banque commerciale du rwanda (b.c.r.)

TRANSCRIPT

Deloitte & Touche Rwanda Boulevard de l’Umuganda Immeuble Aurore - Kacyiru B.P. 1902 Kigali Rwanda Tel : +250 0830 0832 Tel : +250 58 79 33 Fax: +250 58 79 34 E-mail: [email protected] http://www.gpopartenrs.com

BANQUE COMMERCIALE DU RWANDA (B.C.R.)

Auditors Report on Financial Statements

as at 31st December 2007.

Deloitte & Touche Rwanda S.A.R.L. Siège social: Boulevard de l’Umuganda – Immeuble Aurore – Kacyiru – BP 1902 Kigali, Rwanda R.C. 1778 TVA 10016149 Audit.Accounting.Tax.Consulting.Corporate Finance.

2

TABLE OF CONTENTS

PAGE Bank Information 3 Report of Directors 4 Statement of Director’s Responsibilities 5 Report of the Independent Auditors 6

Income Statement 7 Balance Sheet 8 Statement of Changes in Equity 9 Cash Flow Statement 10 Notes to the Financial Statements 11 – 39

3

BANQUE COMMERCIALE DU RWANDA (B.C.R.) BANK INFORMATION PERIOD ENDED 31ST DECEMBER 2007 PRINCIPAL PLACE OF BUSINESS Banque Commerciale du Rwanda 11, Boulevard de la Révolution P.O. BOX 354 Kigali RWANDA REGISTERED OFFICE Banque Commerciale du Rwanda 11, Boulevard de la Révolution P.O. BOX 354 Kigali RWANDA

AUDITORS

Deloitte Rwanda Boulevard de l’Umuganda Immeuble Aurore – Kacyiru P.O. BOX 1902 Kigali Rwanda SHAREHOLDERS OF THE COMPANY The shareholders of BCR are: Name shareholding BCR Investment Company Limited 80.0 % Government of Rwanda 19.8 % Others 0.2 % INCORPORATION

The bank is incorporated and domiciled in Rwanda.

EMPLOYEES The bank employed 290 full time staff and 26 temporary staff as at 31 December 2007. BRANCHES BCR has eight branches, all located in Rwanda:

⋅ Kigali - Head office ⋅ Novotel -Branch ⋅ Butare -Branch ⋅ Gisenyi - Branch ⋅ Cyangugu - Branch ⋅ Byumba - Branch ⋅ Ruhengeri - Branch

In addition to these, BCR has three agencies.

4

BANQUE COMMERCIALE DU RWANDA (B.C.R.) REPORT OF DIRECTORS FOR THE PERIOD ENDED 31ST DECEMBER 2007 The directors present their report together with the audited financial statements for the year ended 31 December 2007. PRINCIPAL ACTIVITIES The principal activity of the bank is the provision of corporate, retail banking and leasing services RESULTS The results for the year are set out on page 7 BOARD OF DIRECTORS AS AT 31 DECEMBER 2007 The directors who served during the year and to the date of this report were: Nkosana Moyo : Chairman Ezra Bunyenyezi : Appointed 2nd December 2004 Paul Kavuma : Appointed 24th May 2006 William Irwin : Appointed 2nd December 2004 David Kuwana : Appointed 1st March 2005 Emmanuel Ntaganda : Appointed 2nd December 2004 Barry D. Northrop : Appointed 31st March 2007 AUDITORS Deloitte Rwanda, having been re-appointed, have expressed their willingness to continue in office in accordance with Laws and regulations of Rwanda.

5

BANQUE COMMERCIALE DU RWANDA (B.C.R) STATEMENT OF DIRECTORS’ RESPONSIBILITIES

ON THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2007 The Rwanda Banking law requires the directors to prepare financial statements for each financial year which give a true and fair view of the state of affairs of the bank as at the end of the financial year and of the operating results of the bank for that year. It also requires the directors to ensure the bank keeps proper accounting records which disclose with reasonable accuracy at any time the financial position of the bank. They are also responsible for safeguarding the assets of the bank. The directors accept responsibility for the annual financial statements, which have been prepared using appropriate accounting policies supported by reasonable and prudent judgments and estimates in conformity with International Financial Reporting Standards and in the manner required by the Rwanda Banking law. The directors are of the opinion that the financial statements give a true and fair view of the state of the financial affairs of the bank and of its operating results. The directors further accept responsibility for the maintenance of accounting records which may be relied upon in the preparation of financial statements, as well as adequate systems of internal financial control. Nothing has come to the attention of the directors to indicate that the bank will not remain a going concern for at least the next twelve months from the date of this statement. ----------------------------------------- ---------------------------------------------- DIRECTOR (Chairman) DIRECTOR

6

REPORT OF THE AUDITORS AS AT 31st DECEMBER 2007

PRESENTED TO THE SHAREHOLDERS OF BANQUE COMMERCIALE DU RWANDA To the shareholders, In accordance with legal and statutory requirements, we are pleased to submit our audit report on the Financial Statements. We have conducted our audit on the financial statements established under the responsibility of the boards of directors, for the period ended 31st December 2007. Our audit has been conducted in accordance with the International Standards on Auditing (ISA). Those standards require that we plan and perform the audit to obtain a reasonable assurance that the financial statements are free of material misstatement in accordance with rules and regulations governing accounts of Commercial banks in Rwanda. We have considered the organisation of the Bank in terms of accounting and administration and its overall internal control system. We have obtained all the information and explanations, which, to the best of our knowledge and belief, were necessary for our audit. We have examined, on a sample basis, evidence supporting the amounts and disclosures in the financial statements in the account as at 31st December 2007. This also includes assessing the accounting principles used and significant estimates made by the directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion. Opinion In our opinion, proper books of accounts have been kept and the financial statements, which are in agreement therewith, give a true and fair view of the state of the financial affairs as at 31st December 2007 and of the profit and cash flows for the year then ended. Without qualifying our opinion, we draw attention to note 32 to the financial statements relating to the ongoing court cases. Kigali, 11th March 2008 For Deloitte Rwanda Patrick GASHAGAZA Partner

7

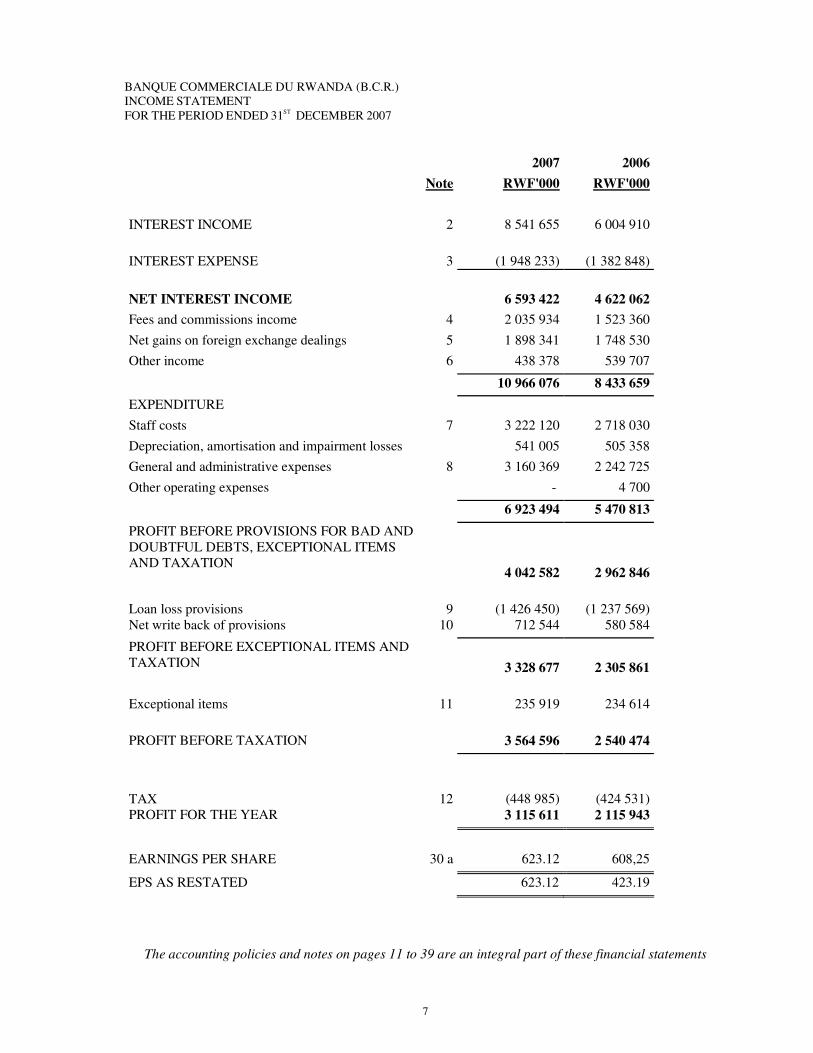

BANQUE COMMERCIALE DU RWANDA (B.C.R.) INCOME STATEMENT FOR THE PERIOD ENDED 31ST DECEMBER 2007 2007 2006 Note RWF'000 RWF'000 INTEREST INCOME 2 8 541 655 6 004 910 INTEREST EXPENSE

3 (1 948 233) (1 382 848)

NET INTEREST INCOME 6 593 422 4 622 062 Fees and commissions income 4 2 035 934 1 523 360 Net gains on foreign exchange dealings 5 1 898 341 1 748 530 Other income 6 438 378 539 707

10 966 076 8 433 659 EXPENDITURE Staff costs 7 3 222 120 2 718 030 Depreciation, amortisation and impairment losses 541 005 505 358 General and administrative expenses 8 3 160 369 2 242 725 Other operating expenses - 4 700

6 923 494 5 470 813

PROFIT BEFORE PROVISIONS FOR BAD AND DOUBTFUL DEBTS, EXCEPTIONAL ITEMS AND TAXATION

4 042 582 2 962 846 Loan loss provisions

9 (1 426 450) (1 237 569)

Net write back of provisions 10 712 544 580 584

PROFIT BEFORE EXCEPTIONAL ITEMS AND TAXATION

3 328 677 2 305 861 Exceptional items

11 235 919 234 614

PROFIT BEFORE TAXATION 3 564 596 2 540 474 TAX

12 (448 985) (424 531)

PROFIT FOR THE YEAR 3 115 611 2 115 943

EARNINGS PER SHARE 30 a 623.12 608,25

EPS AS RESTATED 623.12 423.19

The accounting policies and notes on pages 11 to 39 are an integral part of these financial statements

8

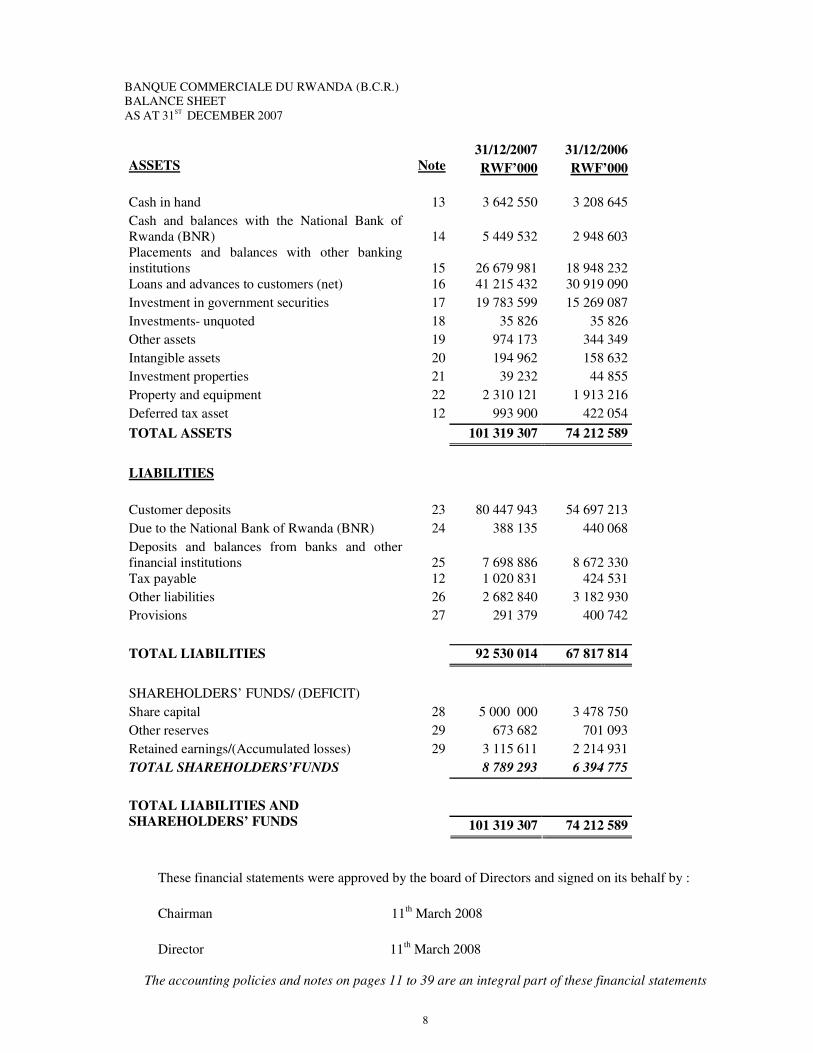

BANQUE COMMERCIALE DU RWANDA (B.C.R.) BALANCE SHEET AS AT 31ST DECEMBER 2007 31/12/2007 31/12/2006 ASSETS Note RWF’000 RWF’000 Cash in hand 13 3 642 550 3 208 645 Cash and balances with the National Bank of Rwanda (BNR)

14

5 449 532

2 948 603

Placements and balances with other banking institutions

15

26 679 981

18 948 232

Loans and advances to customers (net) 16 41 215 432 30 919 090 Investment in government securities 17 19 783 599 15 269 087 Investments- unquoted 18 35 826 35 826 Other assets 19 974 173 344 349 Intangible assets 20 194 962 158 632 Investment properties 21 39 232 44 855 Property and equipment 22 2 310 121 1 913 216 Deferred tax asset 12 993 900 422 054 TOTAL ASSETS 101 319 307 74 212 589 LIABILITIES Customer deposits 23 80 447 943 54 697 213 Due to the National Bank of Rwanda (BNR) 24 388 135 440 068 Deposits and balances from banks and other financial institutions

25

7 698 886

8 672 330

Tax payable 12 1 020 831 424 531 Other liabilities 26 2 682 840 3 182 930 Provisions 27 291 379 400 742 TOTAL LIABILITIES 92 530 014 67 817 814 SHAREHOLDERS’ FUNDS/ (DEFICIT) Share capital 28 5 000 000 3 478 750 Other reserves 29 673 682 701 093 Retained earnings/(Accumulated losses) 29 3 115 611 2 214 931 TOTAL SHAREHOLDERS’FUNDS 8 789 293 6 394 775

TOTAL LIABILITIES AND SHAREHOLDERS’ FUNDS

101 319 307 74 212 589

These financial statements were approved by the board of Directors and signed on its behalf by : Chairman 11th March 2008

Director 11th March 2008

The accounting policies and notes on pages 11 to 39 are an integral part of these financial statements

9

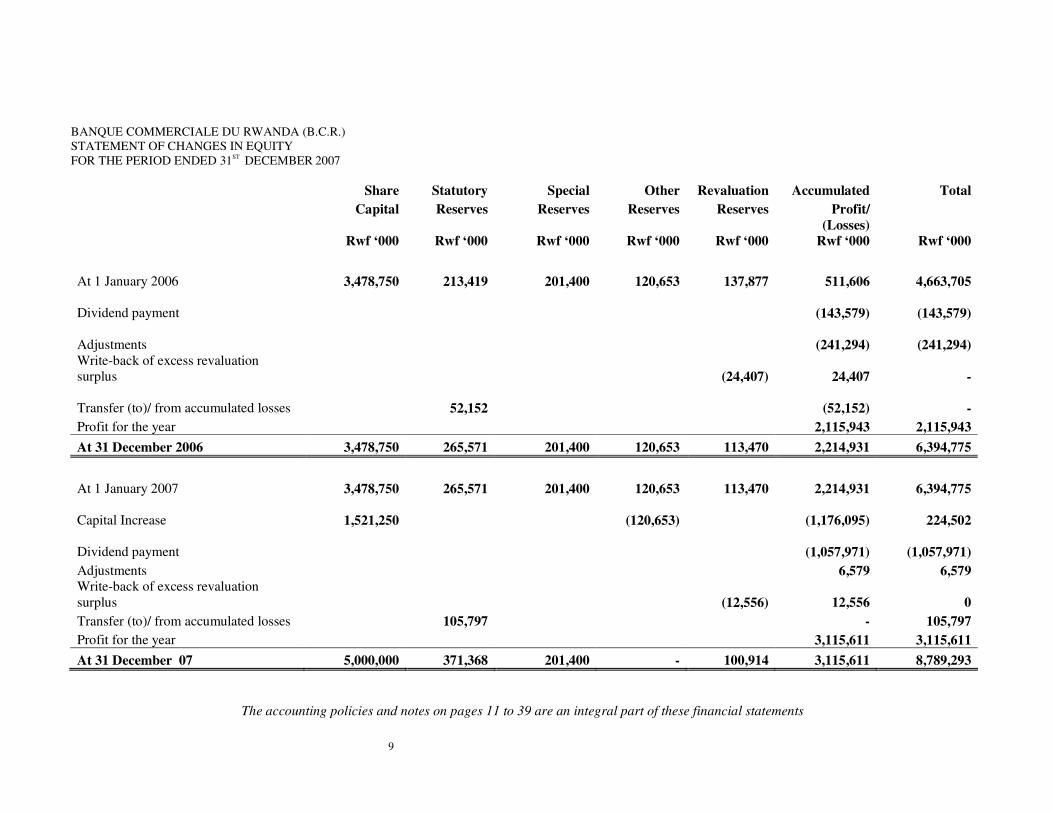

BANQUE COMMERCIALE DU RWANDA (B.C.R.) STATEMENT OF CHANGES IN EQUITY FOR THE PERIOD ENDED 31ST DECEMBER 2007

Share Statutory Special Other Revaluation Accumulated Total

Capital Reserves Reserves Reserves Reserves Profit/

(Losses)

Rwf ‘000 Rwf ‘000 Rwf ‘000 Rwf ‘000 Rwf ‘000 Rwf ‘000 Rwf ‘000 At 1 January 2006 3,478,750 213,419 201,400 120,653 137,877 511,606 4,663,705

Dividend payment

(143,579)

(143,579)

Adjustments

(241,294)

(241,294) Write-back of excess revaluation surplus

(24,407) 24,407 -

Transfer (to)/ from accumulated losses 52,152

(52,152) - Profit for the year 2,115,943 2,115,943 At 31 December 2006 3,478,750 265,571 201,400 120,653 113,470 2,214,931 6,394,775 At 1 January 2007 3,478,750 265,571 201,400 120,653 113,470 2,214,931 6,394,775

Capital Increase 1,521,250

(120,653)

(1,176,095) 224,502

Dividend payment

(1,057,971)

(1,057,971) Adjustments 6,579 6,579 Write-back of excess revaluation surplus

(12,556) 12,556 0

Transfer (to)/ from accumulated losses 105,797 - 105,797 Profit for the year 3,115,611 3,115,611 At 31 December 07 5,000,000 371,368 201,400 - 100,914 3,115,611 8,789,293

The accounting policies and notes on pages 11 to 39 are an integral part of these financial statements

1 0

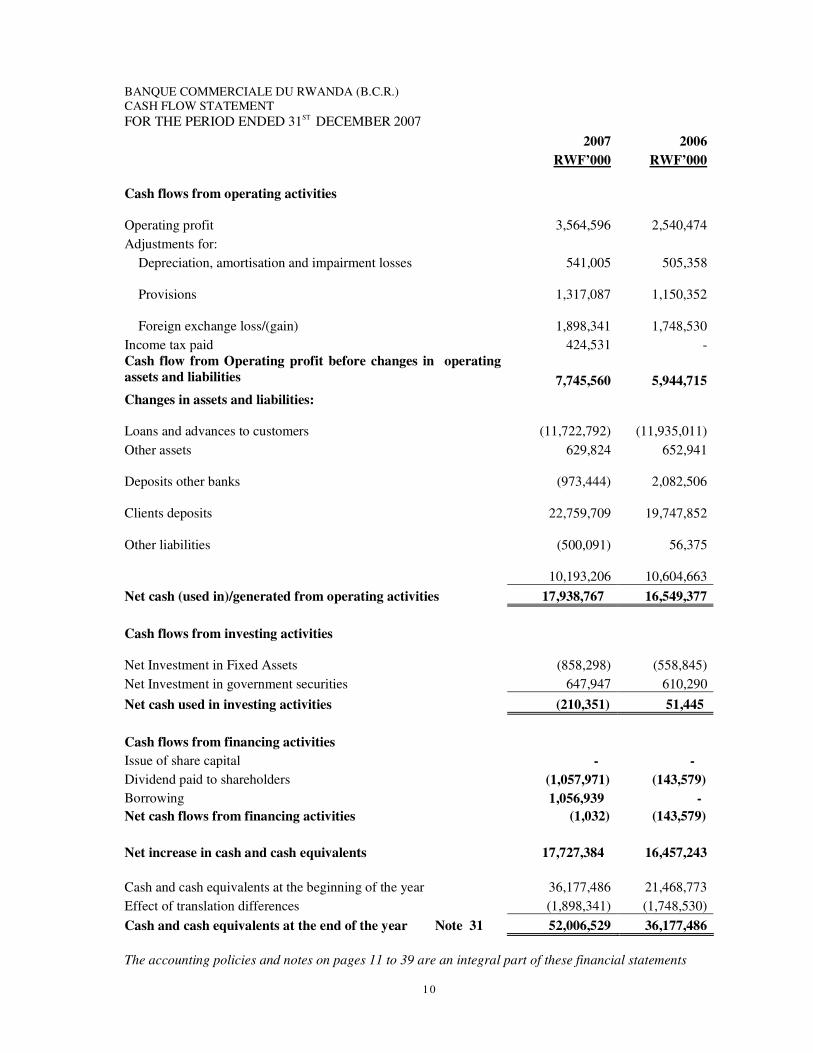

BANQUE COMMERCIALE DU RWANDA (B.C.R.) CASH FLOW STATEMENT FOR THE PERIOD ENDED 31ST DECEMBER 2007

The accounting policies and notes on pages 11 to 39 are an integral part of these financial statements

2007 2006 RWF’000 RWF’000 Cash flows from operating activities

Operating profit

3,564,596

2,540,474 Adjustments for:

Depreciation, amortisation and impairment losses 541,005 505,358

Provisions

1,317,087

1,150,352

Foreign exchange loss/(gain)

1,898,341

1,748,530 Income tax paid 424,531 -

Cash flow from Operating profit before changes in operating assets and liabilities 7,745,560 5,944,715 Changes in assets and liabilities:

Loans and advances to customers

(11,722,792)

(11,935,011) Other assets 629,824 652,941

Deposits other banks

(973,444)

2,082,506

Clients deposits

22,759,709

19,747,852

Other liabilities

(500,091) 56,375

10,193,206

10,604,663 Net cash (used in)/generated from operating activities 17,938,767 16,549,377 Cash flows from investing activities

Net Investment in Fixed Assets

(858,298)

(558,845) Net Investment in government securities 647,947 610,290 Net cash used in investing activities (210,351) 51,445 Cash flows from financing activities Issue of share capital - - Dividend paid to shareholders (1,057,971) (143,579) Borrowing 1,056,939 - Net cash flows from financing activities (1,032) (143,579) Net increase in cash and cash equivalents 17,727,384 16,457,243 Cash and cash equivalents at the beginning of the year 36,177,486 21,468,773 Effect of translation differences (1,898,341) (1,748,530) Cash and cash equivalents at the end of the year Note 31 52,006,529 36,177,486

1 1

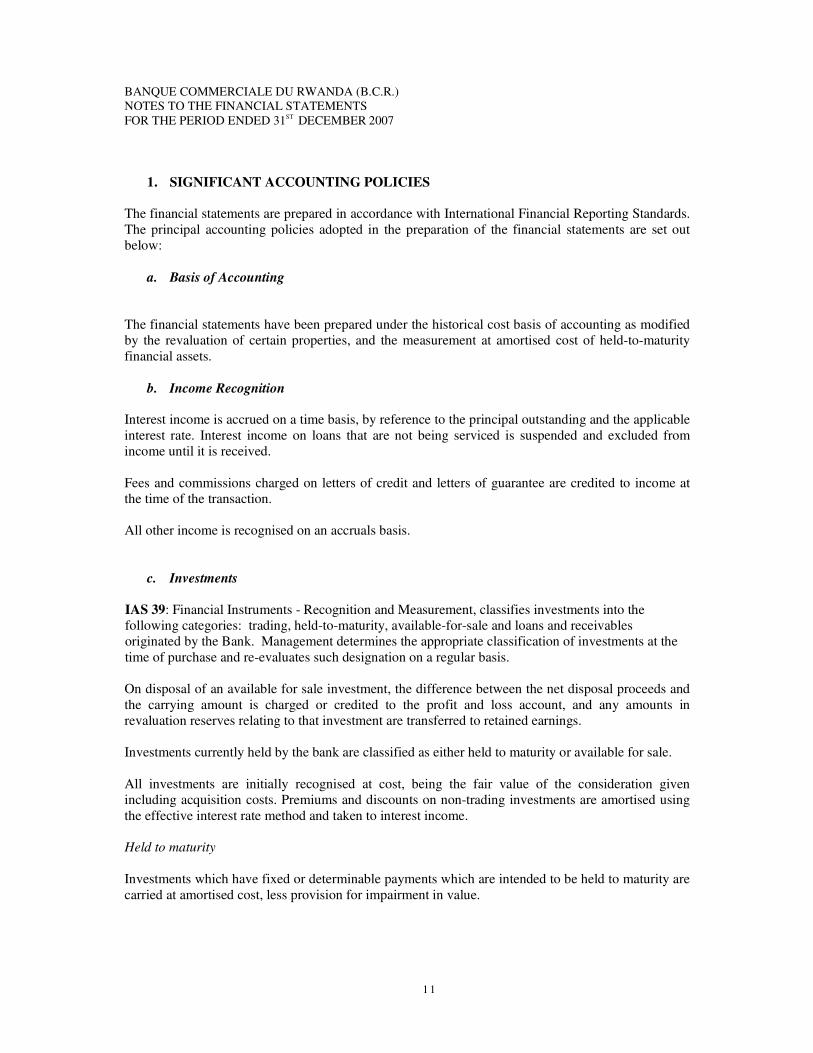

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS FOR THE PERIOD ENDED 31ST DECEMBER 2007

1. SIGNIFICANT ACCOUNTING POLICIES The financial statements are prepared in accordance with International Financial Reporting Standards. The principal accounting policies adopted in the preparation of the financial statements are set out below:

a. Basis of Accounting

The financial statements have been prepared under the historical cost basis of accounting as modified by the revaluation of certain properties, and the measurement at amortised cost of held-to-maturity financial assets.

b. Income Recognition Interest income is accrued on a time basis, by reference to the principal outstanding and the applicable interest rate. Interest income on loans that are not being serviced is suspended and excluded from income until it is received. Fees and commissions charged on letters of credit and letters of guarantee are credited to income at the time of the transaction. All other income is recognised on an accruals basis.

c. Investments IAS 39: Financial Instruments - Recognition and Measurement, classifies investments into the following categories: trading, held-to-maturity, available-for-sale and loans and receivables originated by the Bank. Management determines the appropriate classification of investments at the time of purchase and re-evaluates such designation on a regular basis.

On disposal of an available for sale investment, the difference between the net disposal proceeds and the carrying amount is charged or credited to the profit and loss account, and any amounts in revaluation reserves relating to that investment are transferred to retained earnings. Investments currently held by the bank are classified as either held to maturity or available for sale. All investments are initially recognised at cost, being the fair value of the consideration given including acquisition costs. Premiums and discounts on non-trading investments are amortised using the effective interest rate method and taken to interest income. Held to maturity Investments which have fixed or determinable payments which are intended to be held to maturity are carried at amortised cost, less provision for impairment in value.

1 2

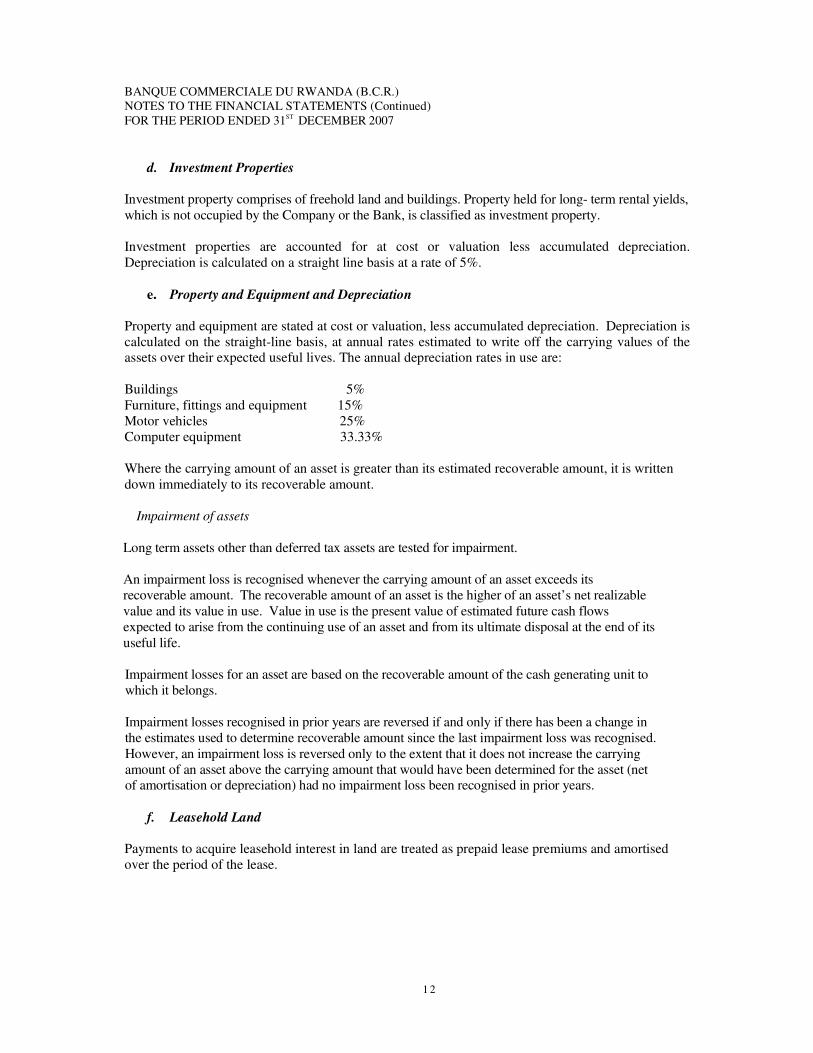

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007

d. Investment Properties Investment property comprises of freehold land and buildings. Property held for long- term rental yields, which is not occupied by the Company or the Bank, is classified as investment property. Investment properties are accounted for at cost or valuation less accumulated depreciation. Depreciation is calculated on a straight line basis at a rate of 5%.

e. Property and Equipment and Depreciation Property and equipment are stated at cost or valuation, less accumulated depreciation. Depreciation is calculated on the straight-line basis, at annual rates estimated to write off the carrying values of the assets over their expected useful lives. The annual depreciation rates in use are: Buildings 5% Furniture, fittings and equipment 15% Motor vehicles 25% Computer equipment 33.33% Where the carrying amount of an asset is greater than its estimated recoverable amount, it is written down immediately to its recoverable amount. Impairment of assets Long term assets other than deferred tax assets are tested for impairment. An impairment loss is recognised whenever the carrying amount of an asset exceeds its recoverable amount. The recoverable amount of an asset is the higher of an asset’s net realizable value and its value in use. Value in use is the present value of estimated future cash flows expected to arise from the continuing use of an asset and from its ultimate disposal at the end of its useful life. Impairment losses for an asset are based on the recoverable amount of the cash generating unit to which it belongs. Impairment losses recognised in prior years are reversed if and only if there has been a change in the estimates used to determine recoverable amount since the last impairment loss was recognised. However, an impairment loss is reversed only to the extent that it does not increase the carrying amount of an asset above the carrying amount that would have been determined for the asset (net of amortisation or depreciation) had no impairment loss been recognised in prior years.

f. Leasehold Land Payments to acquire leasehold interest in land are treated as prepaid lease premiums and amortised over the period of the lease.

1 3

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007

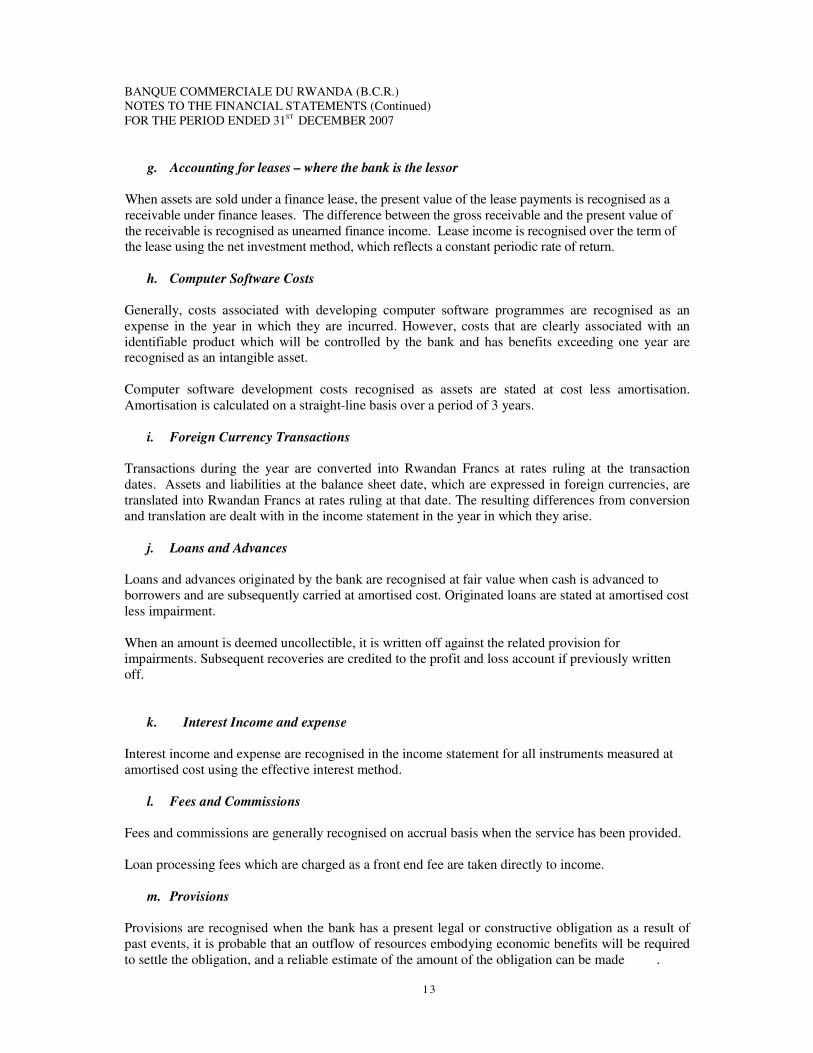

g. Accounting for leases – where the bank is the lessor When assets are sold under a finance lease, the present value of the lease payments is recognised as a receivable under finance leases. The difference between the gross receivable and the present value of the receivable is recognised as unearned finance income. Lease income is recognised over the term of the lease using the net investment method, which reflects a constant periodic rate of return.

h. Computer Software Costs Generally, costs associated with developing computer software programmes are recognised as an expense in the year in which they are incurred. However, costs that are clearly associated with an identifiable product which will be controlled by the bank and has benefits exceeding one year are recognised as an intangible asset. Computer software development costs recognised as assets are stated at cost less amortisation. Amortisation is calculated on a straight-line basis over a period of 3 years.

i. Foreign Currency Transactions Transactions during the year are converted into Rwandan Francs at rates ruling at the transaction dates. Assets and liabilities at the balance sheet date, which are expressed in foreign currencies, are translated into Rwandan Francs at rates ruling at that date. The resulting differences from conversion and translation are dealt with in the income statement in the year in which they arise.

j. Loans and Advances Loans and advances originated by the bank are recognised at fair value when cash is advanced to borrowers and are subsequently carried at amortised cost. Originated loans are stated at amortised cost less impairment. When an amount is deemed uncollectible, it is written off against the related provision for impairments. Subsequent recoveries are credited to the profit and loss account if previously written off.

k. Interest Income and expense Interest income and expense are recognised in the income statement for all instruments measured at amortised cost using the effective interest method.

l. Fees and Commissions

Fees and commissions are generally recognised on accrual basis when the service has been provided.

Loan processing fees which are charged as a front end fee are taken directly to income.

m. Provisions

Provisions are recognised when the bank has a present legal or constructive obligation as a result of past events, it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation, and a reliable estimate of the amount of the obligation can be made .

1 4

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007 .

n. Provision for Doubtful Debts

Provisions are made in respect of loans and advances considered to be doubtful of recovery at the following rates:

Description Class Provision Rate

(%) Current advances 1 - Watch advances 2 - Doubtful advances 3 20/100 Litigious advances 4 50/100 Contentious advances 5 100 Provisions based on periodic appraisals of the advances portfolio in relation to identified risk on loans and advances, reflecting an estimate of loss expected, are gross of mortgage values and are charged to the income statement.

o. Retirement Benefit Costs

The bank contributes to a statutory defined contribution scheme, the Caisse Sociale du Rwanda. Contributions are determined by local statute and are currently limited to 5% of the total of an employee’s basic salary and house allowance. The bank in addition pays pensions to retiring employees based on number of years of service. A provision is made for the liability for pension payable as a result of services rendered by employees up to the balance sheet date. The bank’s contributions to the above scheme and monetary liability for pensions payable are charged to the income statement in the year in which they relate.

p. Employee Entitlements

Employee entitlement to gratuity and long service awards are recognised when they accrue to employees. A provision is made for the liability for such entitlements as a result of services rendered by employees up to the balance sheet date. The monetary liability for employees’ accrued annual leave entitlement at the balance sheet date is recognised as an expense accrual.

q. Letters of Credit The bank makes a provision for letters of credit once they are constituted and blocks an

equivalent amount of cash from the customers’ accounts. Letters of credit and blocked cash constituted in foreign currencies are translated at rates ruling at the balance sheet date and the resulting exchange differences dealt with in the income statement.

1 5

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007

r. Taxation Current taxation is provided for on the basis of the results for the year as shown in the financial statements, adjusted in accordance with the prevailing tax legislation. Deferred taxation is provided using the balance sheet liability method, for all temporary differences arising between the tax bases of assets and liabilities and their carrying values for financial reporting purposes. Deferred tax assets are recognised for all deductible temporary differences, carry forward of unused tax losses and unused tax credits to the extent that it is probable that future taxable profits will be available against which the deductible temporary differences, unused tax losses and unused tax credits can be utilised.

s. Cash and cash equivalents

Cash and cash equivalents comprise balances with maturities of less than 91 days from the date of acquisition and include cash and balances with the National Bank of Rwanda, government securities and deposits with other banks and financial institutions.

t. Comparatives

Where necessary, comparative figures have been adjusted to conform to changes in presentation in the current year.

1 6

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007.

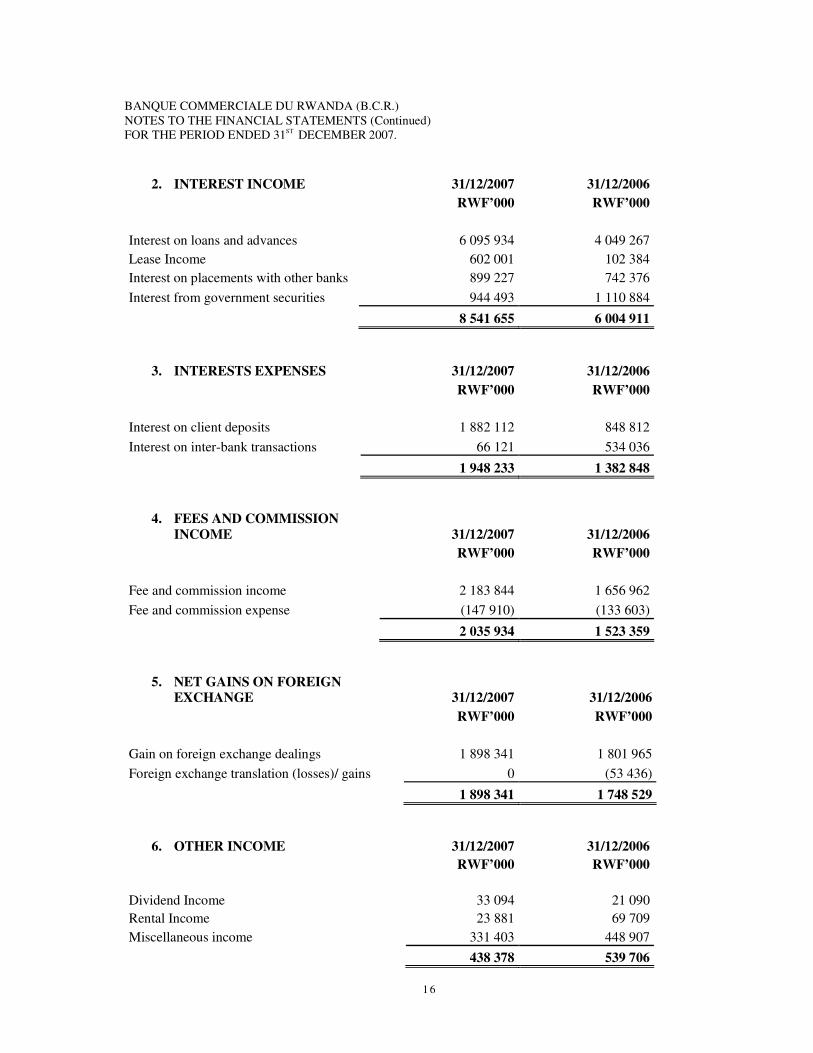

2. INTEREST INCOME 31/12/2007 31/12/2006 RWF’000 RWF’000 Interest on loans and advances 6 095 934 4 049 267 Lease Income 602 001 102 384 Interest on placements with other banks 899 227 742 376 Interest from government securities 944 493 1 110 884

2. INTEREST INCOME 8 541 655 6 004 911

3. INTERESTS EXPENSES 31/12/2007 31/12/2006 RWF’000 RWF’000 Interest on client deposits 1 882 112 848 812 Interest on inter-bank transactions 66 121 534 036

3. INTERESTS EXPENSES 1 948 233 1 382 848

4. FEES AND COMMISSION INCOME 31/12/2007 31/12/2006

RWF’000 RWF’000 Fee and commission income 2 183 844 1 656 962 Fee and commission expense (147 910) (133 603)

4. FEES AND COMMISSION INCOME 2 035 934 1 523 359

5. NET GAINS ON FOREIGN EXCHANGE 31/12/2007 31/12/2006

RWF’000 RWF’000 Gain on foreign exchange dealings 1 898 341 1 801 965 Foreign exchange translation (losses)/ gains 0 (53 436)

5. NET GAINS ON FOREIGN EXCHANGE 1 898 341 1 748 529

6. OTHER INCOME 31/12/2007 31/12/2006 RWF’000 RWF’000 Dividend Income 33 094 21 090 Rental Income 23 881 69 709 Miscellaneous income 331 403 448 907 6. OTHER INCOME 438 378 539 706

1 7

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007

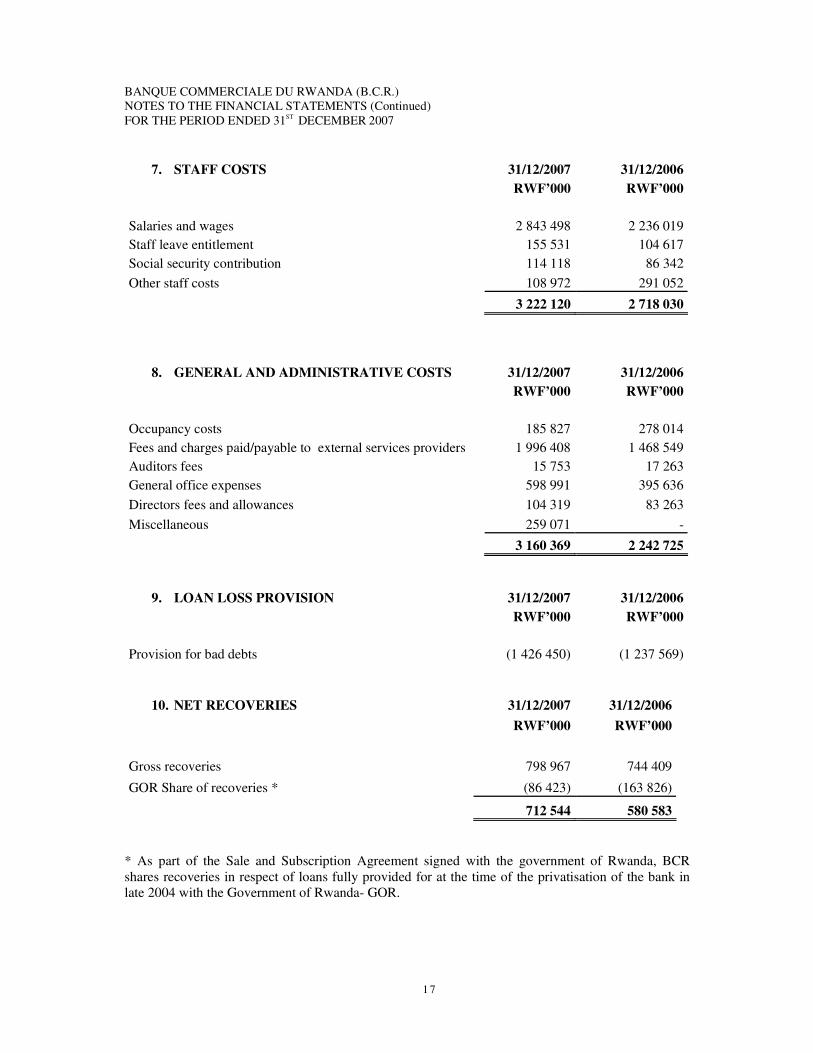

7. STAFF COSTS 31/12/2007 31/12/2006 RWF’000 RWF’000 Salaries and wages 2 843 498 2 236 019 Staff leave entitlement 155 531 104 617 Social security contribution 114 118 86 342 Other staff costs 108 972 291 052

7. STAFF COSTS 3 222 120 2 718 030

8. GENERAL AND ADMINISTRATIVE COSTS 31/12/2007 31/12/2006 RWF’000 RWF’000 Occupancy costs 185 827 278 014 Fees and charges paid/payable to external services providers 1 996 408 1 468 549 Auditors fees 15 753 17 263 General office expenses 598 991 395 636 Directors fees and allowances 104 319 83 263 Miscellaneous 259 071 -

8. GENERAL AND ADMINISTRATIVE COSTS 3 160 369 2 242 725

9. LOAN LOSS PROVISION 31/12/2007 31/12/2006 RWF’000 RWF’000 Provision for bad debts (1 426 450) (1 237 569)

10. NET RECOVERIES 31/12/2007 31/12/2006 RWF’000 RWF’000 Gross recoveries 798 967 744 409

GOR Share of recoveries * (86 423) (163 826)

10. NET RECOVERIES 712 544 580 583 * As part of the Sale and Subscription Agreement signed with the government of Rwanda, BCR shares recoveries in respect of loans fully provided for at the time of the privatisation of the bank in late 2004 with the Government of Rwanda- GOR.

1 8

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007

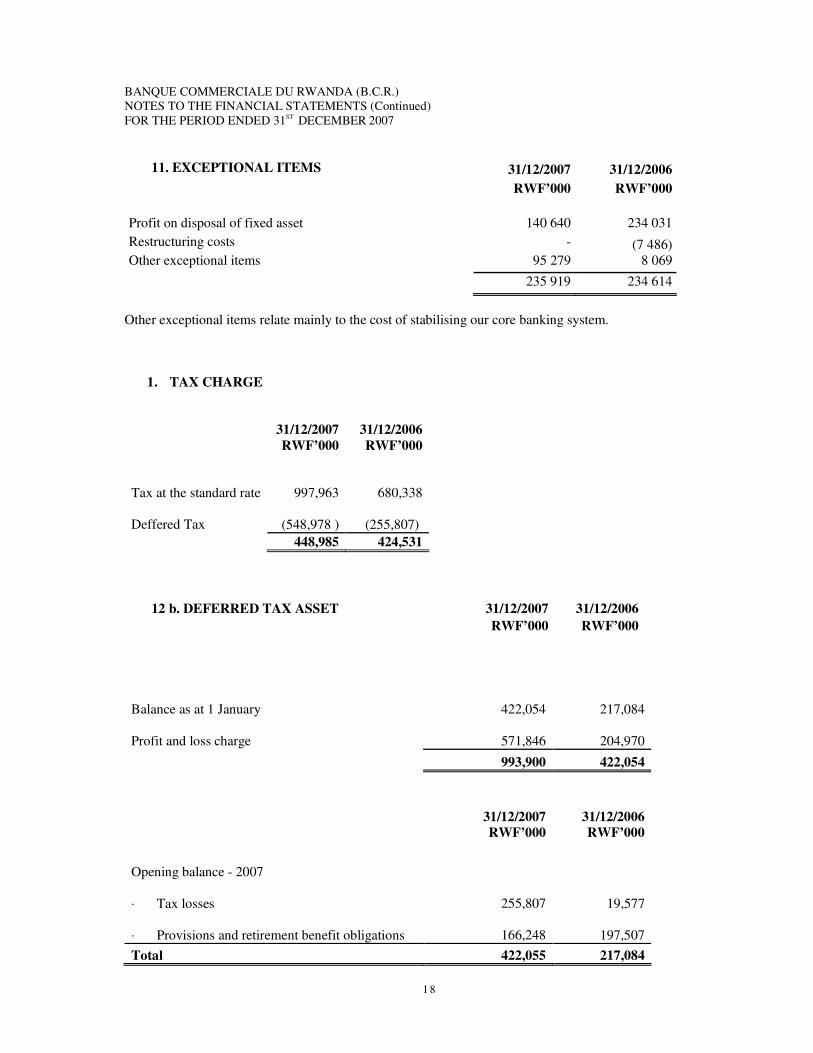

11. EXCEPTIONAL ITEMS 31/12/2007 31/12/2006 RWF’000 RWF’000 Profit on disposal of fixed asset 140 640 234 031 Restructuring costs - (7 486) Other exceptional items 95 279 8 069

11. EXCEPTIONAL ITEMS 235 919 234 614

Other exceptional items relate mainly to the cost of stabilising our core banking system.

1. TAX CHARGE 31/12/2007 31/12/2006 RWF’000 RWF’000

Tax at the standard rate

997,963

680,338

Deffered Tax

(548,978 )

(255,807) 448,985 424,531

12 b. DEFERRED TAX ASSET 31/12/2007 31/12/2006 RWF’000 RWF’000

Balance as at 1 January 422,054

217,084

Profit and loss charge 571,846

204,970

993,900 422,054 31/12/2007 31/12/2006 RWF’000 RWF’000 Opening balance - 2007

⋅ Tax losses 255,807

19,577

⋅ Provisions and retirement benefit obligations 166,248

197,507 Total 422,055 217,084

1 9

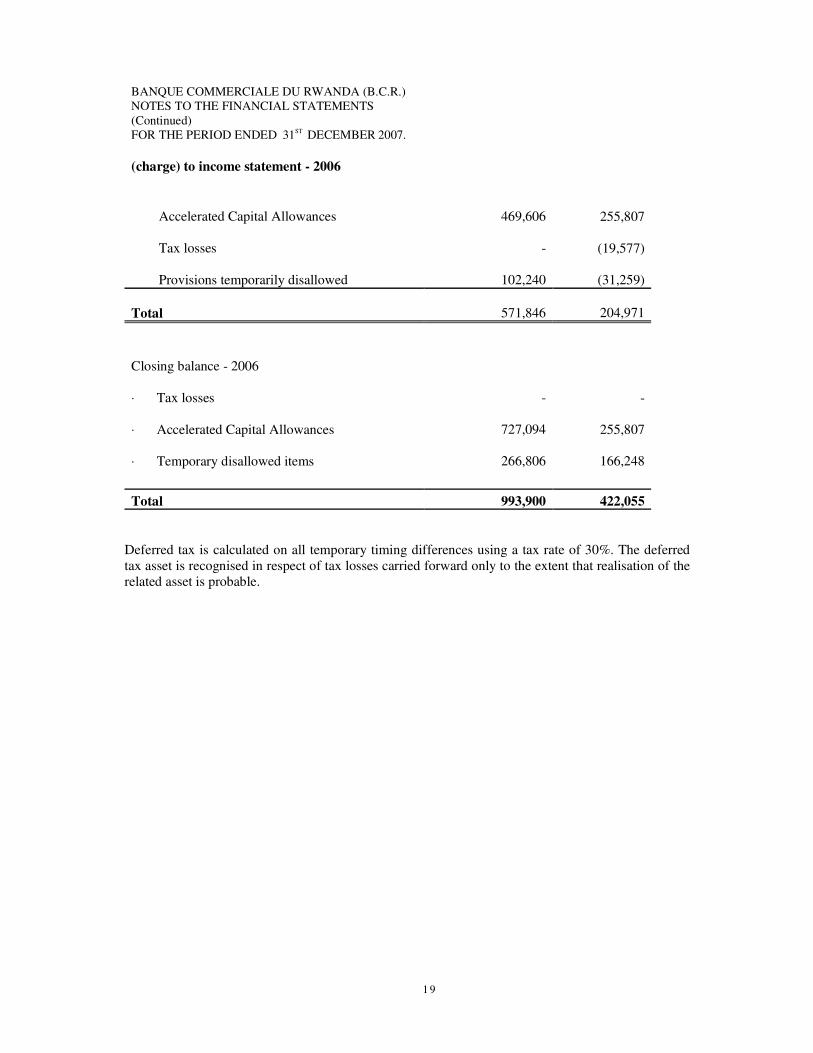

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007. (charge) to income statement - 2006

Accelerated Capital Allowances 469,606

255,807

Tax losses -

(19,577)

Provisions temporarily disallowed 102,240

(31,259)

Total 571,846

204,971 Closing balance - 2006

⋅ Tax losses -

-

⋅ Accelerated Capital Allowances 727,094

255,807

⋅ Temporary disallowed items 266,806

166,248 Total 993,900 422,055

Deferred tax is calculated on all temporary timing differences using a tax rate of 30%. The deferred tax asset is recognised in respect of tax losses carried forward only to the extent that realisation of the related asset is probable.

2 0

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 1ST DECEMBER 2007

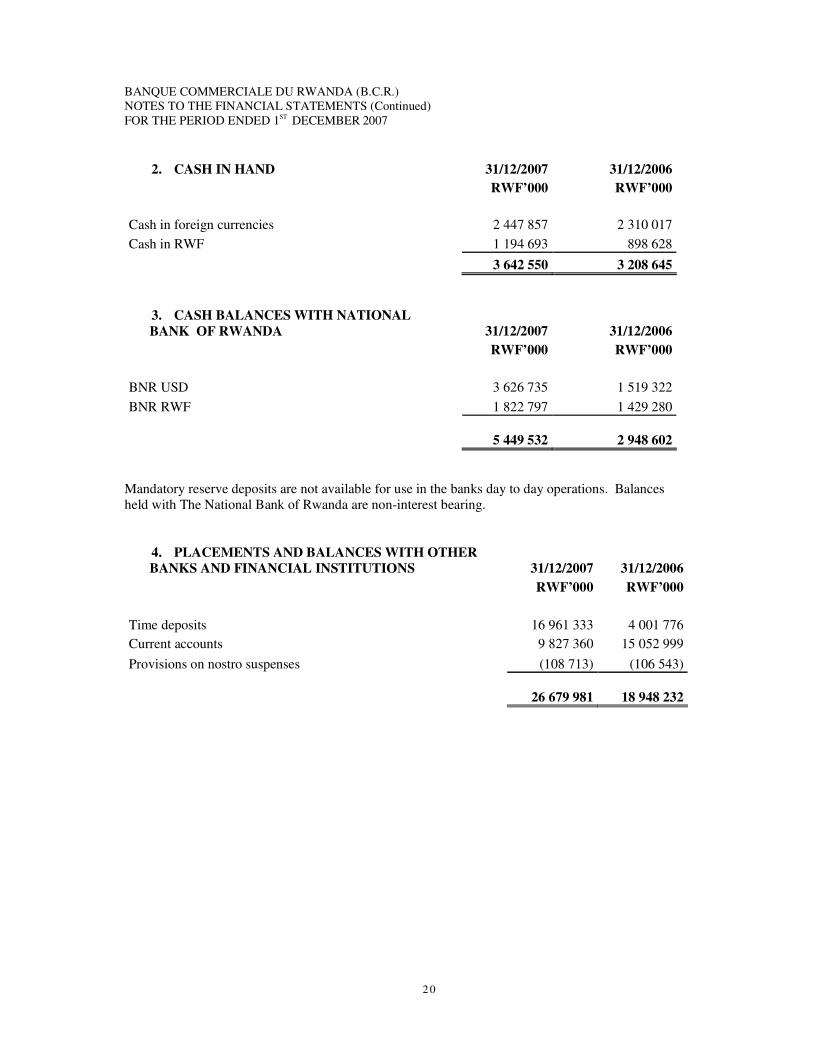

2. CASH IN HAND 31/12/2007 31/12/2006 RWF’000 RWF’000 Cash in foreign currencies 2 447 857 2 310 017 Cash in RWF 1 194 693 898 628 13. CASH IN HAND 3 642 550 3 208 645

3. CASH BALANCES WITH NATIONAL BANK OF RWANDA 31/12/2007 31/12/2006 RWF’000 RWF’000 BNR USD 3 626 735 1 519 322 BNR RWF 1 822 797 1 429 280 14. CASH BALANCES WITH NATIONAL BANK OF RWAN 5 449 532 2 948 602

Mandatory reserve deposits are not available for use in the banks day to day operations. Balances held with The National Bank of Rwanda are non-interest bearing.

4. PLACEMENTS AND BALANCES WITH OTHER BANKS AND FINANCIAL INSTITUTIONS 31/12/2007 31/12/2006 RWF’000 RWF’000 Time deposits 16 961 333 4 001 776 Current accounts 9 827 360 15 052 999 Provisions on nostro suspenses (108 713) (106 543) 15. PLACEMENTS AND BALANCES WITH OTHER BANKS AND FINANCIAL INSTITUTIONS 26 679 981 18 948 232

2 1

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007

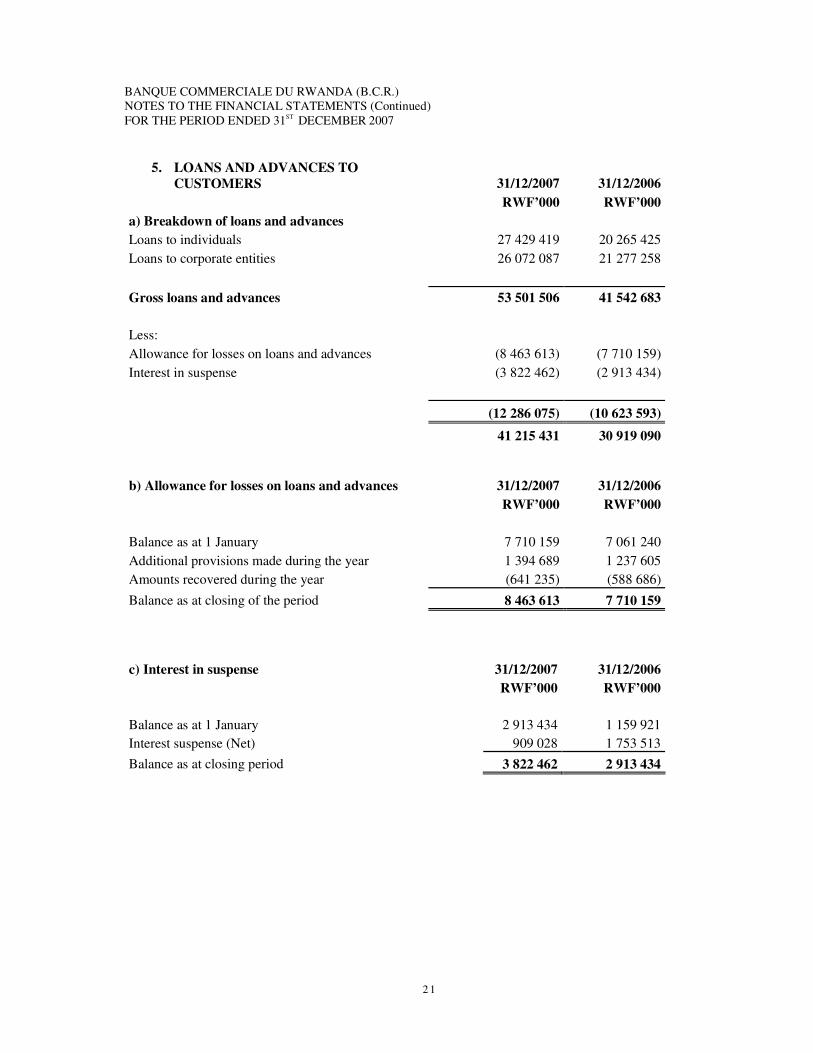

5. LOANS AND ADVANCES TO CUSTOMERS 31/12/2007 31/12/2006

RWF’000 RWF’000 a) Breakdown of loans and advances Loans to individuals 27 429 419 20 265 425 Loans to corporate entities 26 072 087 21 277 258 Gross loans and advances 53 501 506 41 542 683 Less: Allowance for losses on loans and advances (8 463 613) (7 710 159) Interest in suspense (3 822 462) (2 913 434)

(12 286 075) (10 623 593) 41 215 431 30 919 090 b) Allowance for losses on loans and advances 31/12/2007 31/12/2006 RWF’000 RWF’000 Balance as at 1 January 7 710 159 7 061 240 Additional provisions made during the year 1 394 689 1 237 605 Amounts recovered during the year (641 235) (588 686)

Balance as at closing of the period 8 463 613 7 710 159

c) Interest in suspense 31/12/2007 31/12/2006 RWF’000 RWF’000 Balance as at 1 January 2 913 434 1 159 921 Interest suspense (Net) 909 028 1 753 513 Balance as at closing period 3 822 462 2 913 434

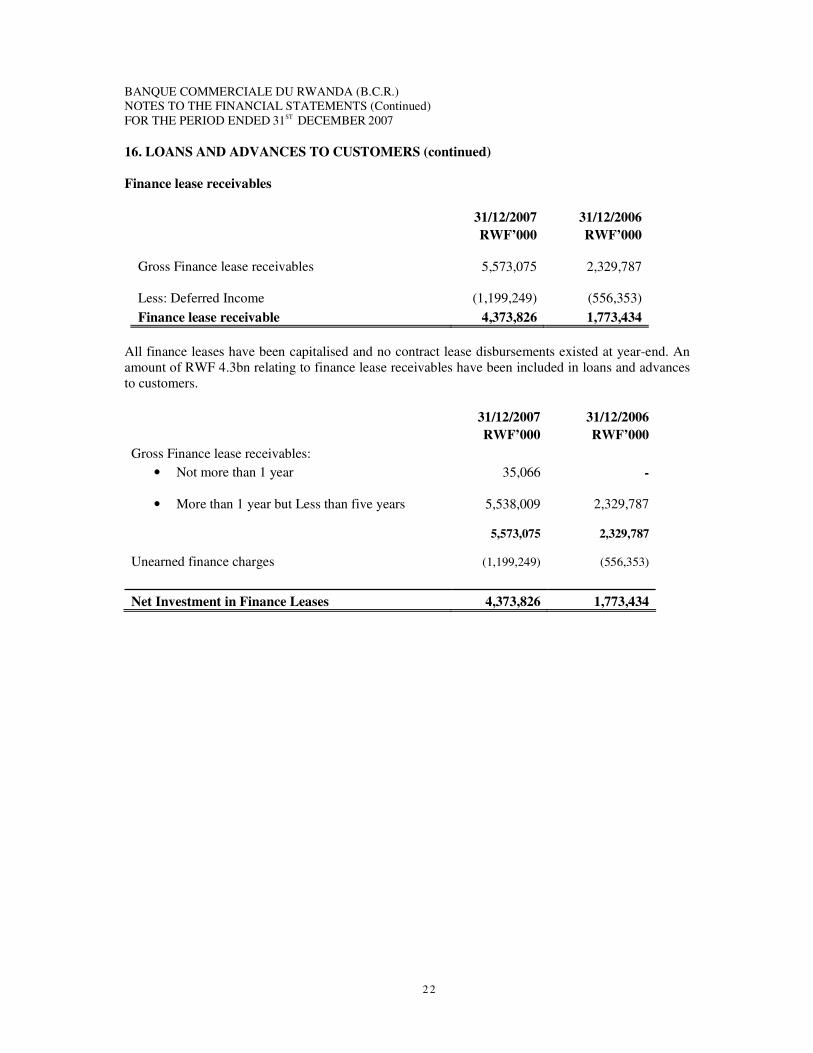

2 2

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007 16. LOANS AND ADVANCES TO CUSTOMERS (continued) Finance lease receivables

31/12/2007 31/12/2006 RWF’000 RWF’000

Gross Finance lease receivables

5,573,075

2,329,787

Less: Deferred Income

(1,199,249)

(556,353) Finance lease receivable 4,373,826 1,773,434

All finance leases have been capitalised and no contract lease disbursements existed at year-end. An amount of RWF 4.3bn relating to finance lease receivables have been included in loans and advances to customers.

31/12/2007 31/12/2006 RWF’000 RWF’000 Gross Finance lease receivables:

• Not more than 1 year 35,066 -

• More than 1 year but Less than five years

5,538,009 2,329,787

5,573,075 2,329,787

Unearned finance charges

(1,199,249)

(556,353)

Net Investment in Finance Leases 4,373,826 1,773,434

2 3

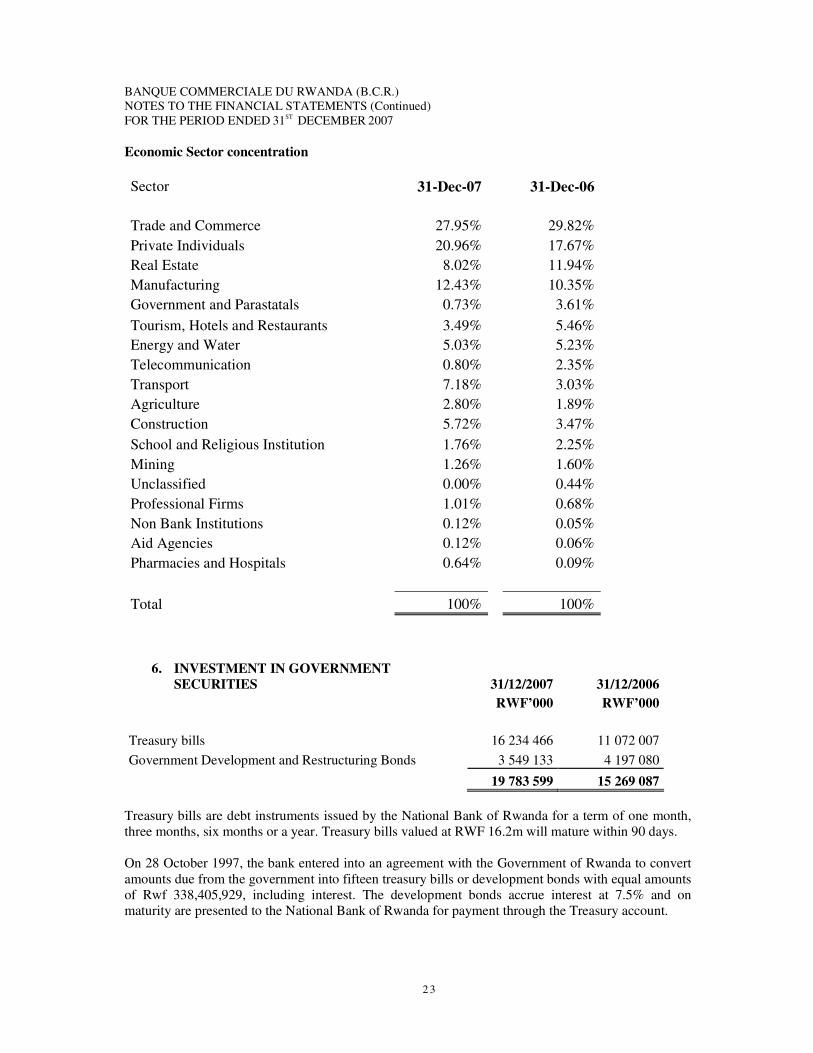

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007 Economic Sector concentration Sector 31-Dec-07 31-Dec-06 Trade and Commerce 27.95% 29.82% Private Individuals 20.96% 17.67% Real Estate 8.02% 11.94% Manufacturing 12.43% 10.35% Government and Parastatals 0.73% 3.61% Tourism, Hotels and Restaurants 3.49% 5.46% Energy and Water 5.03% 5.23% Telecommunication 0.80% 2.35% Transport 7.18% 3.03% Agriculture 2.80% 1.89% Construction 5.72% 3.47% School and Religious Institution 1.76% 2.25% Mining 1.26% 1.60% Unclassified 0.00% 0.44% Professional Firms 1.01% 0.68% Non Bank Institutions 0.12% 0.05% Aid Agencies 0.12% 0.06% Pharmacies and Hospitals 0.64% 0.09% Total 100% 100%

6. INVESTMENT IN GOVERNMENT

SECURITIES 31/12/2007 31/12/2006 RWF’000 RWF’000 Treasury bills 16 234 466 11 072 007 Government Development and Restructuring Bonds 3 549 133 4 197 080

17. INVESTMENT IN GOVERNMENT SECURITIES 19 783 599 15 269 087 Treasury bills are debt instruments issued by the National Bank of Rwanda for a term of one month, three months, six months or a year. Treasury bills valued at RWF 16.2m will mature within 90 days. On 28 October 1997, the bank entered into an agreement with the Government of Rwanda to convert amounts due from the government into fifteen treasury bills or development bonds with equal amounts of Rwf 338,405,929, including interest. The development bonds accrue interest at 7.5% and on maturity are presented to the National Bank of Rwanda for payment through the Treasury account.

2 4

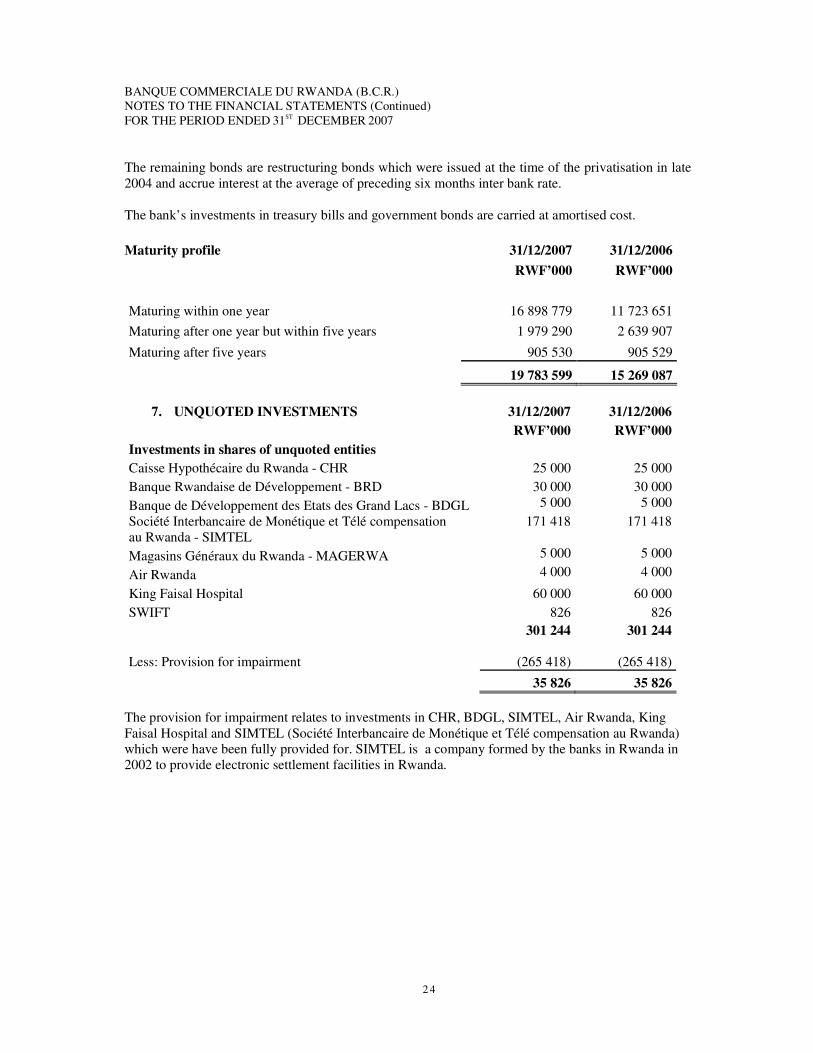

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007 The remaining bonds are restructuring bonds which were issued at the time of the privatisation in late 2004 and accrue interest at the average of preceding six months inter bank rate.

The bank’s investments in treasury bills and government bonds are carried at amortised cost. Maturity profile 31/12/2007 31/12/2006 RWF’000 RWF’000 Maturing within one year 16 898 779 11 723 651 Maturing after one year but within five years 1 979 290 2 639 907

Maturing after five years 905 530 905 529

19 783 599 15 269 087

7. UNQUOTED INVESTMENTS 31/12/2007 31/12/2006 RWF’000 RWF’000 Investments in shares of unquoted entities Caisse Hypothécaire du Rwanda - CHR 25 000 25 000 Banque Rwandaise de Développement - BRD 30 000 30 000 Banque de Développement des Etats des Grand Lacs - BDGL 5 000 5 000 Société Interbancaire de Monétique et Télé compensation au Rwanda - SIMTEL

171 418 171 418

Magasins Généraux du Rwanda - MAGERWA 5 000 5 000

Air Rwanda 4 000 4 000

King Faisal Hospital 60 000 60 000 SWIFT 826 826 301 244 301 244 Less: Provision for impairment (265 418) (265 418)

35 826 35 826 The provision for impairment relates to investments in CHR, BDGL, SIMTEL, Air Rwanda, King Faisal Hospital and SIMTEL (Société Interbancaire de Monétique et Télé compensation au Rwanda) which were have been fully provided for. SIMTEL is a company formed by the banks in Rwanda in 2002 to provide electronic settlement facilities in Rwanda.

2 5

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007

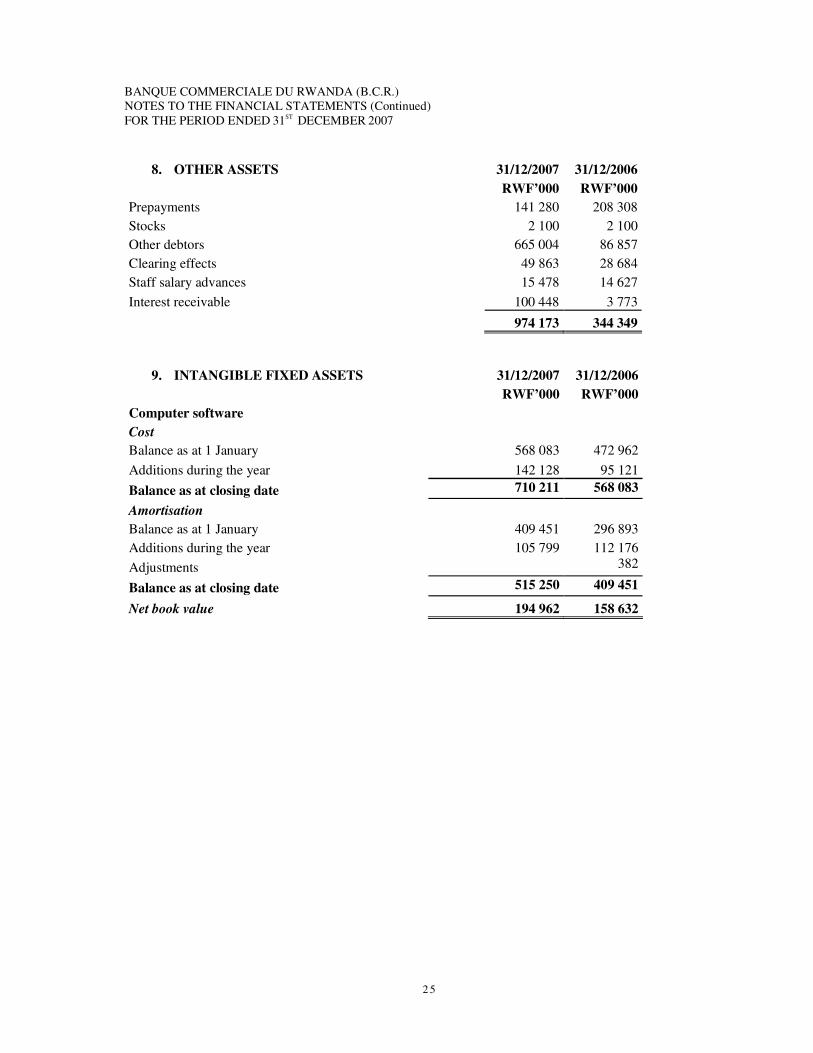

8. OTHER ASSETS 31/12/2007 31/12/2006 RWF’000 RWF’000 Prepayments 141 280 208 308 Stocks 2 100 2 100 Other debtors 665 004 86 857 Clearing effects 49 863 28 684 Staff salary advances 15 478 14 627 Interest receivable 100 448 3 773

19. OTHER ASSETS 974 173 344 349

9. INTANGIBLE FIXED ASSETS 31/12/2007 31/12/2006 RWF’000 RWF’000 Computer software Cost Balance as at 1 January 568 083 472 962 Additions during the year 142 128 95 121 Balance as at closing date 710 211 568 083

Amortisation

Balance as at 1 January 409 451 296 893 Additions during the year 105 799 112 176 Adjustments 382

Balance as at closing date 515 250 409 451

Net book value 194 962 158 632

2 6

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007.

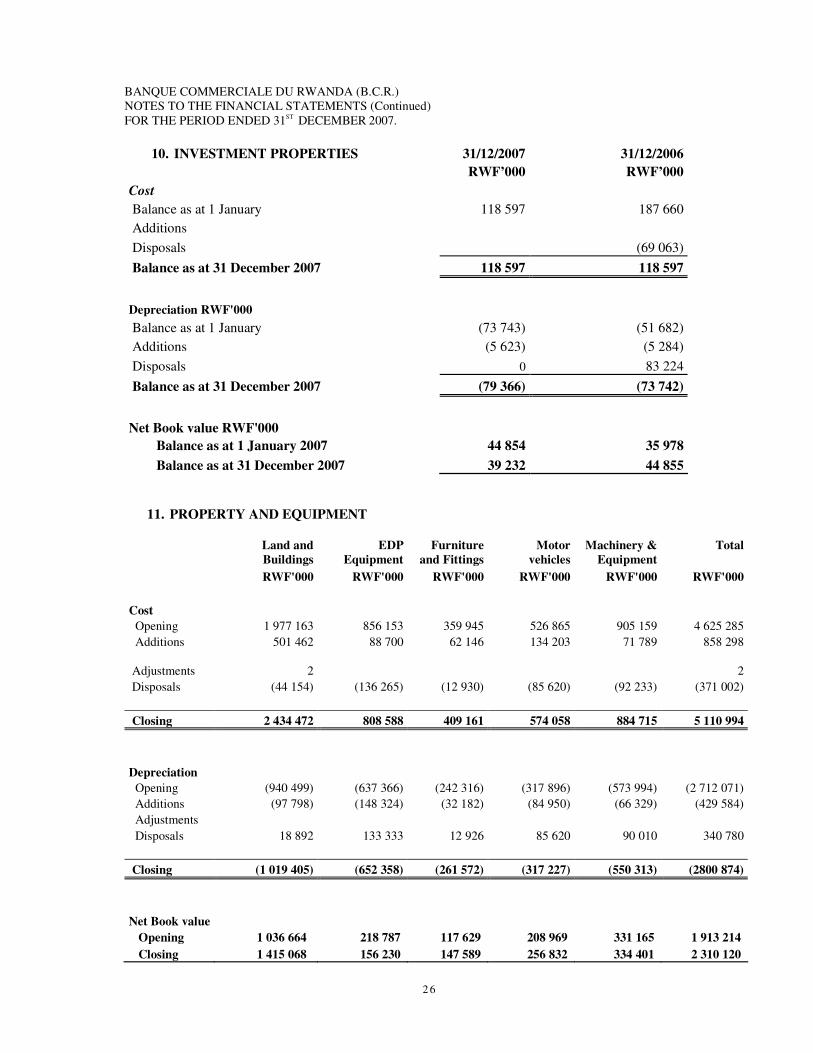

10. INVESTMENT PROPERTIES 31/12/2007 31/12/2006 RWF’000 RWF’000 Cost

Balance as at 1 January 118 597 187 660 Additions

Disposals (69 063) Balance as at 31 December 2007 118 597 118 597 Depreciation RWF'000 Balance as at 1 January (73 743) (51 682) Additions (5 623) (5 284) Disposals 0 83 224 Balance as at 31 December 2007 (79 366) (73 742) Net Book value RWF'000 Balance as at 1 January 2007 44 854 35 978 Balance as at 31 December 2007 39 232 44 855

11. PROPERTY AND EQUIPMENT Land and

Buildings EDP

Equipment Furniture

and Fittings Motor

vehicles Machinery &

Equipment Total

RWF'000 RWF'000 RWF'000 RWF'000 RWF'000 RWF'000 Cost Opening 1 977 163 856 153 359 945 526 865 905 159 4 625 285 Additions 501 462 88 700 62 146 134 203 71 789 858 298

Adjustments 2

2 Disposals (44 154) (136 265) (12 930) (85 620) (92 233) (371 002) Closing 2 434 472 808 588 409 161 574 058 884 715 5 110 994 Depreciation Opening (940 499) (637 366) (242 316) (317 896) (573 994) (2 712 071) Additions (97 798) (148 324) (32 182) (84 950) (66 329) (429 584) Adjustments Disposals 18 892 133 333 12 926 85 620 90 010 340 780 Closing (1 019 405) (652 358) (261 572) (317 227) (550 313) (2800 874) Net Book value Opening 1 036 664 218 787 117 629 208 969 331 165 1 913 214 Closing 1 415 068 156 230 147 589 256 832 334 401 2 310 120

2 7

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007.

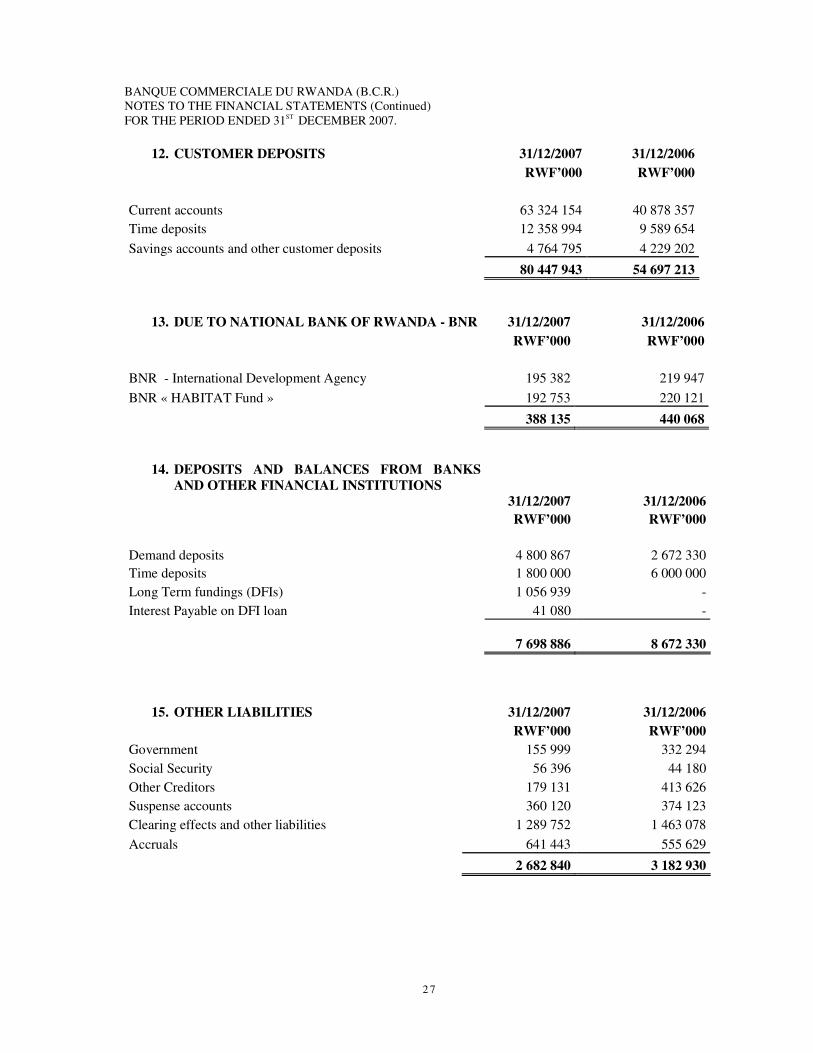

12. CUSTOMER DEPOSITS 31/12/2007 31/12/2006 RWF’000 RWF’000 Current accounts 63 324 154 40 878 357 Time deposits 12 358 994 9 589 654 Savings accounts and other customer deposits 4 764 795 4 229 202

23. CUSTOMER DEPOSITS 80 447 943 54 697 213

13. DUE TO NATIONAL BANK OF RWANDA - BNR 31/12/2007 31/12/2006 RWF’000 RWF’000 BNR - International Development Agency 195 382 219 947 BNR « HABITAT Fund » 192 753 220 121

24. DUE TO NATIONAL BANK OF RWA - BNR 388 135 440 068

14. DEPOSITS AND BALANCES FROM BANKS AND OTHER FINANCIAL INSTITUTIONS

31/12/2007 31/12/2006 RWF’000 RWF’000 Demand deposits 4 800 867 2 672 330 Time deposits 1 800 000 6 000 000 Long Term fundings (DFIs) 1 056 939 - Interest Payable on DFI loan 41 080 - 25. DEPOSITS AND BALANCES FROM BANKS AND OTHER FINANCIAL INSTITUTIONS 7 698 886 8 672 330

15. OTHER LIABILITIES 31/12/2007 31/12/2006 RWF’000 RWF’000 Government 155 999 332 294 Social Security 56 396 44 180 Other Creditors 179 131 413 626 Suspense accounts 360 120 374 123 Clearing effects and other liabilities 1 289 752 1 463 078 Accruals 641 443 555 629

2 682 840 3 182 930

2 8

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007.

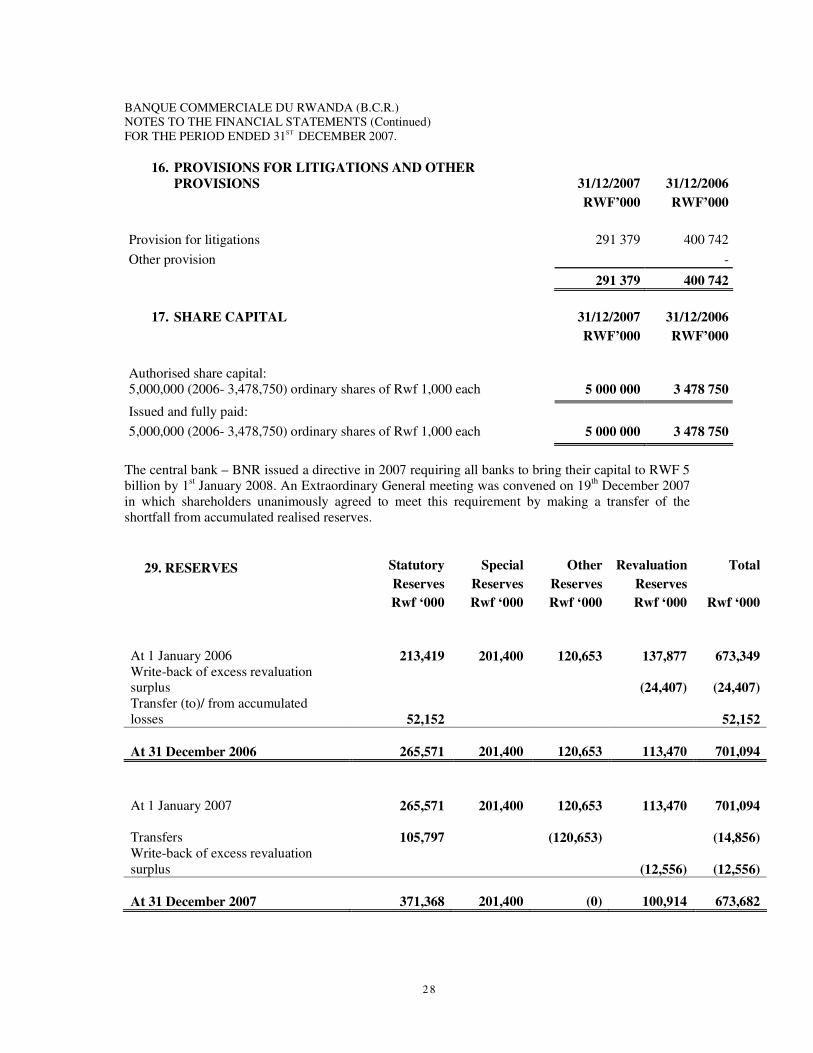

16. PROVISIONS FOR LITIGATIONS AND OTHER PROVISIONS 31/12/2007 31/12/2006

RWF’000 RWF’000 Provision for litigations 291 379 400 742 Other provision -

27. PROVISIONS FOR LITIGATIONS AND OTHER PROVISIONS 291 379 400 742

17. SHARE CAPITAL 31/12/2007 31/12/2006 RWF’000 RWF’000 Authorised share capital: 5,000,000 (2006- 3,478,750) ordinary shares of Rwf 1,000 each 5 000 000 3 478 750 Issued and fully paid: 5,000,000 (2006- 3,478,750) ordinary shares of Rwf 1,000 each 5 000 000 3 478 750

The central bank – BNR issued a directive in 2007 requiring all banks to bring their capital to RWF 5 billion by 1st January 2008. An Extraordinary General meeting was convened on 19th December 2007 in which shareholders unanimously agreed to meet this requirement by making a transfer of the shortfall from accumulated realised reserves. 29. RESERVES Statutory Special Other Revaluation Total Reserves Reserves Reserves Reserves Rwf ‘000 Rwf ‘000 Rwf ‘000 Rwf ‘000 Rwf ‘000

At 1 January 2006 213,419

201,400

120,653

137,877

673,349 Write-back of excess revaluation surplus

(24,407)

(24,407)

Transfer (to)/ from accumulated losses 52,152

52,152

At 31 December 2006 265,571

201,400

120,653

113,470

701,094

At 1 January 2007 265,571

201,400

120,653

113,470

701,094

Transfers 105,797

(120,653)

(14,856) Write-back of excess revaluation surplus

(12,556)

(12,556)

At 31 December 2007 371,368

201,400

(0)

100,914

673,682

2 9

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007.

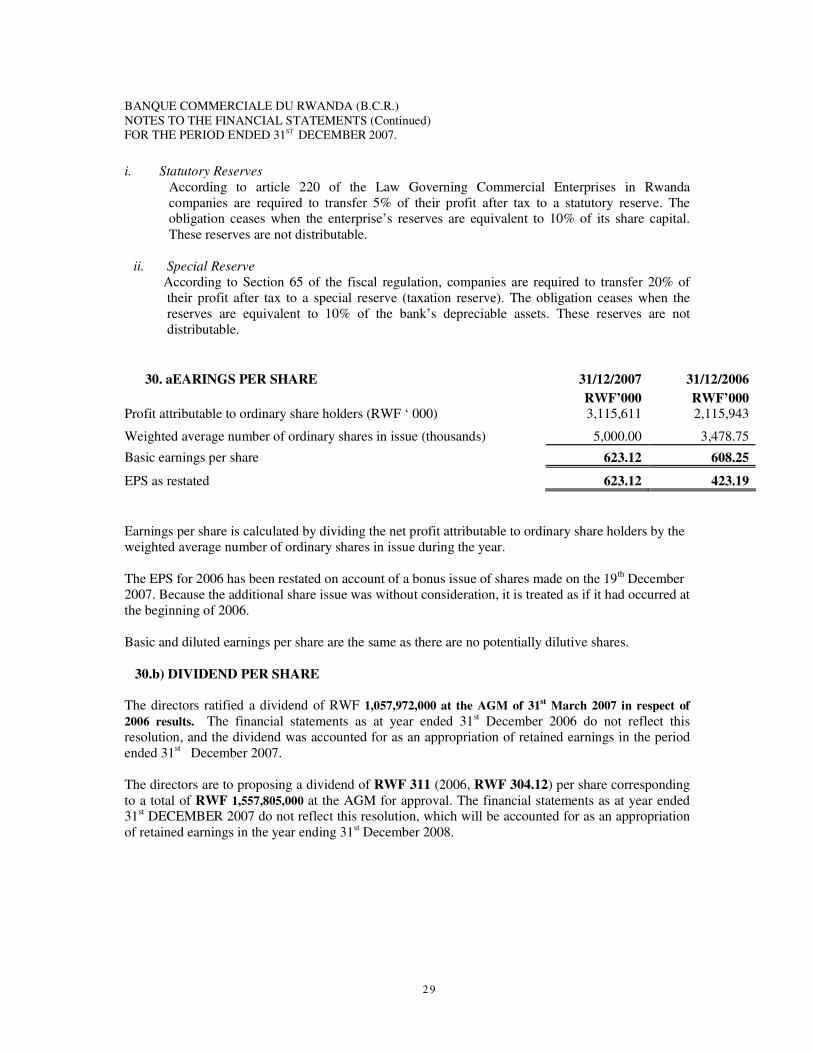

i. Statutory Reserves According to article 220 of the Law Governing Commercial Enterprises in Rwanda

companies are required to transfer 5% of their profit after tax to a statutory reserve. The obligation ceases when the enterprise’s reserves are equivalent to 10% of its share capital. These reserves are not distributable.

ii. Special Reserve

According to Section 65 of the fiscal regulation, companies are required to transfer 20% of their profit after tax to a special reserve (taxation reserve). The obligation ceases when the reserves are equivalent to 10% of the bank’s depreciable assets. These reserves are not distributable.

30. aEARINGS PER SHARE 31/12/2007 31/12/2006 RWF’000 RWF’000

Profit attributable to ordinary share holders (RWF ‘ 000) 3,115,611 2,115,943

Weighted average number of ordinary shares in issue (thousands) 5,000.00 3,478.75

Basic earnings per share 623.12 608.25

EPS as restated 623.12 423.19 Earnings per share is calculated by dividing the net profit attributable to ordinary share holders by the weighted average number of ordinary shares in issue during the year. The EPS for 2006 has been restated on account of a bonus issue of shares made on the 19th December 2007. Because the additional share issue was without consideration, it is treated as if it had occurred at the beginning of 2006. Basic and diluted earnings per share are the same as there are no potentially dilutive shares.

30.b) DIVIDEND PER SHARE The directors ratified a dividend of RWF 1,057,972,000 at the AGM of 31st March 2007 in respect of 2006 results. The financial statements as at year ended 31st December 2006 do not reflect this resolution, and the dividend was accounted for as an appropriation of retained earnings in the period ended 31st December 2007. The directors are to proposing a dividend of RWF 311 (2006, RWF 304.12) per share corresponding to a total of RWF 1,557,805,000 at the AGM for approval. The financial statements as at year ended 31st DECEMBER 2007 do not reflect this resolution, which will be accounted for as an appropriation of retained earnings in the year ending 31st December 2008.

3 0

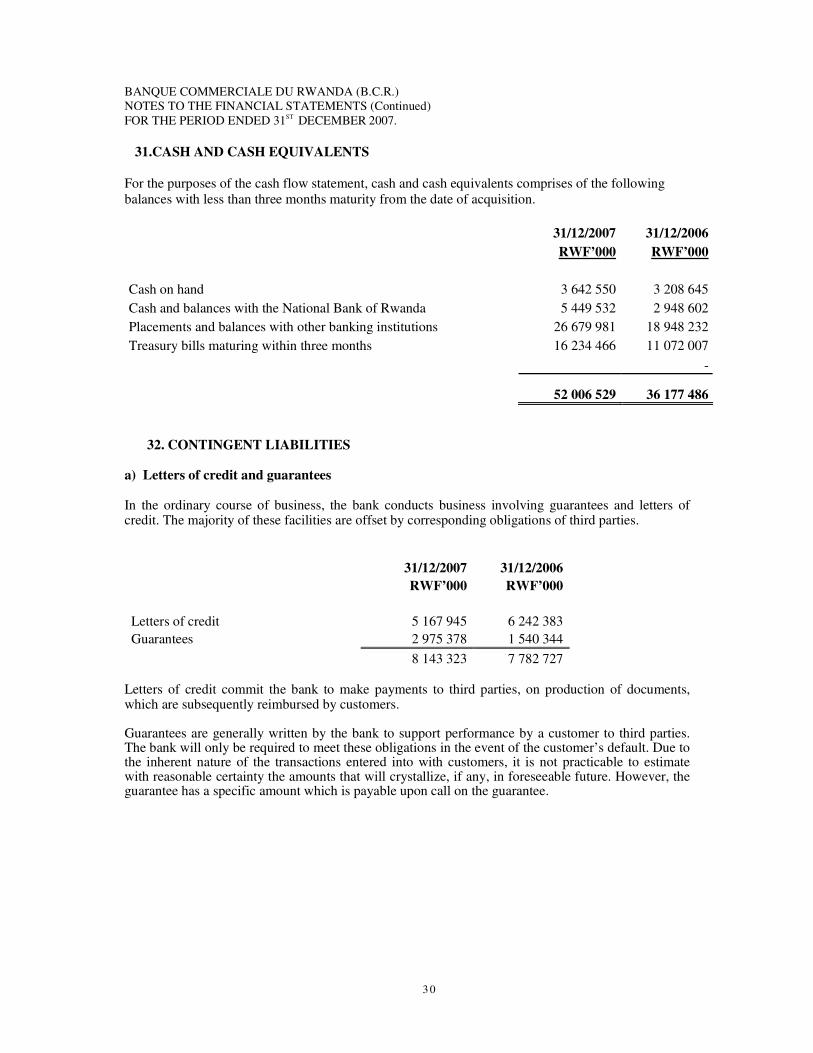

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007. 31.CASH AND CASH EQUIVALENTS For the purposes of the cash flow statement, cash and cash equivalents comprises of the following balances with less than three months maturity from the date of acquisition. 31/12/2007 31/12/2006 RWF’000 RWF’000 Cash on hand 3 642 550 3 208 645 Cash and balances with the National Bank of Rwanda 5 449 532 2 948 602 Placements and balances with other banking institutions 26 679 981 18 948 232 Treasury bills maturing within three months 16 234 466 11 072 007 -

52 006 529 36 177 486

32. CONTINGENT LIABILITIES a) Letters of credit and guarantees In the ordinary course of business, the bank conducts business involving guarantees and letters of credit. The majority of these facilities are offset by corresponding obligations of third parties.

31/12/2007 31/12/2006 RWF’000 RWF’000 Letters of credit 5 167 945 6 242 383 Guarantees 2 975 378 1 540 344 8 143 323 7 782 727

�

Letters of credit commit the bank to make payments to third parties, on production of documents, which are subsequently reimbursed by customers. Guarantees are generally written by the bank to support performance by a customer to third parties. The bank will only be required to meet these obligations in the event of the customer’s default. Due to the inherent nature of the transactions entered into with customers, it is not practicable to estimate with reasonable certainty the amounts that will crystallize, if any, in foreseeable future. However, the guarantee has a specific amount which is payable upon call on the guarantee.

3 1

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007 b) Litigation cases, no provision made

�

The bank is involved in a number of cases, most of which are yet to be concluded by the judicial courts. The damages claimed for cases where the plaintiffs are claiming identifiable specific damages from the bank amount to RWF 2,422,009 for which a provision of RWF 408 million was made in prior years’ the financial statements. No provision has been made for the other court cases in the financial statements, as in the opinion of the directors, the legal outcome will be in the bank’s favour and, where against the bank, will not give rise to any significant losses that are material to the financial statements. These are cases of lender liability in respect of transactions before the privatisation of the bank. As part of the sale and subscription agreement entered into by Actis LLP and the Government of Rwanda, any liability arising from these cases that exceeds provisions made shall be the responsibility of the Government of Rwanda. Any liability in excess of USD 50,000 in respect of cases existing at the time of the privatisation (known and unknown) will be shouldered by the Government of Rwanda. The significant court cases are as follows:

i) ETS RAMNIK- RWF 2,211,285,286

Following court appearances and hearing on various dates in several courts, on 15 January 1999, the Nyabisindu Court of Appeal ordered the bank to pay RWF 2,211,285,286 to ETS RAMNIK for losses incurred by the latter due to delayed clearance of goods from MAGERWA. The bank petitioned against the Court of Appeal’s order RCA 8319/131 and the court upheld BCR’s petition to re-examine the case afresh. On 14 October 1999, ETS RAMNIK appealed against the above decision in the High Court. On 21 October 2001, the High Court referred the matter back to the Nyabisindu Court of Appeal for hearing. The bank is waiting for reaction of the appellate court.

ii) CYFINA- US$ 5,223,600

On 11 October 2002, the Kigali Court of First Instance issued a judgement that nullified the public auction of 27 November 1999, ordered the bank to pay RWF 12,750,000 to Mr Rulinda as damages, ordered the bank to pay SICAF back the money paid for the 14 coffee machines belonging to Mr Rulinda plus interest and to pay back government duties arising from the public auction. On 28 October 2002, Mr Rulinda appealed in the lower courts against the decision seeking US$ 5,223,600 as damages to be paid jointly by the bank, SICAF and the Government of Rwanda. The bank appealed against the decision and hearing is in progress. At the appeal stage, the bank was ordered to pay an amount of RWF 399million. However, according to The Sale and Subscription Agreement – SSA, the Government of Rwanda will pay the amount should the bank be ordered to pay. The case will be heard at the supreme court on the 7th March 2008. A provision of RWF 92m has been made in respect of this case.

iii) OPROVIA- RWF 30,073,339

Oprovia, a parastatal, claimed that two fraudulent withdrawals were made from their account during the war. The company sued the bank and the court of First Instance issued a judgement against the bank due to a lack of evidence, to pay RWF 30,073,733.Both parties appealed against this judgment. At the appeal stage the court confirmed the upheld the first judgement. In the meantime, the evidence has now been found and the case will be heard in the Supreme Court.

3 2

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007.

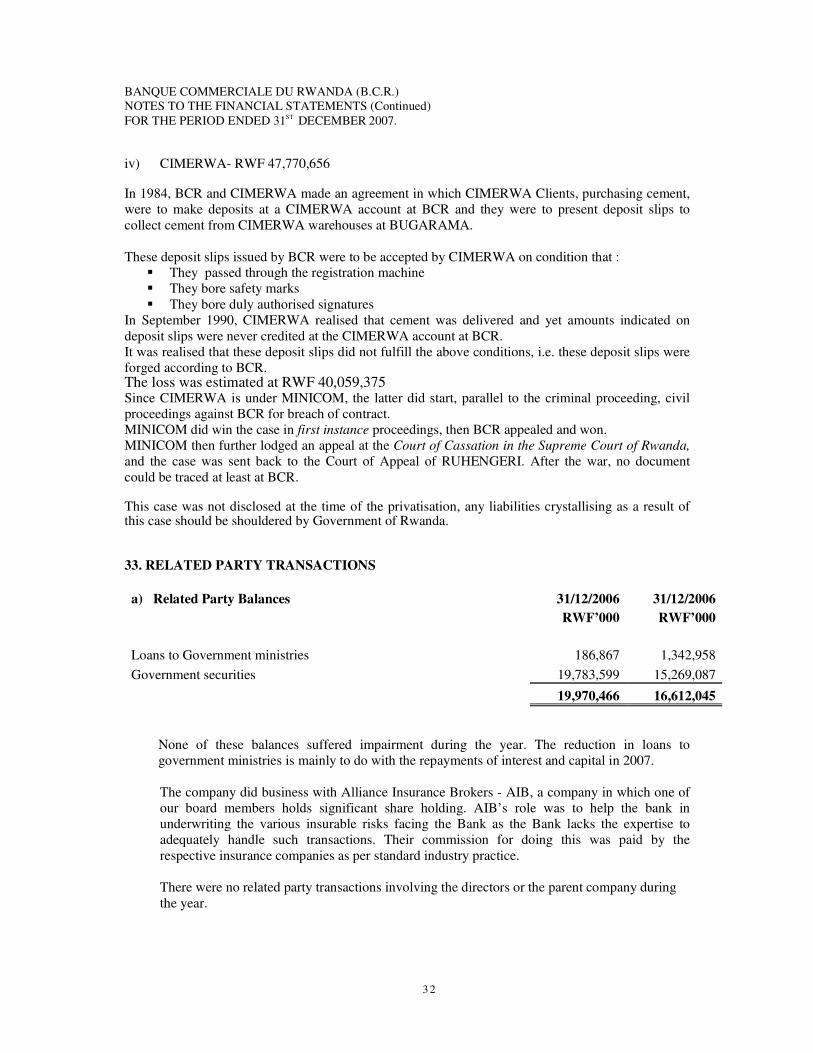

iv) CIMERWA- RWF 47,770,656

In 1984, BCR and CIMERWA made an agreement in which CIMERWA Clients, purchasing cement, were to make deposits at a CIMERWA account at BCR and they were to present deposit slips to collect cement from CIMERWA warehouses at BUGARAMA. These deposit slips issued by BCR were to be accepted by CIMERWA on condition that :

� They passed through the registration machine � They bore safety marks � They bore duly authorised signatures

In September 1990, CIMERWA realised that cement was delivered and yet amounts indicated on deposit slips were never credited at the CIMERWA account at BCR. It was realised that these deposit slips did not fulfill the above conditions, i.e. these deposit slips were forged according to BCR. The loss was estimated at RWF 40,059,375 Since CIMERWA is under MINICOM, the latter did start, parallel to the criminal proceeding, civil proceedings against BCR for breach of contract. MINICOM did win the case in first instance proceedings, then BCR appealed and won. MINICOM then further lodged an appeal at the Court of Cassation in the Supreme Court of Rwanda, and the case was sent back to the Court of Appeal of RUHENGERI. After the war, no document could be traced at least at BCR. This case was not disclosed at the time of the privatisation, any liabilities crystallising as a result of this case should be shouldered by Government of Rwanda. 33. RELATED PARTY TRANSACTIONS a) Related Party Balances 31/12/2006 31/12/2006 RWF’000 RWF’000 Loans to Government ministries 186,867 1,342,958 Government securities 19,783,599 15,269,087

19,970,466 16,612,045

None of these balances suffered impairment during the year. The reduction in loans to government ministries is mainly to do with the repayments of interest and capital in 2007.

The company did business with Alliance Insurance Brokers - AIB, a company in which one of our board members holds significant share holding. AIB’s role was to help the bank in underwriting the various insurable risks facing the Bank as the Bank lacks the expertise to adequately handle such transactions. Their commission for doing this was paid by the respective insurance companies as per standard industry practice. There were no related party transactions involving the directors or the parent company during the year.

3 3

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007.

b) Directors Remuneration

A listing of the members of the Board of Directors is shown on page 4. The total remuneration of the directors during the year amounted to Frw 104,319,488 (2006- Rwf 83,282,638).

34. SEGMENT INFORMATION Business segments: A business segment is a group of assets and operations engaged in providing products or services that are subject to risks and returns that are different that are different from those of other business segments. The bank’s main business is provision of corporate and retail services. Income from the bank’s core business accounts for more than 90% of its total income. There are therefore no material distinct business segments to necessitate detailed disclosures. Geographical segments: A geographical segment is engaged in providing products or services within a particular economic environment services that are subject to risks and returns that are different from those operating in other economic environments. All the bank’s branches operate within Rwanda, and are controlled from the head office in Kigali. Owing to this, no further disclosures have been made on the basis of the geographical spread of the scheme.

35. RISK MANAGEMENT POLICIES

Banking by its nature entails a wide array of risks. The bank’s financial risk management objectives are as outlined below:

a) Credit Risk Management:

Credit risk arises when customers or counterparties are not able to fulfill their contractual obligations.

The bank’s credit – granting standards and credit monitoring process are as follows: � The bank has prudent written lending policies, loan approval and administration

procedures, and appropriate loan documentation essential to a bank’s management of the lending function.

� The board determines the extent to which the bank makes its credit decisions free of conflicting interests and inappropriate pressure from outside parties.

� There’s a well developed process for continuous monitoring of credit relationships including the financial condition of borrowers, a key element of any condition of the loan portfolio, including internal loan grading and classification.

� The bank adheres to adequate policies, practices and procedures for evaluating the quality of assets and adequate loan loss provisions and loss reserves.

3 4

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007.

� The bank periodically reviews individual credits, asset classification and provisioning of loans. The bank has a process in place for overseeing problem credits and collecting past due loans.

� The bank has a mechanism in place for continually assessing the strength of these guarantees and appraising the value of the collateral for advances.

� The bank properly records and holds adequate capital against off-balance sheet exposures when they retain contingent risks.

� Transactions with related parties that pose special risks to the bank are usually

subject to the approval of the bank’s board of directors, or prohibited all together.

b) Interest Rate Risk Management: � The bank is exposed to the risk that the value of financial instruments will

fluctuate due to changes in market interest rate. � The board of directors is regularly informed of the interest risk exposure of the

bank in order to assess the monitoring and controlling of such risk against the boards’ guidance on the levels of risk that are acceptable by the bank

� Senior management ensures that the structure of the bank’s business and the level of interest rate risk it assumes are effectively managed, that appropriate policies and procedures are established to control and limit these risks and that resources are available for evaluating and controlling interest rate risks.

� The bank tries to identify the risks inherent in new products and activities and ensures that these are subject to adequate procedures and controls before being introduced or undertaken.

d) Liquidity Management

� Liquidity management is to ensure that the bank is able to meet fully its

contractual commitments. It’s the ability to fund increases in assets and meet obligations as they come due.

� The bank has an agreed strategy for the day-to-day management of liquidity. This strategy is communicated to the management committee.

� The bank’s board of directors approves the strategy and significant policies related to the management of liquidity, the board also ensures that the senior management takes the steps necessary to monitor and control liquidity

� The board is regularly informed of the liquidity situation of the bank and immediately if there are any material changes in bank’s current or prospective liquidity position.

� Senior management ensures that liquidity is effectively managed, and that the appropriate policies and procedures are established to control and limit liquidity risk.

� The bank systematically measures, monitors, controls, and reports liquidity risk. Reports are provided on a timely basis to the bank’s board of directors, senior management and other appropriate personnel.

e) Operational Risk Management

� Operational risk involves breakdowns in internal controls and corporate

governance. Such breakdowns can lead to financial losses through error or failure to perform in a timely manner or cause the interest of the bank to be compromised in some way.

3 5

BANQUE COMMERCIALE DU RWANDA (B.C.R.) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE PERIOD ENDED 31ST DECEMBER 2007.

� The board of directors ensures that the bank’s operational risk framework is subject to effective and comprehensive internal audit by operationally independent, appropriately trained and competent staff. The internal audit ensures that all operational risks are properly managed.

e) Operational Risk Management (continued)

� Senior management ensures that all levels of staff understand their responsibilities

with respect to operational risk management, and that there are procedures for managing operational risk in all of the bank’s material products, activities, processes and systems

f) Legal Risk

This can include the risk that the assets will turn out to be worth less or liabilities will turn out to be greater than expected because of inadequate or incorrect legal advice or documentation. In addition, existing laws may fail to resolve legal issues involving a bank. The bank has employed a legal advisor to constantly manage the related risks.

g) Reputation Risk

This arises from operational failures, failures to comply with relevant laws and regulations, or other sources. Reputation risk is particularly damaging for banks thus the management tries to maintain the confidence of staff, depositors, creditors and general market place.

3 6

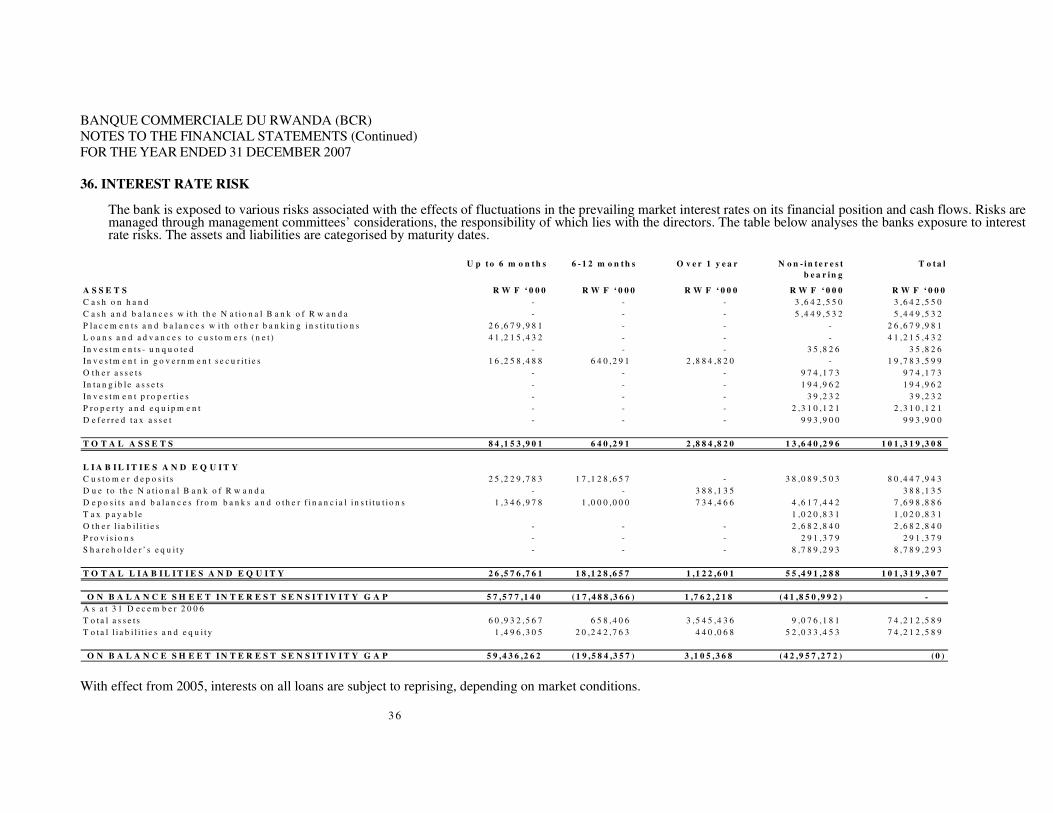

BANQUE COMMERCIALE DU RWANDA (BCR) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE YEAR ENDED 31 DECEMBER 2007 36. INTEREST RATE RISK

The bank is exposed to various risks associated with the effects of fluctuations in the prevailing market interest rates on its financial position and cash flows. Risks are managed through management committees’ considerations, the responsibility of which lies with the directors. The table below analyses the banks exposure to interest rate risks. The assets and liabilities are categorised by maturity dates.

U p t o 6 m o n t h s 6 - 1 2 m o n t h s O v e r 1 y e a r N o n - in t e r e s t

b e a r in gT o t a l

A S S E T S R W F ‘ 0 0 0 R W F ‘ 0 0 0 R W F ‘ 0 0 0 R W F ‘ 0 0 0 R W F ‘ 0 0 0C a s h o n h a n d - - - 3 ,6 4 2 ,5 5 0 3 ,6 4 2 ,5 5 0 C a s h a n d b a l a n c e s w i th t h e N a t io n a l B a n k o f R w a n d a - - - 5 ,4 4 9 ,5 3 2 5 ,4 4 9 ,5 3 2 P l a c e m e n t s a n d b a l a n c e s w i th o th e r b a n k in g i n s t i tu t i o n s 2 6 ,6 7 9 ,9 8 1 - - - 2 6 ,6 7 9 ,9 8 1 L o a n s a n d a d v a n c e s t o c u s to m e r s ( n e t ) 4 1 ,2 1 5 ,4 3 2 - - - 4 1 ,2 1 5 ,4 3 2 In v e s tm e n t s - u n q u o te d - - - 3 5 ,8 2 6 3 5 ,8 2 6 In v e s tm e n t in g o v e r n m e n t s e c u r i t i e s 1 6 ,2 5 8 ,4 8 8 6 4 0 ,2 9 1 2 ,8 8 4 ,8 2 0 - 1 9 ,7 8 3 ,5 9 9 O th e r a s s e t s - - - 9 7 4 ,1 7 3 9 7 4 ,1 7 3 In t a n g ib l e a s s e t s - - - 1 9 4 ,9 6 2 1 9 4 ,9 6 2 In v e s tm e n t p r o p e r t i e s - - - 3 9 ,2 3 2 3 9 ,2 3 2 P r o p e r ty a n d e q u ip m e n t - - - 2 ,3 1 0 ,1 2 1 2 ,3 1 0 ,1 2 1 D e f e r r e d t a x a s s e t - - - 9 9 3 ,9 0 0 9 9 3 ,9 0 0

T O T A L A S S E T S 8 4 ,1 5 3 ,9 0 1 6 4 0 ,2 9 1 2 ,8 8 4 ,8 2 0 1 3 ,6 4 0 ,2 9 6 1 0 1 ,3 1 9 ,3 0 8

L I A B I L I T I E S A N D E Q U I T YC u s to m e r d e p o s i t s 2 5 ,2 2 9 ,7 8 3 1 7 ,1 2 8 ,6 5 7 - 3 8 ,0 8 9 ,5 0 3 8 0 ,4 4 7 ,9 4 3 D u e to t h e N a t io n a l B a n k o f R w a n d a - - 3 8 8 ,1 3 5 3 8 8 ,1 3 5 D e p o s i t s a n d b a l a n c e s f r o m b a n k s a n d o th e r f i n a n c i a l i n s t i t u t i o n s 1 ,3 4 6 ,9 7 8 1 ,0 0 0 ,0 0 0 7 3 4 ,4 6 6 4 ,6 1 7 ,4 4 2 7 ,6 9 8 ,8 8 6 T a x p a y a b le 1 ,0 2 0 ,8 3 1 1 ,0 2 0 ,8 3 1 O th e r l ia b i l i t i e s - - - 2 ,6 8 2 ,8 4 0 2 ,6 8 2 ,8 4 0 P r o v i s io n s - - - 2 9 1 ,3 7 9 2 9 1 ,3 7 9 S h a r e h o ld e r ’ s e q u i ty - - - 8 ,7 8 9 ,2 9 3 8 ,7 8 9 ,2 9 3

T O T A L L I A B I L I T I E S A N D E Q U I T Y 2 6 ,5 7 6 ,7 6 1 1 8 ,1 2 8 ,6 5 7 1 ,1 2 2 ,6 0 1 5 5 ,4 9 1 ,2 8 8 1 0 1 ,3 1 9 ,3 0 7

O N B A L A N C E S H E E T I N T E R E S T S E N S I T I V I T Y G A P 5 7 ,5 7 7 ,1 4 0 ( 1 7 ,4 8 8 ,3 6 6 ) 1 ,7 6 2 ,2 1 8 ( 4 1 ,8 5 0 ,9 9 2 ) - A s a t 3 1 D e c e m b e r 2 0 0 6T o ta l a s s e t s 6 0 ,9 3 2 ,5 6 7 6 5 8 ,4 0 6 3 ,5 4 5 ,4 3 6 9 ,0 7 6 ,1 8 1 7 4 ,2 1 2 ,5 8 9 T o ta l l i a b i l i t i e s a n d e q u i ty 1 ,4 9 6 ,3 0 5 2 0 ,2 4 2 ,7 6 3 4 4 0 ,0 6 8 5 2 ,0 3 3 ,4 5 3 7 4 ,2 1 2 ,5 8 9

O N B A L A N C E S H E E T I N T E R E S T S E N S I T I V I T Y G A P 5 9 ,4 3 6 ,2 6 2 ( 1 9 ,5 8 4 ,3 5 7 ) 3 ,1 0 5 ,3 6 8 ( 4 2 ,9 5 7 ,2 7 2 ) ( 0 ) With effect from 2005, interests on all loans are subject to reprising, depending on market conditions.

3 7

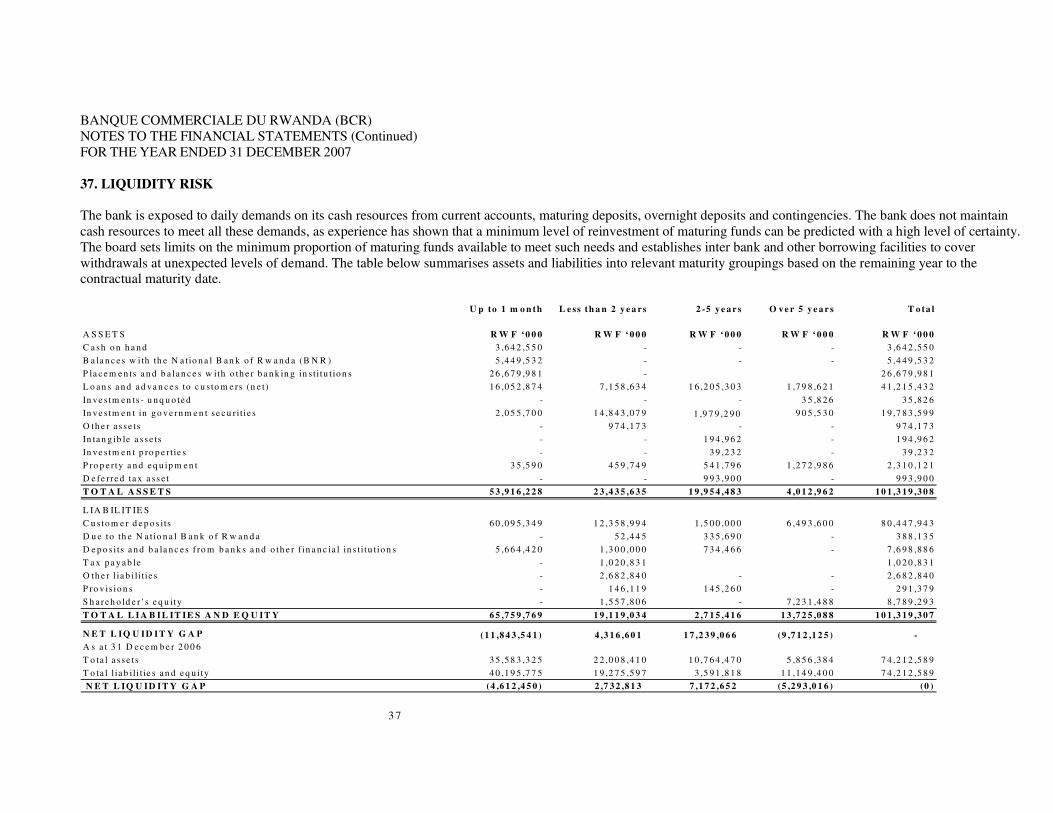

BANQUE COMMERCIALE DU RWANDA (BCR) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE YEAR ENDED 31 DECEMBER 2007 37. LIQUIDITY RISK The bank is exposed to daily demands on its cash resources from current accounts, maturing deposits, overnight deposits and contingencies. The bank does not maintain cash resources to meet all these demands, as experience has shown that a minimum level of reinvestment of maturing funds can be predicted with a high level of certainty. The board sets limits on the minimum proportion of maturing funds available to meet such needs and establishes inter bank and other borrowing facilities to cover withdrawals at unexpected levels of demand. The table below summarises assets and liabilities into relevant maturity groupings based on the remaining year to the contractual maturity date.

U p to 1 m o n th L e ss th a n 2 y e a r s 2 -5 y e a r s O v e r 5 y e a r s T o ta l

A S S E T S R W F ‘0 0 0 R W F ‘0 0 0 R W F ‘0 0 0 R W F ‘0 0 0 R W F ‘0 0 0C a sh o n h a n d 3 ,6 4 2 ,5 5 0 - - - 3 ,6 4 2 ,5 5 0 B a la n c e s w i th th e N a tio n a l B a n k o f R w a n d a (B N R ) 5 ,4 4 9 ,5 3 2 - - - 5 ,4 4 9 ,5 3 2 P la c e m e n ts a n d b a la n c e s w ith o th e r b a n k in g in s titu t io n s 2 6 ,6 7 9 ,9 8 1 - 2 6 ,6 7 9 ,9 8 1 L o a n s a n d a d va n c e s to c u s to m e rs (n e t) 1 6 ,0 5 2 ,8 7 4 7 ,1 5 8 ,6 3 4 1 6 ,2 0 5 ,3 0 3 1 ,7 9 8 ,6 2 1 4 1 ,2 1 5 ,4 3 2 In ve s tm e n ts - u n q u o te d - - - 3 5 ,8 2 6 3 5 ,8 2 6 In ve s tm e n t in go v e rn m e n t se c u ritie s 2 ,0 5 5 ,7 0 0 1 4 ,8 4 3 ,0 7 9 1 ,9 7 9 ,2 9 0 9 0 5 ,5 3 0 1 9 ,7 8 3 ,5 9 9 O th e r a s se ts - 9 7 4 ,1 7 3 - - 9 7 4 ,1 7 3 In ta n g ib le a ss e ts - - 1 9 4 ,9 6 2 - 1 9 4 ,9 6 2 In ve s tm e n t p ro p e rtie s - - 3 9 ,2 3 2 - 3 9 ,2 3 2 P ro p e rty a n d e q u ip m e n t 3 5 ,5 9 0 4 5 9 ,7 4 9 5 4 1 ,7 9 6 1 ,2 7 2 ,9 8 6 2 ,3 1 0 ,1 2 1 D e fe rre d ta x a ss e t - - 9 9 3 ,9 0 0 - 9 9 3 ,9 0 0 T O T A L A S S E T S 5 3 ,9 1 6 ,2 2 8 2 3 ,4 3 5 ,6 3 5 1 9 ,9 5 4 ,4 8 3 4 ,0 1 2 ,9 6 2 1 0 1 ,3 1 9 ,3 0 8

L IA B IL IT IE SC u s to m e r d e p o s its 6 0 ,0 9 5 ,3 4 9 1 2 ,3 5 8 ,9 9 4 1 ,5 0 0 ,0 0 0 6 ,4 9 3 ,6 0 0 8 0 ,4 4 7 ,9 4 3 D u e to th e N a t io n a l B a n k o f R w a n d a - 5 2 ,4 4 5 3 3 5 ,6 9 0 - 3 8 8 ,1 3 5 D e p o s i ts a n d b a la n c e s f ro m b a n k s a n d o th e r f in a n c ia l in s titu tio n s 5 ,6 6 4 ,4 2 0 1 ,3 0 0 ,0 0 0 7 3 4 ,4 6 6 - 7 ,6 9 8 ,8 8 6 T a x p a y a b le - 1 ,0 2 0 ,8 3 1 1 ,0 2 0 ,8 3 1 O th e r lia b i li t ie s - 2 ,6 8 2 ,8 4 0 - - 2 ,6 8 2 ,8 4 0 P ro v is io n s - 1 4 6 ,1 1 9 1 4 5 ,2 6 0 - 2 9 1 ,3 7 9 S h a re h o ld e r’s e q u ity - 1 ,5 5 7 ,8 0 6 - 7 ,2 3 1 ,4 8 8 8 ,7 8 9 ,2 9 3 T O T A L L I A B I L IT IE S A N D E Q U IT Y 6 5 ,7 5 9 ,7 6 9 1 9 ,1 1 9 ,0 3 4 2 ,7 1 5 ,4 1 6 1 3 ,7 2 5 ,0 8 8 1 0 1 ,3 1 9 ,3 0 7

N E T L IQ U ID I T Y G A P (1 1 ,8 4 3 ,5 4 1 ) 4 ,3 1 6 ,6 0 1 1 7 ,2 3 9 ,0 6 6 (9 ,7 1 2 ,1 2 5 ) - A s a t 3 1 D e c e m b e r 2 0 0 6T o ta l a ss e ts 3 5 ,5 8 3 ,3 2 5 2 2 ,0 0 8 ,4 1 0 1 0 ,7 6 4 ,4 7 0 5 ,8 5 6 ,3 8 4 7 4 ,2 1 2 ,5 8 9 T o ta l l ia b ili t ie s a n d e q u ity 4 0 ,1 9 5 ,7 7 5 1 9 ,2 7 5 ,5 9 7 3 ,5 9 1 ,8 1 8 1 1 ,1 4 9 ,4 0 0 7 4 ,2 1 2 ,5 8 9 N E T L IQ U ID I T Y G A P (4 ,6 1 2 ,4 5 0 ) 2 ,7 3 2 ,8 1 3 7 ,1 7 2 ,6 5 2 (5 ,2 9 3 ,0 1 6 ) (0 )

3 8

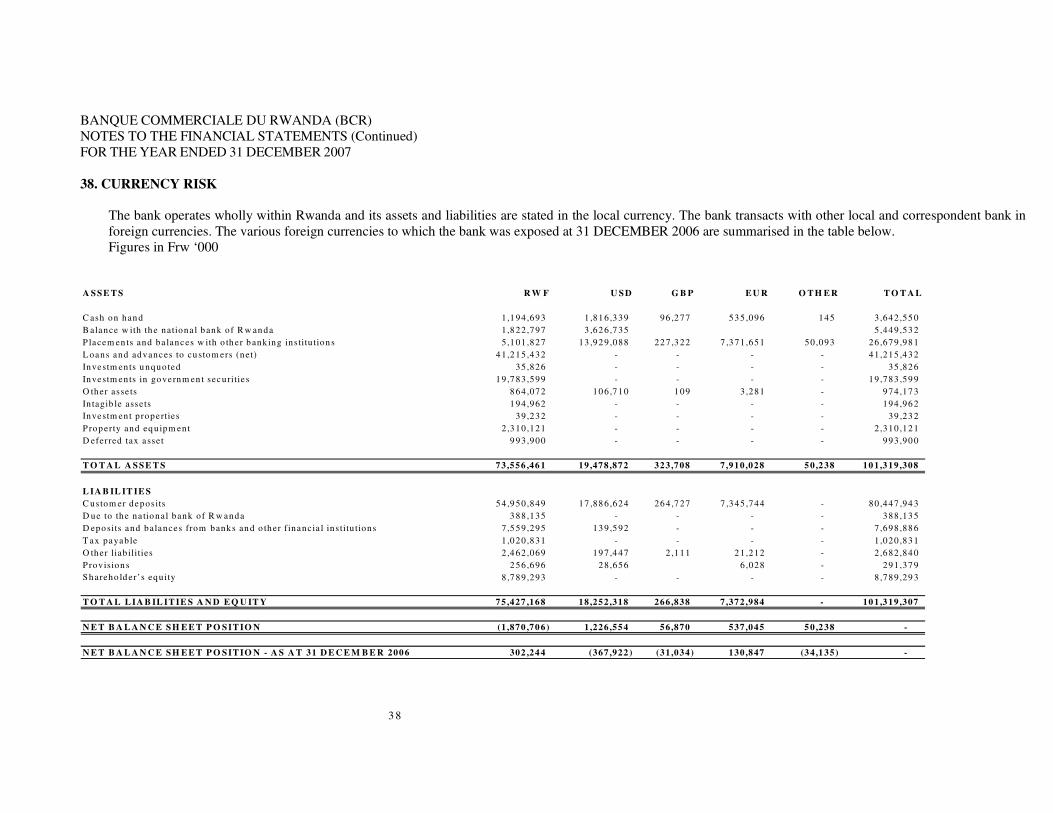

BANQUE COMMERCIALE DU RWANDA (BCR) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE YEAR ENDED 31 DECEMBER 2007 38. CURRENCY RISK

The bank operates wholly within Rwanda and its assets and liabilities are stated in the local currency. The bank transacts with other local and correspondent bank in foreign currencies. The various foreign currencies to which the bank was exposed at 31 DECEMBER 2006 are summarised in the table below. Figures in Frw ‘000

A S S E T S R W F U S D G B P E U R O T H E R T O T A L

C ash on han d 1 ,1 94 ,693 1 ,81 6 ,3 39 96 ,2 77 53 5 ,096 145 3 ,642 ,55 0 B alance w ith th e nationa l b ank of R w an da 1 ,8 22 ,797 3 ,62 6 ,7 35 5 ,449 ,53 2 P lacem en ts and ba lances w ith o th er b anking institu tion s 5 ,1 01 ,827 13 ,92 9 ,088 22 7 ,3 22 7 ,3 71 ,651 50 ,093 26 ,679 ,98 1 L oans and advances to cu stom ers (net) 4 1 ,2 15 ,432 - - - - 41 ,215 ,43 2 Investm ents u nquoted 35 ,826 - - - - 35 ,82 6 Investm ents in go vernm en t securitie s 1 9 ,7 83 ,599 - - - - 19 ,783 ,59 9 O ther asse ts 8 64 ,072 10 6 ,7 10 1 09 3 ,281 - 974 ,17 3 In tagib le assets 1 94 ,962 - - - - 194 ,96 2 Investm ent p roperties 39 ,232 - - - - 39 ,23 2 P rop erty and eq uipm ent 2 ,3 10 ,121 - - - - 2 ,310 ,12 1 D eferred tax asset 9 93 ,900 - - - - 993 ,90 0

T O T A L A S S E T S 73,556 ,46 1 19 ,478 ,872 323 ,708 7 ,910 ,028 5 0 ,2 38 10 1 ,3 19 ,308

L IA B IL IT IE SC ustom er deposits 5 4 ,9 50 ,849 17 ,88 6 ,624 26 4 ,7 27 7 ,3 45 ,744 - 80 ,447 ,94 3 D ue to the na tio nal bank of R w anda 3 88 ,135 - - - - 388 ,13 5 D epo sits and balances from banks an d o ther financia l ins titu tions 7 ,5 59 ,295 13 9 ,5 92 - - - 7 ,698 ,88 6 T ax payable 1 ,0 20 ,831 - - - - 1 ,020 ,83 1 O ther liab ilities 2 ,4 62 ,069 19 7 ,4 47 2 ,1 11 2 1 ,212 - 2 ,682 ,84 0 P rov ision s 2 56 ,696 2 8 ,656 6 ,028 - 291 ,37 9 S h areho ld er’s equ ity 8 ,7 89 ,293 - - - - 8 ,789 ,29 3

T O T A L L IA B IL IT IE S A N D E Q U IT Y 75,427 ,16 8 18 ,252 ,318 266 ,838 7 ,372 ,984 - 10 1 ,3 19 ,307

N E T B A L A N C E S H E E T P O S IT IO N (1,870 ,70 6) 1 ,226 ,554 56 ,870 537 ,045 5 0 ,2 38 -

N E T B A L A N C E S H E E T P O S IT IO N - A S A T 31 D E C E M B E R 200 6 302 ,24 4 (367 ,922 ) (31 ,034) 130 ,847 (3 4 ,1 35) -

3 9

BANQUE COMMERCIALE DU RWANDA (BCR) NOTES TO THE FINANCIAL STATEMENTS (Continued) FOR THE YEAR ENDED 31 DECEMBER 2007 39. FAIR VALUES The carrying values of financial assets and liabilities are not significantly different from their fair values. Carrying values have been revised for all known cases of impairment.

40. EVENTS AFTER THE BALANCE SHEET DATE In January 2008, BCR issued a corporate bond with a nominal value of RWF 5bn. The notes already issued under the program have been listed on the Rwanda over the counter (OTC) market. 41. CURRENCY

The financial statements are presented in thousands of Rwandan Francs (Rwf ‘000).