abc bank - tunisia rapport annuel annual … · les produits financiers islamiques suscitent un...

TRANSCRIPT

2012ABC BANK - TUNISIA

ANNUAL REPORT

COLLABORATION

RAPPORT ANNUEL

4

5

6

8

10

12

14

16

24

26

28

38

41

57

58

59

Notre Groupe /

Notre Engagement /

La Lettre du Président du Conseil d'Administration /

Le Conseil d'Administration /

Chiffres Clés 2012 /

Le Mot du Management /

La Conjoncture Economique Nationale /

Rétrospective de l'Exercice 2012 /

Gouvernance d’Entreprise /

Les Normes Prudentielles de Gestion du Risque /

Développement et Organisation /

Rapport Général des Commissaires aux Comptes /

Etats Financiers /

Extraits des Résolutions de l’Assemblée Générale /

Les Agences ABC-Tunisie /

Le Réseau International ABC /

Our Group

Our Vision

Letter from the Chairman

Board of Directors

Financial Highlights 2012

Managing Director’s Statement

National Economic Outlook

Business Review 2012

Corporate Governance

Prudential Standards and Risk Management

Development and Organization

Independent Auditors' General Report

Financial Statements

Extract from the Ordinary General Assembly Resolutions

ABC-Tunisie branches

ABC Group Directory

SOMMAIRE / CONTENTS

collaboration

ABC Tunisia is building strongrelationships. Productive

teamwork among our employeesand close collaboration with clients

are providing resilience.

Amphithéâtre d’El Jem (Tunisie) / Colosseum of El jem (Tunisia)

coopération

ABC Tunisie privilégie desrelations de partenariat solides.La performance de nos équipes

de travail associée à une coopération étroite avec nosclients assurent notre force.

Steadfast guidance takes us closer to our goals. Clear strategic direction, backed by solid leadership, is being rewarded by stronger relationships

leadership

reliability

Relentless application of our strategy is setting ABC Algeria apart. We are gaining recognition for growing our network and strengthening the quality of our offering.

- Jordan

- Algeria

ABC Egypt has been resolute in the face of uncertainty. Intelligent navigation of the challenges we face is

- Egypt

Notre Groupe / Our Group Notre Engagement / Our Vision

cxcnjas dncbduo muspi merol aisinuT - knaB CBA

- Tunisie

IslamicInternational Jordan

Group Algeria Egypt

Devenir la banque Universelle de référence dans la région MENA qui assure un solide rendement à ses actionnaires et apporte une forte valeur ajoutée à ses clients, tout en attirant, valorisant et fidélisant ses meilleurs éléments.

To become a leading Universal Bank in MENA that delivers superior shareholder returns, provides distinctive services and products to its customers, and is able to attract, develop and top talent.

Le Siège d’ABC-Tunisie aux Berges du Lac (Tunis) / ABC-Tunisie Head Office, in Les Berges du Lac (Tunis)

ABC BANK - TUNISIA4 | ANNUAL REPORT 2012 5

La confiance, la cohérence et la fiabilité sont trois valeurs inestimables pour une Banque. Aux yeux de nos clients, ABC International Bank possède chacune d'entre elles, ce qui explique son statut de partenaire privilégié.

Trustworthiness, consistency and reliability are three invaluable qualities for a bank. In the eyes of our clients, ABC international bank possesses all of them, which is why they make us a preferred partner.

leadership

fiabilité

L'exécution rigoureuse de notre stratégie distingue ABC-Algérie. Notre renommée est acquise avec l'extension de notre réseau et l'amélioration de la qualité de nos services.

Grâce à son esprit d'entreprise, ABC-Jordan est devenue une banque locale réputée et respectée auprès des Entreprises et des Particuliers.La poursuite d'opportunités dans le cadre d'une approche prudente, pour éviter les risques, a stimulé la croissance.

Through its entrepreneurialism, ABC Jordan has become a respected local corporate and retail bank. Skilled pursuit of opportunities, backed by careful avoidance of risks, has fuelled growth.

diligence

créativité

diligence

creativity

détermination

empowerment

determination

empowerment

ABC-Egypt est restée ferme et résolue dans un contexte d'incertitude. Un pilotage intelligent face aux défis confrontés nous guide vers une rentabilité croissance.

Les produits financiers islamiques suscitent un intérêt considérable et croissant. ABC Islamic Bank permet aux Particuliers et aux Entreprises de concilier leurs convictions religieuses avec leurs objectifs financiers.

Demand for Islamic financial products is huge and growing. ABC Islamic Bank gives people and corporate the opportunity to match their religious beliefs and financial goals.

Avoir un management dévouénous rapproche de nos objectifs.Une orientation stratégique claire, soutenue par un leadership constructif et efficace, est récompensée par des relations plus fortes avec nos clients et le succès financier.

La Lettre du Présidentdu Conseil d'Administration

Letter from the Chairman

ABC BANK - TUNISIA6 | ANNUAL REPORT 2012 7

Le "Printemps Tunisien" - précurseur des " printemps arabes " - continue de soulever l'intérêt des observateurs et d'attirer la sympathie des pays amis.

Au niveau économique, les résultats enregistrés en 2012 sont encourageants si l'on prend en considération la conjoncture difficile dans les pays voisins, le marasme dans l'Union Européenne. Ajouter à cela, les intempéries de l'hiver au nord-ouest de la Tunisie qui n'ont pas facilité la tâche du Gouvernement de la Troïka, et ont exacerbé les revendications légitimes mais parfois exagérées des couches sociales défavorisées.

Avec un taux de croissance du PIB de 3,6% en 2012 et des perspectives d'avenir poussant à l'optimisme de l'avis d'institutions financières internationales, nombre d'experts estiment que la Tunisie peut mieux faire, ses fondamentaux sont gérables. Le mal dont souffre son économie est foncièrement politique ainsi qu'il appert des rapports d'agences internationales de notation.

Les autorités tunisiennes, les acteurs économiques et la société civile en sont conscients et réalisent que le manque de visibilité relativement à la stabilité politique et à la paix sociale incite les investisseurs à la prudence et à l'attentisme et freine le rythme de la relance de l'activité économique.

Aussi des voix s'élèvent-elles tant dans la majorité au pouvoir que dans l'opposition pour réclamer l'adoption d'urgence d'un programme consensuel avec un calendrier pour rétablir la sécurité et la confiance, faciliter la relance, réaliser les échéances électorales et mettre fin à la présente phase transitoire du processus de démocratisation.

La Tunisie peut compter sur ses amis tant parmi ses partenaires stratégiques qu'auprès des institutions financières internationales pour réussir sa transition. Il y a un sentiment largement répandu inspiré de propos attribués à Hannibal aux termes desquels " la Tunisie trouvera le chemin menant à son but ou prendra une autre voie pour y arriver ". C'est dire que la confiance est grande en ce pays.

Je ne vais pas m'étaler davantage sur ce sujet. Je laisse au Management, auquel il me plait de réitérer la confiance du Conseil d'Administration, de nous éclairer sur l'activité de notre Banque en 2012.

Je saisis cette occasion pour remercier l'ensemble du personnel d'ABC-Tunisie et renouveler aux Autorités Monétaires tunisiennes, l'expression de notre haute considération et notre reconnaissance pour le soutien qu'elles ont toujours manifesté à l'égard de notre Institution.

The Tunisian Spring which became the catalyst for the wider Arab Spring continues to raise the interest of observers and friendly sympathy of countries.

At the economic level, the results registered in 2012 are encouraging if we take into account the difficult situation in neighboring countries and the slump in the European Union. Adding to that, the adverse winter weather conditions in the Northwest of Tunisia which did not facilitate the task of the ruling Troika Government, and which exacerbated the legitimate claims - although sometimes difficult to content - of socially disadvantaged people.

With a GDP growth rate of 3.6% in 2012 and prospects pushing for optimism in the opinion of international financial institutions, many experts believe that Tunisia can do better and that its fundamentals are manageable. The main problem afflicting the country's economy is inherently political, as it appears from reports by international rating agencies.

The Tunisian authorities along with the economic operators and civil society are well aware of the situation and realize that the lack of visibility into the political stability and social peace encourages investors to be cautious and wait, while it equally slows down the pace of recovery for the economic activity.

Also voices are rising among the ruling majority and the opposition calling for the urgent adoption of a consensual program with a timetable to restore security and trust throughout the country, facilitate recovery, organize the widely anticipated upcoming elections and bring to a close the transitional phase of democratization.

For its successful transition, Tunisia can count on his friends as much among its strategic partners as among international financial institutions. There is a widespread feeling inspired by comments attributed to Hannibal under which "Tunisia will find the path leading to its goal or take a different route to get there." This summarizes how high the degree of confidence is in Tunisia.

I shall not dwell on the subject any further. I leave it to the General Management - to which it pleases me to reiterate the confidence of the Board of Directors - to shed light on the activities of our Bank in 2012.

I take this opportunity to thank all staff members of ABC in Tunisia for their hard work, loyalty and dedication. I would also like to express our highest consideration and appreciation to the Tunisian Monetary Authorities for their continuous support and the guidance they have always demonstrated towardsour institution.

Tunis, Mars / March 2013

Alexander Ashton

Mr. Alexander Ashton, Président du Conseil d’Administration / Chairman of the Board of Directors

Le Conseil d’AdministrationBoard of Directors

ABC BANK - TUNISIA8 | ANNUAL REPORT 2012 9

Président du Conseild’Administration / Chairman Président du Conseild’Administration / Chairman

RC, CG, CC Mr. Alexander Ashton Vice-Président / Deputy ChairmanVice-Président / Deputy Chairman

AC, GC Mr. Sami Bengharsa

Administrateur / Board Member Administrateur / Board Member

AC, CC, GC Mr. Elie Touma Administrateur / Board Member Administrateur / Board Member

AC, RC, GC Mr. Jawad Sacre

Administrateur / Board Member Administrateur / Board Member

RC, CC, GC Mr. Zied Jalali Administrateur / Board Member Administrateur / Board Member

CC Mr. Ali Kooli

Secrétaire du Conseil /Secretary of the BoardSecrétaire du Conseil /Secretary of the Board

Mr. Ismail Mokhtar

du Comité d'AuditAC Membre Member of the Audit Committee

du de CréditComité CC Membre Member of the Credit Committee

RC Membre du Comité des RisquesMember of the Risk Committee

GC Membre du Comité de Nomination et de CompensationMember of the Nomination and Compensation Committee

CONSTITUTION DU CONSEIL D'ADMINISTRATION COMPOSITION OF THE BOARD OF DIRECTORS

Les membres du Conseil d'Administration représentent les intérêts des actionnaires du Groupe Arab Banking Corporation et sont appelés à fixer les objectifs de rentabilité en cohérence avec le maintien de la solidité financière de l'établissement bancaire.

Le Conseil d'Administration de Arab Banking Corporation Tunisie est constitué de six membres :

Members of the Board of Directors represent the interests of shareholders of the Arab Banking Corporation Group and are expected to set targets for profitability consistent with maintaining the financial soundness of the bank.

The Board of Directors of Arab Banking Corporation - Tunisie consists of six members :

Deputy Chief Executive Officer, ABC International Bank - London Mr. Alexander Ashton Mai / May 2013

Mai / May 2013

Mai / May 2013

Mai / May 2013

Mai / May 2013

Mai / May 2013

General Manager ABC International Bank - ParisMr. Sami Bengharsa

Vice-President Project and Structured Finance ABC (BSC) - BahrainMr. Zied Jalali

Vice-President Remadial Loan Unit ABC (BSC) - BahrainMr. Jawad Sacre

Vice-President Retail Banking ABC (BSC) - BahrainMr. Elie Touma

Managing Director and Chief Executive Officer ABC - TunisieMr. Ali Kooli

Mandat / Mandate

ACTIONNARIAT ABC-TUNISIE SHAREHOLDERS OF ABC-TUNISIEABC-Tunisie est détenue en majeure partie par sa maison mère, l'Arab Banking Corporation (BSC) avec une participation de 99,99% au capital. Le détail de l'actionnariat est présenté dans le tableau ci-dessous.

ABC-Tunisie is owned mainly by its parent company Arab Banking Corporation (BSC) with a 99.99% stake in its capital. Details of the ownership are provided in the below table.

Arab Banking Corporation BSC

Boronia Holding LimitedKavita Investments LimitedShereen Investments LimitedVarner Holdings LimitedWepton Properties LimitedArab Co-operation for Financial Investments

Total

4 990 400 100

100100100100100

5 000 000

1000 10001000100010001000

5 000 000

99,9880%

0,0020%0,0020%0,0020%0,0020%0,0020%0,0020%

100%

4 990 400

Actionnaires / Holder Nombre d’actions/Quantity of Shares

Valeurs Nominales/Nominal Value

%

Fonction / Function

ABC BANK - TUNISIA10 | ANNUAL REPORT 2012

Chiffres clés 2012Financial Highlights 2012

ACTIVITE /

RESULTATS /

FONDS PROPRES /

RATIOS FINANCIERS /

RATIOS RÉGLEMENTAIRES /

EFFECTIF ET NOMBRE D'AGENCES /

ACTIVITY

INCOME

NETWORTH

FINANCIAL RATIOS [%]

REGULATORY RATIOS [%]

STAFF AND BRANCHES

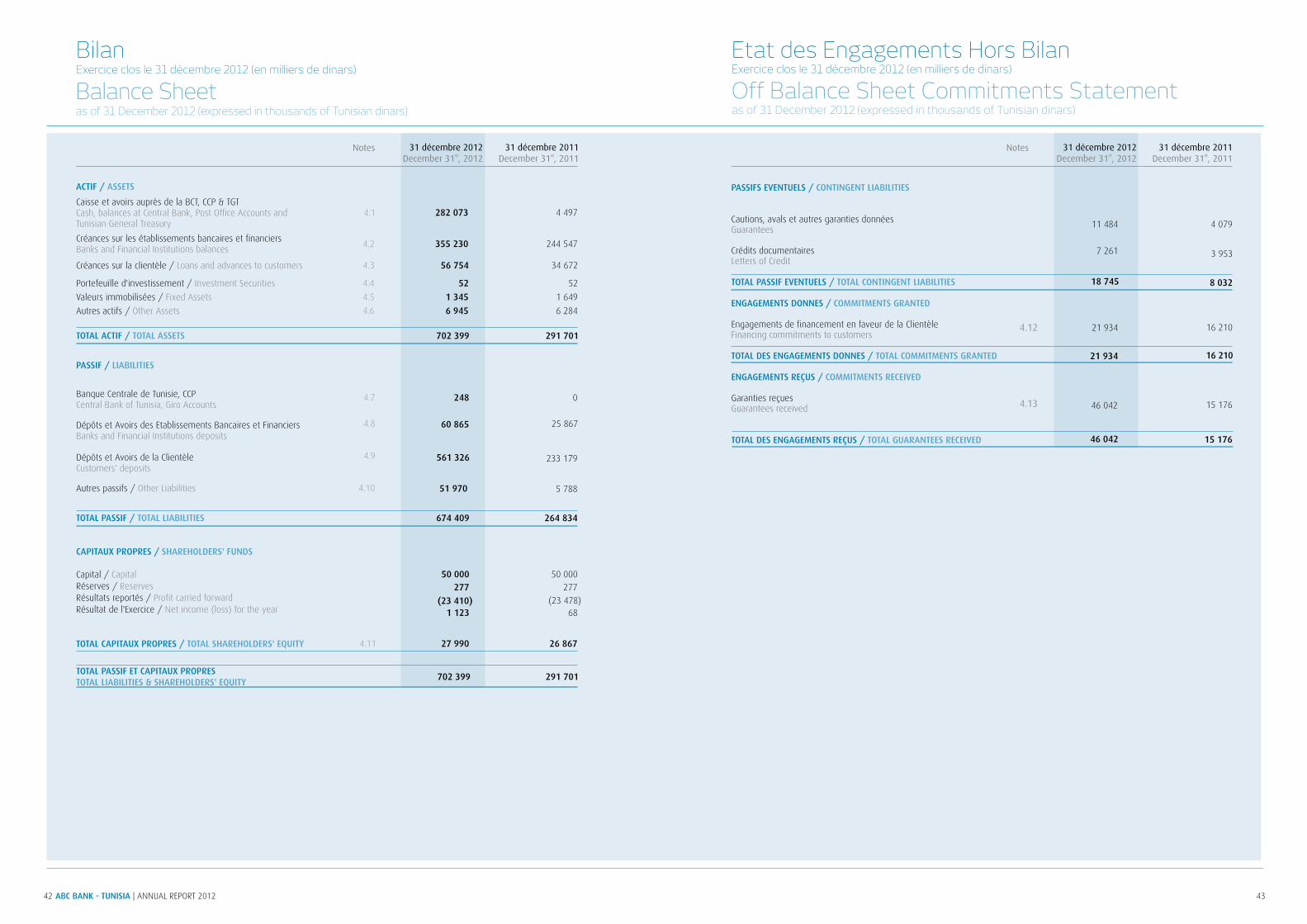

Total Bilan /

Dépôts Clientèle /

Crédits Clientèle /

Marge d'intermédiation /

Commissions /

Produit Net Bancaire /

Frais Généraux /

Résultat Brut d'Exploitation /

Résultat Net /

Fonds Propres Nets /

[Total Crédits Directs / Total Bilan] /

[Total Crédits Directs / Total Dépôts Clientèle] /

[PNB / Total Bilan] /

[PNB / Capitaux Propres] /

Ratio de Couverture des Risques /

Ratio de Liquidité /

Ratio de Solvabilité /

Ratio d'Immobilisation /

Effectif Permanent /

Nombre d'Agences /

Total Assets

Customer Deposits

Customer Loans

Net Interest Margin

Net Fees & Commissions

Total Income

General Operating Expenses

Operating Profit (loss)

Net profit or (Loss)

Networth

[Total Loans and Advances / Total Assets]

Total Loans and Advances / Total Customer deposits]

[Total Income / Total Assets]

[Total income / Shareholders' Equity]

Capital Adequacy Ratio

Liquidity Ratio

Solvency Ratio

Fixed Asset Ratio

Staff

Branches

[In TND,000*]

* Sauf indication contraire / unless stated otherwise

702 399

561 326

56 754

2012

4 893

4 501

9 394

7 982

1 975

1 123

8.1

10.1

1.3

33.6

22.22

155.46

4.0

4.8

1036

27 990

291 701

233 179

34 672

2011

3 850

3 372

7 222

7 117

751

68

11.9

14.9

2.5

26.9

26.5

161.46

9.26.1

936

26 867

90

4

2010

239 040

188 193

25 806

3 200

2 967

6 167

6 535

203

1 251

26 799

10.8

13.7

2.7

23.0

27.14

158.3

11.2

4.2

90

4

2009

225 028171 999

25 141

2 3961 984

4 380

6 165

(1 216)

(1 618)

25 548

11.2

14.6

1.9

17.1

41.5

175.6

11.4

7.7

903

2008

240 884

166 516

46 539

3 524

2 134

5 657

6 422

(217)

1 330

17 166

19.3

27.9

2.4

33.0

28.7

167.9

7.1

12.6

Mr. Sami Bengharsa De gauche à droite / : Mr. Zied Jalali, From left

11

ABC BANK - TUNISIA12 | ANNUAL REPORT 2012

Le Mot du Directeur GénéralManaging Director’s Statement

Ali Kooli

Mr. Ali Kooli, Managing Director & CEO of ABC-TunisieTunis, Mars / March 2013

Dans le Rapport Annuel 2011, il est mentionné qu'il y a en Tunisie, "des prémices annonciatrices de la reprise du tourisme et de l'activité économique avec une bonne campagne agricole en perspective ".

Concernant le bilan d'ABC-Tunisie, il y est indiqué que " tous les postes sont en progression et pratiquement positifs - les perspectives pour 2012 seront dans la même ligne ".

Les résultats de l'Exercice sous examen confortent et confirment ces pronostics. Ils sont conformes au degré de la relance des activités qui est restée en deçà des possibilités du pays.

Il faut reconnaître qu'en 2012, "les affaires roulaient au ralenti " et l'économie était à la recherche d'un second souffle dans une conjoncture endogène et exogène morose avec en prime des liquidités insuffisantes sur le marché bancaire. Insuffisance nécessitant des injections répétées de la part de la Banque Centrale de Tunisie, ce qui a accéléré l'inflation. Pour juguler cette dernière, des mesures ont été prises pour restreindre le crédit à la consommation. Elles ont eu l'effet contre productif, de freiner la production, moteur de la reprise recherchée.

ABC-Tunisie a su s'accommoder de cette situation, s'adapter à la forte concurrence, consolider l'acquis réalisé en 2011 et renouer avec le cycle de la croissance continue.

Parmi les performances enregistrées en 2012, il y a lieu de relever que malgré l'augmentation de l'effectif permanent du personnel de plus de 10% par rapport à 2011 et nonobstant les augmentations salariales consécutives aux négociations sociales entre syndicat, le gouvernement et le patronat tunisiens, le renchérissement du coût de la vie et l'inflation, les dépenses d'exploitation de ABC-Tunisie ont évolué au même rythme que l'année passée ce qui laisse entendre une compression substantielle de ces frais.

Quant aux autres éléments du bilan, ils dénotent une gestion et une base saines de la banque. L'activité dans son double volet Dépôts et Crédits et le Résultat Net sont positifs avec des niveaux largement supérieurs à ceux des années précédentes.

Les perspectives pour 2013 sont sujettes aux aléas du calendrier politique. A priori, et en prenant en considération les déclarations de hauts dirigeants d'institutions financières internationales, la Tunisie est en mesure de réussir la présente phase post-révolutionnaire et la relance économique mesurée de 2012 sera poursuivie à un rythme quelque peu supérieur.

ABC-Tunisie sera, comme par le passé, à l'écoute de sa clientèle qui est en expansion et ne ménagera pas ses efforts pour lui apporter le soutien qu'elle mérite et contribuer ainsi à la réalisation de ses projets.

In the 2011 Annual Report, it is mentioned that there are in Tunisia, sources announcing a recovery in the tourism industry and a revival in economic activity with a good agricultural season in perspective.

Concerning the balance sheet of ABC-Tunisie, it is stated that all positions are following an upward trend and practically positive - the outlook for 2012 will be right in line.

The results of the year under review support and validate these predictions. They are consistent with the degree of re-launch of economic activities which remained below the country's potential.

It must be recognized that in 2012, "business was slow" and the economy was in search of catching its breath in a sluggish environment to which was added the bonus of insufficient liquidity in the banking market. Insufficiency which required repeated injections from the Central Bank of Tunisia, and had the side effect of accelerating inflation. In order to curb the price increases, measures have been taken to restrict consumer credit. These measures had the side effect of restraining production - key driver for the economic recovery sought.

ABC-Tunisie has been able to accommodate with this situation, adapt to the fierce competition, consolidate the achievements made in 2011 and resume high growth.

Among the performances recorded in 2012, it should be noted that despite the increase in the bank's permanent staff by more than 10% compared to 2011, and notwithstanding the subsequent salary increases which were negotiated between trade unions, the Government and Tunisian business representatives, the rising cost of living and inflation, the operating expenses of ABC-Tunisie have evolved at the same pace than last year, which suggests a substantial compression of these costs.

As for the other items of the balance sheet, they denote a sound management and strong foundation. The bank's activity in terms of, both Deposits and Credits, and the Net result are positive reaching levels well above those recorded in previous years.

The forecasts for 2013 are subject to the vagaries of the political agenda. Taking into account the statements made by senior leaders of international financial institutions, Tunisia is able to pass this present post-revolutionary stage and the measured economic recovery recorded in 2012 will be sustained at a somewhat higher rate.

As it has been doing in the past, ABC-Tunisie will continue to listen to the needs of its client base which is rapidly expanding. The bank will spare no effort to provide the support its clients deserve and thereby contribute to the achievement of their projects.

13

ABC BANK - TUNISIA14 | ANNUAL REPORT 2012

La ConjonctureEconomique Nationale

National Economic Outlook

L'économie tunisienne a renoué en 2012 avec la croissance et retrouvé sa résilience après le choc de 2011 consécutif à la révolution.

En effet, nonobstant une conjoncture difficile à l'échelle nationale ou régionale, notamment au sein de l'Union européenne - partenaire majeur et traditionnel de la Tunisie - le PIB a cru de 3,6%n un taux supérieur aux prévisions qui étaient au niveau de 3,5%.

Cette croissance a été générée principalement par les secteurs du tourisme et services, l'agro-alimentaire et l'industrie manufacturière. Elle a eu des effets bénéfiques sur l'emploi où il a été enregistré la création de près de 100.000 emplois. L'inflation a été stabilisée au niveau moyen annuel de 5,6%. Cette croissance a eu également son impact sur les exportations qui ont augmenté de 5,8% par rapport à 2011.

En outre, les perspectives pour 2013 et 2014 confortent la volonté de maintenir et de soutenir la reprise enregistrée en 2012 et tablent sur des taux de croissance respectivement de 4,5% et 5,2%.

Il est un fait que les performances mentionnées ci-dessus sont en deçà des promesses faites par la Troïka pendant la campagne électorale de 2011 ainsi que des attentes des zones géographiques et couches de la population touchées par le chômage et la marginalisation.

Ces résultats ne donnent pas, non plus, le confort nécessaire à nombre d'investisseurs et à des agences internationales de notation qui restent soucieux de l'instabilité politique et du manque de visibilité quant à la date des prochaines échéances électorales et la fin de la présente phase de transition démocratique.

Des experts estiment que le pays est en mesure de réaliser des performances meilleures en considérant ses propres ressources humaines et matérielles ainsi que le soutien dont il jouit auprès de nombreux pays frères et amis et des institutions financières internationales.Les fondamentaux, malgré leur fléchissement par rapport à

leur niveau antérieur, restent gérables. Le taux d'endettement par rapport au PIB (44%) est supportable. Les emprunts obligataires lancés sur le marché international avec la garantie des Etats-Unis d'Amérique ou du Japon, et les prêts obtenus de la part d'autres partenaires tels, à titre indicatif et non limitatif, la Banque Africaine de Développement (BAD), la Banque Européenne d'Investissement (BEI), l'Emirat du Qatar, sont des témoignages de crédibilité à l'égard de l'Etat Tunisien dans son processus de transition vers la démocratie.

The Tunisian economy resumed growth in 2012 and confirmed its resilience after the 2011 shock resulting from the Revolution.

Indeed, despite difficult economic conditions at the national and regional level, especially within the European Union - the major and traditional partner of Tunisia - GDP grew by 3.6%, a rate above forecasts which were at the level of 3.5%. This growth was driven mainly by tourism and services, food processing and manufacturing. It had a positive impact on employment where it has recorded the creation of nearly 100,000 jobs. Inflation has stabilized at an annual average rate of 5.6%. This growth has also had its impact on exports, which increased by 5.8% compared to 2011. In addition, the outlook for 2013 and 2014 confirms the aim to maintain and sustain the recovery recorded in 2012 and expects growth rates of respectively 4.5% and 5.2%.

It is a fact that the performances mentioned above fall short of the promises made by the Troika during the 2011 election campaign as well as the expectations from geographical regions and segments of the population affected by unemployment and marginalization.

These results do not give either, the necessary comfort to many investors and international rating agencies which remain concerned about political instability and the lack of visibility as to when the next elections would be held and when the present phase of democratic transition would come to an end. Experts believe that Tunisia is able to achieve a better performance based on its human capital and own material resources, in addition to the support it enjoys from many fraternal and friendly countries, as well as from international financial institutions.

Despite signs of weakening compared to previous levels achieved, the country's fundamentals remain manageable. The debt to GDP ratio (44%) is bearable. The bond issues in the international market with the guarantee of the United States of America or Japan, and the loans obtained from other partners, including but not limited to, the African Development Bank (AfDB) the European Investment Bank (EIB), the Emirate of Qatar, are testimonies of credibility with regards to the Tunisian State, in its transition to democracy.

De gauche à droite / : Mrs. Fatiha Khelifi, Mr. Nabil MehrezFrom left

15

ABC BANK - TUNISIA16 | ANNUAL REPORT 2012

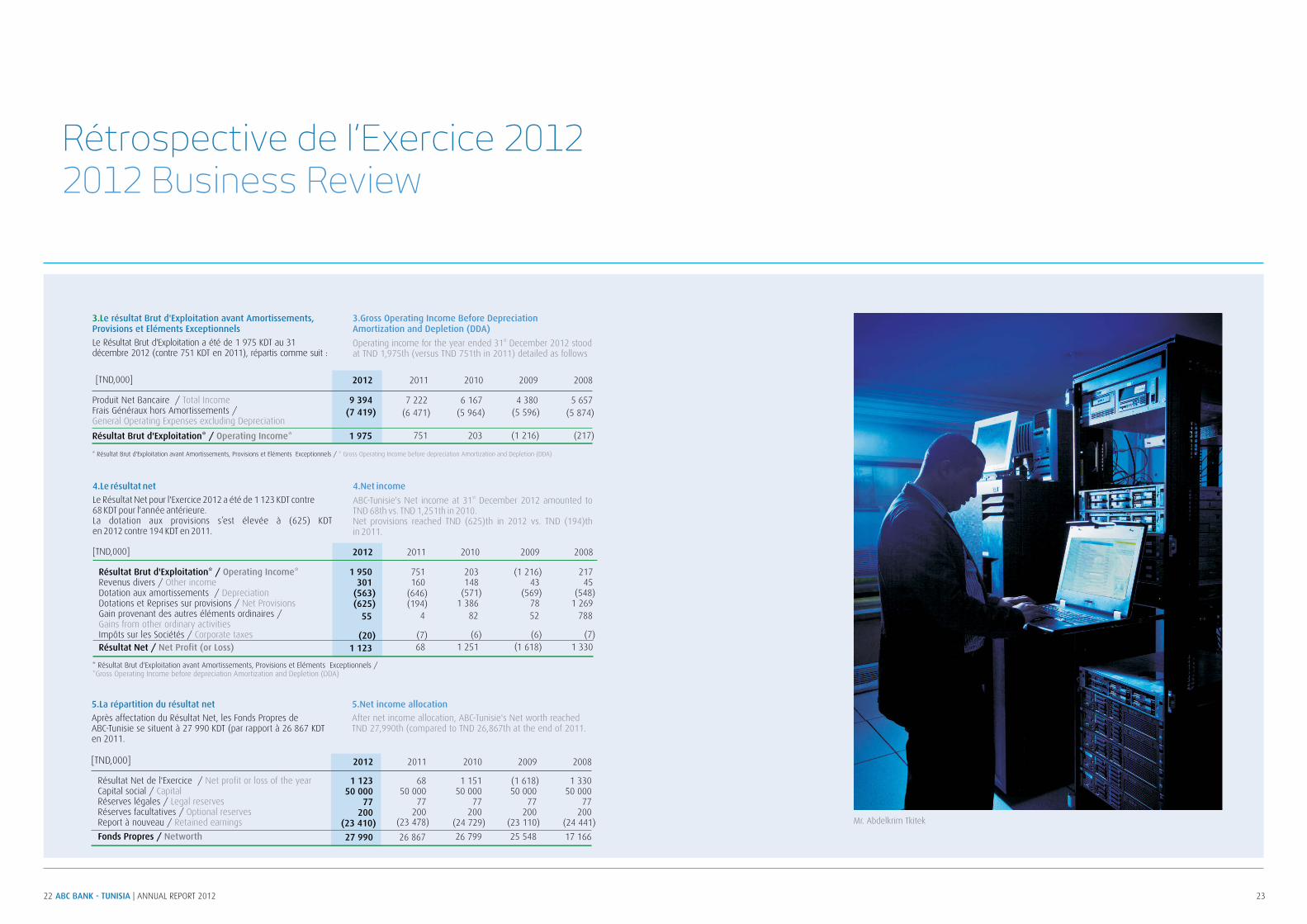

Rétrospective de l’Exercice 20122012 Business Review

1.Les Dépôts de la Clientèle

2.Les Crédits à la Clientèle

Les dépôts collectés auprès de la Clientèle s'élèvent au 31 décembre 2012 à la somme de 561 326 KDT (contre 233 179 KDT en 2011) dont :

519 546 KDT de dépôts à vue (contre 189 732 KDT en 2011) représentant 92,5% de l'ensemble des dépôts (contre 81% en 2011)

8 449 KDT sous forme de dépôts d'épargne (contre 6 626 KDT en 2011) représentant 1,5% des dépôts.

26 172 KDT de dépôts à terme (contre 29 377 KDT en 2011) représentant près de 5% du total des dépôts de la clientèle.

Concernant les dépôts d'épargne, 8 301 KDT (contre 6 483 KDT en 2011) correspondent à des Comptes d'Epargne sur Livretet 148 KDT (contre 143 KDT en 2011) représentent des Comptes Proprio, à savoir des comptes spéciaux d'épargne ouverts dans le cadre d'un plan d'épargne logement afin de bénéficier du CrédiProprio, le crédit conçu par ABC pour l'acquisition d'un logement.

Concernant les dépôts à terme, 6 810 KDT (contre 10 634 KDT en 2011) correspondent à des dépôts en dinars, et un total de 19 362 KDT (contre 18 743 KDT en 2011) représente des dépôts en devises. Les dépôts à terme se répartissent en :

Bons de caisse pour un montant total de 41 KDT (contre 190 KDT en 2011),

Comptes à terme pour un total de 24 631 KDT (contre 27 687 KDT en 2011),

Certificats de dépôts pour un total de 1 500 KDT (1 500 KDT en 2011).

ABC-Tunisie a poursuivi sa politique de financement de l'économie par des crédits destinés essentiellement à faciliter l'activité courante des Entreprises.

Au terme de l'année 2012, le volume des crédits en capitaux s'est situé à la somme de 67 482 KDT (contre 44 319 KDT en 2011). Ces crédits se répartissent comme suit :

2012

%[TND,000] [TND,000] %

2011

Comptes courants débiteurs / Crédit Court Terme Commercial / Crédit Court Terme Financier / Crédit Moyen et Long Terme / Crédits de Consolidation / Impayés /Intérêts courus /

TOTAL (Total brut) /

OverdraftsDiscounts of receivables

Short Term LoansMedium and Long Term Loans

Consolidation Loans Past dues

Accrued Income

TOTAL (Gross amount)

6 6049 862

29 29212 823

4438 232

226

67 482

3 9134 348

13 11013 4292 1717 282

66

44 319

91030305

160

100

10154319

112

0

100

1.Customers' deposits

2.Customers' Loans

On 31 , December 2012, deposits from customers reachedTND 561,326 th (vs. TND 233,179th in 2011). These deposits are mainly composed of the following:

At sight deposits which reached TND 519,546th i.e. representing 92.5% of total customer deposits (compared to TND 189,732th and 81% in 2011).

Savings deposits which reached TND 8,449th (compared to TND 6,626th in 2011), representing 1.5% of Customer deposits.

Term deposits which reached TND 26,172th (vs. TND 29,377 th in 2011) thus representing almost 5% of total Customer deposits (compared to 13% in 2011).

With regards to savings deposits, TND 8,301th (versusTND 6,483th in 2011) represent Booklet Savings accounts and TND 148th (versus TND 143th in 2011) correspond to ABC's Proprio Accounts - a special savings account specifically designed for clients interested in ABC's mortgage (i.e. CrédiProprio).

As regards term deposits, TND 6,810th (compared to TND 10,634th in 2011) correspond to deposits in Tunisian dinars, and TND 19,362th (compared to TND 18,743th in 2011) represent deposits in foreign currencies. Term deposits are split between :

Specific certificate of deposits locally referred to as "Bons de Caisse" which amounted to TND41th (versus TND 190th in 2011),

Time deposits for a volume of TND 24,631th compared to TND 27,687th in 2011, and

Certificates of deposit for a total of TND 1,500th (to TND 1,500th in 2011).

ABC-Tunisie has continued to finance the Tunisian economy through loans essentially designed to facilitate trade finance operations.

stOn 31 December 2012, total gross volume of loans reached TND 67,482th (compared to TND 44,319th in 2011). These loans are composed of the following :

st

Mr. Ikbal Boutabba

17

ABC BANK - TUNISIA18 | ANNUAL REPORT 2012

Rétrospective de l’Exercice 20122012 Business Review

La répartition de ces crédits par segments révèle un volumede 60% (contre 71% en 2011) alloués aux Entreprises et 40% (contre 29% en 2011) aux Particuliers. La part de chacune des Agences de Tunis & centre d'affaires, Sfax, Sousse, Le Belvédère, Mégrine et Ariana dans les concours destinésà la Clientèle a été respectivement de 68%, 9%, 5%, 6%,5% et 7%.

Le tableau suivant détaille la répartition sectorielle des crédits octroyés à la Clientèle.

A closer look into the breakdown of loans per client target shows a 60% allocation to Corporate customers (compared to 71% in 2011) and 40% to Individuals (vs. 29% in 2011). The distribution of loans among the branches shows that Tunis (including the Business Center), Sfax, Sousse, Le Belvédère, Mégrine and Ariana grant respectively 79%; 8%, 5%, 4%, 2% and 2% of total loans to Customers.

The table below shows the sectoral breakdown of bank's exposure in 2012.

2012

%[TND,000] [TND,000] %

2011

Agriculture / AgricultureTélécommunications / Communications

Finance / FinanceInd. Tourisme / Tourism Ind.Ind. Manufacturières / Manufacturing Ind.Commerce / Trade

Transport / TransportParticuliers / Private Individuals

Divers / Others

1222

7 86411 313

1 18027 10820 012

67 482

0000

11.716.8

1.740.229.6

100

457

52

32

05 897

19 239

6 5727 783

4 287

44 319

1.60.10.1

013.343.414.817.69.1

100TOTAL

Les engagements par signature se situent à 40 679 KDT (contre 24 242 KDT en 2011). L'activité liée aux opérations de financement de Commerce Extérieur est essentiellement traitée par l'Unité Off-shore, ABC-Tunis.

Contingent liabilities reached TND 40,679th versus TND 24,242th in 2011. It is worth mentioning that the bulk of foreign trade finance is primarily booked with the Off-Shore Business Unit, ABC-Tunis.

3.Evolution des cours de change

Alors que la transition politique continue de progresser, la Tunisie a entamé l'année 2012 dans une situation difficile de récession accompagnée de troubles intérieurs et dans la région. Malgré des signes de rebondissement de l'activité économique enregistrés au cours du premier semestre, la reprise de l'économie Tunisienne reste toujours timide. Toutefois le potentiel de croissance économique reste favorable à court terme avec la promotion des investissements - clef de la richesse et de l'emploi, mais nécessitant un vrai rétablissement de la situation sécuritaire et politique.

3.FX evolution

While the political transition continues to progress, Tunisia started the year 2012 in a difficult context of recession coupled with internal and external disturbances. Despite signs of rebound in economic activity recorded in the first half of 2012, the recovery of the Tunisian economy remains very timid. Nevertheless, the potential for economic growth remains favorable with the promotion of investments - key to wealth and employment, but requiring a true re-establishment of security and political stability.

La Tunisie aura des défis économiques et sociaux urgents à relever, notamment un taux de chômage élevé (17%), un taux d'inflation de 6 %, la hausse générale des prix, le creusement continu du déficit commercial et des disparités régionales.En vue de parer à l'amplification inflationniste la Banque Centrale de Tunisie a augmenté le taux directeur de 25 Bps le portant de 3,50% à 3,75%, le 29 août 2012.

ABC-Tunisie a continué sa politique de prudence sur le marché local tout en assurant un niveau de liquidité confortable. La banque a continué à placer son excédant de liquidité en devise dans des bons de trésor à un an avec des taux de rendement élevés. En ce qui concerne l'activité de change, le dinar Tunisien s'est déprécié de 5,4% contre l'Euro, 5,6% contre le Dollar américain et 4,9% contre le Yen japonais. Devant cette dépréciation causée essentiellement par l'accélération du rythme des importations, la Banque Centrale de Tunisie a continué son intervention sur le marché de change avec un volume quasi stable comparé à 2011 de 10 milliards de dinars.

Tunisia will be facing economic and social challenges ahead, including a high unemployment rate (17%), an inflation rate of 6%, a general rise in prices, the widening trade deficit and ongoing regional disparities.

In order to counter the inflationary pressures, the Central Bank of Tunisia increased its key lending rate by 25 bps to 3.50% bringing it to 3.75% on 29th August 2012.

ABC-Tunisie has continued its prudent policy on the local market while maintaining a comfortable level of liquidity. The bank continued to place its excess liquidity in foreign currencies in treasury bills of a one-year tenor which generate high yields.

Regarding the Foreign Exchange activity, the Tunisian dinar depreciated by 5.4% against the Euro, 5.6% against the US dollar and 4.9% against the Japanese yen. In front of this impairment which is caused primarily by the accelerated pace of imports, the Central Bank of Tunisia continued its intervention on the Foreign Exchange market with a volume almost stable compared to 2011 at 10 billion dinars.

Mrs. Chédia Bichiou Mr. Sami Bengharsa, Mr. Ismail Mokhtar

19

ABC BANK - TUNISIA20 | ANNUAL REPORT 2012

Rétrospective de l’Exercice 20122012 Business Review

LES RÉSULTATS

1.Le Produit Net Bancaire

Au cours de ce douzième Exercice, les performances réalisées en matière de marge en intérêts et de commissions sur les différents produits et services ABC-Tunisie ont permis de réaliser un PNB de 9 394 KDT contre 7 222 KDT pour l'Exercice antérieur.La Marge d'IntermédiationLa marge en intérêts qui provient de la différence entre le Coût des Ressources et le Rendement des Emplois réalisés a atteint au 31 décembre 2012 la somme de 4 893 KDT soit 52% du PNB (contre 3 850 KDT et 53,3% du PNB en 2011).

PERFORMANCES

1.Total Income

At the end of this twelfth financial year, the performances in terms of Interest Margin and Fees generated a Total Income of TND 9,394th vs TND 7,222th in the previous year.

Interest MarginInterest Margin resulting from the difference between the cost

stof funds and the return on funds reached TND 850th on 31 December 2012 representing 52% of Total Income (compared to 3,850th and 53,3% of Total Income in 2011)

Rendement des Emplois / Crédits à la Clientèle / Placements sur le Marché Monétaire / Coût des Ressources / Ressources Clientèle / Autres Ressources /

Marge d'Intermédiation /

Return on fundsCustomer Loans

Money Market PlacementsCost of funds

Customer resourcesOther resources (Banks and Financial institutions)

Interest margin

[TND,000] 2011

5 3991 2314 168

(1 549)1 233

316

3 850

2010

4 8021 6083 194

(1 602)1 124

478

3 200

2009 20082012

6 8053 9252 880

(1 912)(1 241)

(671)

4 893

4 5582 5422 015

(2 162)(1 732)

(430)

2 396

8 5763 0145 562

(5 052)(4 107)

(945)

3 524

Les CommissionsAu 31 décembre 2012, les commissions nettes bancaires ont atteint la somme de 4 501 KDT soit 48% du PNB (contre3 372 KDT et une proportion de 46,7% en 2011).

Fees and CommissionsstOn 31 December 2012, net banking fees and commissions

reached TND 4,501th (48% of Total Income) compared toTND 3,372th and a proportion of 46,7% in 2011.

[TND,000]

Commissions perçues / Opérations de crédit / Commissions sur comptes / Commissions de gestion & divers / Gains sur portefeuille & opérations financières / Commissions payées /

Commissions nettes /

Fees & commissions collectedCredit operations

Account feesManagement fees & others

Gains on trading securities and financial transactionsFees & commissions paid

Net fees & commissions

20113 542

127241

2 492682

(170)3 372

2012 20103 065

101201

2 764740

(98)2 967

20092 048

48170

1 346484

(64)

1 984

20082 403

56165

1 655527

(269)

2 134

4 794297296

3 206995

(293)

4 501

2.Frais générauxAu cours de l'Exercice 2012, les Frais Généraux se sont élevés à 7 982 KDT (contre 7 117 KDT en 2011). Le tableau ci-après détaille la répartition des Frais Généraux sur les deux Exercices 2011 et 2012.

2.General operating expenses

For the year in review, General Operating Expenses reached TND 7,982th (vs. TND 7,117th in 2011). The table hereafter provides details on the overall breakdown of operating expenses in 2011 and 2012.

2012

4 4342 985

5637 982

2011

3 9282 543

6467 117

2010

3 2502 714

5716 535

2009

3 1402 456

5696 165

2008

3 3072 567

5486 422

[TND,000]

Masse salariale / Dépenses d'exploitation / Amortissements / Frais Généraux /

Personnel expensesOperating expenses

DepreciationGeneral operating expenses

21

Back office Credit

ABC BANK - TUNISIA22 | ANNUAL REPORT 2012

Rétrospective de l’Exercice 20122012 Business Review

4.Le résultat net

Le Résultat Net pour l'Exercice 2012 a été de 1 123 KDT contre68 KDT pour l'année antérieure.La dotation aux provisions s’est élevée à (625) KDTen 2012 contre 194 KDT en 2011.

3.Le résultat Brut d'Exploitation avant Amortissements, Provisions et Eléments Exceptionnels

Le Résultat Brut d'Exploitation a été de 1 975 KDT au 31 décembre 2012 (contre 751 KDT en 2011), répartis comme suit :

4.Net incomestABC-Tunisie's Net income at 31 December 2012 amounted to

TND 68th vs. TND 1,251th in 2010. Net provisions reached TND (625)th in 2012 vs. TND (194)thin 2011.

3.Gross Operating Income Before Depreciation Amortization and Depletion (DDA)

stOperating income for the year ended 31 December 2012 stood at TND 1,975th (versus TND 751th in 2011) detailed as follows

[TND,000] 2011

7 222(6 471)

751

2012

9 394(7 419)

1 975

2010

6 167(5 964)

203

2009

4 380(5 596)

(1 216)

2008

5 657(5 874)

(217)

Produit Net Bancaire / Frais Généraux hors Amortissements /

Résultat Brut d'Exploitation* /

Total Income

General Operating Expenses excluding Depreciation

Operating Income*

* Résultat Brut d'Exploitation avant Amortissements, Provisions et Eléments Exceptionnels / * Gross Operating Income before depreciation Amortization and Depletion (DDA)

[TND,000]

Résultat Brut d'Exploitation* / Revenus divers / Dotation aux amortissements / Dotations et Reprises sur provisions / Gain provenant des autres éléments ordinaires /

Impôts sur les Sociétés / Résultat Net /

Operating Income*Other income

DepreciationNet Provisions

Gains from other ordinary activitiesCorporate taxes

Net Profit (or Loss)

2012

1 950301

(563)(625)

55

(20)1 123

2011

751160

(646)(194)

4

(7)68

2010

203148

(571)1 386

82

(6)1 251

2009

(1 216)43

(569)7852

(6)(1 618)

2008

21745

(548)1 269

788

(7)1 330

* Résultat Brut d'Exploitation avant Amortissements, Provisions et Eléments Exceptionnels / *Gross Operating Income before depreciation Amortization and Depletion (DDA)

5.La répartition du résultat net

Après affectation du Résultat Net, les Fonds Propres deABC-Tunisie se situent à 27 990 KDT (par rapport à 26 867 KDTen 2011.

5.Net income allocation

After net income allocation, ABC-Tunisie's Net worth reached TND 27,990th (compared to TND 26,867th at the end of 2011.

[TND,000]

Résultat Net de l'Exercice / Capital social / Réserves légales / Réserves facultatives / Report à nouveau /

Fonds Propres /

Net profit or loss of the yearCapital

Legal reservesOptional reserves

Retained earnings

Networth

2012

1 12350 000

77200

(23 410)

27 990

2011

6850 000

77200

(23 478)

26 867

2010

1 15150 000

77200

(24 729)

26 799

2009

(1 618)50 000

77200

(23 110)

25 548

2008

1 33050 000

77200

(24 441)

17 166

23

Mr. Abdelkrim Tkitek

ABC BANK - TUNISIA24 | ANNUAL REPORT 2012

Gouvernance d’EntrepriseCorporate Governance

1.Gouvernance & détails de la mise en œuvre

2.Renforcement du système de suivi des opérations

Fort d'une expertise de terrain acquise depuis des années, le Groupe Arab Banking Corporation (BSC) a toujours adhéré aux principes déontologiques obligeant tous les intervenants à agir honnêtement, au mieux des intérêts de ses clients et de l'intégrité du marché. Dans ce cadre, ABC-Tunisie a adhéré aux efforts du Groupe ABC (BSC) depuis 2005. Par ailleurs, conformément à la volonté de la Banque Centrale de Tunisie (BCT) de renforcer la culture de l'éthique et de la bonne gouvernance (Circulaire BCT n°2011-06 relative au renforcement des règles de bonne gouvernance) ABC-Tunisie a poursuivi ses efforts d'amélioration de son système de gouvernance, répondant aux exigences du respect de la déontologie bancaire. Ces efforts ont été matérialisés par des actions concrètes dont :

La création de divers comités qui assistent le Conseil d'Administration dont : le Comité Risque, le Comité Exécutif de Crédits, Comité d'Audit ainsi que le Comité de Gouvernance et de Nomination.

L'établissement d'une Charte de Gouvernance détaillant notamment les rôles et responsabilités des membres du Conseil, les mécanismes d'évaluation des travaux du Conseil et des comités, les règles de gestion des conflits d'intérêts et le fonctionnement des comités. Cette charte a été validée par le Conseil d'Administration.

L'adoption du Code de Conduite Professionnelle validé par le Conseil d'Administration.

L'adoption d'une politique et d'un code de gestion des cadeaux et leurs acceptations par les employés.

La mise en place d'un dispositif d'alerte professionnelle (whistle-blowing) permettant aux employés de dénoncer, sans crainte de représailles, des comportements frauduleux ou contraires à l'éthique.

La prise en charge de nouveaux types de risques tel que: le risque de blanchiment, le risque de réputation, le risque de fraude…

La définition d'une charte liée à l'utilisation de l'outil informatique et à la protection des données à caractère personnel.

La déclaration et l’affirmation des valeurs de la banque afin de promouvoir une culture d'entreprise s'articulant autour des aspects suivants: Honnêteté, Intégrité, Respect de l'individu et responsabilité envers l'ensemble des partenaires.

L’implémentation de la fonction " Conformité ", son rattachement au plus haut niveau du Management et la définition d'une " Politique Conformité " approuvée par le Conseil d'Administration.

Dans le cadre de la lutte anti-blanchiment et afin de palier aux risques accrus, liés particulièrement à son environnement local et

1. Governance and implementation details

2.Strengthening of the operations' monitoring system

Backed by its expertise acquired over the years, the Arab Banking Corporation (B.S.C) Group has always adhered to ethical guidelines requiring all stakeholders to act honestly, fairly and in the best interests of its clients and in the integrity of the market. In this context, ABC-Tunisie acceded to the efforts of the Arab Banking Corporation (BSC) Group since 2005. Furthermore, in accordance with the will of the Central Bank of Tunisia (BCT) to strengthen the culture of ethics and good governance (i.e. BCT Circular nr. 2011-06 on strengthening the rules of good governance), ABC-Tunisie has continued its efforts to improve its system of corporate governance, by complying with the requirements of banking ethics. These efforts have been materialized by concrete actions among which:

The establishment of various committees that assist the Board of Directors including: The Risk Committee, the Credit Committee, the Audit Committee and the Nomination and Compensation Committee.

The establishment of a Governance Charter detailing in particular, the roles and responsibilities of the members of the Board, the assessment processes and policies of works directed by the Board and Committees, the monitoring and management of potential conflicts of interest, along with the administration and running of the Committees. This Charter has been validated by the Board of Directors.

The adoption of an Employee's Code of Professional Conduct validated by the Board of Directors.

The adoption of a Policy and Code of Management relevant to gifts and their acceptance by employees.

The implementation of a whistle-blowing device allowing employees to denounce, without fear of any retaliation, fraudulent or unethical behaviors.

The supervision of new types of risk such as: money laundering risk, reputation risk, fraud...

The definition of a Charter related to the use of the computer tools and the protection of the personal data.

The conveyance and exemplification of the bank's core values based on the following principles: Honesty, Integrity, Respect for the individual and responsibility towards all partners.

The implementation of the function "compliance", its connection with the highest level of Management and the definition of a "compliance policy" approved by the Board of Directors.

In its policy of prevention of money laundering and in order to reinforce its internal means in front of such high risks - related

particularly to its local environment and international - ABC Tunisie has undertaken in 2012 to strengthen and upgrade its system for monitoring and detecting unusual transactions. Indeed, the system used for monitoring operations is an essential element of the framework to fight against money laundering and its effectiveness. In this context:

An assessment of the effectiveness of the existing system has been carried.

An analysis of the risks relevant to geography, customer and service has been made.

The different parameters and filters of the system were reviewed and fine-tuned (including detections thresholds)

New Alert Reports were developed to cover the areas of risk including: transfers involving countries at risk, transactions involving the use of new technologies, "striped volumes" covering a specific period of time, significant accounts' activity...

These improvements are intended to reconcile the commercial development of ABC-Tunisie with minimum standards of transparency and management of risks (including that of money laundering).

international, auxquels doit faire la banque, ABCT a entrepris en 2012 de renforcer et mettre à jour son système de suivi et de détection des opérations inhabituelles. En effet, le système de suivi des opérations est un élément essentiel du système de lutte anti blanchiment et de son efficacité. Dans ce cadre :

Une évaluation de l'efficacité du système existant a été effectuée.

Une analyse des risques notamment risques géographique, client et service a été effectuée.

Les différents paramètres et filtres du système ont été revus et affinés (notamment les seuils de détections)

De nouveaux rapports d'alerte ont été développés pour couvrir les zones de risques notamment : transferts impliquant des pays à risque, transactions impliquant l'utilisation des nouvelles technologies, volumes " agrégés " couvrant une période de temps, comptes à activité importante…

Ces améliorations visent à concilier le développement commercial d'ABC-Tunisie avec des règles minimales de transparence et de gestion des risques (notamment celui du blanchiment).

De gauche à droite / : Miss Emira Tekaïa, Mr. Nizar HannachiFrom left

25

ABC BANK - TUNISIA26 | ANNUAL REPORT 2012

Les Normes Prudentiellesde Gestion du risque

Prudential Standardsand Risk Management

1.Classification et Provisionnement des Créances

2.Les Ratios réglementaires

Les créances classées (Classes 2, 3 et 4) comportant un risque de non recouvrement au sens de la Circulaire BCT n°91-24 s'élèvent à 13 352 KDT (contre 13 203 KDT en 2011), et représentent 19.8% de l'ensemble des engagements bruts en capitaux (contre 29.8% en 2011).

Le montant des provisions sur créances douteuses s'élève à6 406 KDT au 31 décembre 2012 (contre 5 898 KDT en 2011),

Le montant des agios réservés s'élève à 4 186 KDT au 31 décembre 2012 (contre 3 749 KDT en 2011),

Le total de la couverture des créances douteuses en principal et intérêt s'élève à 10 592 KDT (contre 9 647 KDT en 2011), cequi représente 79.3% (contre 73.1% en 2011) des créances classées.

Conformément à la circulaire aux banques n°2012-02, telle que modifiée par les textes subséquents, la banque a constitué au titre de l'exercice 2012 des provisions à caractère généraldites « provisions collectives » sur les engagements courants(classe 0) et ceux nécessitant un suivi particulier (classe 1) pour un montant de 136 KDT.

Le ratio de couverture des Risques pondérés (Ratio Cooke) calculé par le rapport Fonds Propres Nets/Total Risques s'est élevé au 31 décembre 2012 à 22.2 % contre 26.5% en 2011 pour un minimum réglementaire de 8%.

Quant au ratio d'Immobilisation, calculé par le Rapport Immobilisations Nettes / Fonds Propres Nets, il s'est élevé à 4.8% (contre 6.1% en 2011), pour un maximum réglementaire de 75%.

D'autre part, le montant total des risques encourus n'excèdent pas :

Trois fois les Fonds Propres Nets de la Banque pour les Bénéficiaires dont le risque s'élève à 5% ou plus desdits Fonds Propres Nets. Les risques encourus s'élèvent à 88 378 KDT (contre 60 046 KDT en 2011) soit 316% (contre 223% en 2011) des Fonds Propres Nets de la Banque.

Une fois et demie les Fonds Propres Nets de la Banque pour les bénéficiaires dont le risque s'élève à 15% ou plus desdits Fonds Propres Nets. Les risques encourus s'établissent à79 638 KDT (contre 44 563 KDT en 2011), soit 285% (contre 166% en 2011) des Fonds Propres Nets de la Banque.

1.Debt Classification and Funding

2.Regulatory ratios

In accordance with the guidelines given in the Central Bank of Tunisia's Circular No.91-24, classified debts (type B2, B3 and B4) bearing a risk of non recovery amount to TND 13,352th (vs. TND 13,203th in 2011) representing 19.8% of total gross loans (compared to 29.8% in 2011).

The amount of provisions on doubtful loans is TND 6,406th as stof 31 December 2012 (compared to TND 5,898th in 2011).

The amount of reserved interest reaches TND 4,186th as of 31st December 2012 (vs. TND3,749th in 2011).

The total volume of coverage for doubtful loans, in principal and interest, reaches TND 10,592th (vs. TND 9,647th in 2011), which represents 79.3% (vs. 73.1% in 2011) of classified loans.

In accordance with the Circular to banks No. 2012-02, as later amended by the subsequent articles, the Bank constituted in respect of its fiscal year 2012, a volume of general provisions of TND 136th. These provisions, known as 'collective provisions', are relevant to current commitments (i.e. the performing loans with risk category 0) and those requiring special monitoring (i.e. performing loans in risk category 1).

The Capital Adequacy Ratio (Net Capital Funds/Total Risks Weighted) has reached 22.2% at the term of the year 2012 (compared to 26.5% in 2011). Regulatory ratio is a minimum of 8%.

As for the Fixed Asset Ratio (Fixed Assets / Net worth), it has reached 4.8% (compared to 6.1% in 2011) for a maximum authorized ratio of 75%.

stOn the other hand, as of 31 December 2012, the total amount of risk incurred does not exceed:

Three times net capital funds for clients posing a risk reaching 5% or more of the Bank's net capital funds. Risk incurred amount to TND 88,378th (compared to TND 60,046th in 2011). This represents a portion of 316% of the Bank's own net funds, compared to 223% in 2011.

One and a half time the Bank's net capital funds for clients with risk exposure of 15% or more of the Bank's net capital funds. Risk incurred amounts to TND 79,638th (compared to TND 44,563th in 2011) i.e. 285% of the Bank's net capital funds (vs. 166% in 2011).

One time the Bank's net capital funds for any related party to the bank, as defined by the clause No. 23 of LawNo. 2001-65. The risk exposure reaches TND41,627th i.e. 149% of the bank's net own funds.

The ratio accounting for an exposure reaching twenty five percent (25%) of the bank's own funds for one single beneficiary has been exceeded for a number of four business relationships.

Une fois les Fonds Propres Nets de la Banque pour les bénéficiaires ayant des liens avec la banque au sens de l'article 23 de la loi n°2001-65. Les risques encourus s'élèvent à41 627 KDT, soit 149% des fonds propres nets de la Banque.

25% des fonds propres sur un même bénéficiaire, ce ratio a été dépassé, pour quatre relations.

De gauche à droite / : Mrs Olfa Derouiche, Mr. Mohamed BelgacemFrom left

27

ABC BANK - TUNISIA28 | ANNUAL REPORT 2012

Développement et OrganisationDevelopment and Organization

1. LE CAPITAL HUMAIN

StatistiquesABC Tunisie, compte au 31 décembre 2012, 110 employés répartis comme suit :

Contrats à Durée Indéterminée (CDI) et Contrats à Durée Déterminée (CDD) Personnel Titulaire : 97 personnes soit 88% Personnel Contractuel (CDD & SIVP) : 13 personnes soit 12%

1. HUMAN

Statistics

CAPITAL

stOn 31 December 2012, ABC-Tunisie counts 110 employees. Details are provided hereafter:

Indefinite vs. Fixed-term employment contracts

The number of employees benefitting from a permanent employment contract stands at 97, which represents 88% of staff.The number of employees with a fixed-term contract (CDD) or undergoing a professional training to promote their integration into the work sphere (SIVP) stands at 13, which accounts for 12% of the bank's staff.

Cadres et Personnel d’Exécution Personnel Cadre : 88 employés soit 80%Personnel d'Exécution : 22 employés soit 20 %

0%

20%

ExécutionCadres

40%

60%

80%

100%

80%

20%

Nos cadres comptent plus de 70% d'universitaires ce qui prouve l'intérêt que porte la banque pour cette génération prometteuse.

0%

20%

CDDCDI

40%

60%

80%

100%

88%

12%

Contrats d’Emploi / Employment Contracts

Genre / Gender

0[25-35] Plus/Above

de 55 Moins/Less than

de 25 35-45 [ ] 45-55 [ ]

50

Tranches d’âge / ABC Staff

Taux d’encadrement / Managerial staff rate

CDD / Fixed Term Contract

Femmes / Women

Execution / Operations staff

CDI / Indefinite Term Contract

Hommes / Men

Cadres / Executives

Avec un pourcentage de 80 % de cadres,notre banque connaît l'un des taux d'encadrementles plus élevés du secteur

Executives vs. Operational staffBank executives are numbered at 88 or 80% of staffOperational staff includes 22 employees or 20%.

With a managerial staff rate of 80% , ABC-Tunisieregisters one of the highest ratios in the sector.

Men vs. WomenThe population of men employed stands at 65 individuals or 59% of staffThe number of women employed stands at 45. This represents 41% of total staff.

Our staff includes over 70% of university graduates. This demonstrates the level of interest and focus granted by the bank to the new generation.

Hommes et Femmes Personnel Masculin : 65 employés soit 59%Personnel Féminin : 45 employés soit 41%

0%

20%

FemmesHommes

40%

60%

80%

100%

59%

41%

La structure de notre staffABC-Tunisie est une banque à la population jeune ayant un âge moyen de 37 ans, et où 83% de la population est âgée entre 25 à 34 ans.

The structure of our staffABC in Tunis holds a young population whose average age is 37. A proportion of 83% of the bank's staff is aged between 25 and 34 years.

Santé

" Améliorer les conditions de vie au travail : notre Engagement au Quotidien "

ABC Tunisie a porté une attention particulière à l'amélioration des conditions de vie au travail en fournissant un effort au quotidien dans la mise en place d'actions permettant de favoriser l'équilibre personnel et professionnel de ses employés en veillant sur leur bonne santé et leur hygiène et sécurité à travers :

Une campagne annuelle de vaccination contre la grippe saisonnière prise en charge totale par ABCUn bilan de santé annuel pour tout le personnel à travers une batterie d'analyse plus élargie, avec la possibilité pour chaque employé de consulter et de suivre les résultats de son bilan sur internetUne visite périodique accomplie par le médecin de travail pour l'ensemble du personnel

Health

" Improving working conditions at our bank: our daily commitment "

ABC-Tunisie has paid special attention to improving working conditions at the bank by providing on a daily basis a series of actions to promote the personal and professional balance of its employees and to safeguard their health and safety. These actions can be summarized as follows :

An annual vaccination program against seasonal influenza fully taken in charge by ABCAn annual comprehensive health checkup for all employees, with the opportunity given to each for tracking and viewing his medical assessment via Internet.A periodic visit of the Bank's appointed doctor for all of the staff members.

29

Ans/Years

ABC BANK - TUNISIA30 | ANNUAL REPORT 2012

Développement et OrganisationDevelopment and Organization

Formation en 2012 /

Effectif du Service Formation

Effort de formation (en % du temps de travail)

Pourcentage des formations réalisées par des formateurs internes

Pourcentage des formations réalisées par des formateurs externes

Pourcentage d'effectif ayant bénéficié d'une formation dans l'année

Moyenne des heures de formation par stagiaire

Training in 2012

Number of employees in the Training Dept.

Training effort (as a percentage of working time)

Percentage of trainings carried by in-house trainers

Percentage of trainings carried by external trainers

Percentage of employees benefitting from a training during the year

Average number of training hours per trainee

Formation « Soutenir l'investissement dans la Formation : notre Priorité »

Training« Supporting investment in training: Our Priority »

1

30%

80,8%

26,2%

93.33%

33

Projeté vers un avenir meilleur pour ses employés, ABC-Tunisie décide de miser et d'investir dans la formation qui est une démarche très importante permettant d'améliorer et de renforcer les connaissances de ses employés afin de garantir la réussite. Cela explique la réalisation de 1006 heures de formation repartis entre les actions en INTER et les actions en INTRA.

Les formations en INTRA étaient d'ailleurs une priorité de l'année 2012, stratégie adoptée pour faire bénéficier un plus grand nombre de participants.

« Parce que nous avons tous été stagiaire ! »ABC-Tunisie accorde une très grande importance pour l'encadrement des jeunes. En 2012, nous avons accueillis 34 jeunes stagiaires dont 12 ont été encadrés pour l'élaboration de leurs projets de fin d'études " PFE " en les dotant des enseignants et des équipements nécessaires.

Taux d'encadrement des stagiaires : 31%, parmi lesquels, 10% ont élaboré leurs projets de fin d'études sous tutelle des cadres de la banque.

« Aucun de nous ne sait ce que nous savons tous, ensemble »L'année 2012 a été l'année où l'accent a été mis sur " le Team Building" qui signifie: la " construction d'équipe ", c'est un exercice qui permet de renouer avec le lien social et qui a pour objectif de renforcer la cohésion d'équipe, de développer

Aiming towards a better future for its employees, ABC in Tunisia is committed to investing in training. This remains an important step to improving and strengthening the knowledge of its employees and guarantees its success. With this objective in mind, ABC in Tunisia has achieved some 1,006 hours of training including in-house and external trainings.

In-house trainings were set as priority in 2012 - the strategy being pursued is to involve a larger number of participants.

« Because we have all been trainees once! »ABC-Tunisie grants a significant focus on the training of young recruits. In 2012, the bank welcomed 34 young trainees, outof which, 12 were assisted to develop their End of YearProjects (PFE) by providing the relevant tutors and necessary equipment.

The rate of supervision of trainees is estimated at 31%, among which 10% have elaborated their End of Year Projects under the supervision of bank executives.

« None of us knows anymore than we all may know, together »Year 2012 was the year where focus has been made on "Team Building". The exercise helps participants to reconnect with their social ties and aims at strengthening team cohesion, develop professional relationships, and enhance motivation,

des relations professionnelles, d'améliorer la motivation, la communication, l'entraide et la confiance au sein d'une équipe. Il s'agit donc de créer une atmosphère favorable grâce à des activités récréatives, participatives et originales, qui stimulent les individus pour renforcer l'énergie ce qui améliore la productivité d'un groupe de collaborateurs.

L'événement fut un franc succès pour un premier groupe comptant 10 responsables et c'est la raison pour laquelle, nous tenons à organiser une deuxième session durant l'année 2013.

communication, and mutual trust within a team. It is therefore meant to create a favorable atmosphere thanks to recreational, participatory and creative activities which stimulate individuals to strengthen their energy and improve their productivitywithin a group.

The event was a great success for a first group comprising 10 bank executives and this is the reason why a second session would be scheduled in the course of 2013.

De gauche à droite / From left: Miss Fatma Chebbi, Miss Emira Mrad, Mrs. Neïla Ben Achour

31

Mr. Ikbal Boutabba, Mrs. Meriam Ben Achour Kefi,Mrs. Henda Jaziri

ABC BANK - TUNISIA32 | ANNUAL REPORT 2012

Développement et OrganisationDevelopment and Organization

TLC@ABC Tunis

Cette année, a misé sur le développement des talents en réussissant un événement unique TLC1@ABC lors du passage de 28 membres du groupe ABC (12 de l'Algérie, 04 de l'Egypte, 02 de Bahreïn et 10 d’ABC Tunis) qui se sont réunis en Tunisie pour le même objectif celui de transformer l'état d'esprit et les attitudes d'un manager en ceux d'un leader reconnu comme tel par les membres de son équipe. Le but ultime de cette action était donc d'apprendre aux responsables le meilleur d'eux-mêmes au bénéfice de leur organisation et de leurs équipes.

ABC Tunisie en mode « Glocal »

Cette année, grâce aux efforts de l'équipe RH et à une prise de conscience générale du Staff de la Banque, l'ePam a connu une grande réussite avec un taux de participation de 78.5%.Cela a facilité les évaluations et les travaux d'avancement de fin d'année permettant une meilleure visibilité des objectifs fixés à l'avance et leur réalisation.

La banque a conçu de nouveaux formulaires à renseigner, et par l'employé, et par son chef de département. Cette méthode permet de confronter les résultats et faire ressortir toute divergence/écart entre les deux évaluations et d'agir en conséquence.

Cette année, à l'occasion des travaux d'avancement, 68 personnes ont fait l'objet d'une promotion et/ou une augmentation de salaire, ce qui représente 63% de l'effectif total - un taux plus que satisfaisant.

ABC Tunisie : Une Banque à l'écoute de ses Employés ABC Group a mis en place l'enquête annuelle de satisfaction, Annuel Yearly Employee Survey -Yes @ABC .

ABC-Tunisie est à son 3ème exercice consécutif qui a connu cette année un taux de participation massif, soit 85% dont ci après les meilleurs scores :

ABC-Tunisie

" "

TLC@ABC Tunis

This year, ABC in Tunisia has focused on the development of talent by successfully managing a single event "TLC1 @ ABC" during the visit of 28 staff members of the ABC Group (12 from Algeria, 4 from Egypt, 2 from Bahrain and 10 fromABC Tunis) which met in Tunisia with the same purpose, i.e. to transform the mindset and attitudes of a Manager into thoseof a leader as acknowledged by his team. The ultimate goalof this action was therefore to teach participants on thebest of themselves for the benefit of their organization and their teams.

ABC Tunisia « Glocal» mode

This year, thanks to the efforts of the HR team and the employees' wider awareness, the ePam has enjoyed great success with a participation rate of 78.5%.This has facilitated the performance appraisals and work progress of at the end of the year, enabling a better visibility of objectives set in advance and their implementation.

The bank developed of new application forms to fill in, by the employee and his supervisor. This method allows comparing the results and highlighting any discrepancies / gap between the two assessments and acting accordingly.

This year, 68 employees have been promoted and / or have enjoyed a salary increase. This represents 63% of the total workforce which stands at a more than satisfactory level.

ABC Tunisie listens to its employeesABC Group has implemented an annual satisfaction survey :"Annual Yearly Employee Survey - Yes@ABC".

The bank has carried its third consecutive exercise which met a participation rate of 85%. The highest scores are reflected in the table below :

Satisfaction du personnel d'être personnel ABC en Tunisie

Participation du personnel au développement d'ABC en Tunisie

Encadrement et assistance des responsables

Communication interne a augmenté de 8% par rapport à l'année 2011

Conditions de travail améliorées de 16% par rapport à 2011

Overall employee satisfaction

The work I do contributes to the success of ABC in Tunisia

Supervision and guidance of unit/service Heads

Internal communication has improved by 8% compared to 2011

Working conditions improved by 16% compared to 2011

86%

97%

68%

48%

67%

Mr. Alaeddine Alibi

33

ABC BANK - TUNISIA34 | ANNUAL REPORT 2012

Développement et OrganisationDevelopment and Organization

2. Le Système d'Information

Dans un contexte d'accélération du mouvement de concentration bancaire et de concurrence accrue, les transformations métiers résultants des orientations stratégiques prises par ABC Bank nécessitent de faire évoluer les systèmes d'information au regard des nombreuses contraintes imposées par la transformation de l'environnement.

Les systèmes d'information de ABC Bank constituent ainsi un levier pour accélérer et sécuriser la mise en place de solutions évolutives dont les objectifs consistent principalement à :

Rationaliser les systèmes d'information et exploiter les innovations technologiques

Accroître la souplesse et l'intégration des systèmes d'information afin d'assurer une vision globale pour le client de la banque (nature et nombre de transactions, mise à jour en temps réel des positions, produits souscrits, rentabilité…)

Favoriser et optimiser l'utilisation des canaux de distribution

Déployer des applications métiers et plateformes technologiques appropriées aux problématiques d'intégration (intégration front/back office, architectures orientées clients…).

Disposer de systèmes réactifs permettant de traiter de manière performante et sécurisée une volumétrie importante de données au meilleur coût possible.

Permettre un pilotage fin de la performance et des coûts au regard des objectifs stratégiques fixés.

Dans cette perspective d'optimisation et de standardisation des systèmes d'information, dans le seul objectif de suivre lestechnologies les plus avancées dans le domaine des technologies de l'information, ABC Bank se veut un partenaire stratégique et concurrentiel en matière d'évolution et développement.

Au courant de l'année 2012, ABC Bank a su incorporer dans l'environnement des systèmes d'informations une suite d'applications serveur qui permet aux utilisateurs d'accéder aux données de n'importe quelle source et de les combiner afin de créer de puissants rapports d'analyses. L'utilisation de cette application permet une visualisation interactive, une étude concise des données, un partage de l'information à des vitesses extrêmes, et le filtrage des données.

2.The Information System

In a context of acceleration in bank concentration and increased competition, the changes in job positions resulting from strategic directions taken by the Bank have required an upgrade in Information Systems, given the numerous constraints imposed by transformation of the business environment.

The Information Systems of ABC Bank constitute a leverage to accelerate and secure the development of scalable solutions whose main aims are summarized hereafter:

Streamline Information Systems and take advantage of technological innovations

Increase the flexibility and integration of Information Systems in order to ensure a comprehensive vision for the customer (type and number of transactions, update in real-time positions, products purchased, profitability ...)

Promote and optimize the use of distribution channels

Deploy appropriate technological platforms and business applications answering the issues of integration (integration front / back office, customer-oriented templates ...).

Hold reactive systems which may address in an efficientand secure way significant volumes of data at the lowest possible cost.

Allow a fine tuning between performance and costs in line with strategic objectives.

In the perspective of optimization and standardization of Information Systems with the sole purpose of following the most advanced technologies in the field of Information Technology, ABC Bank wants to be a strategic and competitive partner in regards to progress and development.

In the course of year 2012, ABC Bank was able to incorporate in its Information Systems a server application that enables users to access data from any systems source and combine them to create powerful analytical reports. The use of this application allows interactive visualization, a concise review of the data, sharing information at extreme speed, anddata filtering.

Parallèlement à cette infrastructure informatique, ABC Banka réussi le développement d'une suite intégrée de fonctionnalités serveur qui contribue à améliorer l'efficacité de notre prestation en fournissant des fonctionnalités de gestion de contenu et de recherche en entreprise complètes, en accélérant les processus d'entreprise partagés et en facilitant le partage d'informations pour offrir une vision globale de l'entreprise. Sous cette suite ont été développées une multitude d'applications telles que (Gestion des Saisies Arrêts, Gestion des immobilisations, registration automatique des chèques impayés).

Dans le cadre des améliorations des infrastructures informatiques, ABC Bank a entamé un projet de consolidation des équipements et des plateformes d'applications afin d'optimiser et de centraliser la gestion des ressources informatiques.

Along with this IT infrastructure, ABC Bank has successfully managed the development of an integrated system which helps improve the efficiency of the bank's services by providing new features for managing data and obtaining a comprehensive information on an account beneficiary. The system enables accelerated processing of shared data and facilitates the transfer of information to provide a global vision of the client. This system equally allowed the development of a variety of applications such as the Management of Account Seizures, Asset Management, and the Automatic Registration of Check Payment incidents).

As part of the improvements in its IT infrastructure, ABC Bank has initiated a project to consolidate its equipments and application platforms to optimize and centralize the management of IT resources.

De gauche à droite / : Mr. Mehdi Kouki, Miss Ahlem Ben Mekki, Mr. Bilel Gmati, Mrs. Imène Horchani AkroutFrom left

35

ABC BANK - TUNISIA36 | ANNUAL REPORT 2012

Développement et OrganisationDevelopment and Organization

3. Business Development and Marketing

ABC-Tunisie commercial policy mainly targets the following markets:

State-owned EnterprisesSupported by successful syndication deals and the Group's expertise in this field, ABC-Tunisie focused on building stronger ties with state-owned companies, helping them meet challenges and contributing to the realization of their investment projects

Private Companies and GroupsIn accordance with the Credit Policy Group, the Bank has focused its current business with companies operating in industries with high added value. The Bank has in particular focused his intervention in the operations of international trade as well as expansion schemes in bordering markets.

Leasing CompaniesABC-Tunisie's experience in managing bills portfolio of leasing companies has been positive and profitable one. The Bank remains committed to developing its relations with this particular segment, by designing service-tailored solutions to answer their specific needs, and play a more active role in their activity funding.

On another level, ABC Bank Tunisia continued its policy to support the development and expansion of the Tunisian economy by providing credit facilities and its expertise in foreign trade operations and cash / change.

Individuals and ProfessionalsThe retail banking portfolio has grown significantly in 2012. The assets' portfolio size increased by 150% compared to 2011 while the liabilities' net growth was around 36% for the same period. This has also been reflected in a 50% growth of the revenues from this channel.

The bank's commercial offer has lately improved to attract more clients from both the Government and private sectors and from the professionals segment as well.

Year 2013 is expected to show a more diversified product range and an extension in the branch network to make the retail banking contribution to the Bank's overall revenues, a considerable one.

3. Le Développement Commercial et Marketing

La politique de développement commercial d'ABC-Tunisie cible essentiellement les marchés suivants:

Les Entreprises PubliquesVu l'expérience réussie d'un certain nombre de crédits syndiqués et de l'expertise du Groupe ABC en la matière, ABC-Tunisie s'investit de la mission de soutenir les entreprises publiques dans leur développement économique et l'accès au financement pour la réalisation de leurs projets d'investissements.