north africa's cement industry facing great challenges de cemento/z825i_11… · maroc ct en...

TRANSCRIPT

i!

"~~

~~ Suez Cement plant • Werk Suez Cement

North Africa's cement industry facinggreat challengesDI', [oachim Hardcr()',<,'<;1,11/(, Cvll';l/lrill,~ Cf<J/!p, Bllxrl"iIl'cÍ,' (" rIIl 1)

Summary: The cement indusrry in Nonh Africa is being considerablv arfecred bv rhe currenr polirical uphcavals in rhe region. How-cver, in Tunisia at least the expecred slump in ceme nr sales did nor ycr occur in rhe firsr quarrcr of ~(¡1 l . In Egypt. plant stol'pagescaused a loss of abour rwo production wccks. ¡n Libya, production has come to a total standsrill smce rhe beginning of [he civil war.

The situation in Morocco and AJgeria is also regarded as tense. The corning monrhs will be marked by hopc .md fear and [he ccmenrindustry naturaJly wants the situation ro rerurn ro norrnaliry as quicklv as possible. The Iollowing r<'port deals wirh rhe situaton ofthe cernenr industry in the North Afiican countries and describes the prospects up ro the year ~() 12.

Nordafrikas Zementindustrie vorgroBen Herausforderungen

Zusammenfassung: Die Zementindus-tric in Nordafrika ist nicht unerheblich

von den mornentanen politischcn Um-walzungcn in den Landcrn betrofien. InTunesren zurnindest sind aber die crwar-

tcren Embruche m dem Zcmentabsatz im

crsten Quartal Zül 1 noch ausgcblieben.In

Agypten gingen durch Anlagensrillst.indeetwa zwei Produkrionswochen verlorcnIn Libyen ist die Produktion scir l:3eginn

des Biirgerkr iegs ZUTll ErJiegen gekorn-

men. Die Lagc in Marokko und !\Igc-rien gilt ebenfalls als angespannr. Hoffcnund Bangen werden die nachsren 1\110-

nate besrimrnen und die Zemenrindus-rr ie móchre narürlich moglichst schnellzur Normalirar zurückkehren. In dern

nachfolgenden 13eitrag wird die Situation

der Zementindustr ie in den nordafrika-

nischen Landcrn beleuchtet und ein Aus-

blick bis ZUI1l Jahr 2012 gegeben.

46

L'industrie du ciment nord-africaineface a de grands défis

Résumé: L'indusrric du ciment en Afriquec1u Nord esr ;¡t1Cctt't' dans une mesure non

négligcablc par les boulcverscrnents po-

litiquc actuel- d.ins (es pays. En Tunisie.k, baisse- de ventcs de cuueut atrcnducsu'onr ras encere eu heu Jll cours du pre-mier rrimcstre ~{J I 1, En Egypre. prcs de

deux scmaines de producrion ont été per-dues par suire de lar ret des cimenrerics.En Libve. la production est arrcté e depuis

le' debut de la guerre civile. La siruation au

Maroc ct en Algcr ie esr tendue. Les mOI>

prochains seronr marqués par l' espoir er l,¡

crainre. lindustrie du ciment souh.iitantrevenir aussi vire que possible a la nor-malc. L arricle qlll suir donne un .Ipen,:usur la situation de lindustrie du cimeur

dans les pays nord-africains ainsi quuneperspective á l'horizon 2012.

ZKG INTERNATIONAL No, 7/8,2011 www.zkg-onlme.mfo

La industria del cemento en el Nortede África afronta grandes retos

Resumen: La industria del cemento en elNorte de Átrio estél considcrablci ientc

afecrada por las .'((UdIeS revueltas po itic.isen J.¡ regIón Ln Túnez no ha ocurrido,

SIl1 embargo dur.uire ti pruuer cuan o delano ~(,I J J., caid<l de 1,1' ventas dé cc ncn-

to esperada En Egiptc se perdió la pro-ducc.ón de aproximadamente dos scma-

uas por paradas de pl.mtas. En L ibia se: 11.1parado totalmente la producción de' de el

comienzo de la g:lIerra civil. LJ situ.ictónen i\1arrllcco, " A.rgeJi<1 es también ten-s.i. Los próximos meses e-tarán marcados

por la esperanza " el temor. La industriadel cemento desea naturalmente q .ie la

situación rctor ne a la normalidad lo másrápidamente posible. Este artículo tr.ira la

situación de la industria del cemento en

el Norte de Áti'ica y describe la per,pec-

tiva en el ano 2012.

8.0 rcicbischc Asamcr Gruppe. die 'In drci \X/erkenbctciligr ist. hat <arntliche nichr-cinhcirruschenMirarbciter vorübergehcnd aus Libven abge-

zogcn. Ein Toralverlusr der Werke. der 110cl1 imMúz drohre. ist durch die z une hmcndc Kon-

trolle dcr vvcsrhchen Streitkrafre aber kuumnoch zu befiirchten.

El Population growth in %

O GDP growth in %

O Cement growth in %

8 Die Liinder iVlarokko. Algcrien. Tunesie n.Libven und Agyp¡en kornmen derzcir aufeine Bevolkerungszab] von J 65.8 Millionen.

Ó (Bild 1) ])il' Zemcntkapazitat berragt ·111) Mil-.1s; lionen Jahreswnnen (Mra). In 2Ul () I:tg dert Zemenrvcrbrauch bei 1f)(J.~ Mta, \vas einern

,3 durchschnitrlichen Prokopf-Zeme nrverbrauch(pCC) ven 606 kg emspricht nach ~~:: kg in2()()1) 111. Westeuropa kOl11l11t im Verglcich dJZlI

nur auf einen PCC vo n etwa 4-'1-0kg 12(10).

Den hochsren I'CC: In Nordafrika habcn Libren (1431 kg).TlI-nexi..n (6~2 kg) und Agypten (616 kg). den niedrigsrcn haben

M.HOkko (~Sll kg) urid Algc:rien (565 kg). Auch bei de m 13e-volkcrungsvvachstum. dern \X1irrschafrswdchst1lll1 und J\nstiegdes Zernenrvcrbrauches ftir das Jabr 201 () ergibr sich·tir dieLandcr ei" uneinheitliches 13ild (Bild 2). Agvpten und Libyenverz cir hnen das grof)tc Bevolkcrungs- und Wirtschafhwachs-turn. Libven und Tunesicn komrue n auf das gróf3tc Zvment-wach-tu¡n. iJ"s gnillgst" Zcrncutw.rchsrum nnt fI,~· '~.;,wurdein i\rlJrokko reglstricrt.

2 A comparíson of growth rates (2010) • Wachstumsraten (2010) ím Vergleích

lowest are in Moroeco (450 kg) and Algeria (')(,5 kg). The fig-unes for population gro\\'tb. economic grO\\"th .md mercase incernenr consumption for 21) 1il also show an 1I1lt'\'Cn picture

(Fig. 2). Egvpr and Libva have rhe largest grO\\th in both pOpll-l.uion and economy, while Libya and Tunisia han' thc highestgrowth in cernent cousumption. The lowesr gro\\"th in cernenr

consumption \V;1S registercd in Morocco.

3 Country reports3.1 Algeria

Thc econornic and politic.il situarion in rhc counrrv " tense.Algeria srancd privarizing rhe cerucnr indusrrv .1 tevv vears ago.having esrablished ;1 holding company (CIC,'\. = Croup lndus-

uiel de Ciments el' Algéric) tor this purposc. This now holds ,,11four statc-owncd ccment producers. Of thc countrv's total of 14cement factones. with their total capacitv 01' 21).3 Mta (Fig,3).

CICA is cur rentlv rhe majority shareholdcr in 12 cernenr facto-I ries wirh a total cemenr production capaciry of 11.7 Mta.The rc-

maining capaciry of8J, Mta al rwo facrories (Fig, 4) is owned byLafarge. due to their rakeover of Orascorn. Of the statc-ownedcompanies, ER.CE OWIlS a capaClty of 4.5 Mta at ') Iacrorics in

Ain El Kebira. Ain Toura, Hamma Bouz.une. Hadjar SOLld andEl Maa El Abyad (Tebessa). Then come ERCO with 2.7 Mta ar3 tacrorics III Saida, Beni Saf and Zahana. ERCC: with 2.') iVllaar .3 facrories in Rais Hamidou. Sour El Chozl.me .md Meftah

ami ECDE wuh .1 r.ipacitv of 2.1) M t,l ar thc rd((OP~ in Chlcf.

Up ro now, ~ minorirv shareholdings han' becn gr,lIlteJ. Yi "e>

of the sharcs in rhc Beni SJf cerncnr tactorv vverc sold tO the

[} fRCE

O ~CO

<O ERCC

@L.,E,<;:OE,E8

< -Lafarge §o

~U

~"O

~~;3

3 2010 market shares in Algeria • Marktanteile in Algerien 2010

48 ZKG INTFRNATIONAL No. 7/8-2011

3 Uinderberichte3.1 AlgerienDie wirrschafclichc und polirischc Lage irn Lund ist derz cit an-gespallllt iVIit der Pri\·atislerung der Zemencindustric wurdebcreirs vor cinigen Jahrcn bcgcnnen und d'IZLI cine Betcilungs-gescllscluft (CICA = Group Indusrriel de Cirnents d'Algérie)gq~ri.indcr, die <arntliche vier staatlichen Zemenrunrcruehmeuumfasst. VOIl den insgesarnt J -'1-Zernenrwerken des Laudes mit

cincr Ccsamtkapaz irar \'011 20,3 Mra (Bild 3), halr die CICAdcrzeir die Mehrheitsbercilizunu an inszesamt 12 Zcme ntwer-~ b ~

ken rmr 1 1,7 Mta Zemcnrkapazitar. Auf die restlichc Kapazirarvon ~.6 Mta aus zwer \Xlcrkcn (Bild 4) kornrnt Lafarge 11,ICh der

Übnnahme von Orascorn. Von den staarlichen Unrernchmcnverfiigr ERCE iiber cinc Kap.izitar von ~,5 Mra aus den 5 :\n-Llgcn In Ain El Kebira. '\in Tonta. Hal1l111J Bouz.unc. Hadjar

'soud und El Maa El Abvad (Tebessa). Dahinter tolgen ::RCOmit 2.7 Mra :lUS den 3 AlllagCll in Saida, l3eni SJf und :":.¡]una,

ERCC mil 2,5 Mra nut den :1Anbgen in Rais Harnidou. Sour

4 Ciba cement plant in Algeria • Ciba Zementwerk in Algeríen

www.zkg-cnline.mfo

,

5 Sour el Ghozlane cement plant • Zementwerk Sour el Ghozlane

Saudi-Arabian companv Pharaon Commerr i.rl l nvestrnent.Lafarge purchased 35 'r., of the shares in rhe Mefi:ah Iacror y and

simulraneouslv took over managemem of the facrorv under a1u-vcar ronr rnct.Tíuz z: Unicern rook over 35 0/., in each of rhcrwo factories Som el Ghozlane (Fig. 5) and Hadjar Soud audthus influences a cernent producrion capacirv of2_ J MtJ_ASEe

Cement (Citadcl Capital) took J 35 'Yrl sharehoiding in ZahanaCcment. The new plant thar ASEC is planning in DJelfa íor an

ultimate cerncnt production capar irv 0[3.2 Mta IS lhc mosr irn-portanr planncd capaciry expausion. The tirst stagc of rhe pl.inris due ro cornmcnce operarions in 2(¡ J 2. ASEe also l'bm to

extend rhc Zahuna factory Irorn its prcsent J.2 Mta to 2.8 IVlr3.In 201 J. Llfargc is going to exp.md it, grinding capaciry bv (1.5

Mta. The capacities of rhe starc-owned facrories in Chlct. AinEl Kebira and J3eni Saf are to be increased bx (,.11 Mr.i.

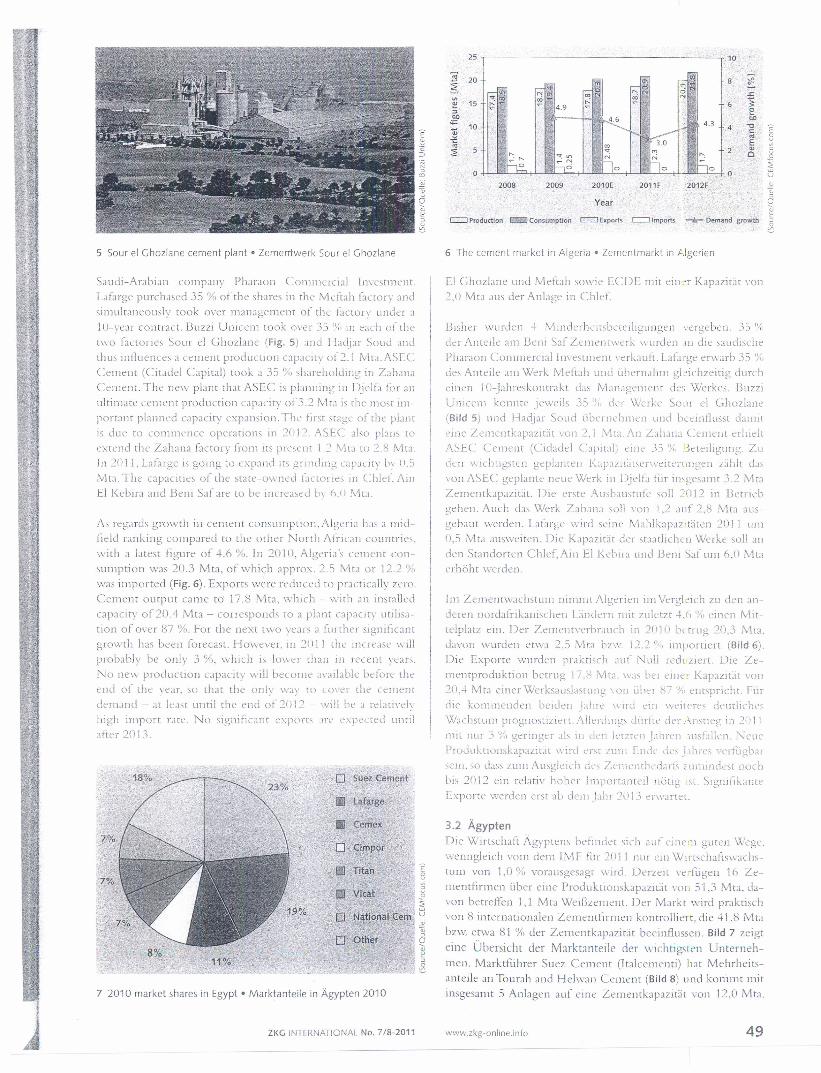

As regards growth 111cement corisumption.Algeri» has a mid-field ranking compared to rhe orlier North AfricJn countrie-,with a Iatest figure of 4.6 %,. In 2010. AIgeria's cerncnr COI1-sumprion was 20.3 Mra. of which approx. 2.) Mta or 12.2 ':l.,was irnported (Fig. 6). Exports were re duccd to pr.rctically zero.Cement output carne to 17.B Mra. which - wirh an installed

capacirv 0120.4 Mta - corrcsponds to a planr capacity utilisa-tion 01 over 87 'Yo.For rhc nexr rwo vears a further signiticantgrowrh has been forecast. However, in ::!( ) 11 rhc increase willprobably be only 3 %, which is lower than in recenr ycar5.

No new production capacitv will become available beforc rheend 01 thc vcar. 50 that the onlv wav to cover rhe cerncntdcrn.md - ,It Iea-r until the end 012012 - wil] be 3 rel.rtivclv

high iinport rateo No sigllificant expon, are expccrcd unrilafter 20 J 3.

7 2010 market shares in Egypt • Marktanteile in Agypten 2010

ZKG INTERNATIONAL No. 7/8-2011

25 10

';;¡20 ~ 8 ~.

~ Nl 11 ~o

o<i ::;¡ .s:~ '<1:00 oO~ ~.~ ai ~~ 15 ~ e- 4.9 "- ~ . 6~ Eeo ,K' bll;¡:: ~ 4.3 -o~ 10 4'" : .~

<:~ '":;; , - Ecc '":'! r-, -..-'" ' "'~ M ": C.....:r--:·~ci no . -'lo ha

O-e o

2008 2009 2010E 2011F 2012F

Year

oo~U"<;~Q"-.- Demand growth ~~

c::::::J Production c:::ll Consumption c::J Exports c::J Imports

6 The cement market in Algeria • Zementmarkt in Algerien

El Ghozlanc und Mefiah sowie ECDE rnir ein -r Kapaz ir.it von2,0 Mra JUS der Anlagc in Chlef.

Bisher xvurdcn 4 Mindcrheirsbcrciligungell vergebcn. 35 '1<,der Aurc ile arn Be ni Saf Zcnu-nrwcr k wurden III die saudischePharaon Comrnercial l nvestrnent verkaufr. Lata -ge erwarb 35 '){¡

des Anteilc am \Verk Mefrah und íibcrnahm gl:ichzeitig durch

cinen JO-Jahreskontr;¡kt das Managt'lllem de.; Wcrkes. Buzz:Uniccrn konnte jcweils 35 0";, der \Verke So.ir el Ghozlane

(Bild 5) und Hadjar Soud uberne hrncn und bceinflussr damitcine Zementkapazirar von 2. j Mu. /\n Zah.ma C:CIl1CIlt crhieltASEe Cernenr (Cie!ae!el Capital) cine J.') v: 3ereiligllng. Zllden \\ ichtigstcn geplanten Kapazir.irscrvveitcrungcn z.ihlr das

von ASEe gcpIante ncue \Vcrk in DjeltJ für ill'gesJlllt 3.::! MraZemeurkapazirat. Die ersrc Ausbausrufe soll ::012 in Betr iebgehell. Auch das Werk Zahana soll von 1,2 auf ::!,8 Mta aus-gcbaui werden. LaÚlrgl' wird scin« Mahlkap.rzr.itcn 2011 um0,5 Mra ausweiren. Die Kapazirar der staatlichcn Werke soll anden Standortcn Chlef,Ain El Kchira und l3eni Saf lIJll 6_0 Mtaerhohr wcrden.

Irn Zernenrwachstum nirnmt Algericn IIll Verglcich zu den an-deren nordafiikanische n Lindcrn mil zuletzt 4.h '?" cinen Mit-tclplarz ein. Der Zementvcrbrauch in 2(¡ll} b. trug 20,3 Mta.davon wurden etwa 2,5 Mta bzw. J 2.2 ','1" imporricrt (Bild 6).

Die Exporte wurden prakrisch aut NlIlJ rcduzierr. Die Ze-

menrproduktion berrug J 7.X ,\1tJ. \\ClS be i ciner Kapazitar von20.4 Mta einer Werksauslasrul1¡.c vo n iihn x7 % cnrspr ichr. Fürdie konuncuden hciden j.ihr, "'Ird cm \h'ircres dcurlichcsWJchstllJl1 prognostiziert. ¡\llenllllg< diirftc dCT Ansneg in 2(1 i Imil nur 3 % geringer als liJ den lcrzrc n .I;¡hn:n rusfallcn. Neuc

Produkrionskapazir.it wird n,t zum Ende de' J rhres verriigb.u<cin. so dass zum AlIsgleieh des Zemcntbcdarts L urnindest norh

bis 201::! cm relativ hohcr Importanrcil !long ist. SignifikanreExporte werden erst ab den: j.ihr 2013 erwartet.

3.2 AgyptenDie Wirtschaft Agyprcns befinder sich auf cine-u gutcll \(lcge.wcnngleich VOIl1 dern IMF für 2(Jl J nur ein \Virtschatts,,"Jchs-rurn von 1.0 % vorausgesagt wird. Derzeit \'erfugen 1(, Ze-

JIlemfirmen über eine Produktionskapazitat \-on 51,3 MtJ, da-von betreffen 1,1 Mta WeiGzelllent. Der Markt \YÍrd praktisch

von 8 internationalen Zemenrtirmen kontroJliert, die 41.8 Mta

bzw. etwa 81 % der Zemcntbpdzitat beeinflussell_ Bíld 7 zeigt

eine Übersichr der MarktJnteilc der \úchtigsten Unterneh-men. Marktflihrer Suez Cement (Italcementi) llat Mehrhcits-anteile <111Tourah and HeJwJIl Cement (Bild 8) und kOl1Jmt mitinsgesalllt 5 Anlagen all( cine ZemcJltkapazirar von 12,0 Mta.

www.zkg~onljne.info 49

f

i

Il

I

20 10

'E ~S 15

o

J:::V> / ¡: ~1:'::1 obJ:) 10 b¡,

"" "O., <:-'" '" '"• 00 E;;; 5 " ,:2 ' '~

.,= Zl O el

-J..:

O.~;o

-2

2008 2009 2010E 2011F 2012F

.~e~Oj¿S;

~~r=.:J Irnports -.- Demand growth ¿Year

c:::=::J Production c::::g Consumption c:::::::J Exports

23 Cement market in Tunisia • Zementmarkt in Tunesien

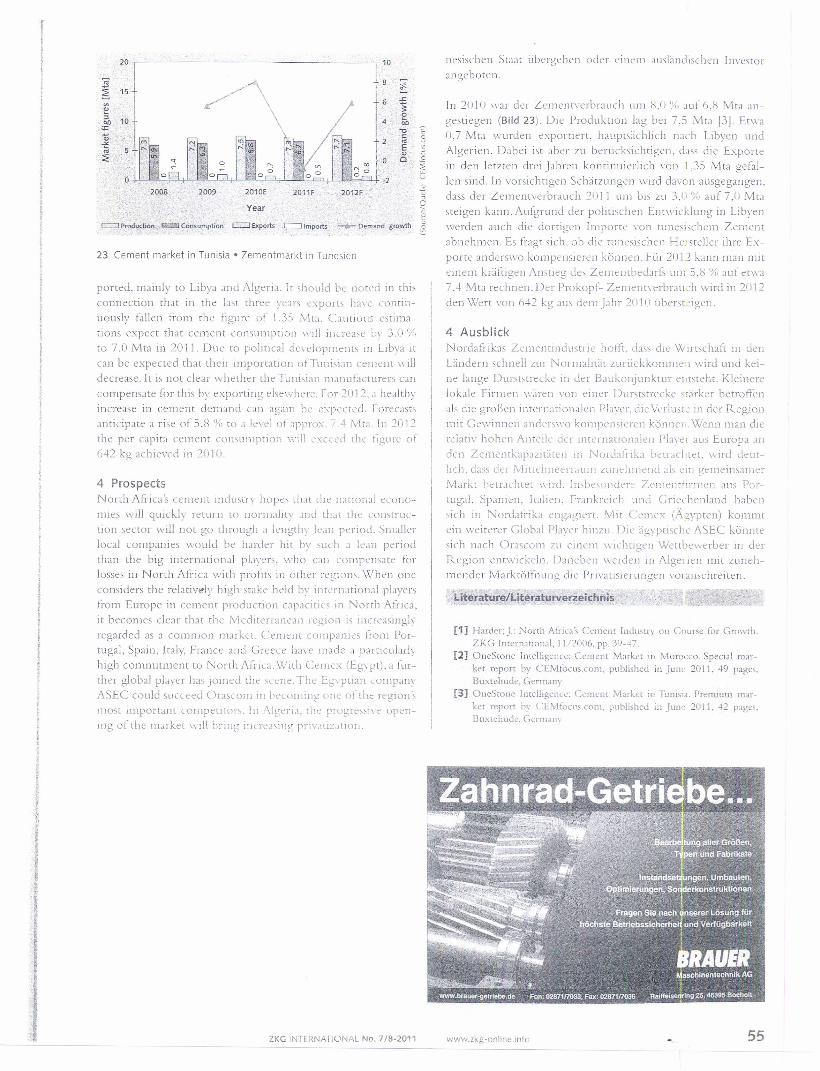

poned. mainly to Libra and Algeria. l r should be' nored in rhi~connection thar in the lasr thrce vcn rs expon< have contin-uously fallen frorn the figure of 1.3.:; \I\rJ. Caurious estima-tions expect rhat cement consurnprion wil] mercase bv 3.0 '/\,

to 7.0 Mta in 2011. Due to polirical dcvcloprne nts in Libva ircan be expected thar their imporration of Tunisian ccmcnt will

decrease. It is nor clear whether the Tunisian manufacrurers cancompensa te for this by exporting clsewherc. For 2012. a healthv

increase in cernent demand can again be expcctcd. Forecnsrsanticípate a r ise of 5.8 'r., to a level 01 approx. 7.-1 Mta. In 2012thc per capita cemenr con-umption will l'xcl'c'd ihe figure of().+2 kg achieved in 2fJ](J.

4 ProspectsNorth Africa 's cemcnt indusrrv hope-. rhat rhe n.uion.il eco no-

mies vvill quickly return ro uormaliry and that rhc consrruc-tion sector will not go through ,1 kngthy lea» periodo Smallcrlocal cornpanies would be harder hit bv sur h J lean per iod

than the big incernational plavers. who can corupensare forlosses in North Afiica xvirh profirx in orher rt:,giom. \vhc'n oneconsiders the relatively high stake held bv inrernational playersfrom Europe m cernent production capacirics 111 North África.

ir bccornes clear rhat thc Medirerrancan region i, iucrcasinglyregarded as a cornmo n marker. Cement companics frorn Por-tugal, Spain, Italy, France and Grcccc have madc ;¡ particularlyhigh commitmenr to Norrh Africa. Wirh Cemex (Eg\"pt). a fur-

rher global plaver has joincd the <cene Thc Egvptian company/I.SEC could succeed Orascorn in bccomine orie otrhe rqnOlú1ll0St important competirors. !Il Aigen,1. rb e progreSS1\'c' opcn-ing of rhc marker will br irn; iJlcrc~l,ing prrv.uiz.mon.

ZKG iNTERNATIONAL No. 7/8-2011

nesischcn Staat libcrgehcn oclcr cmcrn ausl.indischen 1nvcstorangeboten.

In 2(¡ 1() war der Zernenrverbrauch lllll R.I) 'j' , auf (,.f.> Mra an-gesriegen (Bild 23). Die Produktion lag bei 7.5 Mra 13). Ftwa0,7 Mta wurden exporrierr. hauprsachlich nach Libyen und

AIgerien. Dabei ist aber Zll berücksichrigen, dass die Exportein den letzten drei jahre» kontinuicrlicb ven 1.35 Mta gefal-len sind. In vorsichtigen Scharzungen wird davon ausgegangen.dass der Zemenrvcrbr.ruch 21,11 U111bis zu 3,(1 'j;, JUf 7.0 Mra

sreigen kann. Autgrund der polirischen Enrwicklung in Libven

werden auch die donigen Imporrr von runesischern Zementabnehmen. Es fragr sich. ob die mnesischen Hersreller ihre Ex-

porte anderswo kompcnsieren konncn. Für 201.2 kann IlUI1 miteinern kr.ifiigen Ansrieg des Zementbedarfs 1I1115.8 % auf erwa7 ..+ Mta rechnen. Der Prokopf- Zemenrverbrnuch wird in 21)12den Wert vo n 0.+2 kg aus dem jahr 2(111) ubcrvt-igen.

4 AusblickNordafrikas Zemcnrindustrie hottr. dass die \X¡ irtschafi in den

Landern schnell zur Normalitar zuruckkomme 1 wird und kei-nc lange Dursr-treckc in der Baukonjunktur eursteht. Kleinerelokale Firmen w.iren von einer Durststrccke srarker betroffen

.rls die groBen iutcmationalcn Plaver. die Verlusre in der Regionmit C<:\\-inl1Cll andcrvwo kornpensieren konner .Wenn man die

relativ hohen Anreilc del' inrcrnarionalen Plaver aus Europa <Inden Zemcurkupaziraren in Nordatrika bcrracluct. \\-ird deur-lich, d.1'5 der !v]Jttell11Cerralllll zuuehmend al-, cin ge meinsam .cr

Markt bcrrachtcr vvird. lnsbesondcrc Z.ememtirlllen aus Por-tugal. Spanicn. l ralie n. Frankreich und Grierhenland habensich in Nordatrika engagiert. Mir Cernex (Asypren) kommr

ein weiterer Global Plaver hinzu. Die agyptischc ASEC konnresich nach Orascom zu einern wichrigen \Vettbewerber in derRegion entwickeln. Danebcn werden in AIgerien mit zuneh-mender Marktóffnung die Privarisierunge n voranschreitcn.

. Üterat~!:e/Lite1'aturvérzeichni5

[1] Harder;J.: North Afnco\ Cernenr lndustrv on Course for Crowrh.ZKG Jnrcrnarional, J j/2006, pp. 3<)-47.

[2] One Srone lntelligence: Cemenr Markct in Morocco. Special 1110r-ket repon by CEMfocus.cOll1, published in Jun •. 2011, 49 pages,Buxtehude, Gerrnany

[3] OneStone Intelligence: Ccmenr Market in Tunisia. Prernium 111ar-ker report by CEi\lfocus.com. published in JUIl" 201 l. -12 pages.Buxtehude. Gcrmany

www.zkg-onlme.into 55