercy début

2017)

Les obligations FATCA en France

• Pour les comptes existants au 30 juin 14, dispense de déclaration :

- Pour les personnes physiques, les comptes dont le solde est inférieur à 50.000 $

◦ Jusqu’à franchissement d’un solde supérieur à 1 million de $ au 31.12 d’une année ultérieure

- Pour les entités, les comptes dont le solde est inférieur à 250.000 $

◦ Jusqu’à franchissement d’un solde supérieur à 1 million de $ au 31.12 d’une année ultérieure

• Pour les comptes ouverts à compter du 1er juillet 2014:

- ! Pas de seuil d’exemption pour les nouveaux comptes des personnes physiques et des entités

Les obligations FATCA en France

PwC

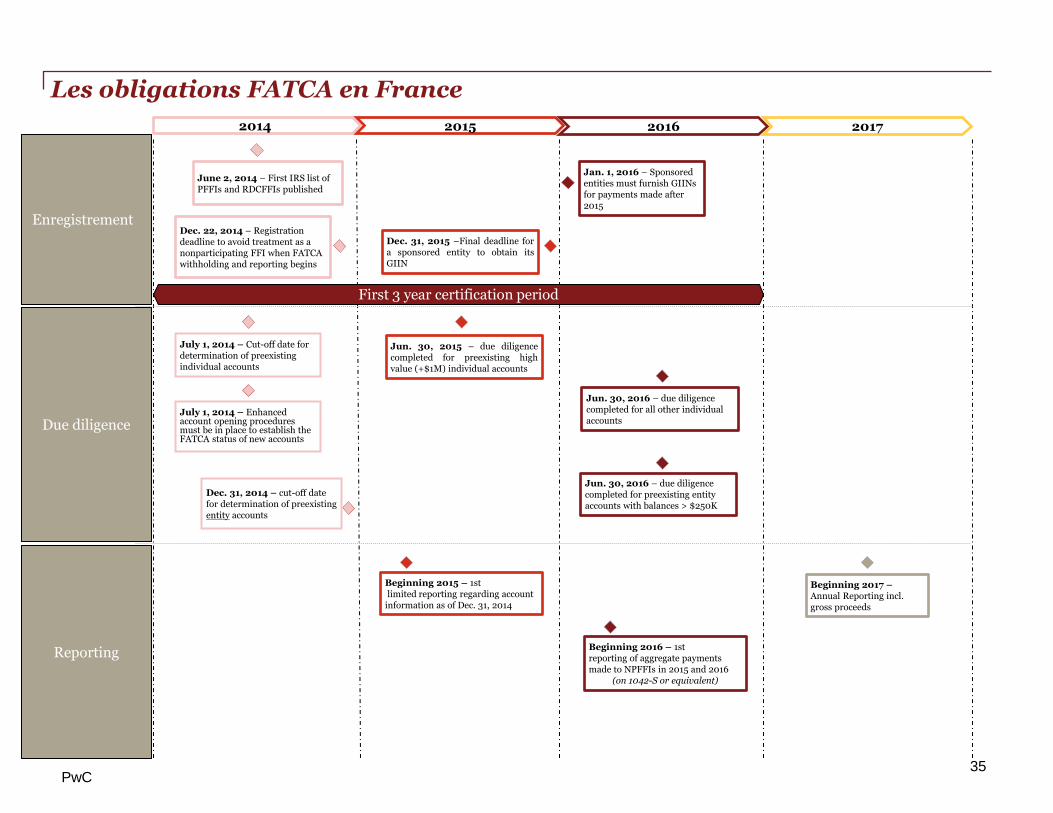

July 1, 2014 – Cut-off date for determination of preexisting individual accounts

Enregistrement

Due diligence

Reporting

Beginning 2015 – 1st limited reporting regarding account information as of Dec. 31, 2014

Beginning 2017 – Annual Reporting incl. gross proceeds

2014 2015 2016 2017

Dec. 22, 2014 – Registration deadline to avoid treatment as a nonparticipating FFI when FATCA withholding and reporting begins

First 3 year certification period

June 2, 2014 – First IRS list of PFFIs and RDCFFIs published

July 1, 2014 – Enhanced account opening procedures must be in place to establish the FATCA status of new accounts

Dec. 31, 2014 – cut-off date for determination of preexisting entity accounts

Jan. 1, 2016 – Sponsored entities must furnish GIINs for payments made after 2015

Dec. 31, 2015 –Final deadline for a sponsored entity to obtain its GIIN

Jun. 30, 2015 – due diligence completed for preexisting high value (+$1M) individual accounts

Jun. 30, 2016 – due diligence completed for all other individual accounts

Jun. 30, 2016 – due diligence completed for preexisting entity accounts with balances > $250K

Beginning 2016 – 1st reporting of aggregate payments made to NPFFIs in 2015 and 2016

(on 1042-S or equivalent)

Les obligations FATCA en France

35

Les risques en cas de non conformité

Pénalités fiscales

Perte potentielle du statut d’«Institution financière de la Juridiction partenaire »:

Taux de retenue à la source sanction de 30% sur l’ensemble des revenus de source américaine versés par l’agent payeur à l’«Institution financière non participante »

Risque de ‘contagion’ aux autres membres appartenant au même EAG

Les obligations FATCA en France

www.landwell.fr

Le secteur de l’Asset Management

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Établissement de dépôt

Détenir des actifs financiers pour le compte de tiers

Établissement gérant des

dépôts de titres

Entité d'investissement

Entités recevant des dépôts dans l’exercice normal d’une activité bancaire ou similaire

• Banque de détail

• Banque mutualiste

• …

Investir, réinvestir ou négocier des valeurs mobilières, des participations, des matières premières

+ sociétés de gestion

ASSUREURS-Vie

• Dans le contexte des IGA, les « Foreign Financial Institutions » (FFI) regroupent les entités suivantes dans le secteur financier et incluent en particulier le secteur de l’asset management

• Les entités non-US ne relevant d’aucune de ces quatre catégories sont considérées comme des Non Financial Foreign Entities (NFFE)

Le secteur de l’Asset Management

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• Les entité d'investissement sont définies comme suit par les accords inter-gouvernementaux :

« Le terme «entité d’investissement» désigne toute entreprise dont l’activité propre comprend l’exercice, pour le compte de clients, d’une ou plusieurs des activités ci-dessous (ou qui est gérée par une entreprise exerçant une telle activité):

- (1) transactions sur les instruments du marché monétaire (chèques, effets, certificats de dépôt, instruments dérivés,

etc.); marché des changes, instruments sur devises, taux d’intérêt et indices; valeurs mobilières; marchés à terme de

marchandises;

- (2) gestion individuelle et collective de portefeuille; ou

- (3) autres opérations d’investissement, d’administration ou de gestion de fonds ou d’argent pour le

compte de tiers.

Le présent alinéa est interprété conformément à la définition de l'expression « Institution financière» qui figure dans les Recommandations du Groupe d'action financière (GAFI). »

“The term “Investment Entity” means any Entity that conducts as a business (or is managed by an entity that conducts as a business) one or more of the following activities or operations for or on behalf of a customer:

- (1) trading in money market instruments (cheques, bills, certificates of deposit, derivatives, etc.); foreign exchange; exchange, interest rate and index instruments; transferable securities; or commodity futures trading;

- (2) individual and collective portfolio management; or

- (3) otherwise investing, administering, or managing funds or money on behalf of other persons.

This subparagraph 1(j) shall be interpreted in a manner consistent with similar language set forth in the definition of “financial institution” in the Financial Action Task Force Recommendations.”

Nota : Définition convergente avec celle de la réglementation unilatérale Américaine (Treasury Regulations par.1.1471 – 1.1474)

Divider

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Le secteur de l’Asset Management

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• Principe: Les Investment entities sont des « Reporting financial Institutions » soumises au régime Fatca correspondant:

- Enregistrement auprès de l’IRS

- Due diligence des comptes-clients et ayants-droits en vue d’identifier les US persons

◦ Concept de compte/financial account: référence au ‘registre’ de l’OPC

◦ Pour les nouveaux comptes:

› recherche, le cas échéant, d’une auto-certification attestant auprès du titulaire de compte pour vérifier s’il est ou pas US person

+ vérifier la vraisemblance de cette auto-certification par rapprochement avec les informations disponibles

- Reporting des informations-Fatca concernant les titulaires de comptes ou ayant-droits identifiés comme US persons

◦ Données administratives

◦ Données financières: soldes de comptes ou des valeurs de contrats

- Reporting les paiements effectués au profit de NPFFI

◦ Nom

◦ Montant total des paiements effectués

• Délégation ou sous-traitance de ces travaux par la société de gestion à un prestataire de services (Cf. l’IFU) ?

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Le secteur de l’Asset Management

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Les Investment entities sont en principe des « Reporting financial Institutions » c’est-à-dire des institutions financières déclarantes ; un enregistrement est donc en principe requis.

L’AFG considère sur la base de l’IGA Model 1 signé par la France (Annexe II-II-C-3) ainsi que du HIRE Act (1471(d)(1)(C)) que lorsqu’un fonds ayant adopté le statut de Reporting FI a dans son registre à la fois des titres au nominatif pur et des titres détenus en mode nominatif administré ou au porteur, ses obligations d’identification des investisseurs ainsi que ses obligations déclaratives ne portent que sur les comptes au nominatif pur sachant que :

• pour les titres au porteur, Euroclear, en tant que dépositaire central faisant fonction de teneur de registre, n’accepte que des membres ayant un statut de PFFI ou assimilé, quel que soit le pays de résidence de ces membres (IGA1, IGA2, sans IGA)

• pour les titres au nominatif administré, les intermédiaires financiers dont le nom figure dans le registre de l’OPC ont un statut de PFFI ou assimilé, quel que soit leur pays de résidence (IGA1, IGA2, sans IGA) ou encore, éventuellement, NPFFI

Ce statut de Reporting FI s’applique obligatoirement aux fonds dont le registre (qu’il soit tenu en nominatif pur, administré ou reflété en Euroclear) comporte le nom d’institutions financières non conformes à Fatca ou dont le registre est tenu au nominatif pur et comporte au moins une personne physique.

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Le secteur de l’Asset Management

The term “Financial Account” means an account maintained by a Financial Institution, and includes (…) in the case of an Entity that is a Financial Institution solely because it is an Investment Entity, any equity or debt interest (other than interests that are regularly traded on an established securities market) in the Financial Institution

Il s’agit du passif de l’entité d’investissement

Le secteur de l’Asset Management

Entité d'investissement

Comptes financiers / Financial

accounts

Titulaire de compte Titulaire de compte

Titulaire de compte Titulaire de compte

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• Statut optionnel spécifique à la gestion d’actifs permettant de réduire les obligations des fonds d’investissements:

« The following Financial Institutions are Non-Reporting French Financial Institutions (…)

B. Certain Collective Investment Vehicles [‘CCIV’]

An Investment Entity established in France that is regulated as a collective investment vehicle, as well as the “société de ”Credit foncier » and the « société de financement de l’habitat”, provided that all of the interests in the collective investment vehicle (including debt interests in excess of $50,000) are held by or through one or more:

• Exempt beneficial owners, • Active NFFEs (…), • US Persons that are not Specified U.S. persons, • or Financial Institutions that are not Nonparticipating Financial Institutions.”

• Qui est visé par ces termes et donc admis dans un CCIV?

- Exempt beneficial owners : collectivités territoriales, banque centrale, organisations internationales, caisses de retraite, caisses de congés payés.

- Active NFFEs: les entreprises dont l’activité est non-financière au sens de FATCA (véritable activité industrielle, commerciale, artisanale ou de prestataire de services)

- US Persons that are not Specified U.S. persons: personnes ou entités américaines entrant dans les catégories suivantes : les sociétés US cotées en bourse et leurs filiales, les sociétés US membres d’un Expanded Affiliated Group US et incluant une société US cotée, les organisations US exemptéees de taxe ou les plans de retraites individuelles US, les Etats-Unis (chacun de ses Etats, le District de Columbia, tout territoire US etc…), les établissements bancaires US

- Financial Institutions that are not Nonparticipating Financial Institutions: institutions financières en conformité avec la réglementation FATCA

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Le secteur de l’Asset Management

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• Déclinaison du statut CCIV selon le mode de détention des titres dans le fonds d’investissement:

- OPC dont les titres sont au porteur

- OPC dont les titres sont au nominatif administré

Les titres de l’OPC sont bien détenus par l’intermédiaire d’institutions financières. Si ces dernières participent toutes à FATCA (en ayant un statut de Reporting FI, Non-Reporting FI, de PFFI etc…), alors l’OPC peut bénéficier du statut CCIV

- OPC dont les titres sont détenus au nominatif pur

◦ Accès au statut Certain Collective Investment Vehicles si tous les porteurs appartiennent aux catégories admises

• Exemples de configurations permettant l’application du statut CCIV :

- Un OPC au nominatif pur dédié à une entreprise non-financière qui a le statut de Active NFFE

- Un OPC au nominatif pur détenu par une ou plusieurs caisse(s) de retraite,

- Un OPC admis en Euroclear dont toutes les parts sont au porteur ou au nominatif administré (à l’heure actuelle Euroclear n’a que des adhérents qui sont conformes à FATCA.),

• Obligations à la charge des OPC optant pour le statut CCIV :

- Prévoir d’auto-certifier ce statut de Non-Reporting FATCA French FI sur un imprimé W-8BEN-E,

- Accepter d’informer l’IRS de tout changement qui rendrait le FFI inéligible au statut de Non-Reporting F.I./Deemed compliant F.I.

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Le secteur de l’Asset Management

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

L’accord inter-gouvernemental liant la France et les Etats-Unis prévoit la possibilité d’appliquer, dans le secteur de la gestion d’actifs, un statut spécifique permettant de réduire les obligations pesant sur les entités d’investissement.

Appliqué à la réglementation FATCA, il apparait que concernant les détention au porteur et en nominatif administré, les titres de l’OPC sont bien détenus par l’intermédiaire d’institutions financières. Si ces dernières participent toutes à FATCA (en ayant un statut de Reporting FI, Non-Reporting FI, de PFFI etc…), alors l’OPC peut bénéficier du statut allégé CCIV.

Les OPC dont les titres sont détenus au nominatif pur peuvent également bénéficier de ce même statut Certain Collective Investment Vehicles si tous les porteurs appartiennent à l’une ou plusieurs des 4 catégories ci-dessous :

1. Bénéficiaires effectifs dispensés de déclaration /Exempt beneficial owners

2. Entités étrangères non financières actives / Active NFFEs

3. Personnes américaines qui ne sont pas des personnes américaines déterminées

4. Institutions financières qui ne sont pas des institutions financières non participantes

Certains OPC ont des porteurs personnes physiques dont les titres sont détenus au nominatif pur, ce qui leur interdit d’opter pour un statut de Non-Reporting/Deemed-Compliant/CCIV.

Un fond bénéficiant de ce statut doit néanmoins prévoir d’auto-certifier ce statut de Non-Reporting French FI sur un imprimé W-8BEN-E.

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Le secteur de l’Asset Management

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• Régime de parrainage des fonds d’investissements « reporting FI » – ‘Sponsoring’

- Régime permettant à une entité d’investissement sous régime Reporting FI d’être parrainée par une Sponsoring entity en vue de lui déléguer ses obligations FATCA

- Délégation opposable aux autorités fiscales (locales et IRS)

- Le statut de Sponsoring entity est réservé à une « entité parrainante » qui peut justifier que :

◦ elle est autorisée à agir au nom de l’entité,

◦ elle s’est enregistrée en cette qualité auprès de l’administration américaine (et devra enregistrer les fonds qu’elle parraine)

◦ elle a donné son accord par voie contractuelle à la délégation des obligations FATCA d’un fonds, et

◦ elle mentionne qu’elle agit au nom de l’institution financière parrainée.

- Ce régime présente l’avantage pratique de « concentrer » l’ensemble des obligations FATCA d’un ou plusieurs fonds sur par exemple sa société de gestion.

◦ ! L’OPC reste responsable des obligations effectuées en son nom

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Le secteur de l’Asset Management

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

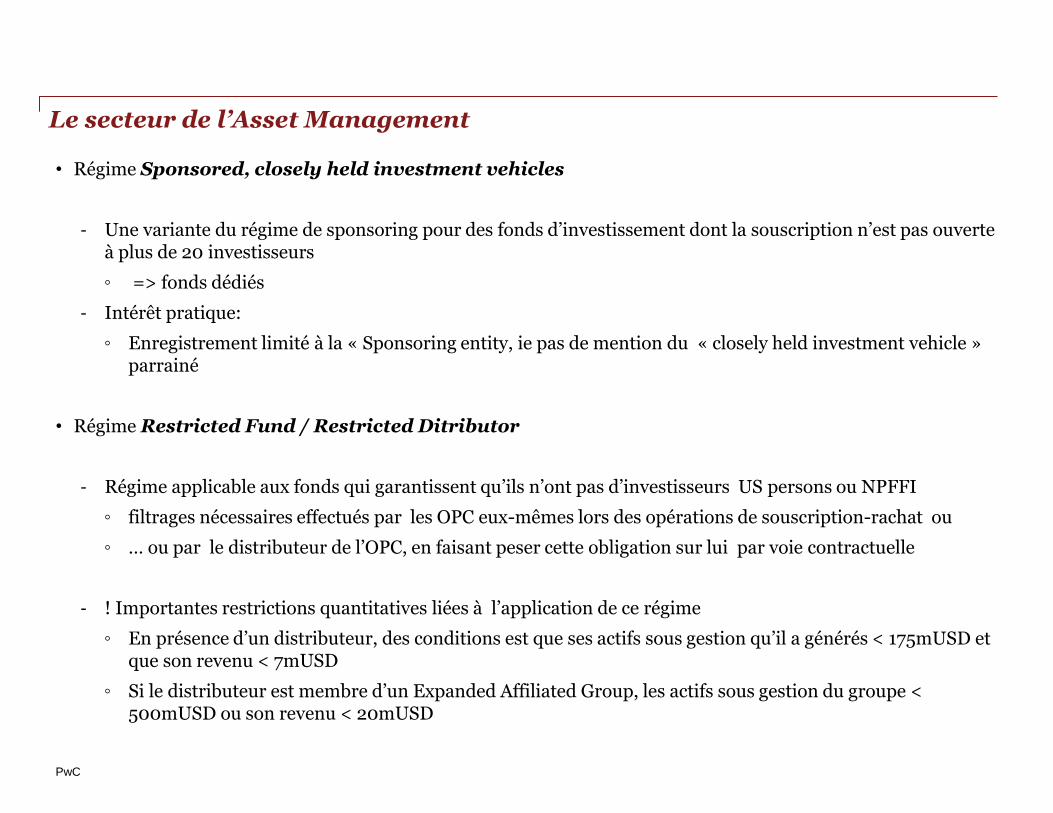

• Régime Sponsored, closely held investment vehicles

- Une variante du régime de sponsoring pour des fonds d’investissement dont la souscription n’est pas ouverte à plus de 20 investisseurs

◦ => fonds dédiés

- Intérêt pratique:

◦ Enregistrement limité à la « Sponsoring entity, ie pas de mention du « closely held investment vehicle » parrainé

• Régime Restricted Fund / Restricted Ditributor

- Régime applicable aux fonds qui garantissent qu’ils n’ont pas d’investisseurs US persons ou NPFFI

◦ filtrages nécessaires effectués par les OPC eux-mêmes lors des opérations de souscription-rachat ou

◦ … ou par le distributeur de l’OPC, en faisant peser cette obligation sur lui par voie contractuelle

- ! Importantes restrictions quantitatives liées à l’application de ce régime

◦ En présence d’un distributeur, des conditions est que ses actifs sous gestion qu’il a générés < 175mUSD et que son revenu < 7mUSD

◦ Si le distributeur est membre d’un Expanded Affiliated Group, les actifs sous gestion du groupe < 500mUSD ou son revenu < 20mUSD

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Le secteur de l’Asset Management

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• Le statut -Fatca des sociétés de gestion

• Les sociétés de gestion sont des investment entities au sens de FATCA

- Principe: Ce sont donc des Reporting Financial Institutions

- l’ensemble des obligations FATCA leur est donc applicable

• Alternative 1: Statut investment manager – investment adviser

- Un statut allégé ne nécessitant pas d’enregistrement auprès de l’IRS prévu par la réglementation US

- Possibilité d’application confirmée dans certains pays

• Alternative 2: Régime de parrainage:

- Régime applicable à une société de gestion détenue à 100%, directement ou indirectement, par une société-mère américaine

- Condition que la société mère US partage un système d’information commun avec la société de gestion parrainée

Divider

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Le secteur de l’Asset Management

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• La spécificité du concept d’Expanded Affiliated Group dans le secteur de l’Asset Management:

• S‘agisant des entités assimilables à des partnerships, la notion de Groupe-FATCA (« Expanded Affiliated Group », EAG ) inclut l’ensemble des entités détenues directement ou indirectement à plus de 50 % en valeur , sans considération et critère de droit de vote

- Cas des FCP

- Cas des SICAV

- Cas des fonds d’investissement dédiés ou détenus à plus de 50% => Appartenance du fonds dédié à l’EAG de l’investisseur dans le fonds Divider

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Le secteur de l’Asset Management

www.landwell.fr

Les spécificités immobilières

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• Fonds immobiliers

- FATCA ne vise pas à fournir à l’administration Américaine des informations sur des flux de revenus immobiliers

◦ le droit d’imposer est réservé, généralement, à l’Etat de situation du bien

› =>Les droits ou biens immobiliers détenus en direct et leurs flux de revenus qu’ils génèrent ne devraient pas être impactés par FATCA

› => Au UK, les entités détenant de l’immobilier en direct sont considérées comme des Active NFFEs

! Cas particulier des biens immobiliers US ou des participations dans des REITS US

- En cas de chaîne d’investissement immobilier où le fonds est investi dans une ou plusieurs holding ou une société-propriétaire qui détient elle-même le bien ou droit immobilier en direct, le fonds détient une valeur mobilière, tombant dans l’acception large de »security » au sens de FATCA

◦ Le revenu généré par cette valeur mobilière pourrait donc être considéré comme entrant dans le champ des obligations déclaratives FATCA

Divider

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

Règles applicables aux fonds immobiliers

PwC

Use the divider control box below to

make the slide title appear in your

primary TOC and section TOCs.

Please follow these steps:

Type ‘Divider’ in the control box

provided below.

Click the Divider command on the

Smart ribbon.

Enter the text that you’d like to

appear in the TOCs and select a

divider level.

Click Update. The slide title should

now appear on all TOCs.

To remove the slide title from your

TOCs, delete the ‘Divider’ text from

the divider control box and hit

Update.

• Fonds immobiliers

• Les entités d’investissement dont les actifs sont composés de droits ou biens immobiliers détenus en direct ne devraient pas inclure les flux de revenus dans leurs déclarations en matière FATCA.

• Cf l’instruction fiscale britannique relative à la réglementation FATCA: ces entités sont considérées comme des active NFFEs, des entités non-financières donc. Enfin, les Treasury Regulations (par.1.1471 – 1.1474) semblent confirmer également ce principe, sous forme d’un exemple.

• En cas de chaîne d’investissements immobiliers où le fonds est investi dans une holding ou une société-intermédiaire qui détient elle-même le bien ou droit immobilier

• Le fonds détient alors une valeur mobilière (= une « security » au sens de FATCA)

• Le revenu généré par cette valeur mobilière pourrait donc être considéré comme entrant dans le champ des obligations déclaratives FATCA (même si le flux économique sous-jacent est fondamentalement un revenu immobilier ou une plus-value immobilière)

Divider

Use the divider control box below to

make the slide title appear in your