développement de la climatisation en europe et …compressor) and a splitting in 3 or 4 units of...

TRANSCRIPT

Jérôme Adnot, Matthieu Orphelin et Philippe Rivière, Ecole des Mines, à partir des résultats de divers groupes de travail

" Développement de la climatisationen Europe et impacts sur le réseau

électrique”

1-Etudes menées par Ademe et EDF sur une alternative àla ligne Boutre-Carros

Région, Départements, Ademe, EDF, RTE, Inestene2-EERAC Energy Efficiency of Room Air Conditioners

3-EECCAC Energy Efficiency and Certification of Central Air Conditioners

Financement et suivi DGTREN (UE)

EERAC Participants

Ecole des Mines de Paris, PW Consulting, Un. of Athens, INESTENECCE (Portugal), IDAE (Spain), ENEA (Italy), EVA (Austria), Ademe (France)EdF (France), ENEL (Italy), CECED and Eurovent/Cecomaf, Eurovent / CertificationCoordinator : Jérôme ADNOT

EECCAC Participants

Armines, Un. of Athens Poltecnico diMILANO Inestene now “Energies Demain”

AICIA, U.Seville AQEEB-UCBucharest BREEurovent Cecomaf and Certification ,

AICARR IDAE CCE now ADENE EVA EDF Electricité de France

Coordinator : Jérôme ADNOT

DEUX RAPPORTS DGTREN

DEFINITIONS AND BASIC DATA FOR CENTRAL AND SELF STANDING SYSTEMSFIGURES FOR AIR-CONDITIONING IN EUROPETECHNICAL AND ECONOMIC EVALUATION OF THE ELEMENTARY EQUIPMENT USEDOPTIMISATION OF SYSTEMS INCLUDING PART LOAD AND SECONDARY SYSTEMSEFFICIENCY RATING AT PART LOADENERGY AND ENVIRONMENTAL BENEFITS: HIGHER EFFICIENCY SCENARIOS

Structure de l’exposé

Quelques chiffresUn marché de produits sans aucun règlementUn marché de conception, presque sans règlementProblèmes induits sur le réseau électrique, principalement à venir

Quelques chiffres

Nota bene : on ne discute jamais ici les raisons du choix clim/non clim; on

le constate et on le modélise

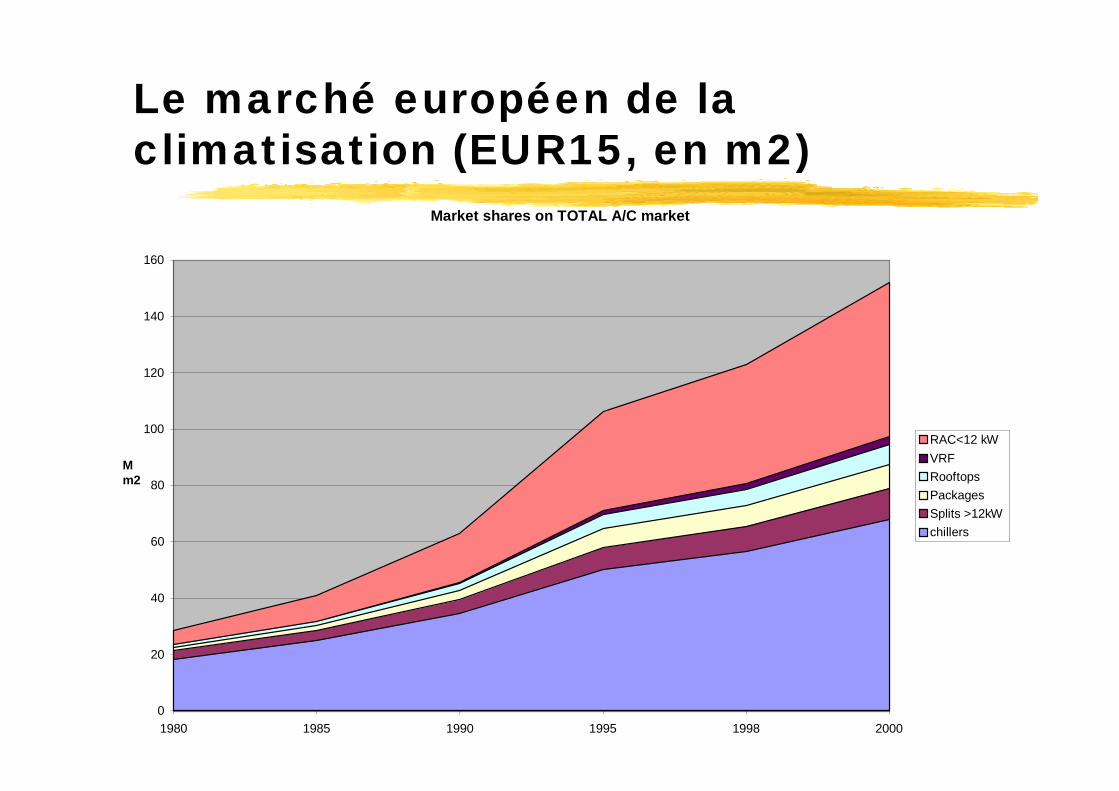

Le marché européen de la climatisation (EUR15, en m2)

Market shares on TOTAL A/C market

0

20

40

60

80

100

120

140

160

1980 1985 1990 1995 1998 2000

Mm2

RAC<12 kWVRFRooftopsPackagesSplits >12kWchillers

PROJECTIONS A 2010 ET 2020 (BAU)

From markets to stock (regressive model)from stock to consumption (DOE2 simulations and climatic extrapolationthrough CDD regression)a different consumption (kWh/m2) foreach country and each systemGWh, tCO2, etc by country/year

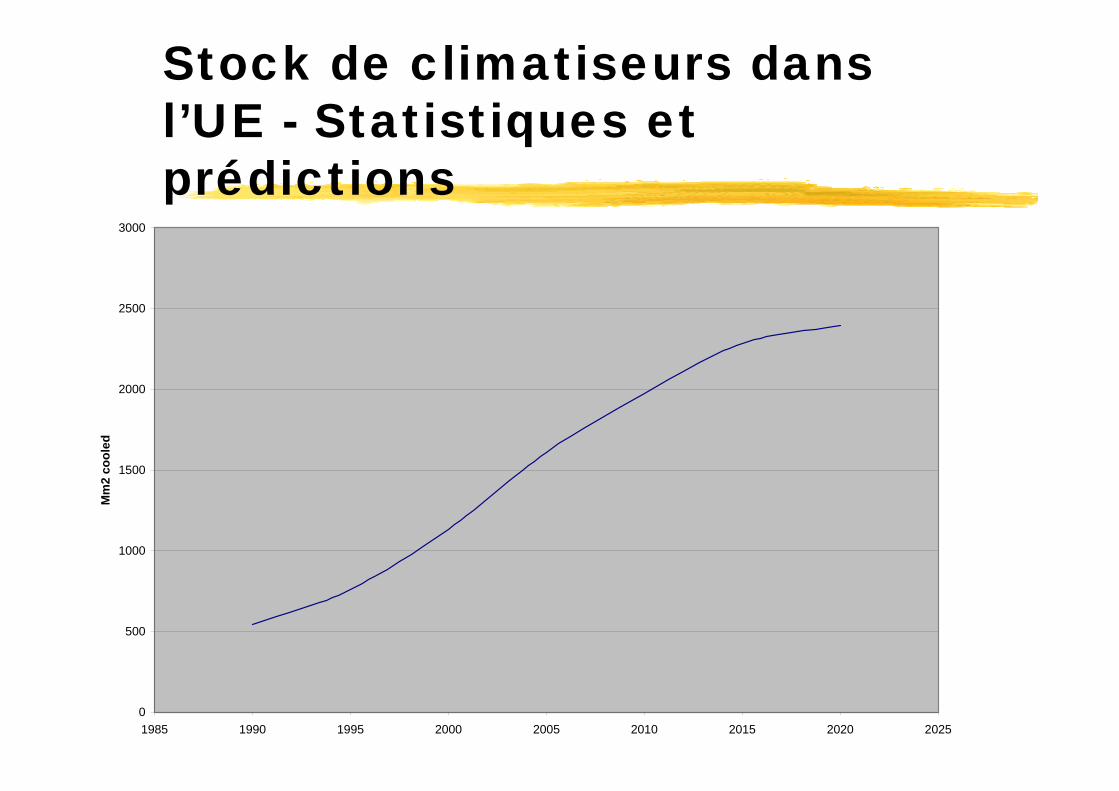

Stock de climatiseurs dans l’UE - Statistiques et prédictions

0

500

1000

1500

2000

2500

3000

1985 1990 1995 2000 2005 2010 2015 2020 2025

Mm

2 co

oled

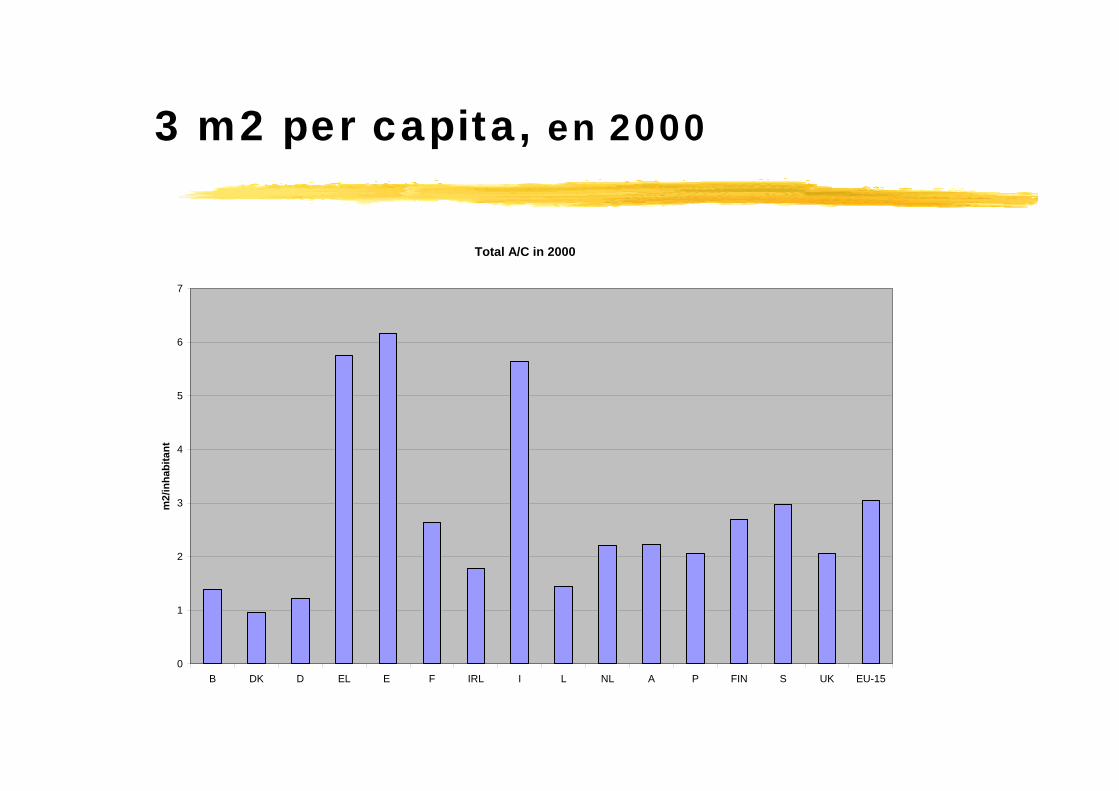

3 m2 per capita, en 2000

Total A/C in 2000

0

1

2

3

4

5

6

7

B DK D EL E F IRL I L NL A P FIN S UK EU-15

m2/

inha

bita

nt

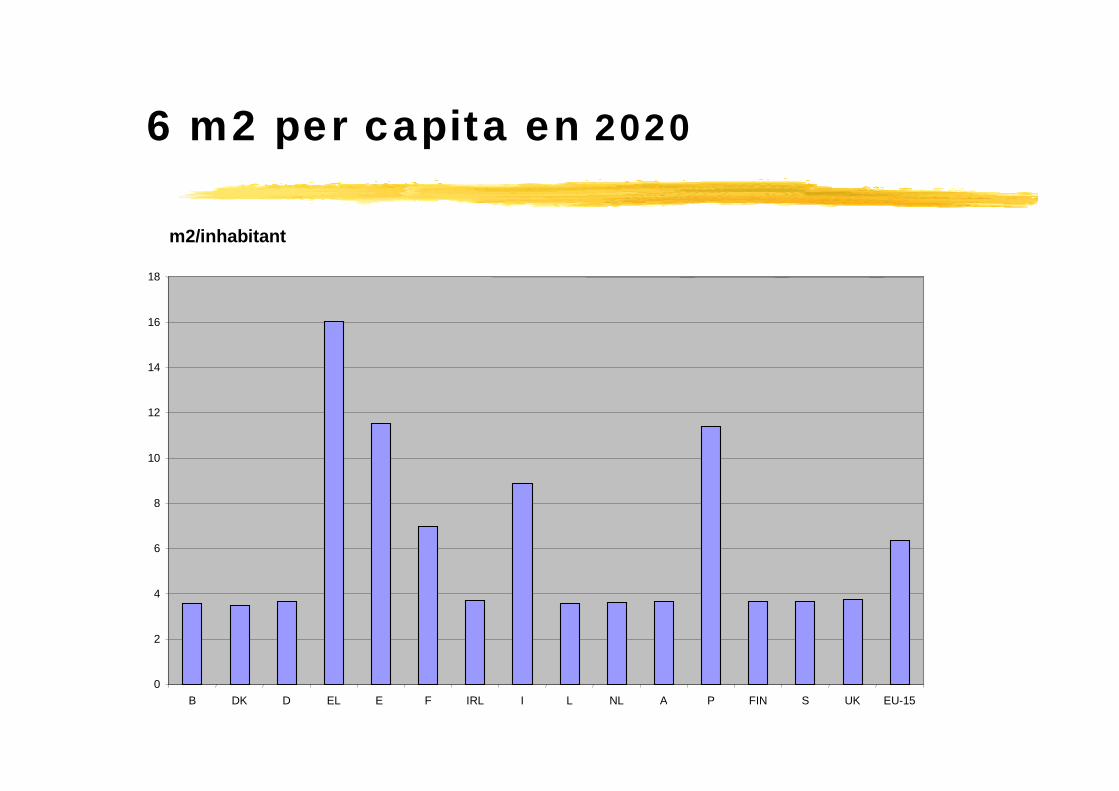

6 m2 per capita en 2020

m2/inhabitant

0

2

4

6

8

10

12

14

16

18

B DK D EL E F IRL I L NL A P FIN S UK EU-15

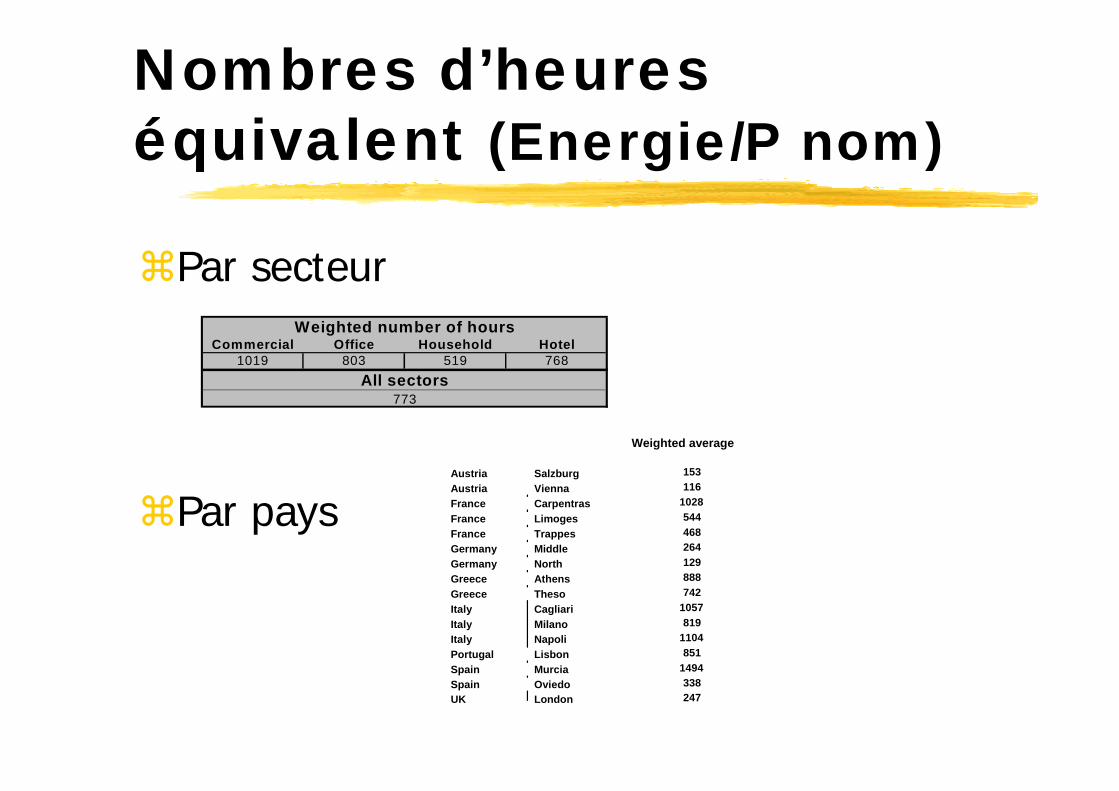

Nombres d’heures équivalent (Energie/P nom)

Par secteur

Par pays

Commercial Office Household Hotel1019 803 519 768

Weighted number of hours

773All sectors

Austria SalzburgAustria ViennaFrance CarpentrasFrance LimogesFrance TrappesGermany MiddleGermany NorthGreece AthensGreece ThesoItaly CagliariItaly MilanoItaly NapoliPortugal LisbonSpain MurciaSpain OviedoUK London

153116

1028544468264129888742

1057819

1104851

1494338247

Weighted average

Des contrastes géographiques à ne pas négliger

CommercesNumber of hours of air conditioning in the commercial sector

752

199

431

1017

1366

984

85912652157

678

1226

790

1414

230

177 134

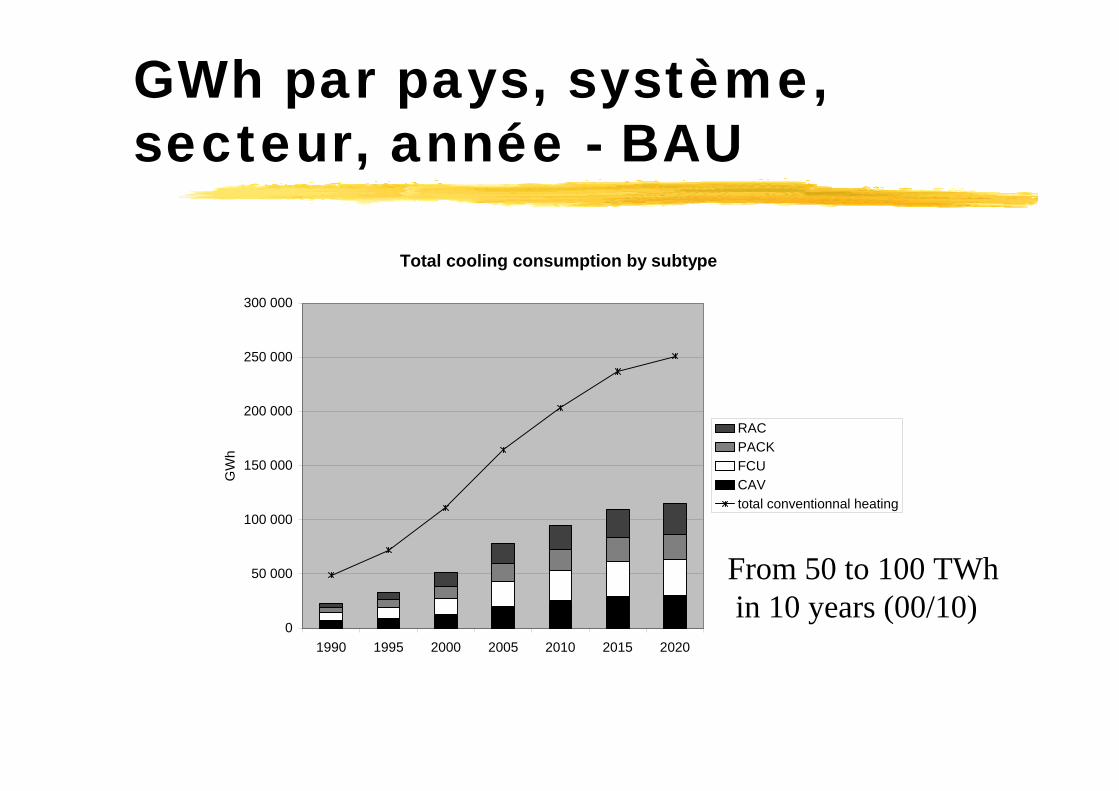

GWh par pays, système, secteur, année - BAU

Total cooling consumption by subtype

0

50 000

100 000

150 000

200 000

250 000

300 000

1990 1995 2000 2005 2010 2015 2020

GW

h

RACPACKFCUCAVtotal conventionnal heating

From 50 to 100 TWhin 10 years (00/10)

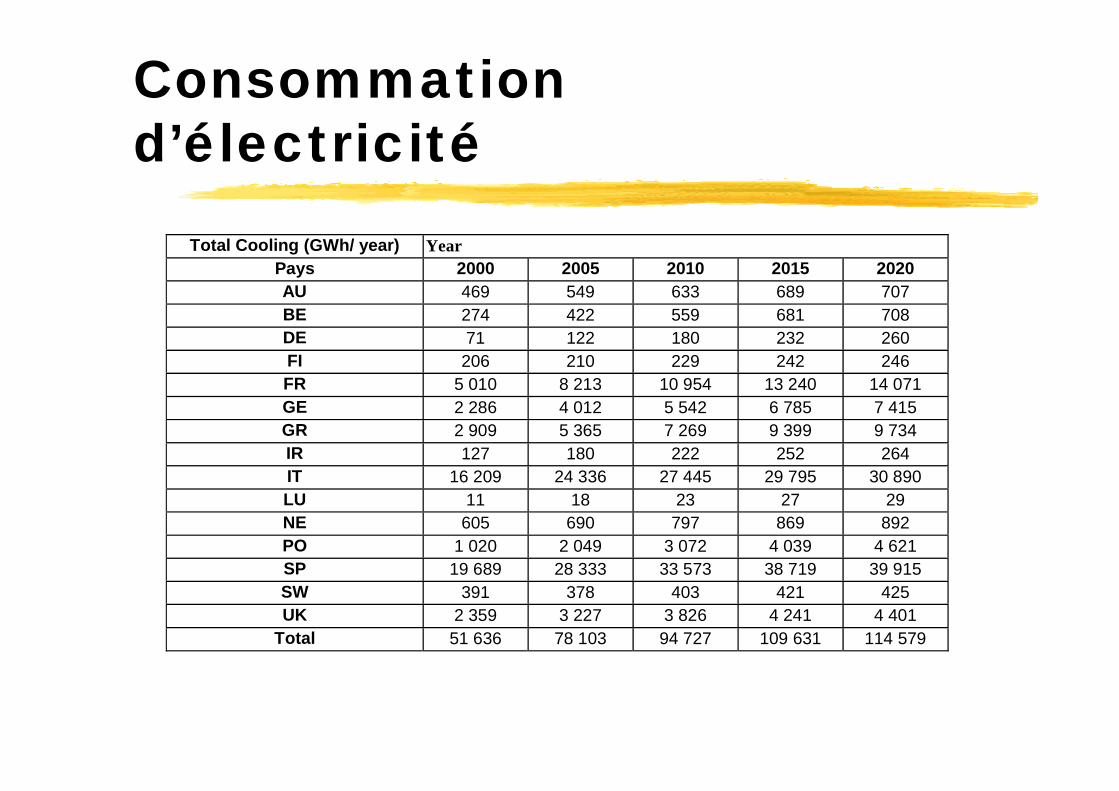

Consommation d’électricité

Total Cooling (GWh/ year) Year Pays 2000 2005 2010 2015 2020 AU 469 549 633 689 707 BE 274 422 559 681 708 DE 71 122 180 232 260 FI 206 210 229 242 246 FR 5 010 8 213 10 954 13 240 14 071 GE 2 286 4 012 5 542 6 785 7 415 GR 2 909 5 365 7 269 9 399 9 734 IR 127 180 222 252 264 IT 16 209 24 336 27 445 29 795 30 890 LU 11 18 23 27 29 NE 605 690 797 869 892 PO 1 020 2 049 3 072 4 039 4 621 SP 19 689 28 333 33 573 38 719 39 915 SW 391 378 403 421 425 UK 2 359 3 227 3 826 4 241 4 401

Total 51 636 78 103 94 727 109 631 114 579

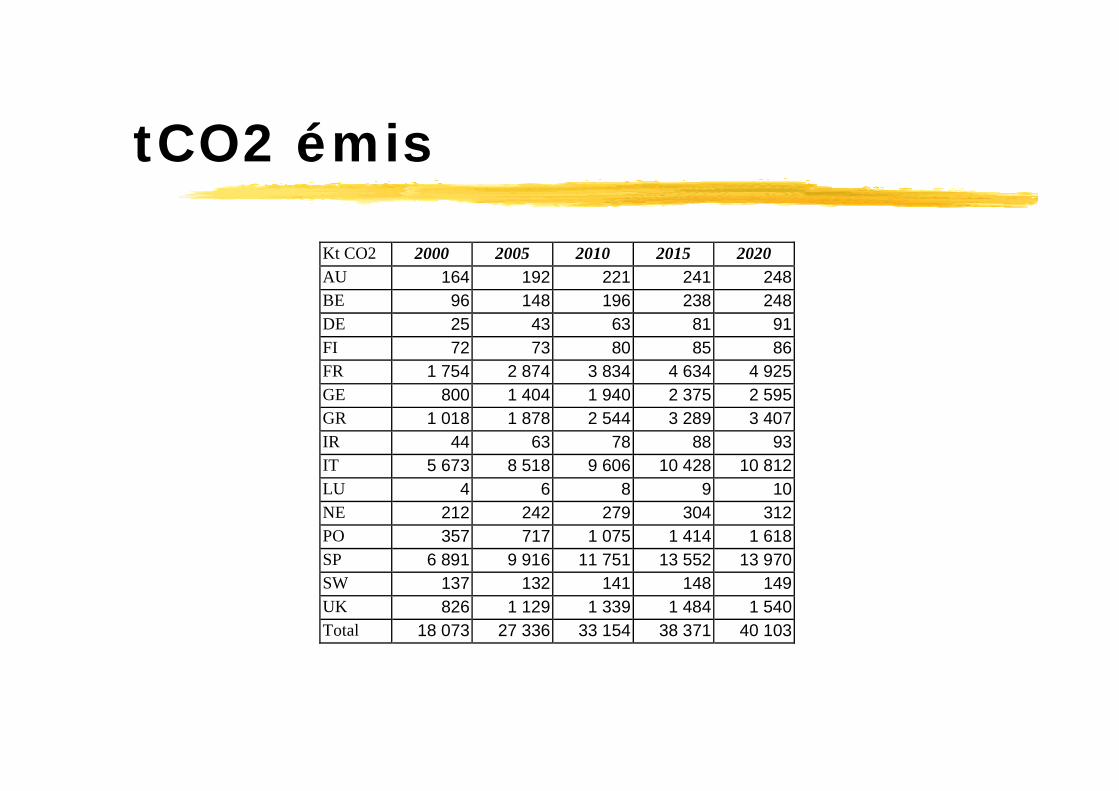

tCO2 émis

Kt CO2 2000 2005 2010 2015 2020AU 164 192 221 241 248BE 96 148 196 238 248DE 25 43 63 81 91FI 72 73 80 85 86FR 1 754 2 874 3 834 4 634 4 925GE 800 1 404 1 940 2 375 2 595GR 1 018 1 878 2 544 3 289 3 407IR 44 63 78 88 93IT 5 673 8 518 9 606 10 428 10 812LU 4 6 8 9 10NE 212 242 279 304 312PO 357 717 1 075 1 414 1 618SP 6 891 9 916 11 751 13 552 13 970SW 137 132 141 148 149UK 826 1 129 1 339 1 484 1 540Total 18 073 27 336 33 154 38 371 40 103

Un marché de produits sans aucun règlement

On s’intéresse à l’efficacité énergétique : comment assurer la fonction demandée avec

moins d’énergie et « plus d’équipement »

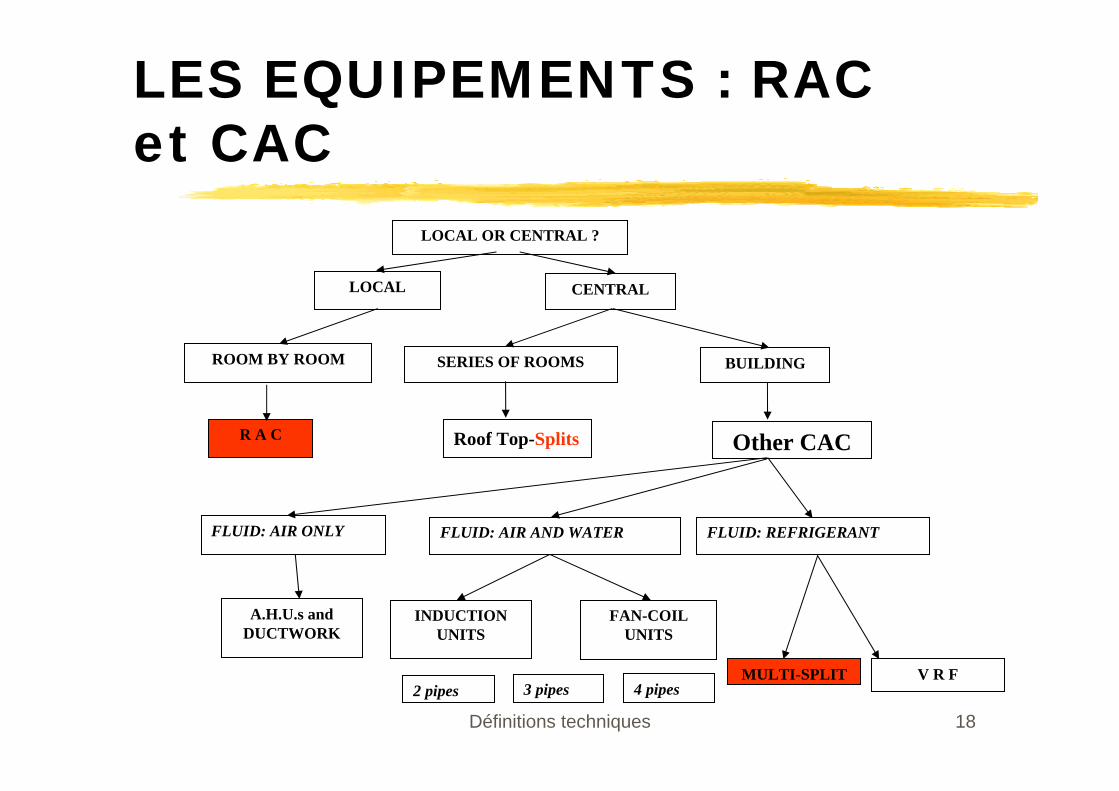

Définitions techniques 18

LES EQUIPEMENTS : RAC et CAC

LOCAL OR CENTRAL ?

LOCAL CENTRAL

ROOM BY ROOM

Roof Top-Splits

SERIES OF ROOMS BUILDING

R A C Other CAC

FLUID: AIR ONLY FLUID: AIR AND WATER FLUID: REFRIGERANT

A.H.U.s andDUCTWORK

INDUCTION UNITS

FAN-COIL UNITS

2 pipes 3 pipes 4 pipesMULTI-SPLIT V R F

Définitions techniques 19

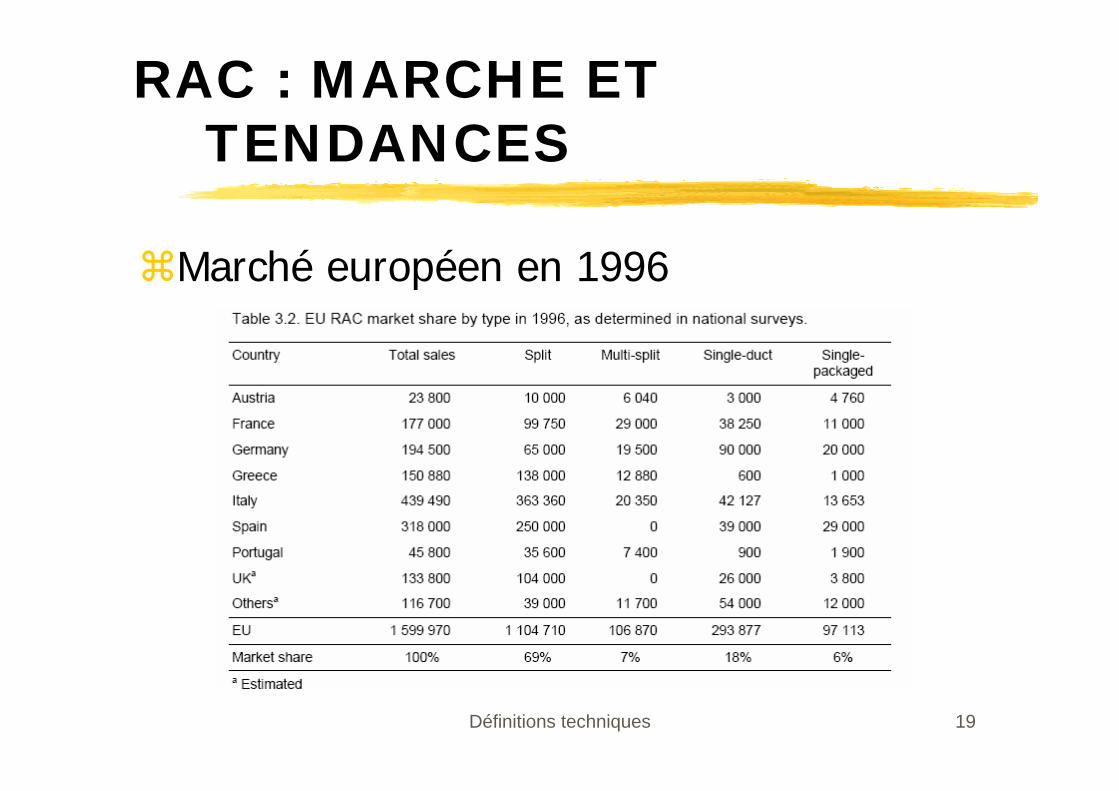

RAC : MARCHE ET TENDANCES

Marché européen en 1996

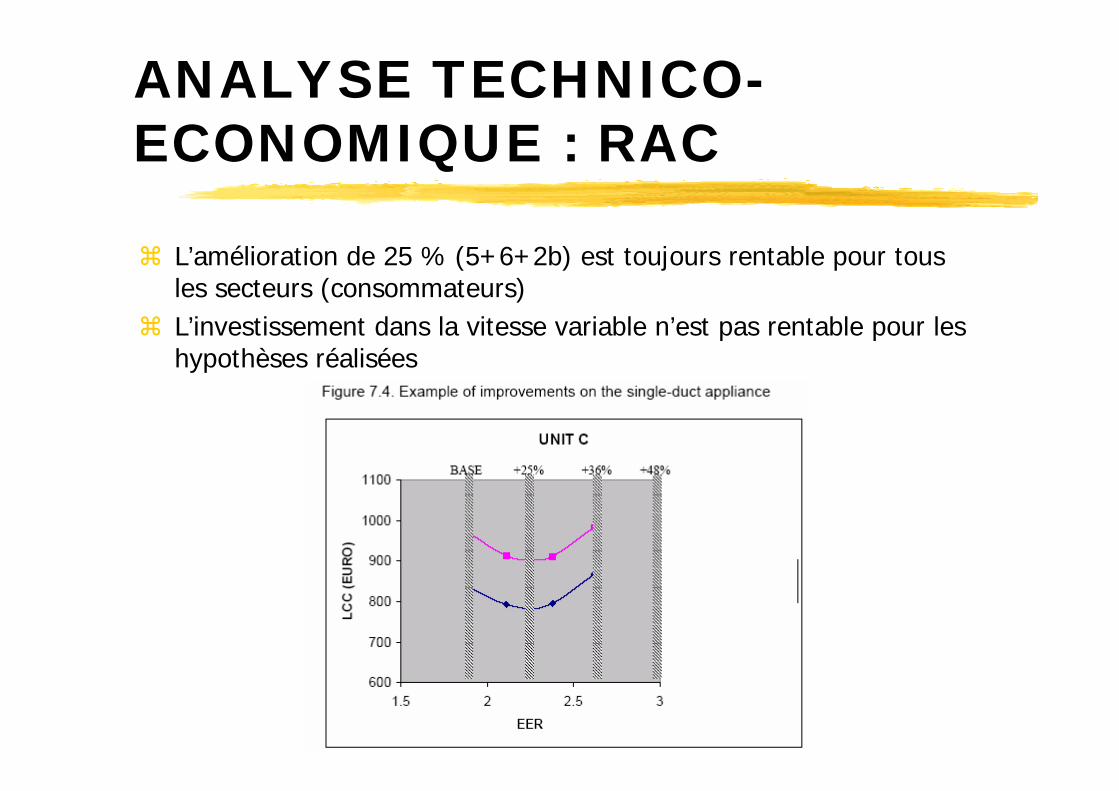

ANALYSE TECHNICO-ECONOMIQUE : RAC

L’amélioration de 25 % (5+6+2b) est toujours rentable pour tous les secteurs (consommateurs)L’investissement dans la vitesse variable n’est pas rentable pour les hypothèses réalisées

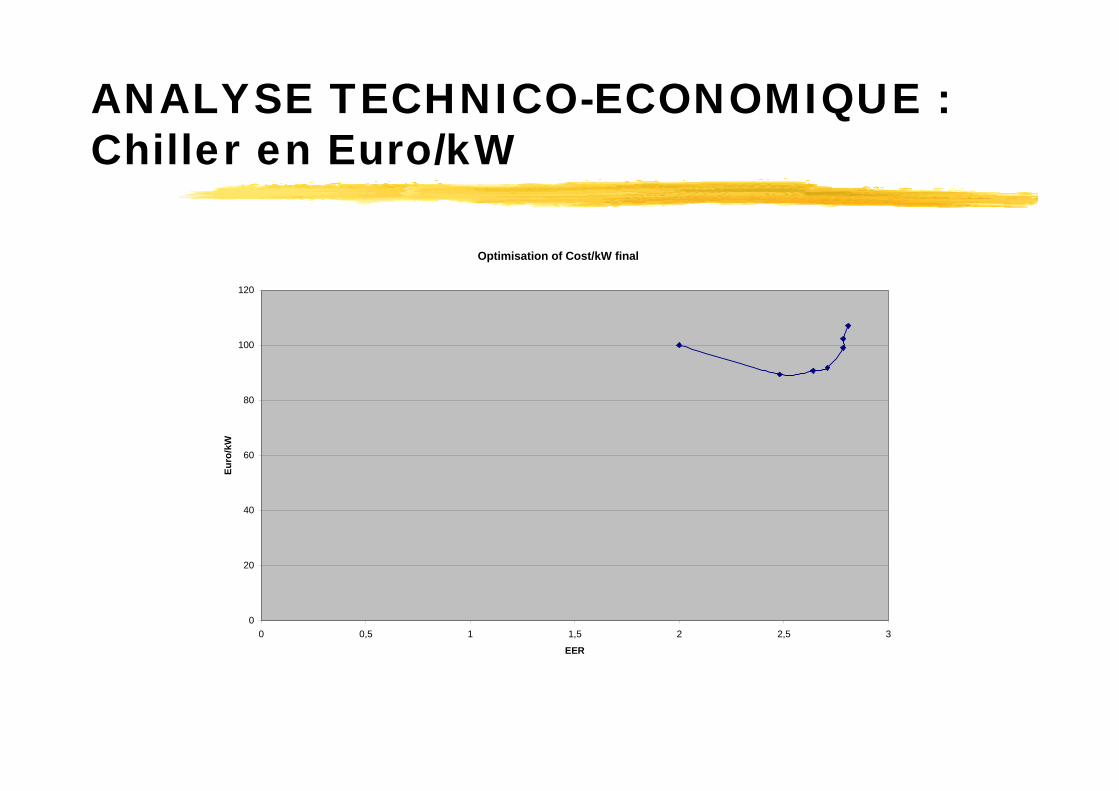

ANALYSE TECHNICO-ECONOMIQUE : Chiller en Euro/kW

Optimisation of Cost/kW final

0

20

40

60

80

100

120

0 0,5 1 1,5 2 2,5 3

EER

Euro

/kW

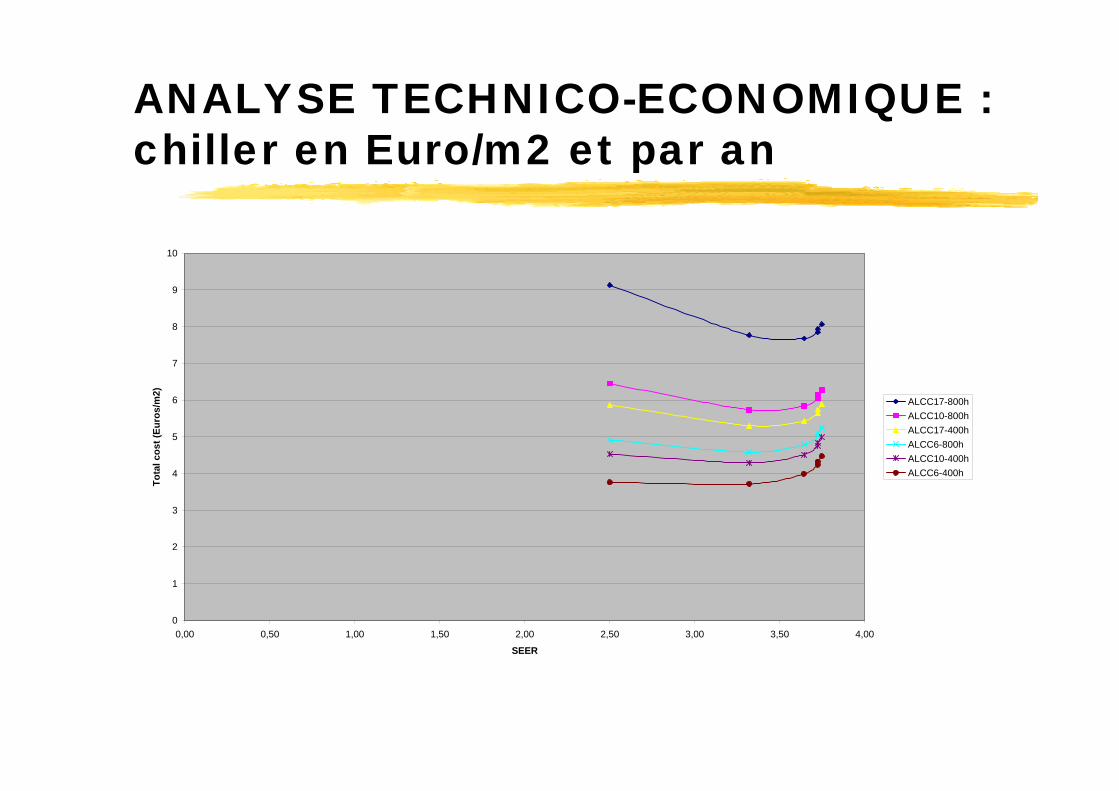

ANALYSE TECHNICO-ECONOMIQUE : chiller en Euro/m2 et par an

0

1

2

3

4

5

6

7

8

9

10

0,00 0,50 1,00 1,50 2,00 2,50 3,00 3,50 4,00

SEER

Tota

l cos

t (Eu

ros/

m2)

ALCC17-800hALCC10-800hALCC17-400hALCC6-800hALCC10-400hALCC6-400h

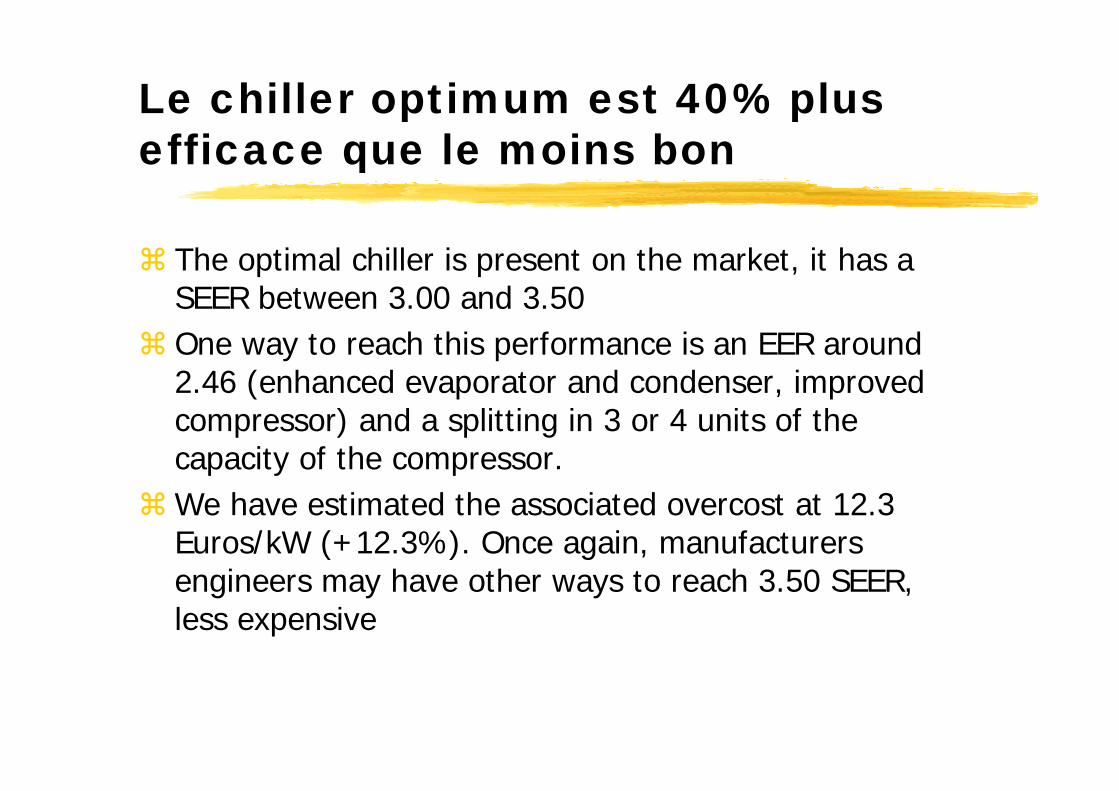

Le chiller optimum est 40% plus efficace que le moins bon

The optimal chiller is present on the market, it has a SEER between 3.00 and 3.50One way to reach this performance is an EER around 2.46 (enhanced evaporator and condenser, improved compressor) and a splitting in 3 or 4 units of the capacity of the compressor.We have estimated the associated overcost at 12.3 Euros/kW (+12.3%). Once again, manufacturers engineers may have other ways to reach 3.50 SEER, less expensive

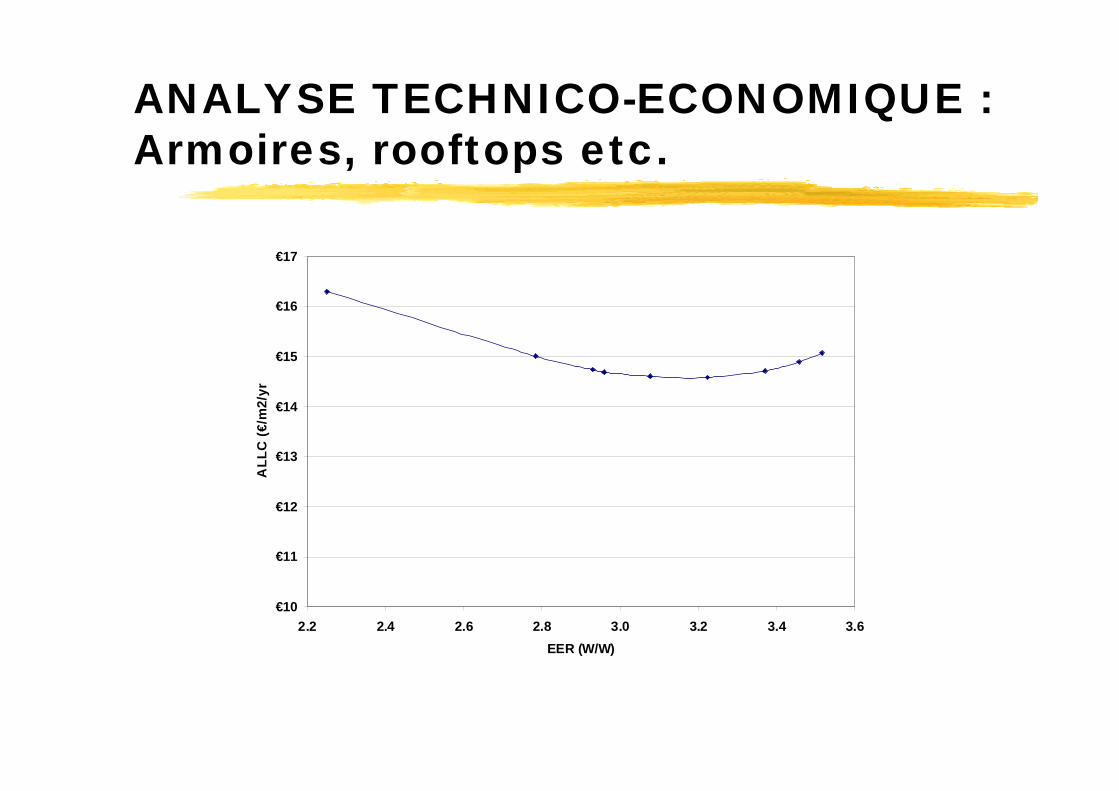

ANALYSE TECHNICO-ECONOMIQUE : Armoires, rooftops etc.

€10

€11

€12

€13

€14

€15

€16

€17

2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6EER (W/W)

ALL

C (€

/m2/

yr

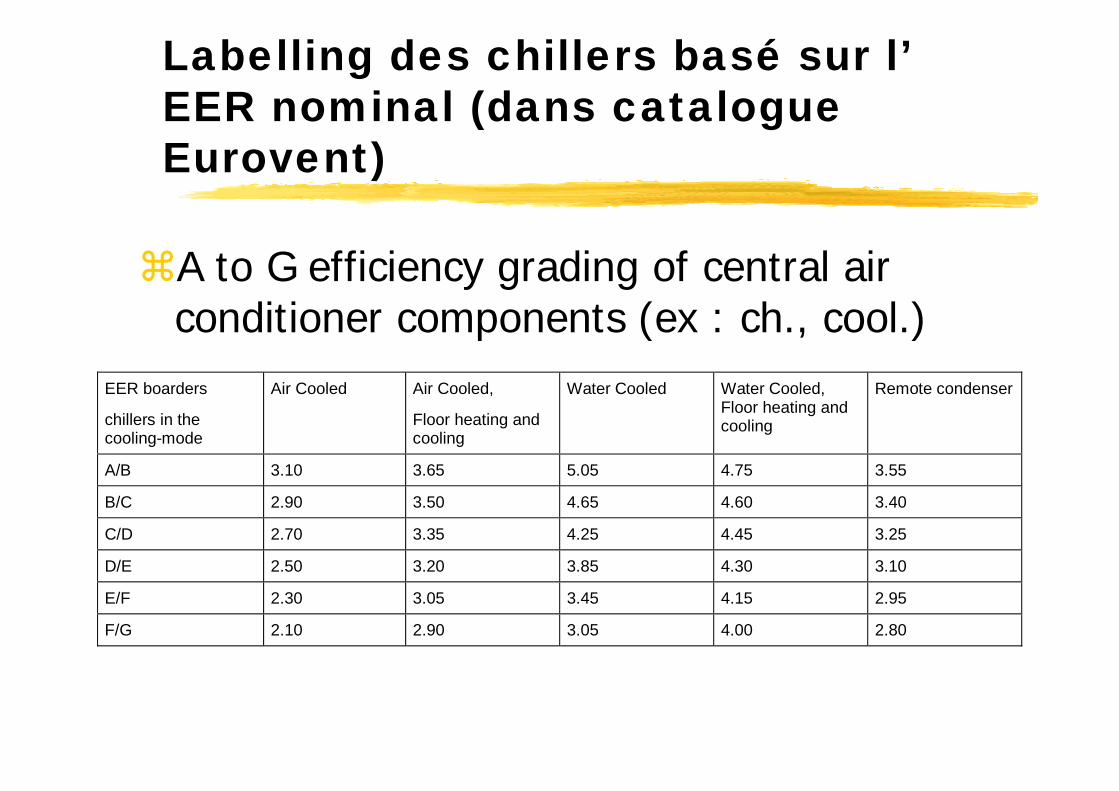

Labelling des chillers basé sur l’EER nominal (dans catalogue Eurovent)

A to G efficiency grading of central air conditioner components (ex : ch., cool.)

EER boarders

chillers in thecooling-mode

Air Cooled Air Cooled,

Floor heating andcooling

Water Cooled Water Cooled,Floor heating andcooling

Remote condenser

A/B 3.10 3.65 5.05 4.75 3.55

B/C 2.90 3.50 4.65 4.60 3.40

C/D 2.70 3.35 4.25 4.45 3.25

D/E 2.50 3.20 3.85 4.30 3.10

E/F 2.30 3.05 3.45 4.15 2.95

F/G 2.10 2.90 3.05 4.00 2.80

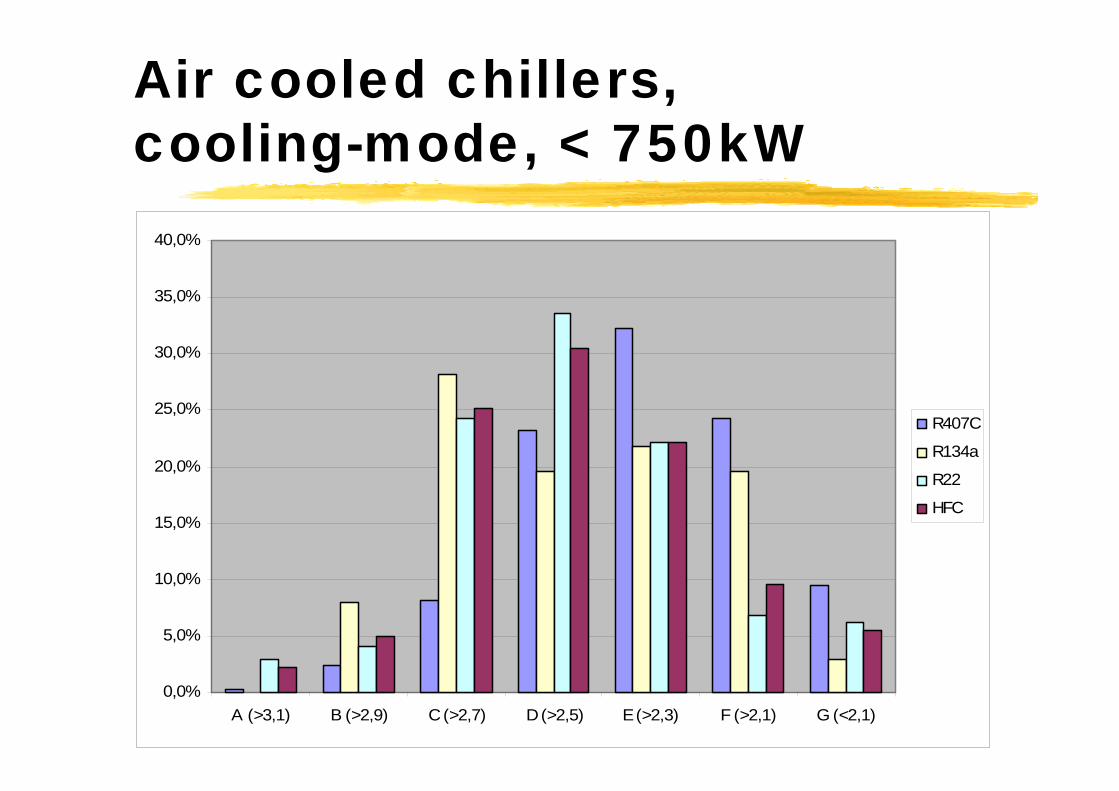

Air cooled chillers, cooling-mode, < 750kW

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

40,0%

A (>3,1) B (>2,9) C (>2,7) D (>2,5) E (>2,3) F (>2,1) G (<2,1)

R407C

R134a

R22

HFC

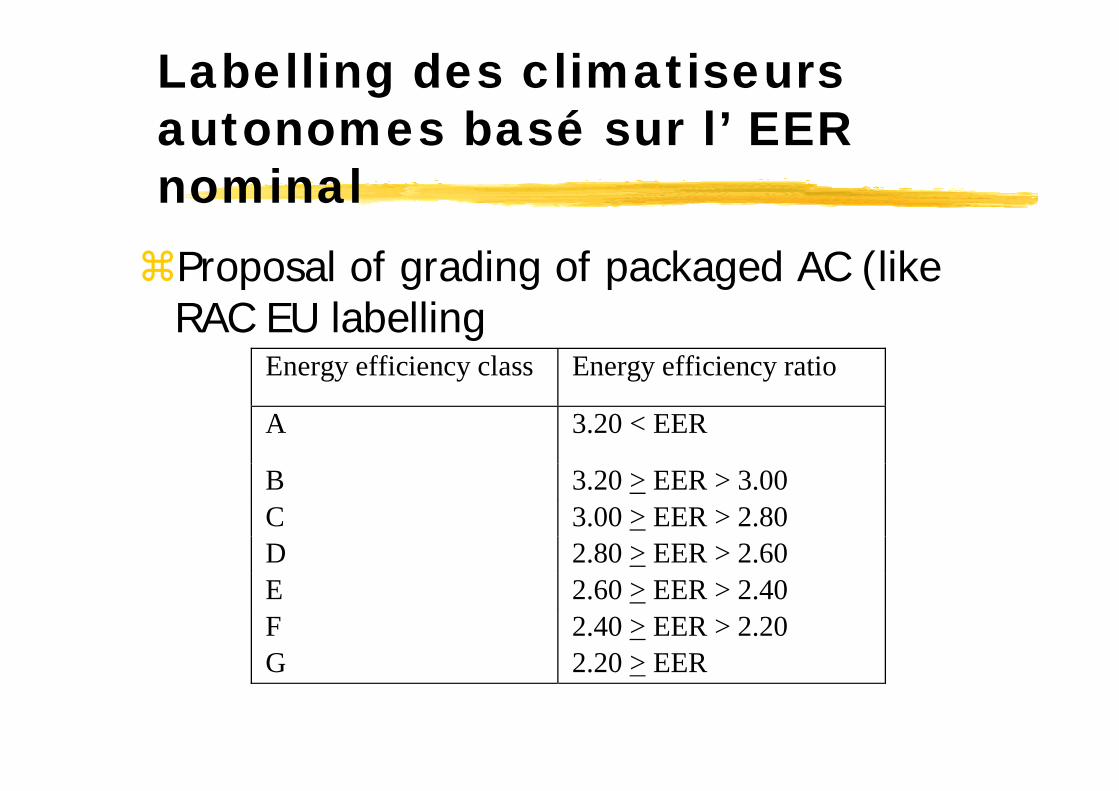

Labelling des climatiseurs autonomes basé sur l’ EER nominalProposal of grading of packaged AC (likeRAC EU labelling

Energy efficiency class Energy efficiency ratio

A 3.20 < EER

B 3.20 > EER > 3.00C 3.00 > EER > 2.80D 2.80 > EER > 2.60E 2.60 > EER > 2.40F 2.40 > EER > 2.20G 2.20 > EER

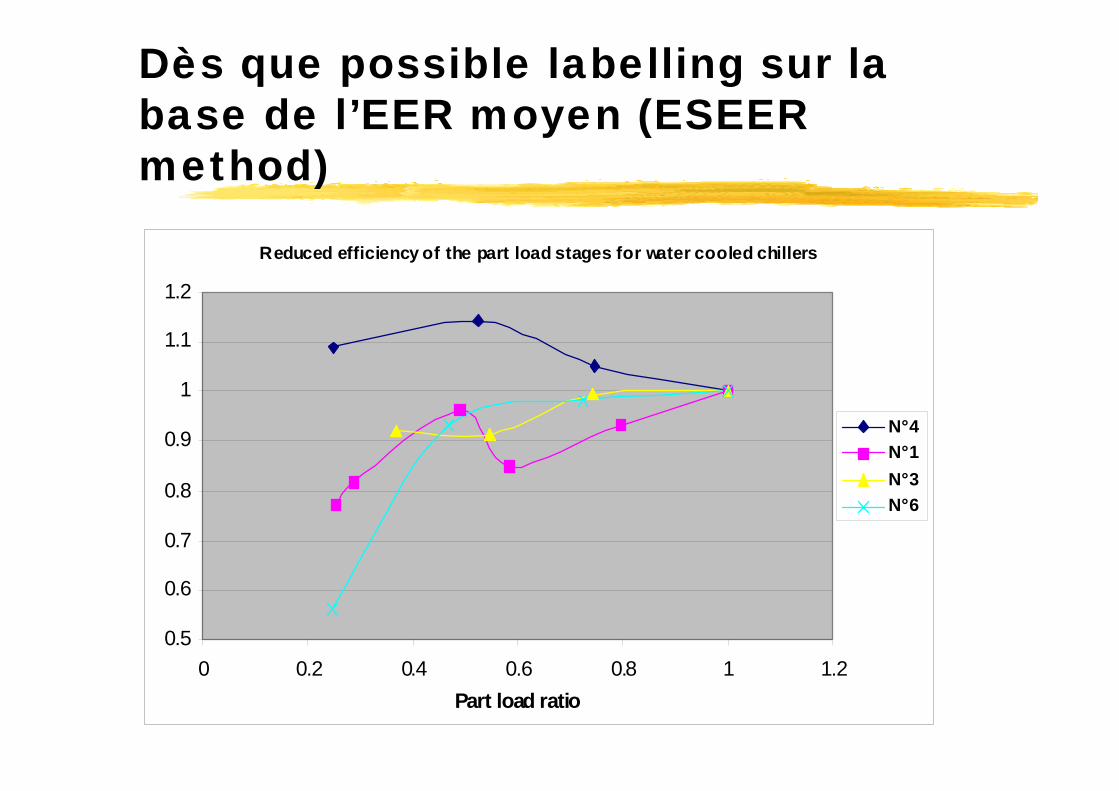

Dès que possible labelling sur la base de l’EER moyen (ESEER method)

Reduced efficiency of the part load stages for water cooled chillers

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

0 0.2 0.4 0.6 0.8 1 1.2Part load ratio

N° 4N° 1N° 3N° 6

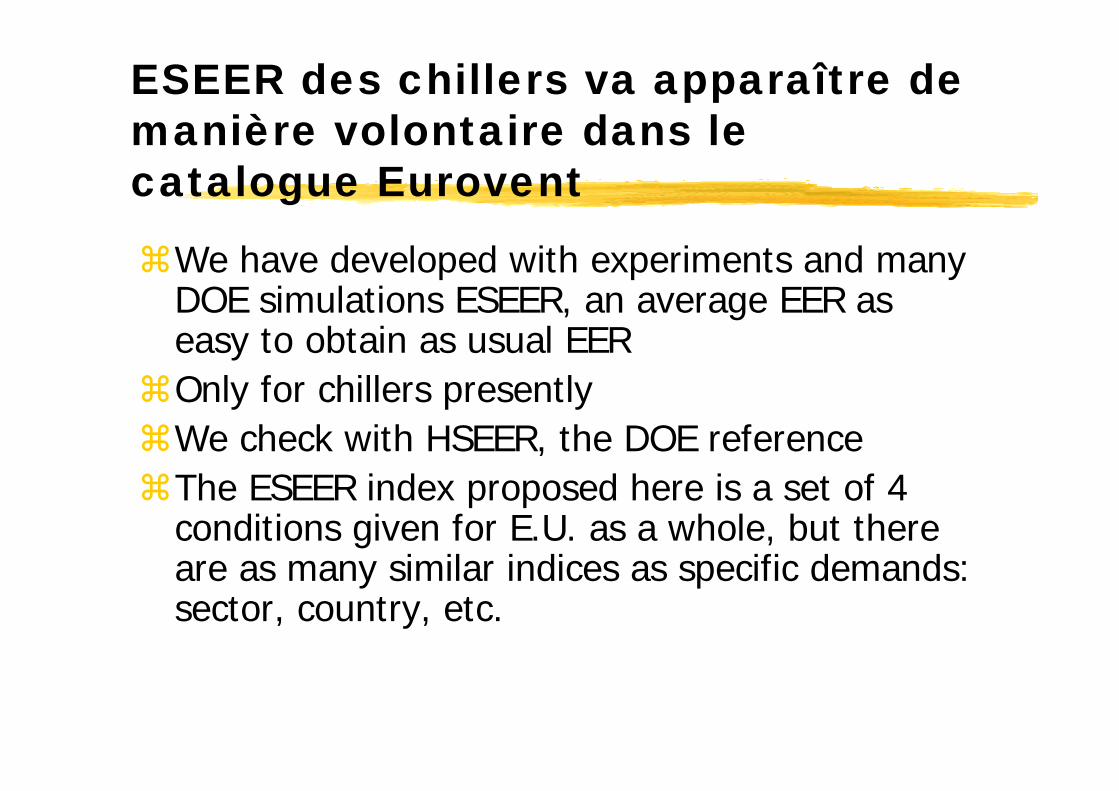

ESEER des chillers va apparaître de manière volontaire dans le catalogue Eurovent

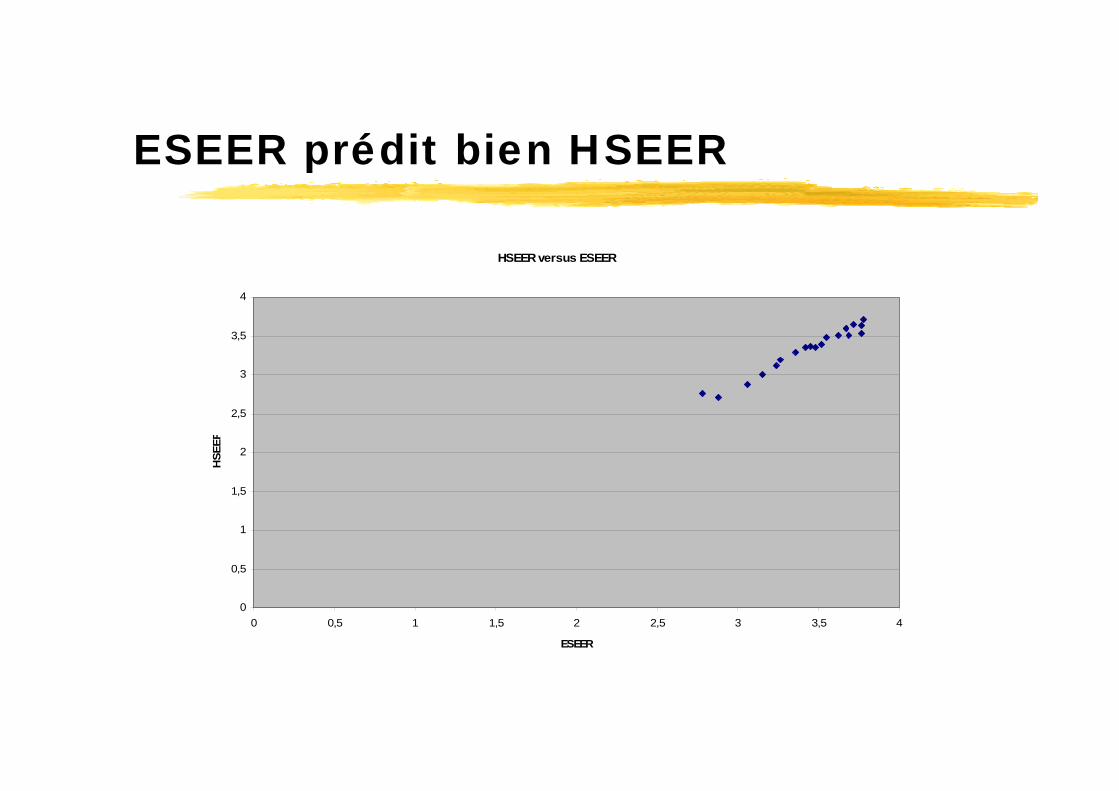

We have developed with experiments and many DOE simulations ESEER, an average EER as easy to obtain as usual EEROnly for chillers presentlyWe check with HSEER, the DOE referenceThe ESEER index proposed here is a set of 4 conditions given for E.U. as a whole, but there are as many similar indices as specific demands: sector, country, etc.

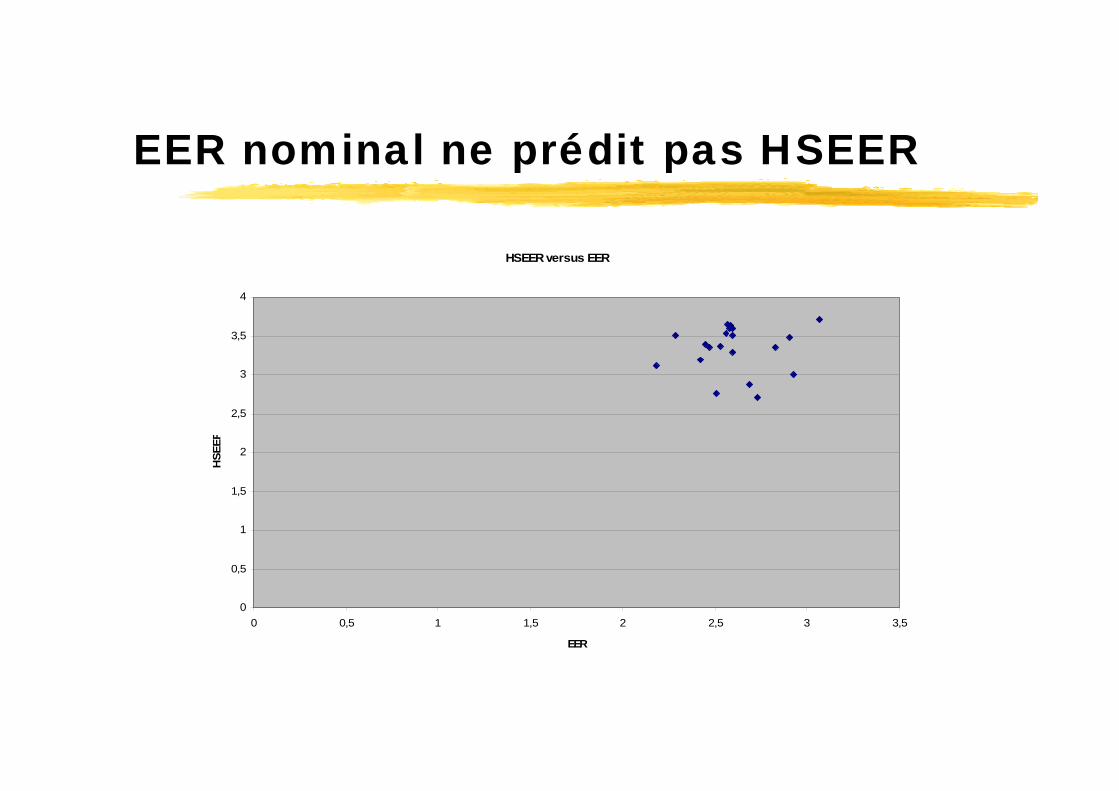

EER nominal ne prédit pas HSEER

HSEER versus EER

0

0,5

1

1,5

2

2,5

3

3,5

4

0 0,5 1 1,5 2 2,5 3 3,5

EER

HSE

ER

ESEER prédit bien HSEER

HSEER versus ESEER

0

0,5

1

1,5

2

2,5

3

3,5

4

0 0,5 1 1,5 2 2,5 3 3,5 4

ESEER

HSE

ER

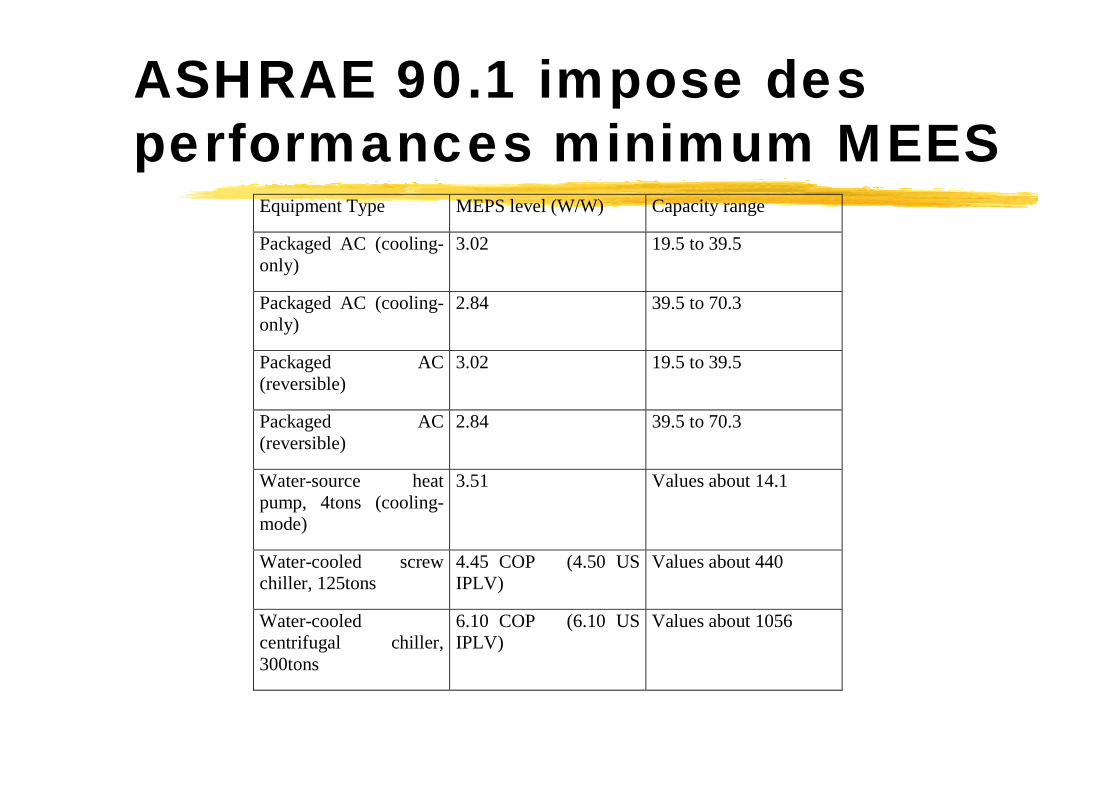

ASHRAE 90.1 impose des performances minimum MEES

Equipment Type MEPS level (W/W) Capacity range

Packaged AC (cooling-only)

3.02 19.5 to 39.5

Packaged AC (cooling-only)

2.84 39.5 to 70.3

Packaged AC(reversible)

3.02 19.5 to 39.5

Packaged AC(reversible)

2.84 39.5 to 70.3

Water-source heatpump, 4tons (cooling-mode)

3.51 Values about 14.1

Water-cooled screwchiller, 125tons

4.45 COP (4.50 USIPLV)

Values about 440

Water-cooledcentrifugal chiller,300tons

6.10 COP (6.10 USIPLV)

Values about 1056

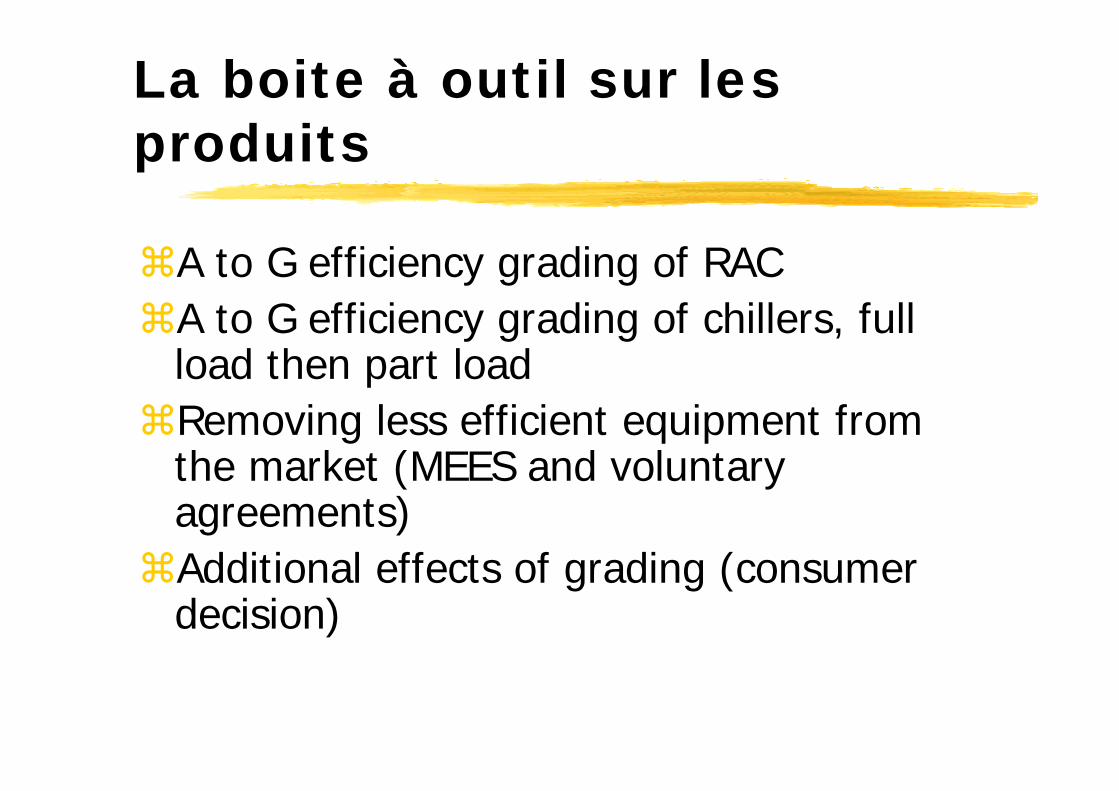

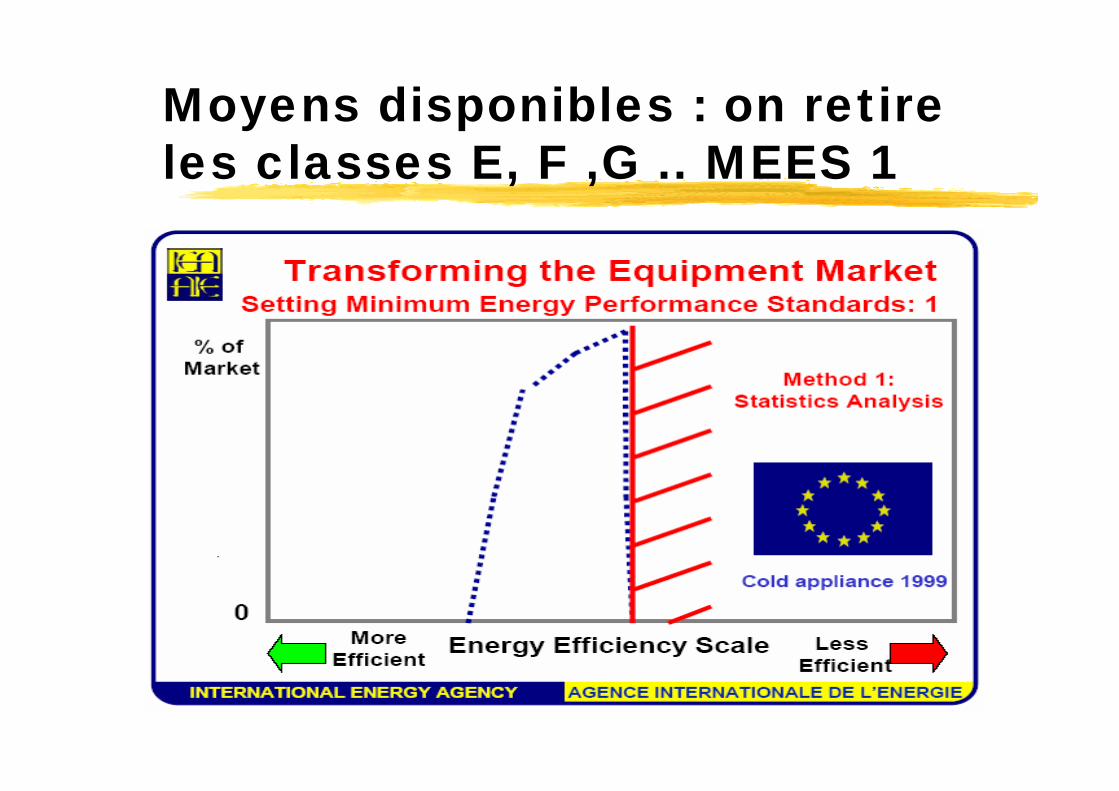

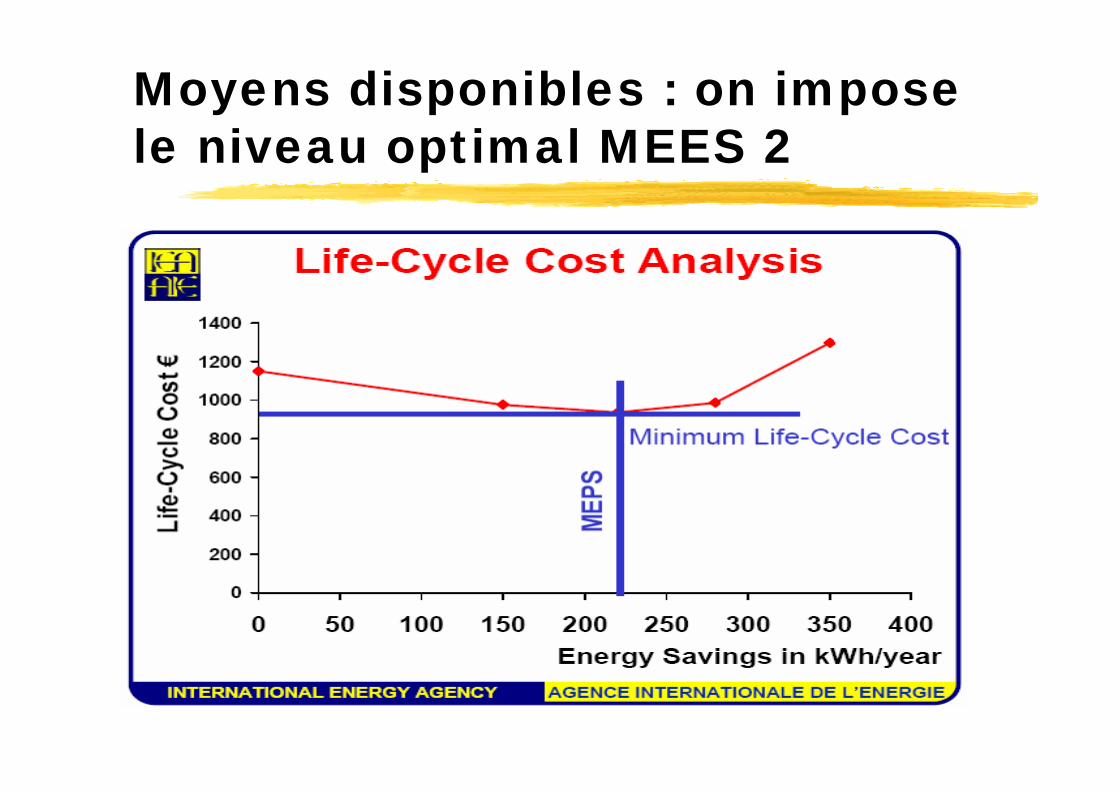

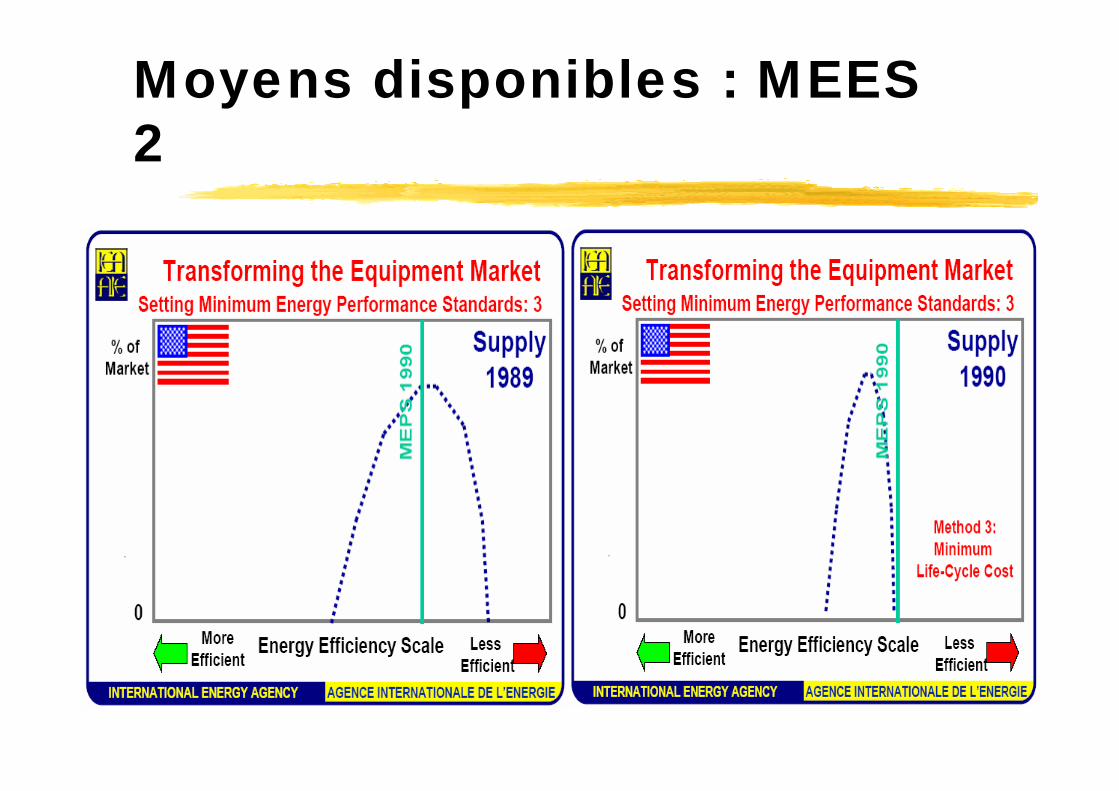

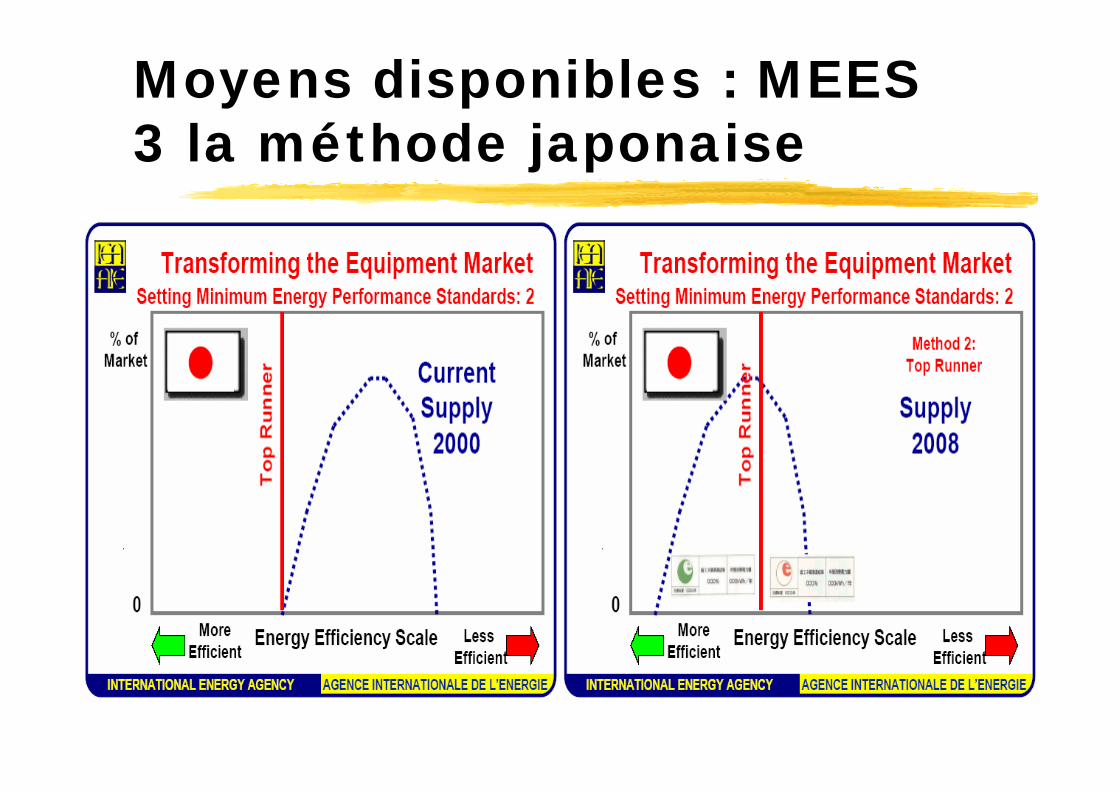

La boite à outil sur les produits

A to G efficiency grading of RACA to G efficiency grading of chillers, full load then part loadRemoving less efficient equipment from the market (MEES and voluntaryagreements)Additional effects of grading (consumer decision)

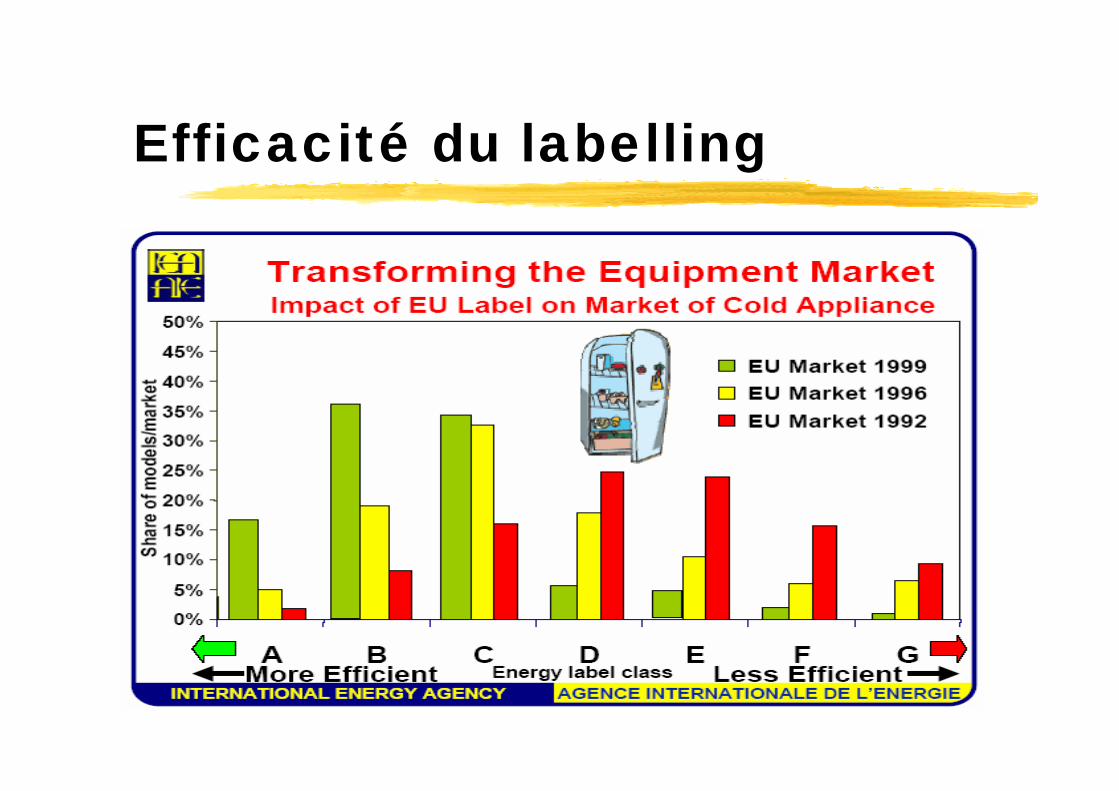

Efficacité du labelling

Moyens disponibles : on retire les classes E, F ,G .. MEES 1

Moyens disponibles : on impose le niveau optimal MEES 2

Moyens disponibles : MEES 2

Moyens disponibles : MEES 3 la méthode japonaise

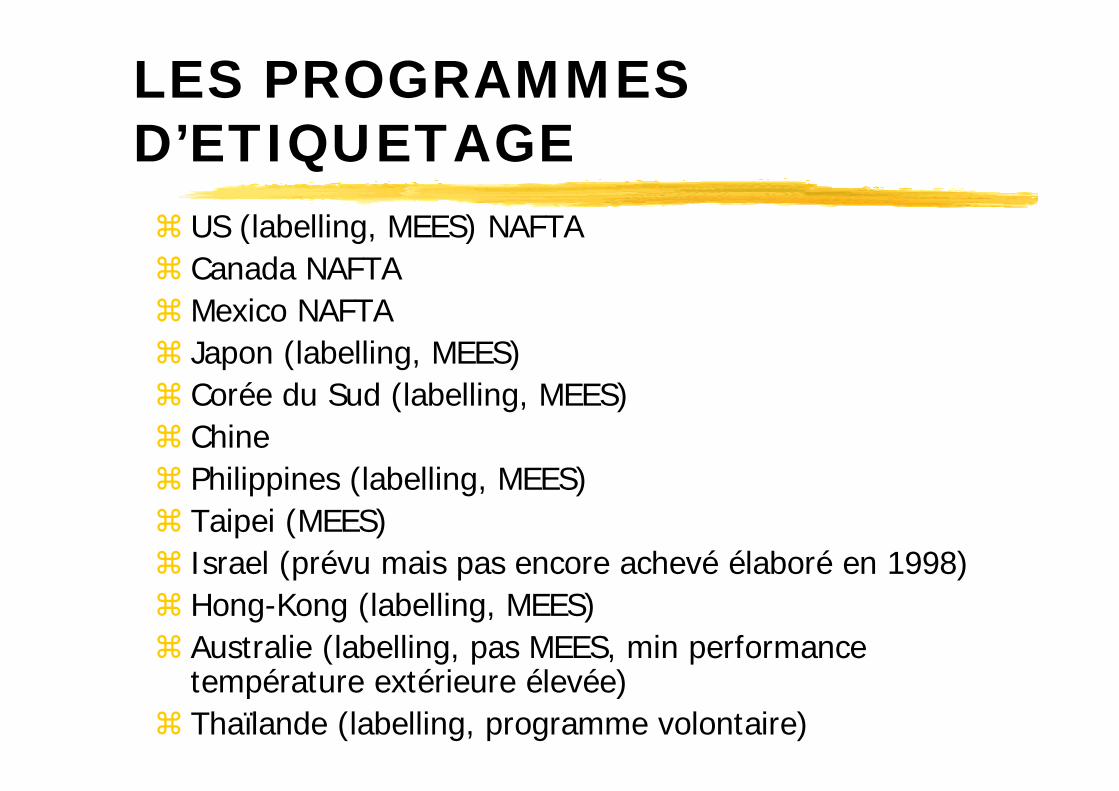

LES PROGRAMMESD’ETIQUETAGE

US (labelling, MEES) NAFTACanada NAFTAMexico NAFTAJapon (labelling, MEES)Corée du Sud (labelling, MEES)ChinePhilippines (labelling, MEES)Taipei (MEES)Israel (prévu mais pas encore achevé élaboré en 1998)Hong-Kong (labelling, MEES)Australie (labelling, pas MEES, min performance température extérieure élevée)Thaïlande (labelling, programme volontaire)

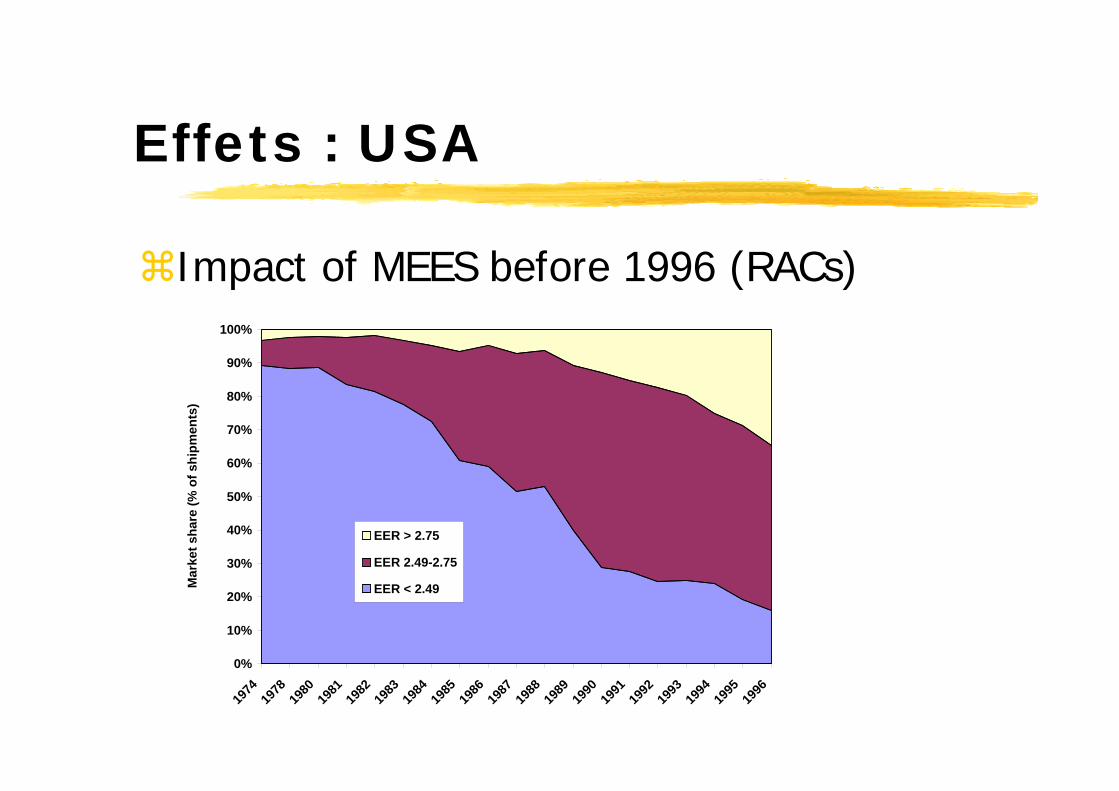

Effets : USA

Impact of MEES before 1996 (RACs)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1974

1978

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

Mar

ket s

hare

(% o

f shi

pmen

ts)

EER > 2.75

EER 2.49-2.75

EER < 2.49

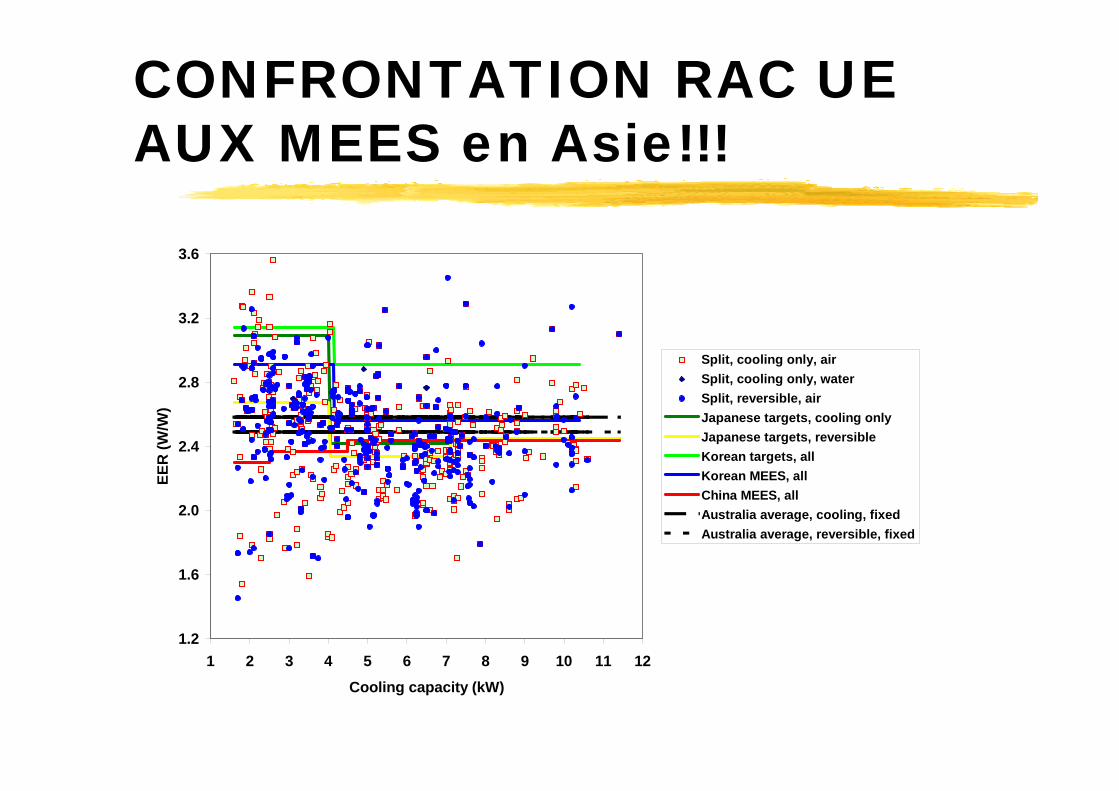

CONFRONTATION RAC UE AUX MEES en Asie!!!

1.2

1.6

2.0

2.4

2.8

3.2

3.6

1 2 3 4 5 6 7 8 9 10 11 12

Cooling capacity (kW)

EER

(W/W

)

Split, cooling only, airSplit, cooling only, waterSplit, reversible, airJapanese targets, cooling onlyJapanese targets, reversibleKorean targets, allKorean MEES, allChina MEES, allAustralia average, cooling, fixedAustralia average, reversible, fixed

Un marché de conception, presque sans règlement

On s’intéresse à l’efficacité énergétique : comment assurer la fonction demandée avec moins d’énergie et « plus d’intelligence » ou

« plus de régulation»

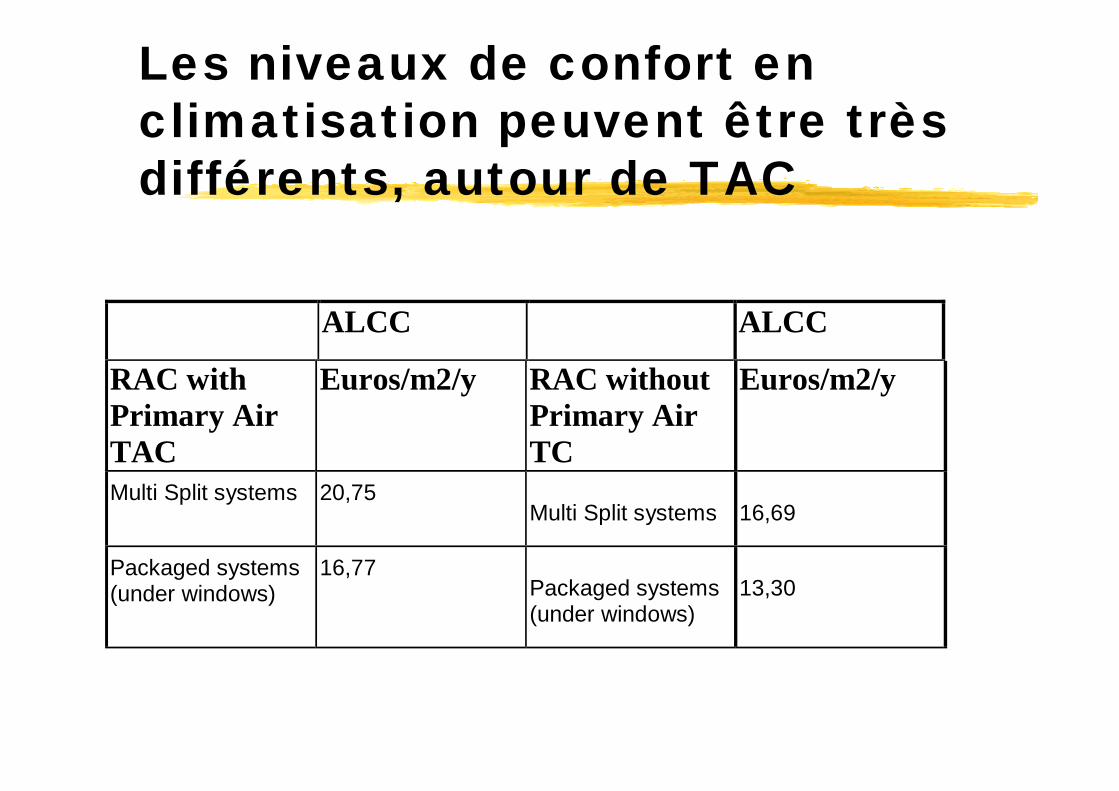

Les niveaux de confort en climatisation peuvent être trèsdifférents, autour de TAC

ALCC ALCC

RAC withPrimary AirTAC

Euros/m2/y RAC withoutPrimary AirTC

Euros/m2/y

Multi Split systems 20,75Multi Split systems 16,69

Packaged systems(under windows)

16,77Packaged systems(under windows)

13,30

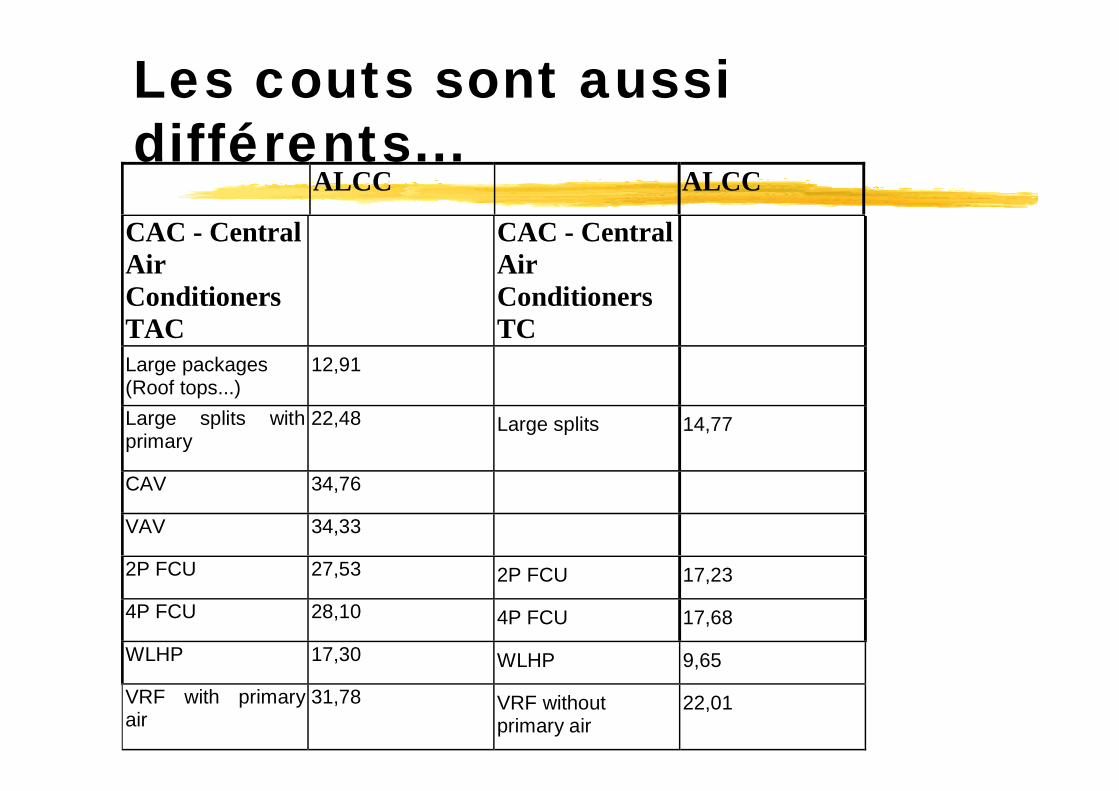

Les couts sont aussidifférents...

ALCC ALCC

CAC - CentralAirConditionersTAC

CAC - CentralAirConditionersTC

Large packages(Roof tops...)

12,91

Large splits withprimary

22,48 Large splits 14,77

CAV 34,76

VAV 34,33

2P FCU 27,53 2P FCU 17,23

4P FCU 28,10 4P FCU 17,68

WLHP 17,30 WLHP 9,65

VRF with primaryair

31,78 VRF withoutprimary air

22,01

DOE2 pour les simulations et extrapolation par DJ

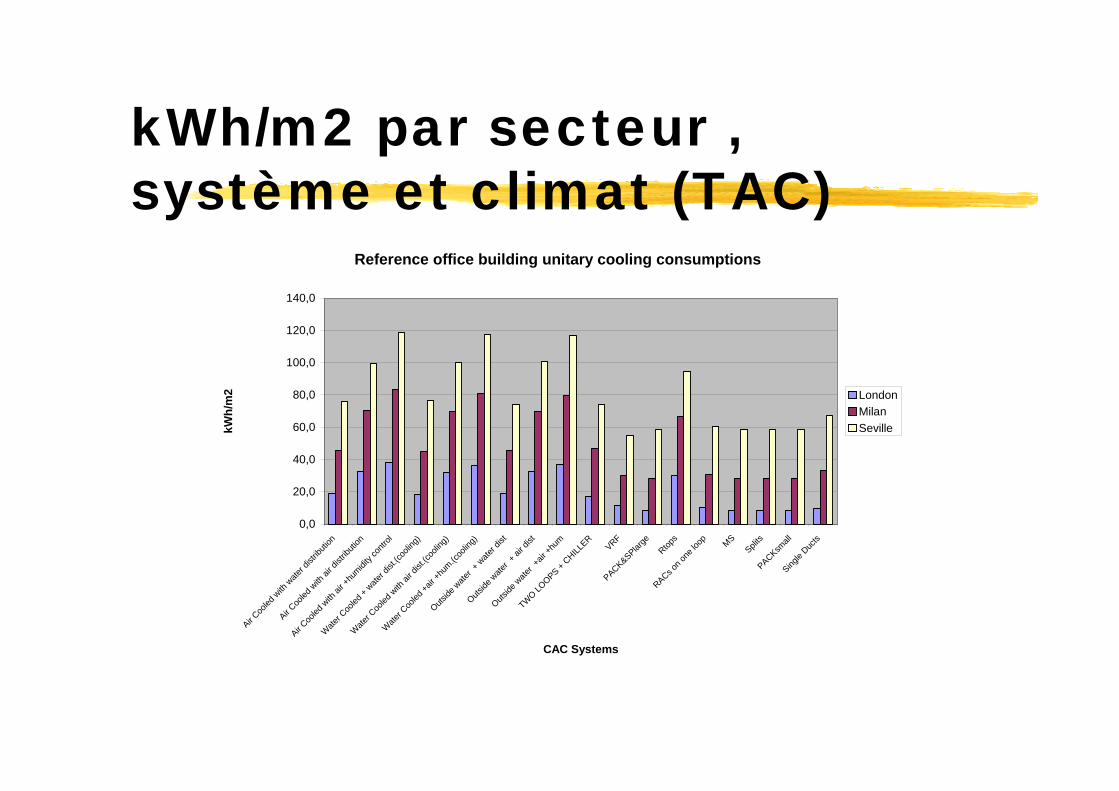

kWh/m2 par secteur , système et climat (TAC)

Reference office building unitary cooling consumptions

0,0

20,0

40,0

60,0

80,0

100,0

120,0

140,0

Air Coo

led w

ith w

ater d

istrib

ution

Air Coo

led w

ith ai

r dist

ributi

on

Air Coo

led w

ith ai

r +hu

midity

contr

ol

Wate

r Coo

led +

water d

ist.(c

oolin

g)

Wate

r Coo

led w

ith ai

r dist

.(coo

ling)

Wate

r Coo

led +a

ir +hu

m.(coo

ling)

Outside

wate

r + w

ater d

ist

Outside

wate

r + ai

r dist

Outside

wate

r +air

+hum

TWO LOOPS +

CHILLER

VRFPACK&SPlar

ge

Rtops

RACs on o

ne lo

op

MS

Splits

PACKsmall

Single

Ducts

CAC Systems

kWh/

m2 London

MilanSeville

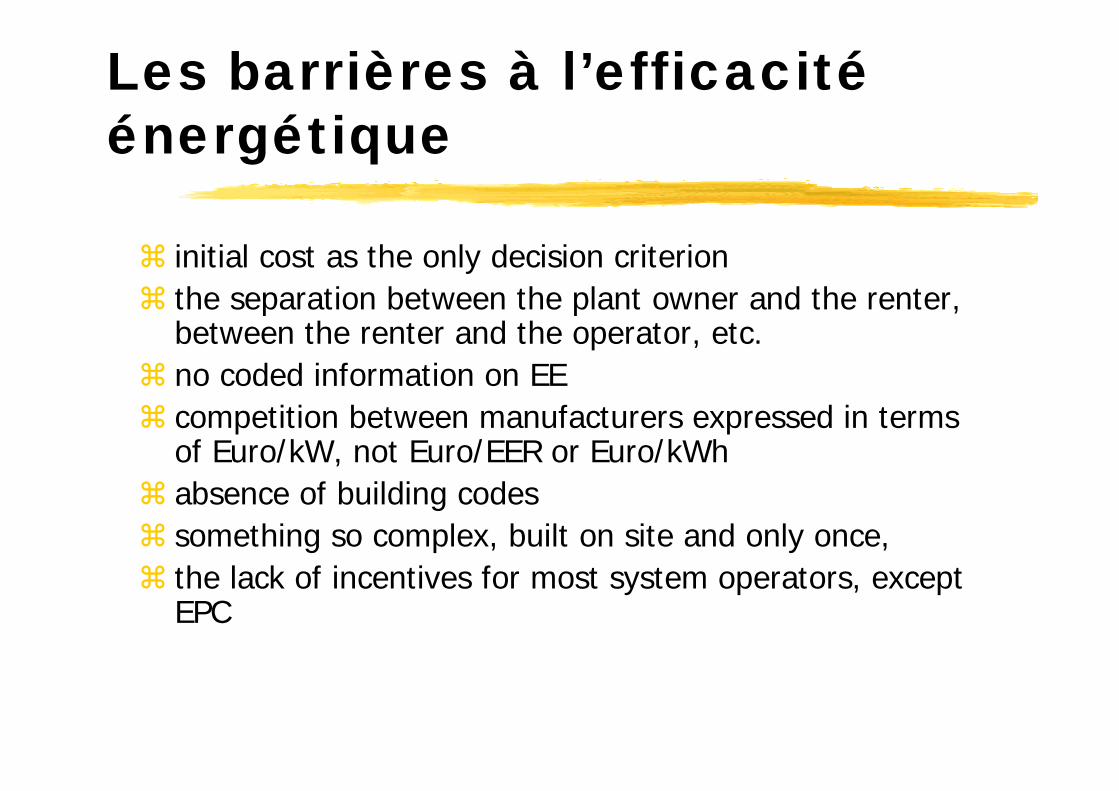

Les barrières à l’efficacitéénergétique

initial cost as the only decision criterionthe separation between the plant owner and the renter,between the renter and the operator, etc. no coded information on EEcompetition between manufacturers expressed in termsof Euro/kW, not Euro/EER or Euro/kWhabsence of building codessomething so complex, built on site and only once,the lack of incentives for most system operators, exceptEPC

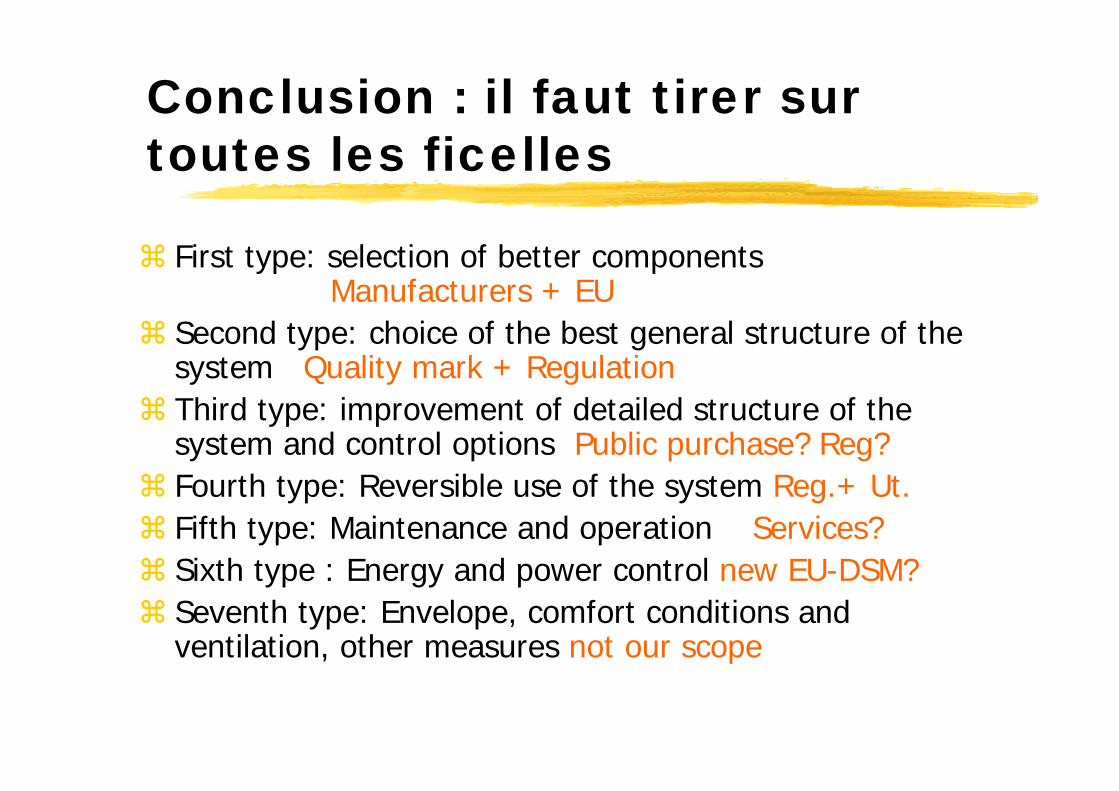

Conclusion : il faut tirer sur toutes les ficelles

First type: selection of better components Manufacturers + EU

Second type: choice of the best general structure of the system Quality mark + RegulationThird type: improvement of detailed structure of the system and control options Public purchase? Reg?Fourth type: Reversible use of the system Reg.+ Ut.Fifth type: Maintenance and operation Services?Sixth type : Energy and power control new EU-DSM?Seventh type: Envelope, comfort conditions and ventilation, other measures not our scope

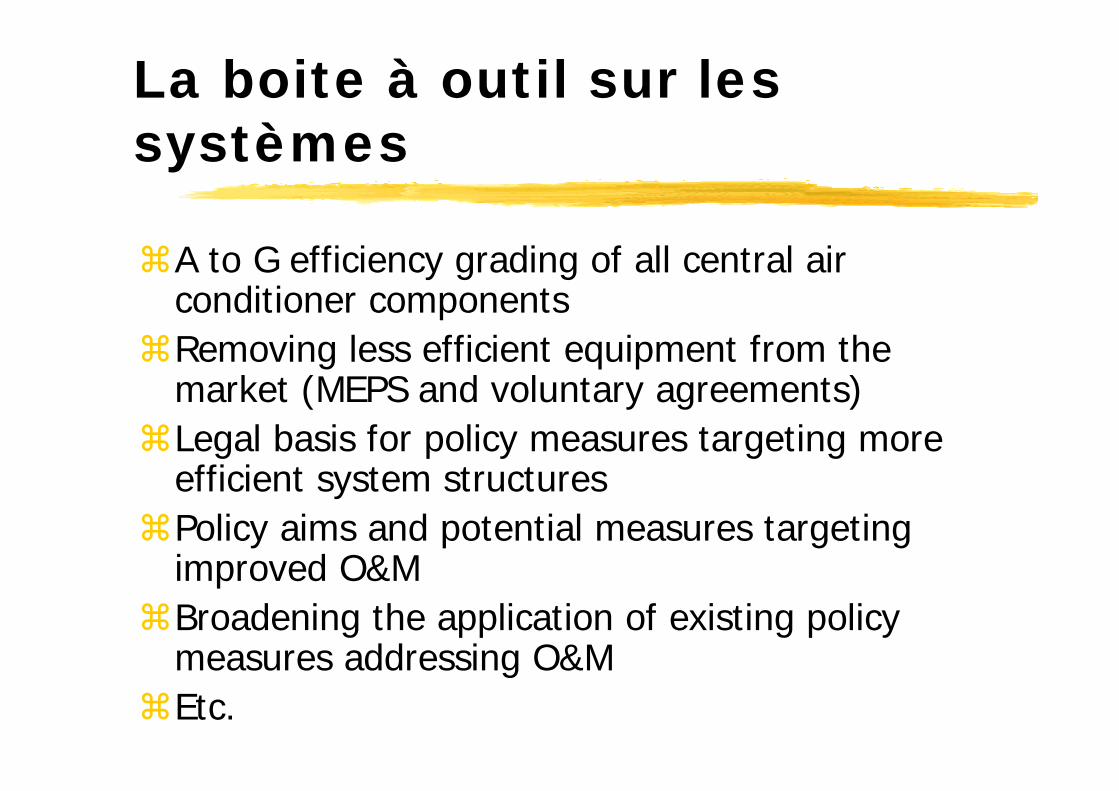

La boite à outil sur les systèmes

A to G efficiency grading of all central airconditioner componentsRemoving less efficient equipment from the market (MEPS and voluntary agreements)Legal basis for policy measures targeting more efficient system structuresPolicy aims and potential measures targeting improved O&MBroadening the application of existing policy measures addressing O&MEtc.

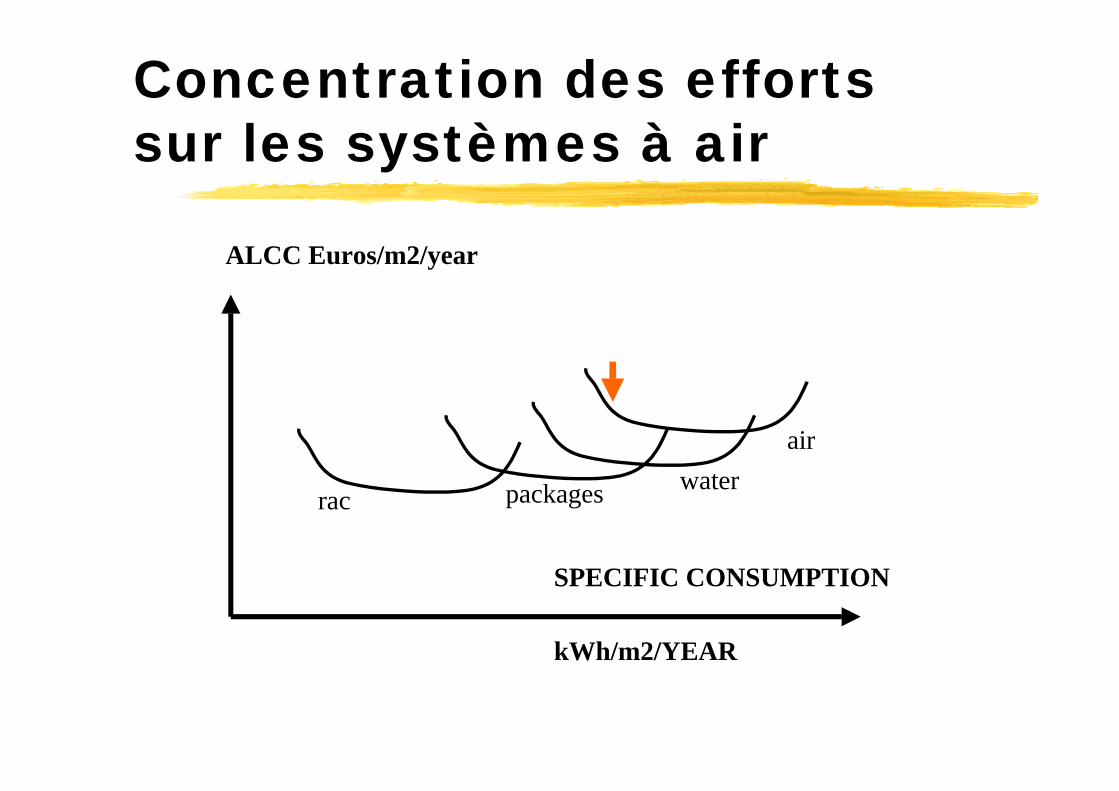

Concentration des efforts sur les systèmes à air

SPECIFIC CONSUMPTION

ALCC Euros/m2/year

kWh/m2/YEAR

airwaterpackagesrac

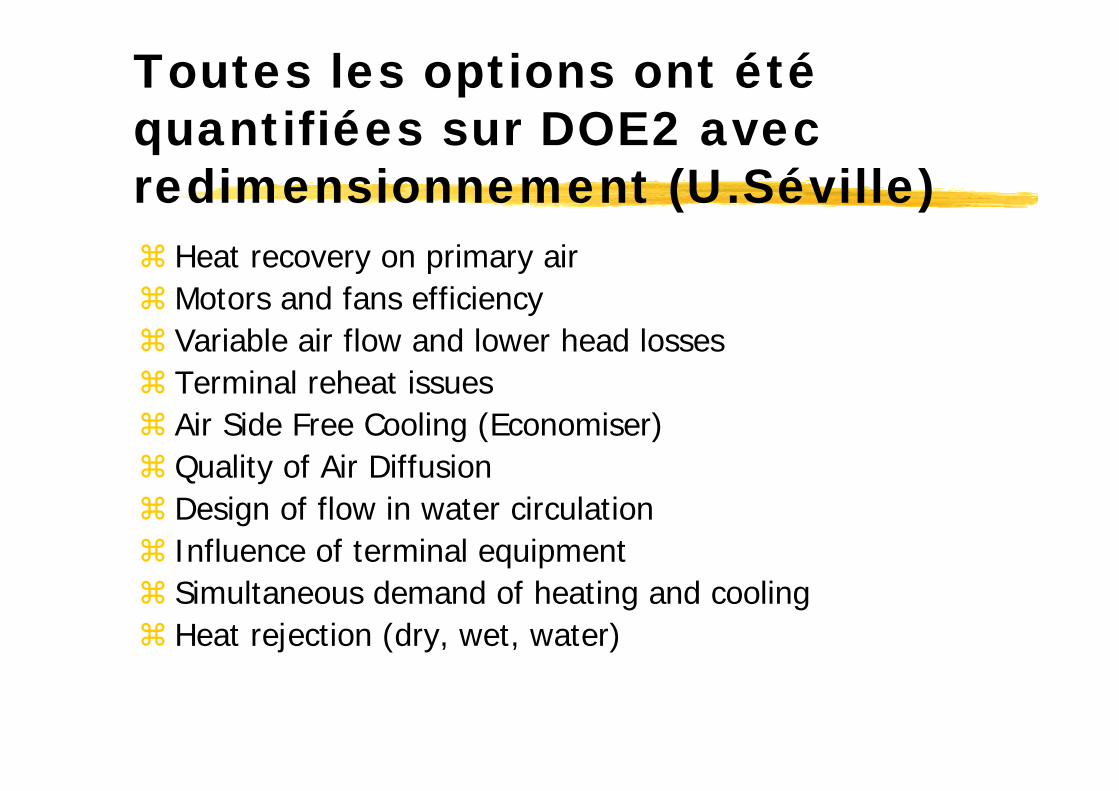

Toutes les options ont étéquantifiées sur DOE2 avec redimensionnement (U.Séville)

Heat recovery on primary airMotors and fans efficiencyVariable air flow and lower head lossesTerminal reheat issuesAir Side Free Cooling (Economiser)Quality of Air DiffusionDesign of flow in water circulationInfluence of terminal equipmentSimultaneous demand of heating and coolingHeat rejection (dry, wet, water)

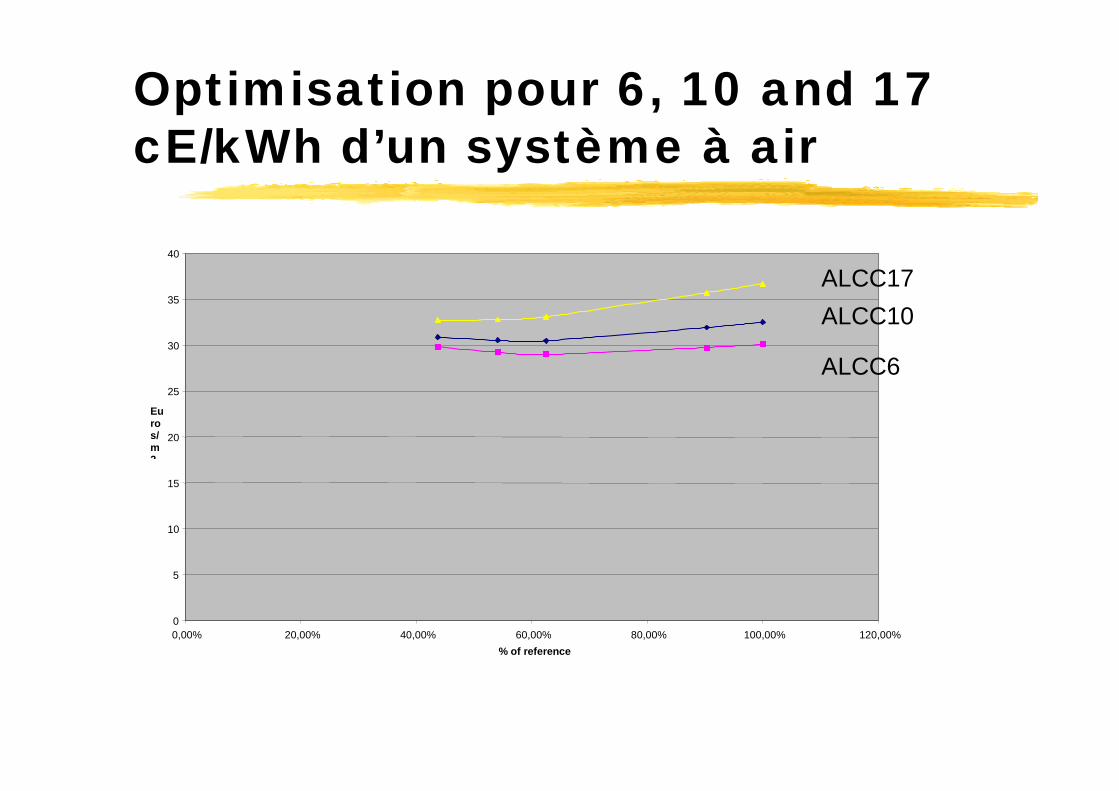

Optimisation pour 6, 10 and 17 cE/kWh d’un système à air

0

5

10

15

20

25

30

35

40

0,00% 20,00% 40,00% 60,00% 80,00% 100,00% 120,00%% of reference

Euros/m2

ALCC17ALCC10

ALCC6

La directive PEB : un premier pas

Building codes are the primary policy measure available to encourage the adoption of more efficient system types. Energy Performance in Buildings Directive is an opportunityIn the case of the UK this Directive may simply require minor revisions of the existing regulations for building cooling energy performance The requirement that a simple calculation method should be constructed against which the compliance of the MEPS is to be judged may also require modification of the Portuguese regulations. Ultimately such a code could be the EU equivalent to the US ASHRAE 90.1 standard, which is none-binding in itself but can be bought either wholly or in-part into national regulations

Une possibilité d’effort volontaire :labelling des projets de A à G

The difficulty in obtaining the best grades (closer to A) should be increasing and involve not only the manufacturer but also other elements of the chain. Moving from G to F or E might be based only on full-load ratings i.e. readily available EER values. Following these measures the importance of system design cannot be neglected. A designer could refer to a design procedure proving he has considered all cost effective options of the project. and reached a certain performance level like C (- 25 %) or B(-50 %) or even A (-75%) compared with the average European performance level, just as is currently the case in the US Energy Star for buildings scheme.

Problèmes induits sur le réseau électrique,

principalement à venir

On s’intéresse à l’efficacité économique : comment être sûr que celui qui entraîne des

dépenses les paye (internalisation)

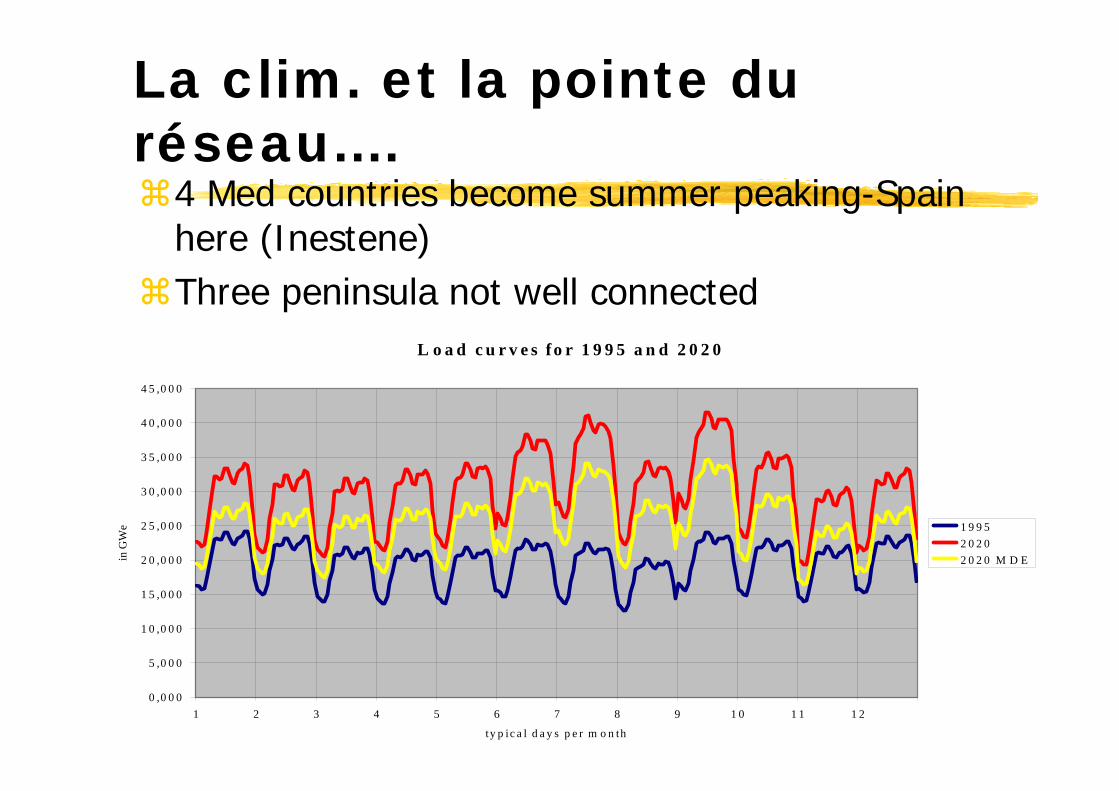

La clim. et la pointe du réseau….

4 Med countries become summer peaking-Spain here (Inestene)Three peninsula not well connected

L o a d c u r v e s fo r 1 9 9 5 a n d 2 0 2 0

0 ,0 0 0

5 ,0 0 0

1 0 ,0 0 0

1 5 ,0 0 0

2 0 ,0 0 0

2 5 ,0 0 0

3 0 ,0 0 0

3 5 ,0 0 0

4 0 ,0 0 0

4 5 ,0 0 0

1 2 3 4 5 6 7 8 9 1 0 1 1 1 2

ty p ic a l d a y s p e r m o n th

in G

We 1 9 9 5

2 0 2 02 0 2 0 M D E

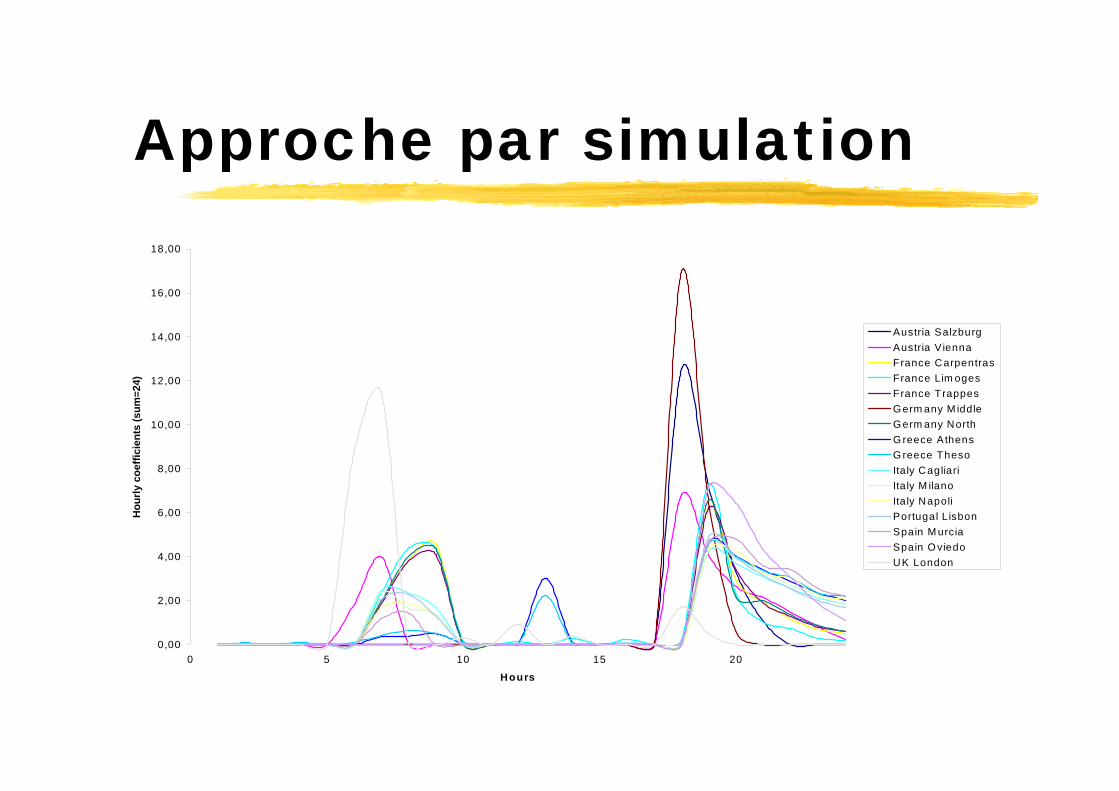

Approche par simulation

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

16,00

18,00

0 5 10 15 20

Hours

Hou

rly c

oeffi

cien

ts (s

um=2

4)

Austria SalzburgAustria V iennaFrance CarpentrasFrance Lim ogesFrance T rappesG erm any M iddleG erm any NorthG reece AthensG reece ThesoItaly CagliariIta ly M ilanoItaly NapoliPortugal L isbonSpain M urciaSpain O viedoUK London

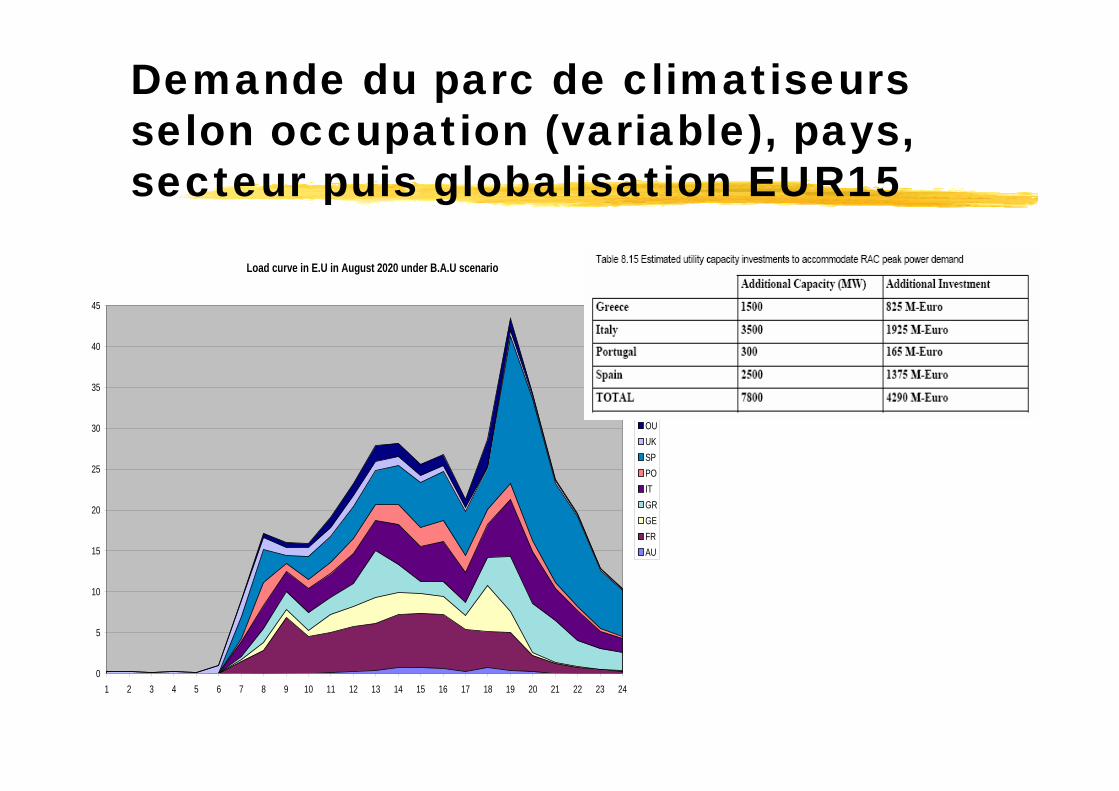

Demande du parc de climatiseurs selon occupation (variable), pays, secteur puis globalisation EUR15

Load curve in E.U in August 2020 under B.A.U scenario

0

5

10

15

20

25

30

35

40

45

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

OUUKSPPOITGRGEFRAU

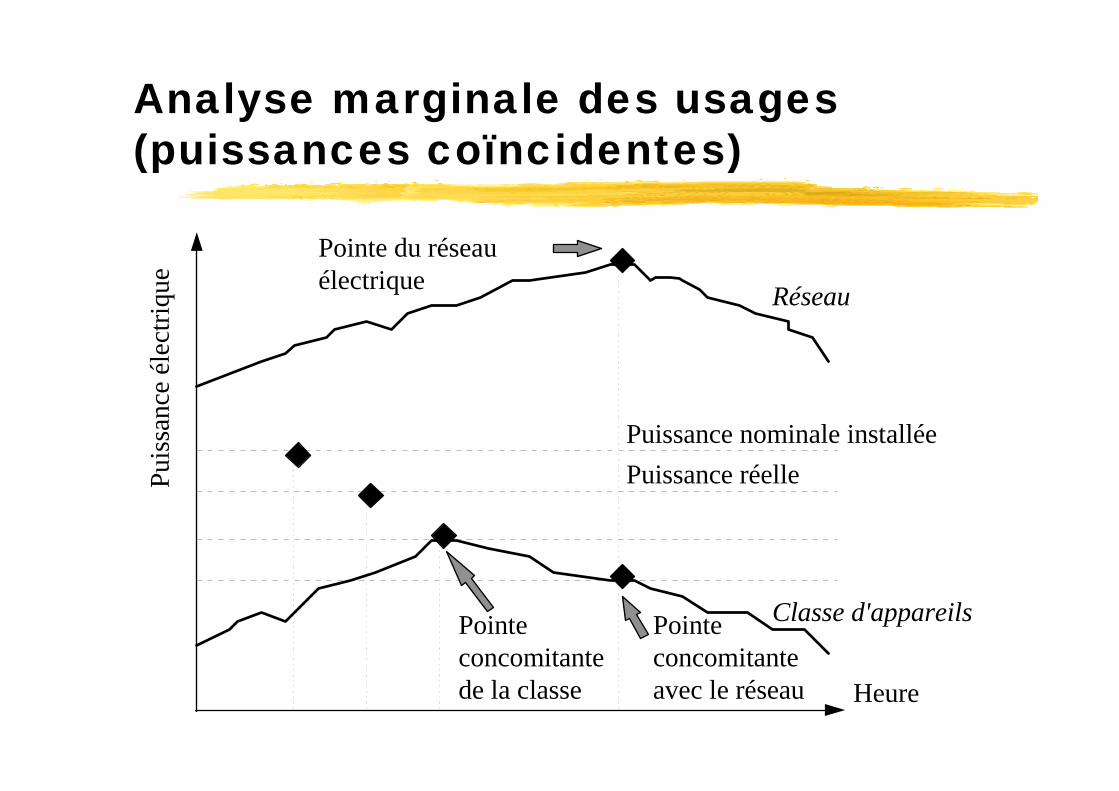

Analyse marginale des usages (puissances coïncidentes)

Heure

Puis

sanc

e él

ectri

que

Pointeconcomitantede la classe

Pointe du réseau électrique Réseau

Puissance nominale installée

Classe d'appareils

Puissance réelle

Pointeconcomitanteavec le réseau

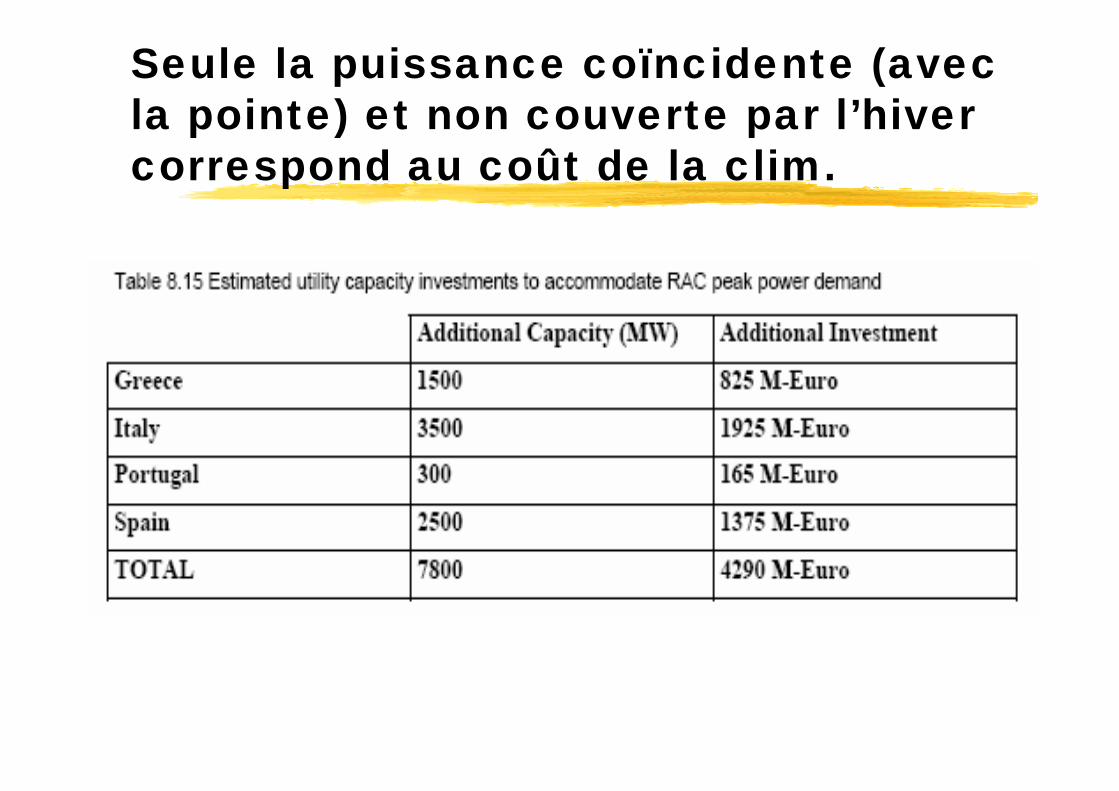

Seule la puissance coïncidente (avec la pointe) et non couverte par l’hiver correspond au coût de la clim.

La nouvelle ligne France Espagne?

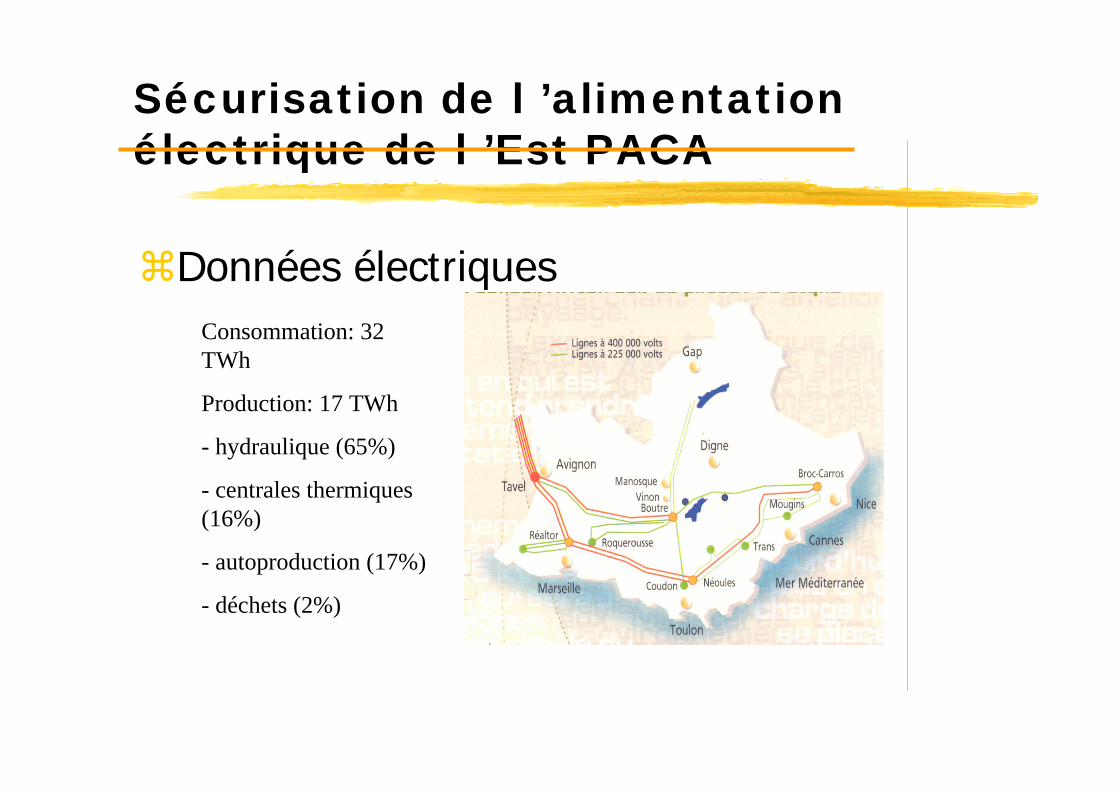

Sécurisation de l ’alimentation électrique de l ’Est PACA

Données électriquesConsommation: 32 TWh

Production: 17 TWh

- hydraulique (65%)

- centrales thermiques (16%)

- autoproduction (17%)

- déchets (2%)

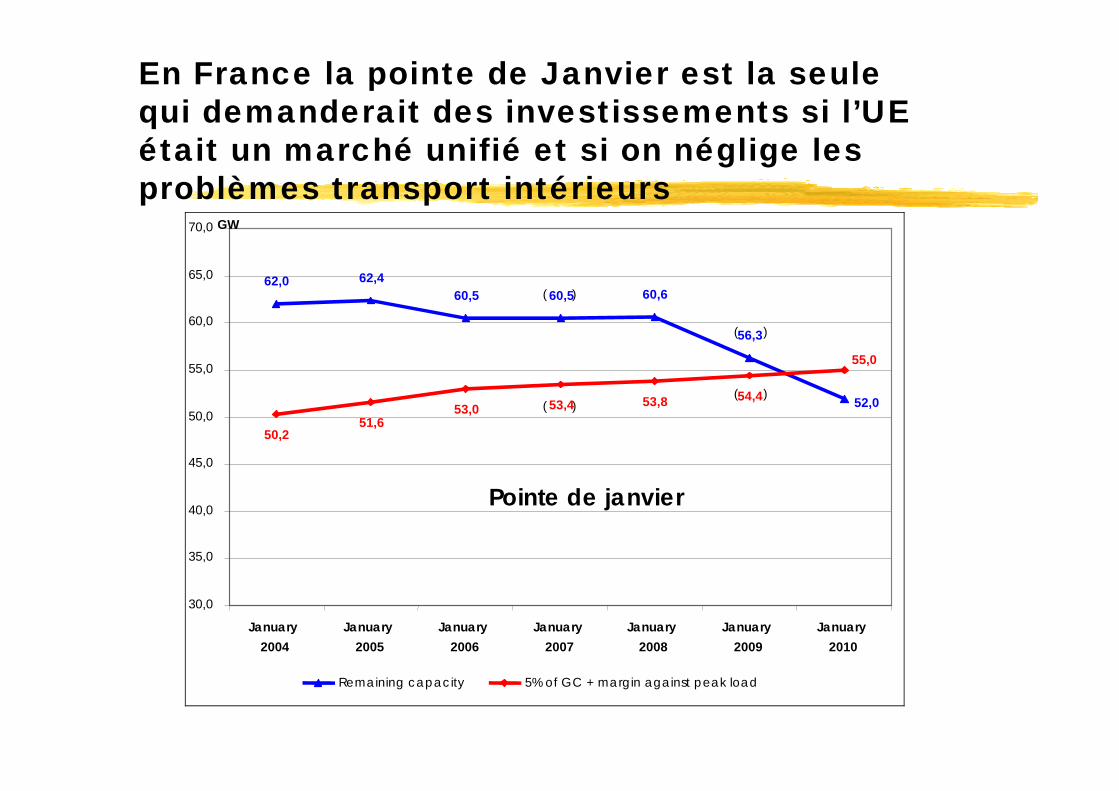

En France la pointe de Janvier est la seule qui demanderait des investissements si l’UE était un marché unifié et si on néglige les problèmes transport intérieurs

62,460,5 60,5 60,6

56,3

51,653,0 53,4 53,8 54,4 52,0

62,0

55,0

50,2

30,0

35,0

40,0

45,0

50,0

55,0

60,0

65,0

70,0

January2004

January2005

January2006

January2007

January2008

January2009

January2010

GW

Remaining capacity 5% of GC + margin against peak load

Pointe de janvier

( )

( )

( )( )

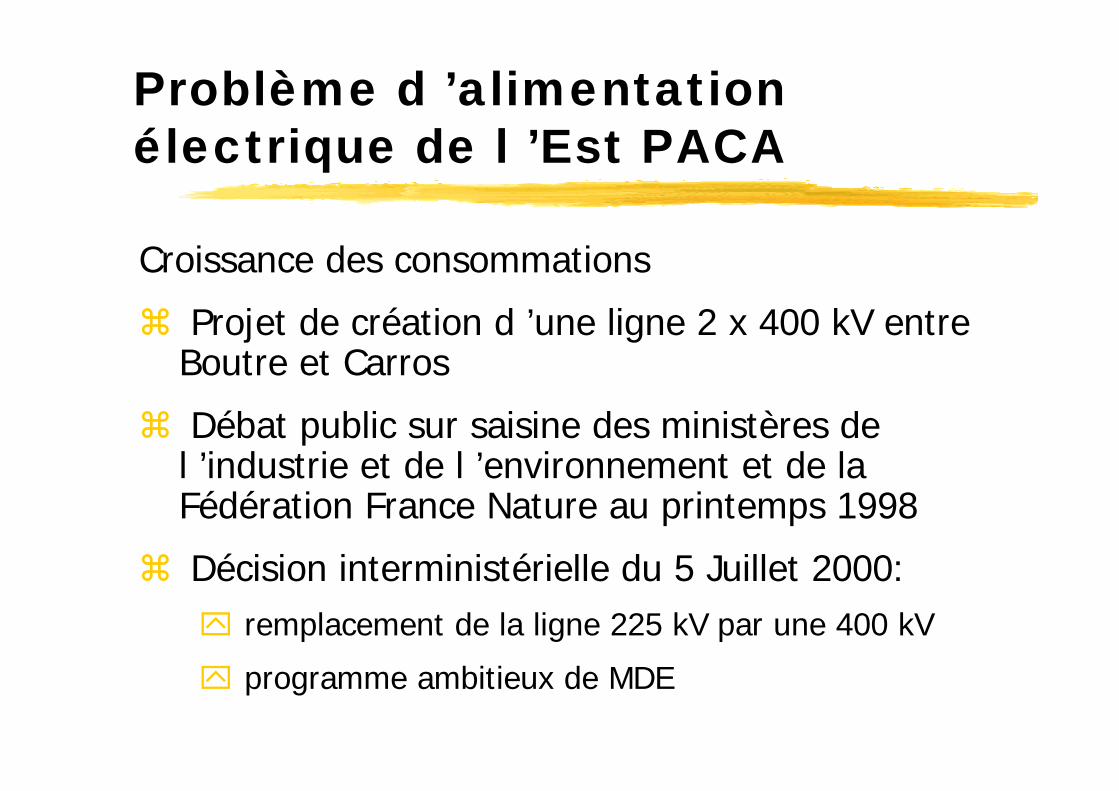

Problème d ’alimentation électrique de l ’Est PACA

Croissance des consommations

Projet de création d ’une ligne 2 x 400 kV entre Boutre et Carros

Débat public sur saisine des ministères de l ’industrie et de l ’environnement et de la Fédération France Nature au printemps 1998

Décision interministérielle du 5 Juillet 2000:remplacement de la ligne 225 kV par une 400 kV

programme ambitieux de MDE

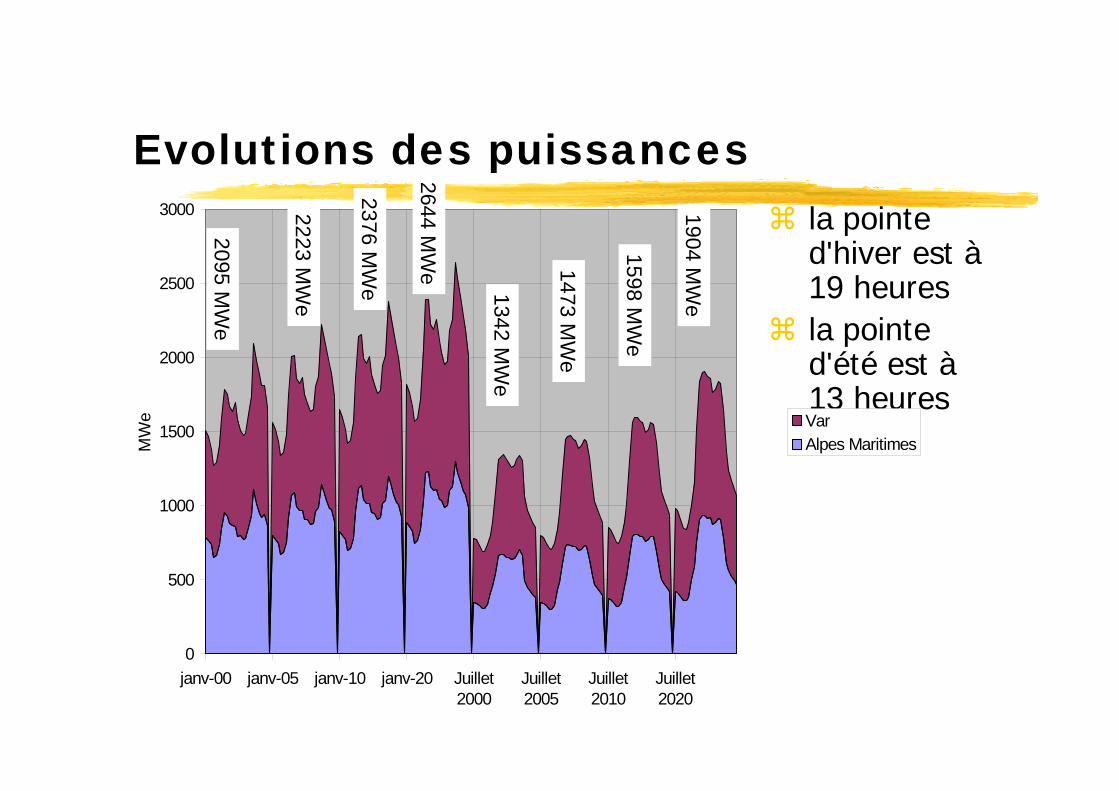

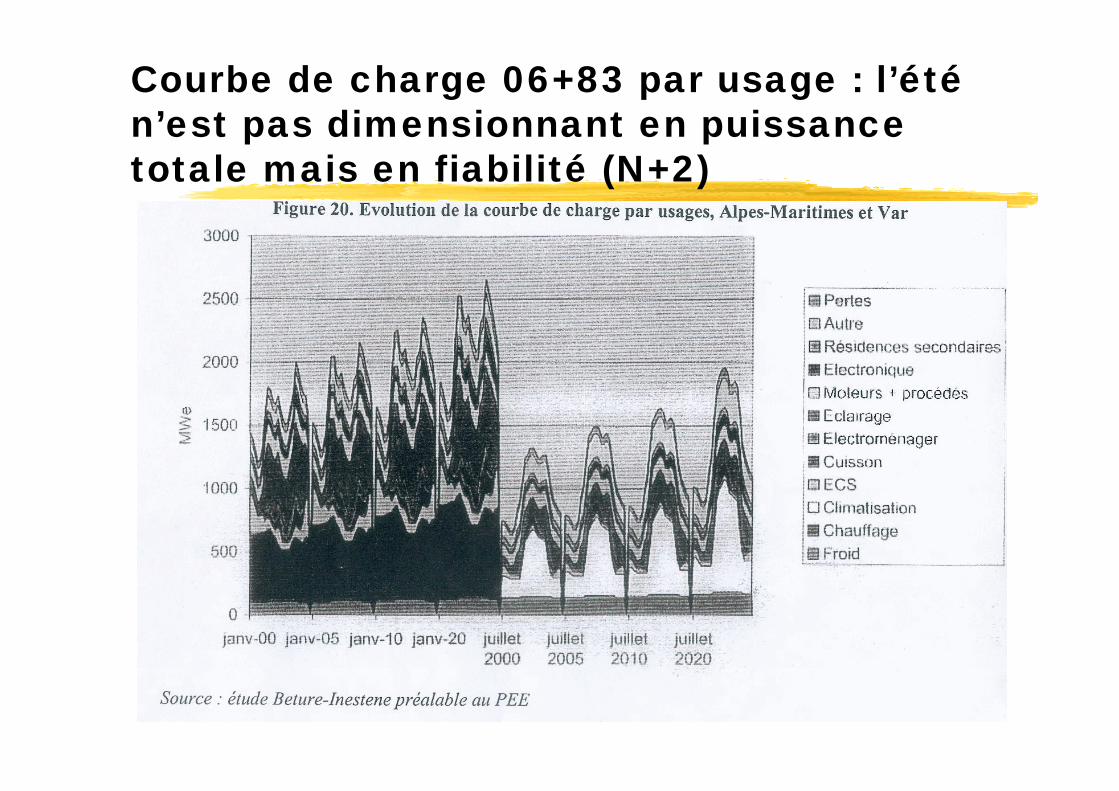

Evolutions des puissancesla pointe d'hiver est à19 heuresla pointe d'été est à13 heures

0

500

1000

1500

2000

2500

3000

janv-00 janv-05 janv-10 janv-20 Juillet2000

Juillet2005

Juillet2010

Juillet2020

MW

e VarAlpes Maritimes

2095M

We

2223M

We

2376M

We

2644M

We

1342M

We

1473M

We

1598M

We

1904M

We

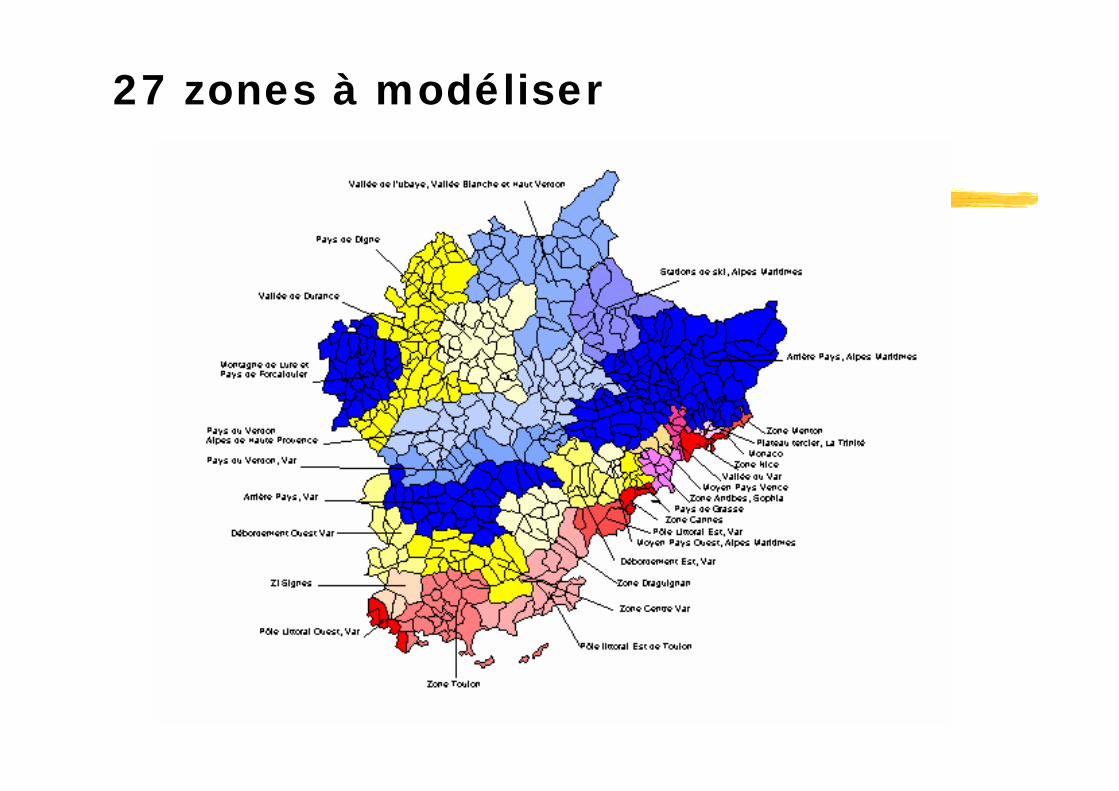

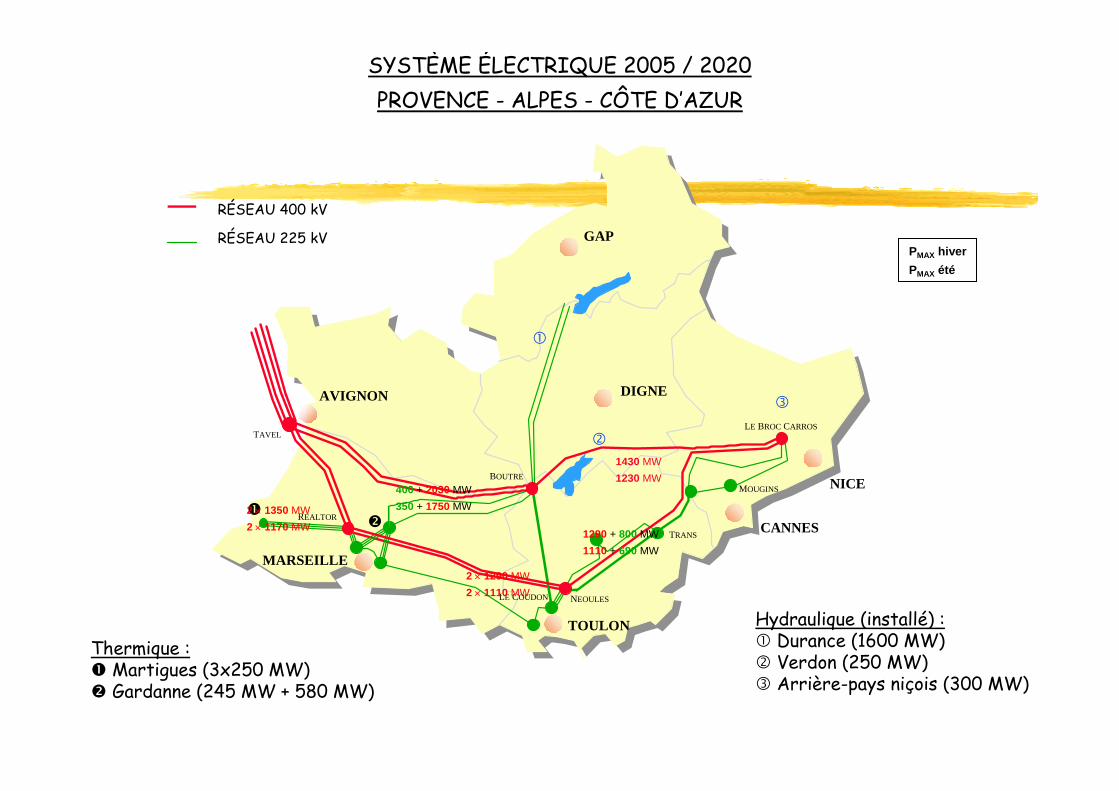

27 zones à modéliser

AVIGNON

TOULON

DIGNE

NICE

GAP

MARSEILLE

CANNES

TAVEL

REALTOR

NEOULES

TRANS

MOUGINS

LE BROC CARROS

BOUTRE

RÉSEAU 400 kV

RÉSEAU 225 kV

LE COUDON

PRÉVISIONS DE CONSOMMATION2005 / 2010 / 2020

2000 1 222 MW 835 MW2005 1 310 MW + 1,4 %/an 903 MW + 1,6 %/an2010 1 373 MW + 0,9 %/an 976 MW + 1,6 %/an2020 1 519 MW + 1,0 %/an 1 156 MW + 1,7 %/an

Hiver Eté

Alp

es-M

.

2000 929 MW 643 MW2005 998 MW + 1,5 %/an 695 MW + 1,6 %/an2010 1 060 MW + 1,2 %/an 757 MW + 1,7 %/an2020 1 189 MW + 1,2 %/an 907 MW + 1,8 %/an

Hiver EtéV

ar

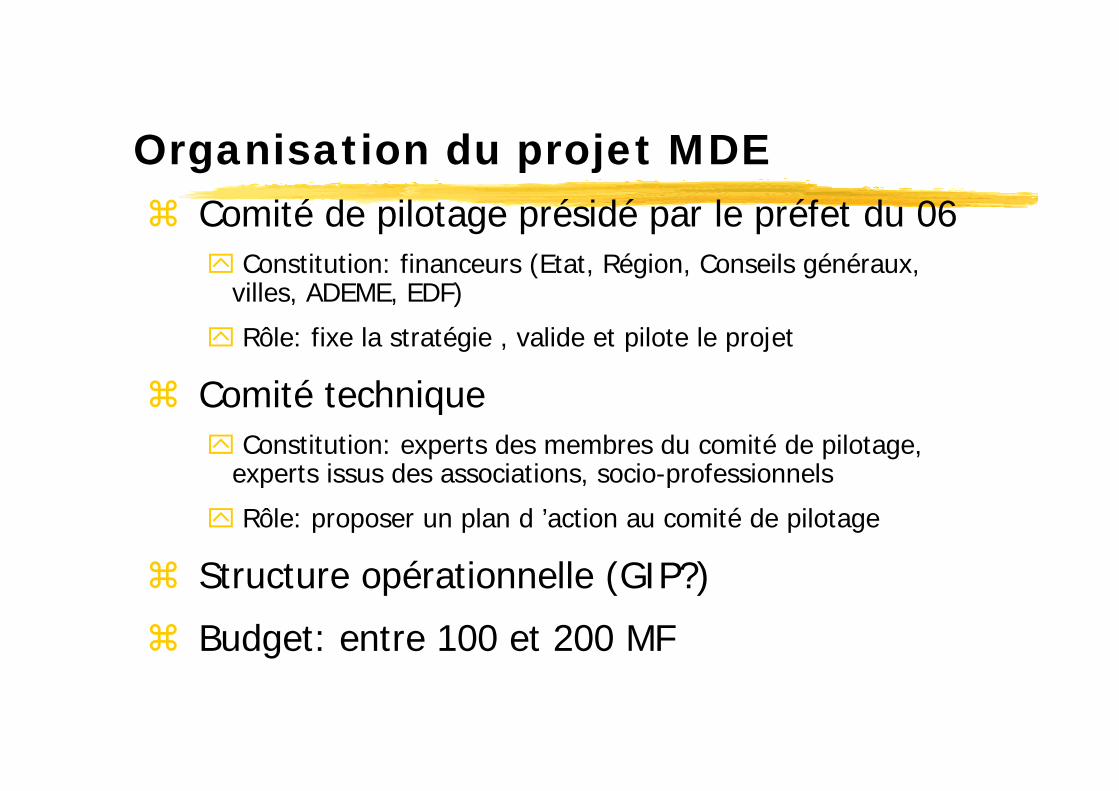

Organisation du projet MDEComité de pilotage présidé par le préfet du 06

Constitution: financeurs (Etat, Région, Conseils généraux, villes, ADEME, EDF)

Rôle: fixe la stratégie , valide et pilote le projet

Comité techniqueConstitution: experts des membres du comité de pilotage,

experts issus des associations, socio-professionnels

Rôle: proposer un plan d ’action au comité de pilotage

Structure opérationnelle (GIP?)

Budget: entre 100 et 200 MF

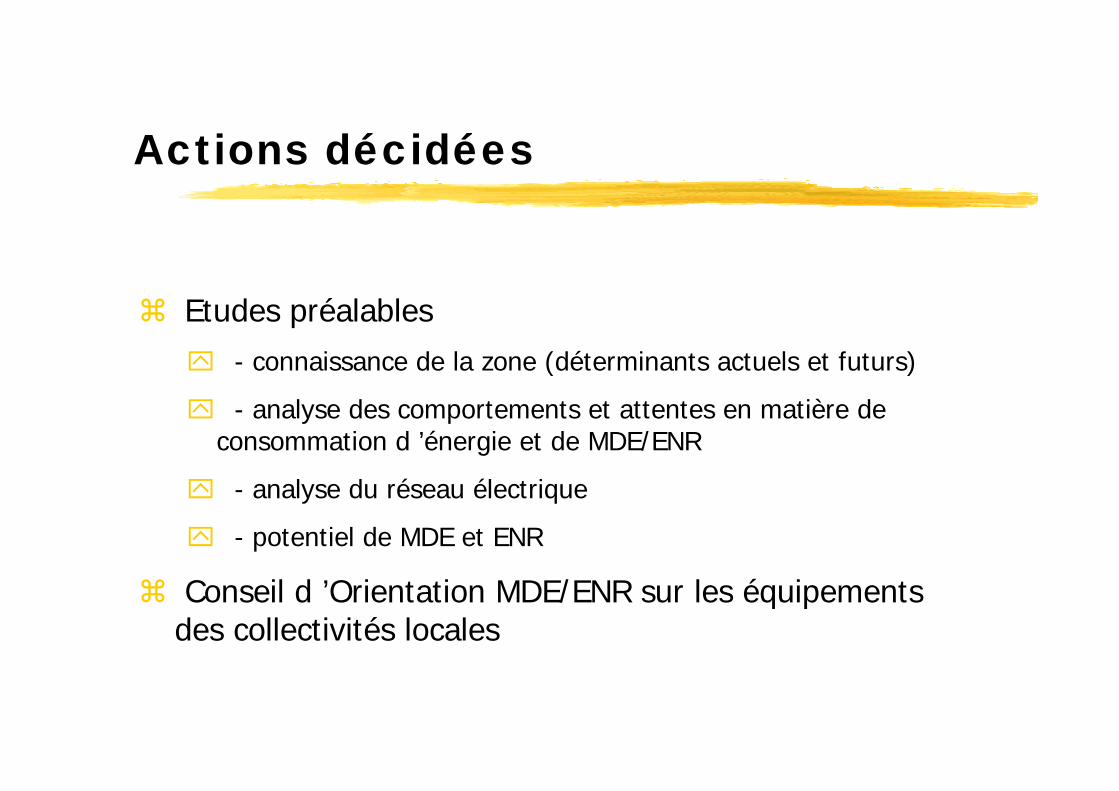

Actions décidées

Etudes préalables- connaissance de la zone (déterminants actuels et futurs)

- analyse des comportements et attentes en matière de consommation d ’énergie et de MDE/ENR

- analyse du réseau électrique

- potentiel de MDE et ENR

Conseil d ’Orientation MDE/ENR sur les équipements des collectivités locales

Courbe de charge 06+83 par usage : l’étén’est pas dimensionnant en puissance totale mais en fiabilité (N+2)

Structure des puissances de pointe en 2000

Pointe hiver Pointe été

Froid6%

Chauffage26%

ECS4%

Cuisson6%

Electroménager7%

Eclairage31%

Moteurs + procédés7%

Electronique5%

Résidences secondaires

1%

Autre3%

Pertes4%

Froid12%

Climatisation40%

Moteurs + procédés10%

Electronique3%

Résidences secondaires

1%Autre10%

Pertes4%

ECS1%

Cuisson4%

Electroménager1%

Eclairage14%

AVIGNON

TOULON

DIGNE

NICE

GAP

MARSEILLE

CANNES

TAVEL

REALTOR

NEOULES

TRANS

MOUGINS

LE BROC CARROS

BOUTRE

RÉSEAU 400 kV

RÉSEAU 225 kV

LE COUDON

SYSTÈME ÉLECTRIQUE 2005 / 2020PROVENCE - ALPES - CÔTE D’AZUR

2 × 1350 MW2 × 1170 MW

2 × 1290 MW2 × 1110 MW

400 + 2030 MW350 + 1750 MW

1290 + 800 MW1110 + 690 MW

1430 MW1230 MW

PMAX hiverPMAX été

Thermique : Martigues (3x250 MW) Gardanne (245 MW + 580 MW)

Hydraulique (installé) : Durance (1600 MW) Verdon (250 MW) Arrière-pays niçois (300 MW)

AVIGNON

TOULON

DIGNE

NICE

GAP

MARSEILLE

CANNES

TAVEL

REALTOR

NEOULES

TRANS

MOUGINS

LE BROC CARROS

BOUTRE

RÉSEAU 400 kV

RÉSEAU 225 kV

LE COUDON

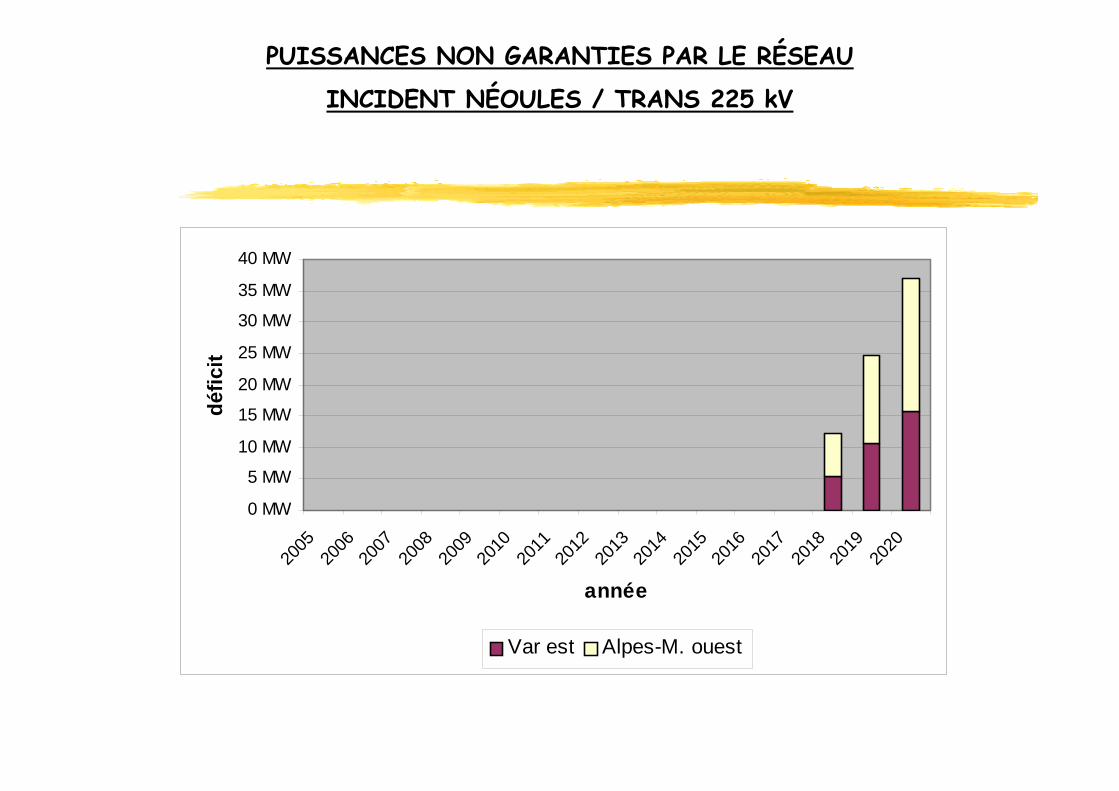

CONTRAINTE À LA POINTE HIVERINCIDENT NÉOULES / TRANS 225 kV

Risque :- probabilité : 1 tous les 2 ans- durée : 1 à 2 jours- risque 2020 : 2250 h (25 %)

Surcharge

Perte momentanPerte momentanéée e àà partir de 2018partir de 2018

PUISSANCES NON GARANTIES PAR LE RÉSEAU

INCIDENT NÉOULES / TRANS 225 kV

0 MW

5 MW

10 MW

15 MW

20 MW

25 MW

30 MW

35 MW

40 MW

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

année

défic

it

Var est Alpes-M. ouest

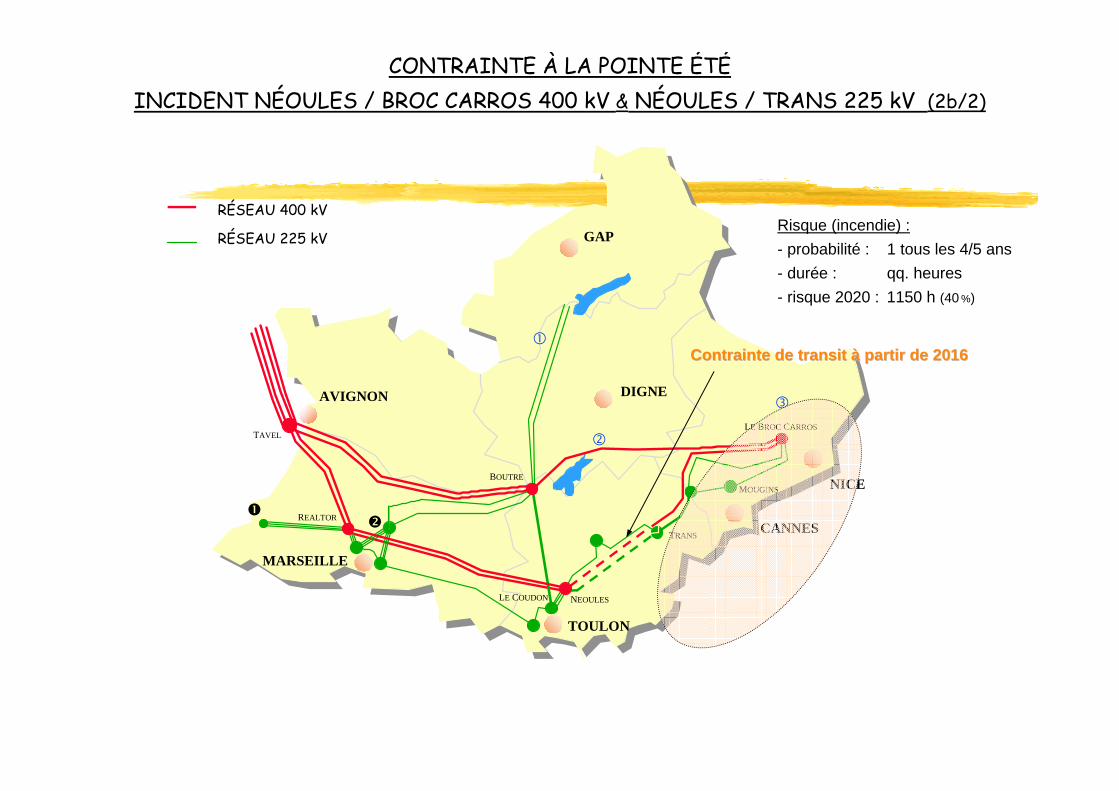

Risque (incendie) :- probabilité : 1 tous les 4/5 ans- durée : qq. heures- risque 2020 : 1150 h (40 %)

AVIGNON

TOULON

DIGNE

NICE

GAP

MARSEILLE

CANNES

TAVEL

REALTOR

NEOULES

TRANS

MOUGINS

LE BROC CARROS

BOUTRE

RÉSEAU 400 kV

RÉSEAU 225 kV

LE COUDON

CONTRAINTE À LA POINTE ÉTÉINCIDENT NÉOULES / BROC CARROS 400 kV & NÉOULES / TRANS 225 kV (2b/2)

Contrainte de transit Contrainte de transit àà partir de 2016partir de 2016

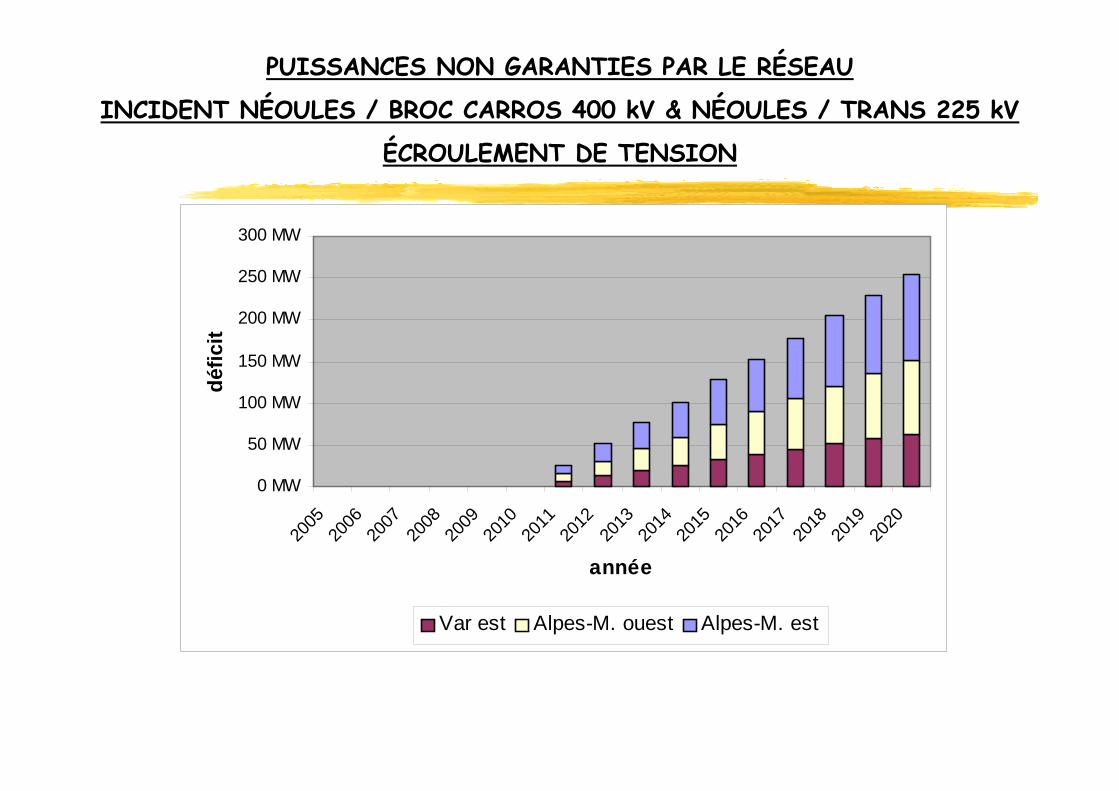

PUISSANCES NON GARANTIES PAR LE RÉSEAU

INCIDENT NÉOULES / BROC CARROS 400 kV & NÉOULES / TRANS 225 kV

ÉCROULEMENT DE TENSION

0 MW

50 MW

100 MW

150 MW

200 MW

250 MW

300 MW

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

année

défic

it

Var est Alpes-M. ouest Alpes-M. est

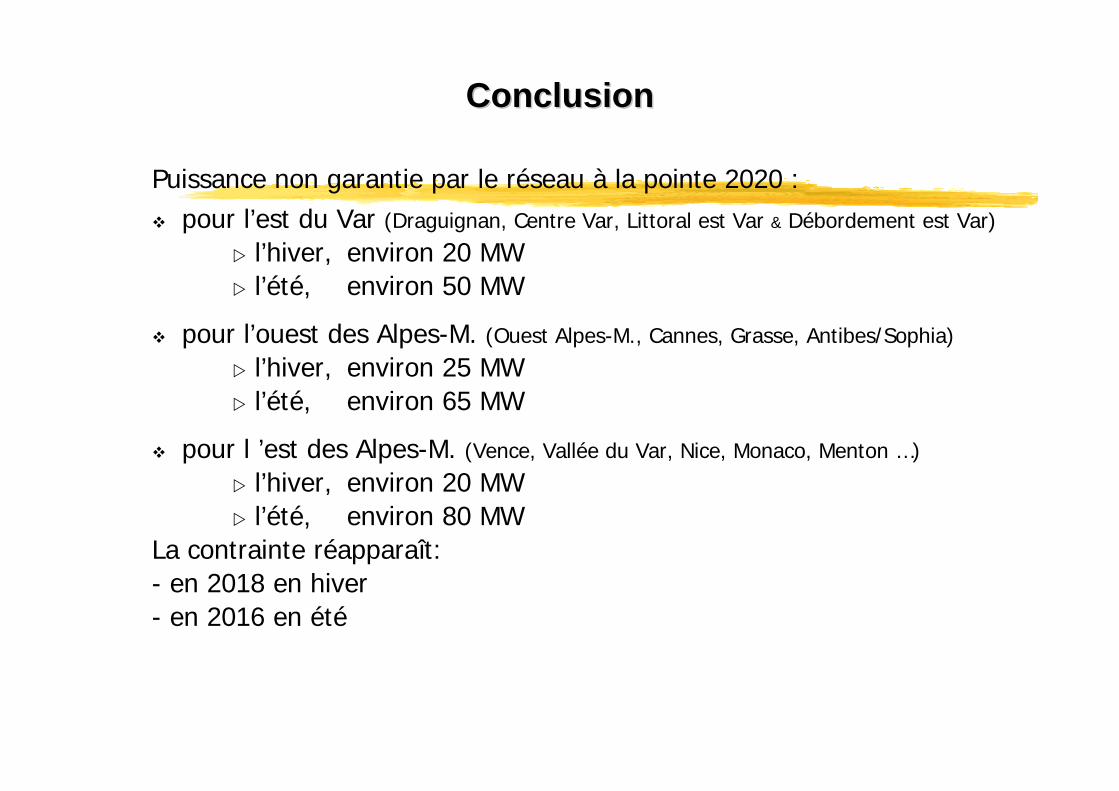

ConclusionConclusion

Puissance non garantie par le réseau à la pointe 2020 :pour l’est du Var (Draguignan, Centre Var, Littoral est Var & Débordement est Var)

l’hiver, environ 20 MWl’été, environ 50 MW

pour l’ouest des Alpes-M. (Ouest Alpes-M., Cannes, Grasse, Antibes/Sophia)

l’hiver, environ 25 MWl’été, environ 65 MW

pour l ’est des Alpes-M. (Vence, Vallée du Var, Nice, Monaco, Menton …)

l’hiver, environ 20 MWl’été, environ 80 MW

La contrainte réapparaît:- en 2018 en hiver- en 2016 en été

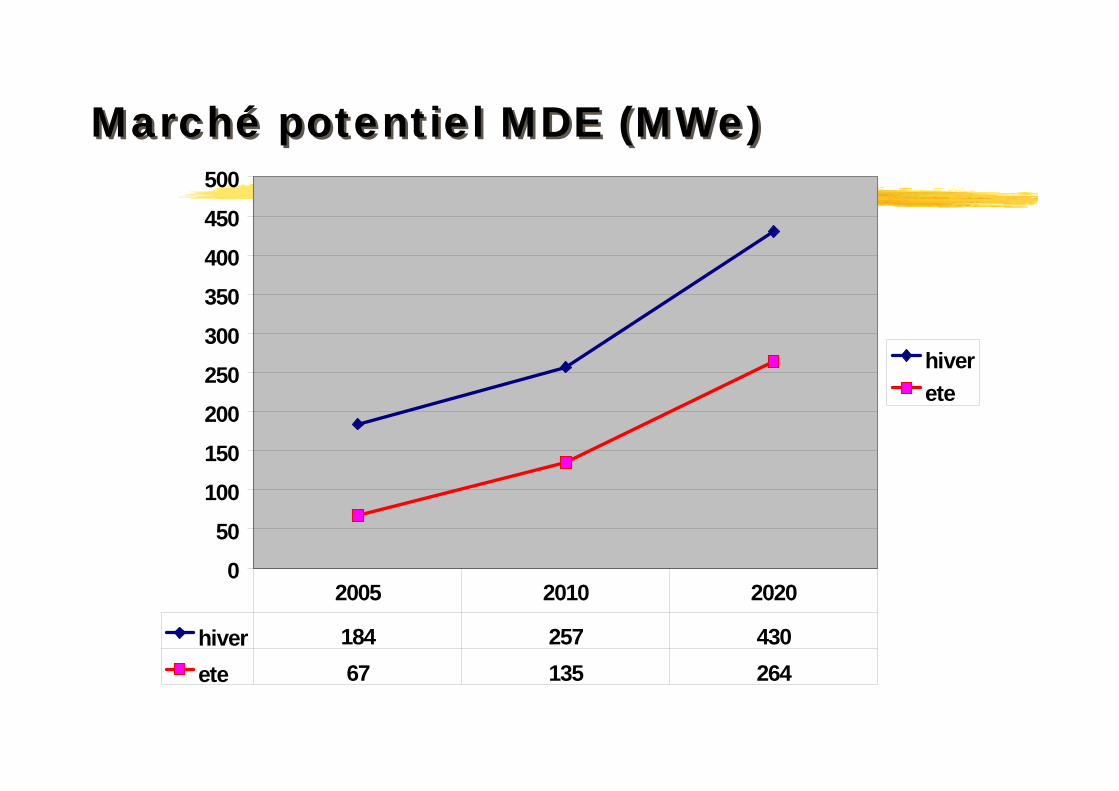

Marché potentiel MDE (MWe)Marché potentiel MDE (MWe)

0

50

100

150

200

250

300

350

400

450

500

hiverete

hiver 184 257 430ete 67 135 264

2005 2010 2020

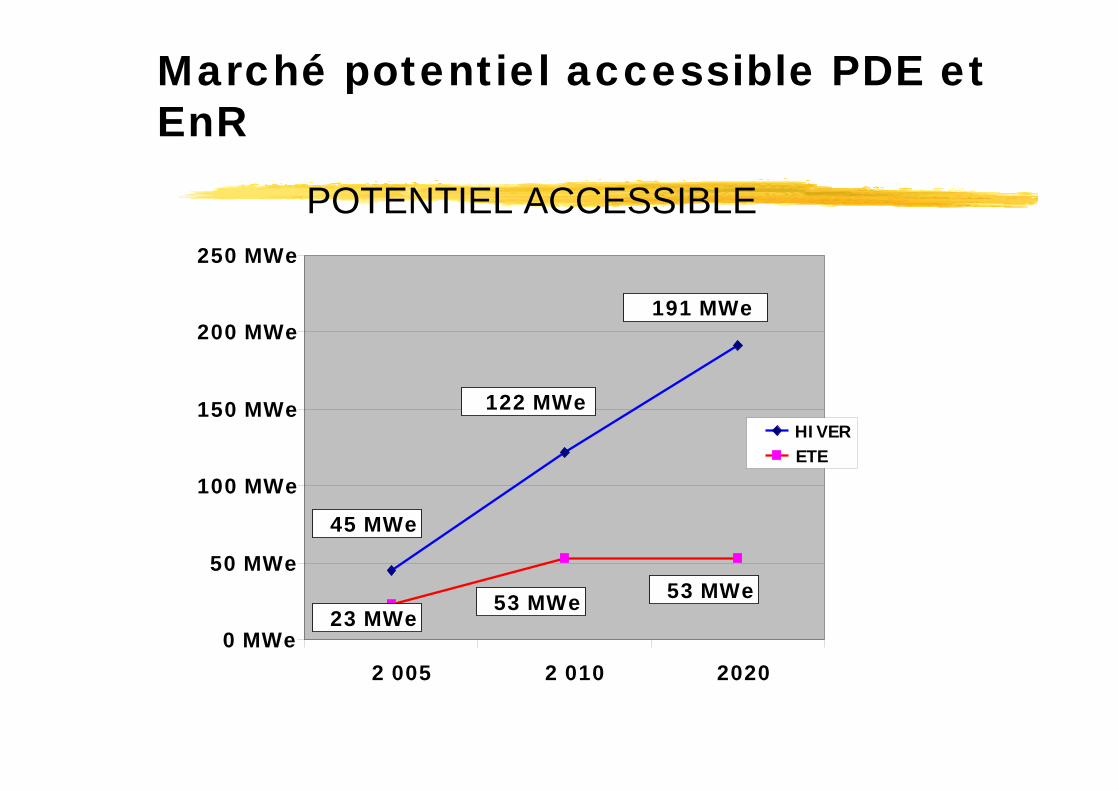

Marché potentiel accessible PDE et EnR

POTENTIEL ACCESSIBLE

0 MWe

50 MWe

100 MWe

150 MWe

200 MWe

250 MWe

2 005 2 010 2020

HIVERETE

23 MWe53 MWe 53 MWe

191 MWe

122 MWe

45 MWe

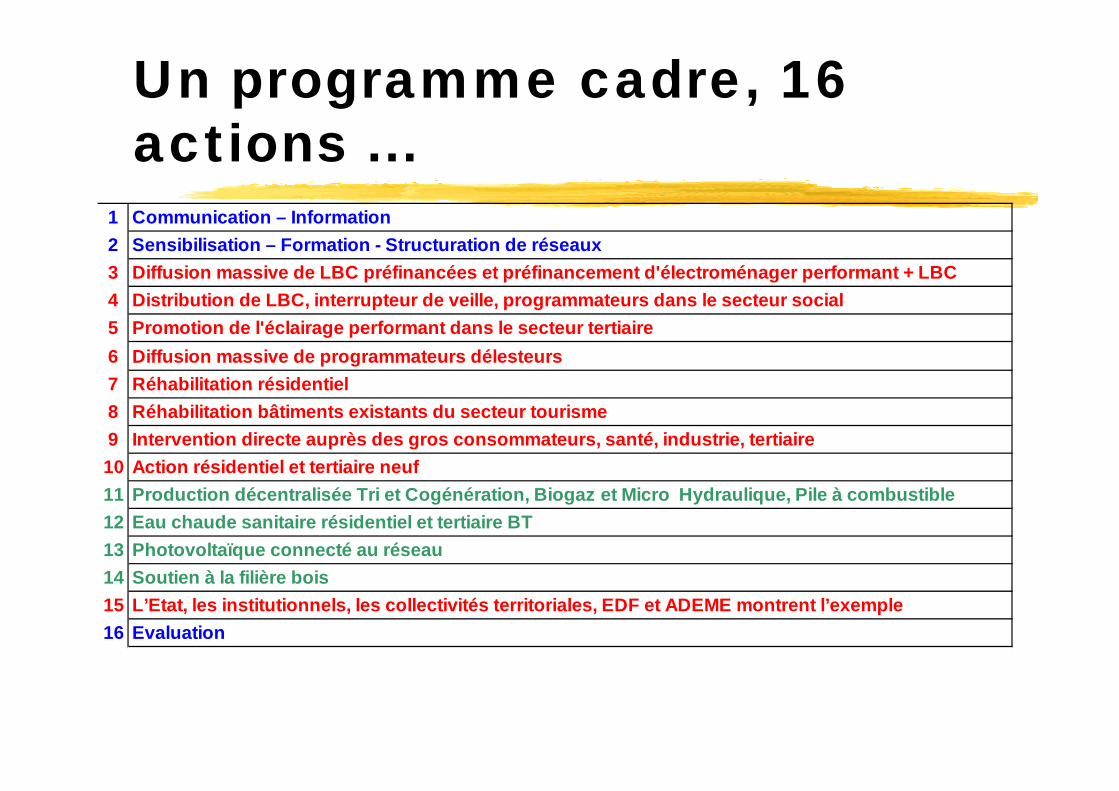

Un programme cadre, 16 actions ...

1 Communication – Information 2 Sensibilisation – Formation - Structuration de réseaux3 Diffusion massive de LBC préfinancées et préfinancement d'électroménager performant + LBC4 Distribution de LBC, interrupteur de veille, programmateurs dans le secteur social5 Promotion de l'éclairage performant dans le secteur tertiaire6 Diffusion massive de programmateurs délesteurs7 Réhabilitation résidentiel8 Réhabilitation bâtiments existants du secteur tourisme9 Intervention directe auprès des gros consommateurs, santé, industrie, tertiaire10 Action résidentiel et tertiaire neuf11 Production décentralisée Tri et Cogénération, Biogaz et Micro Hydraulique, Pile à combustible12 Eau chaude sanitaire résidentiel et tertiaire BT13 Photovoltaïque connecté au réseau14 Soutien à la filière bois15 L’Etat, les institutionnels, les collectivités territoriales, EDF et ADEME montrent l’exemple16 Evaluation

Jérôme Adnot, Matthieu Orphelin et Philippe Rivière, Ecole des Mines, à parir des résultats de divers groupes de travail

" Développement de la climatisationen Europe et impacts sur le réseau

électrique”

Quelques questions :Suivi et évaluation des actions de MDE?

Audit des installations de climatisation existante?Interaction Clim. / Marché libre Electrique ?

La directive PEB va-t-elle réaliser une partie des actions possibles?

Les raisons du choix clim/non clim et la continuitéréglementaire sur la frontière?