théorie financière 2004-2005 1. introduction

DESCRIPTION

Théorie Financière 2004-2005 1. Introduction. Professeur André Farber. Organisation du cours. Ouvrages de référence: Brealey, R. and Myers, S. Principle of Corporate Finance 7th ed., McGraw-Hill 2003 Farber,A. Laurent, M-P., Oosterlinck, K., Pirotte, H. (FLOP) Finance - PowerPoint PPT PresentationTRANSCRIPT

Théorie Financière2004-20051. Introduction

Professeur André Farber

Tfin 2004 01 Introduction |2August 23, 2004

Organisation du cours

• Ouvrages de référence:Brealey, R. and Myers, S.

Principle of Corporate Finance7th ed., McGraw-Hill 2003

Farber,A. Laurent, M-P., Oosterlinck, K., Pirotte, H. (FLOP)Finance

Pearson Education, 2004

• Site web: www.ulb.ac.be/cours/solvay/farber• Copie des transparents (PowerPoint)• Glossaire anglais - français• Notes pédagogiques, exercices, anciens examens• Liens vers d’autres sites

• Examen(s)

Tfin 2004 01 Introduction |3August 23, 2004

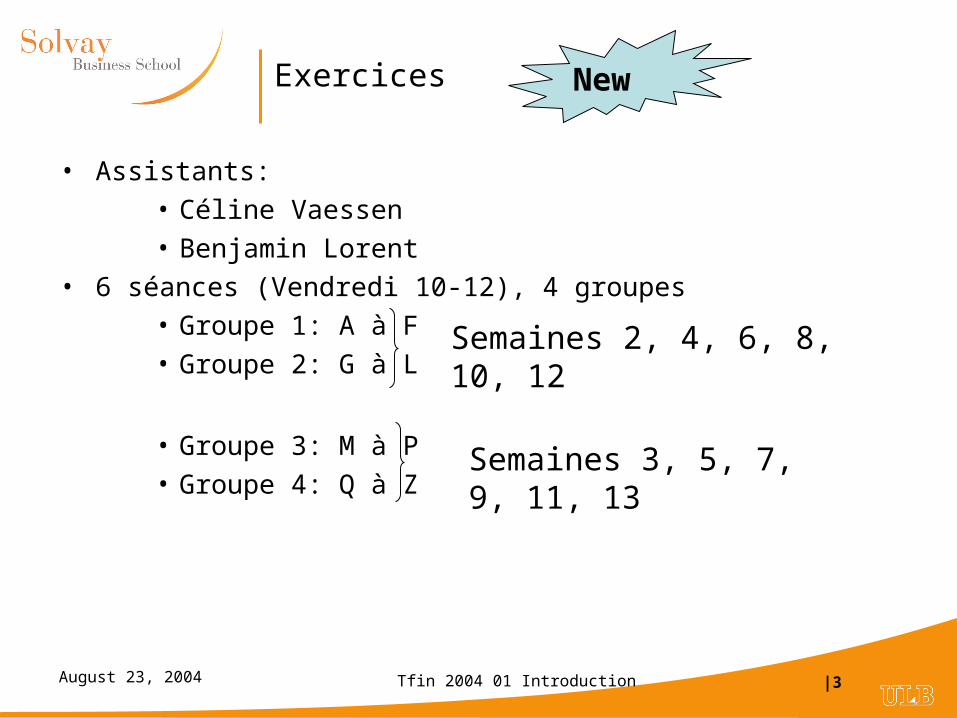

Exercices

• Assistants:

• Céline Vaessen

• Benjamin Lorent

• 6 séances (Vendredi 10-12), 4 groupes

• Groupe 1: A à F

• Groupe 2: G à L

• Groupe 3: M à P

• Groupe 4: Q à Z

New

Semaines 2, 4, 6, 8, 10, 12

Semaines 3, 5, 7, 9, 11, 13

Tfin 2004 01 Introduction |4August 23, 2004

Plan du cours

• 1. Introduction

• 2. Valeur actuelle

• 3. Cash flows, planning financier

• 4. Evaluation d’entreprises

• 5,6. Analyse de projets d’investissement

• 7,8. Rentabilité attendue et risque

• 9,10. Options

• 11, 12. Evaluation et financement

Tfin 2004 01 Introduction |5August 23, 2004

What is Corporate Finance?

• INVESTMENT DECISIONS: Which REAL ASSETS to buy ? • Real assets: will generate future cash flows to the firm

• Intangible assets : R&D, Marketing, ..

• Tangible assets : Real estate, Equipments,..

• Current assets: Inventories, Account receivables,..

• FINANCING DECISIONS: Which FINANCIAL ASSET to sell ?• Financial assets: claims on future cash flows

• Debt: promise to repay a fixed amount

• Equity: residual claim

• DIVIDEND DECISION: How much to return to stockholders?

Tfin 2004 01 Introduction |6August 23, 2004

Accounting View of the Firm

• Balance sheet Income statement

Sales

– Operating expenses

= Earnings before interest and taxes (EBIT)

– Interest expenses

– Taxes

= Net income (earnings after taxes)

• Retained earnings

• Dividend payments

Current assets

Fixed assets

Current liabilites

Long-term debt

Shareholders’ equity

Net Working Capital

Tfin 2004 01 Introduction |7August 23, 2004

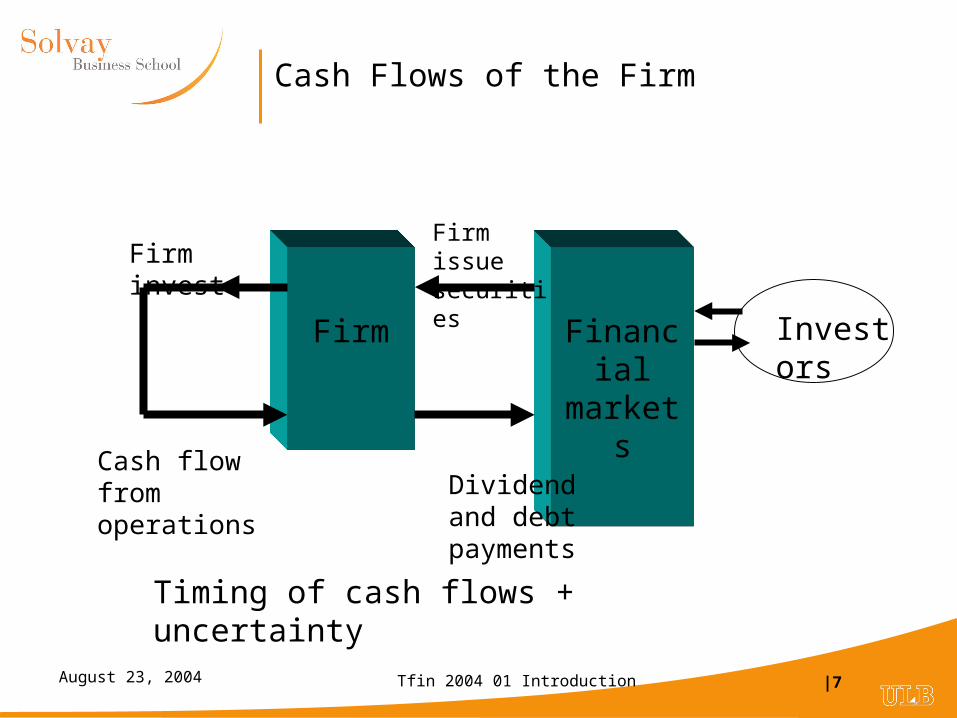

Cash Flows of the Firm

Firm Financial markets

Firm issue securitiesFirm invest

Cash flow from operations Dividend and

debt payments

Timing of cash flows + uncertainty

Investors

Tfin 2004 01 Introduction |8August 23, 2004

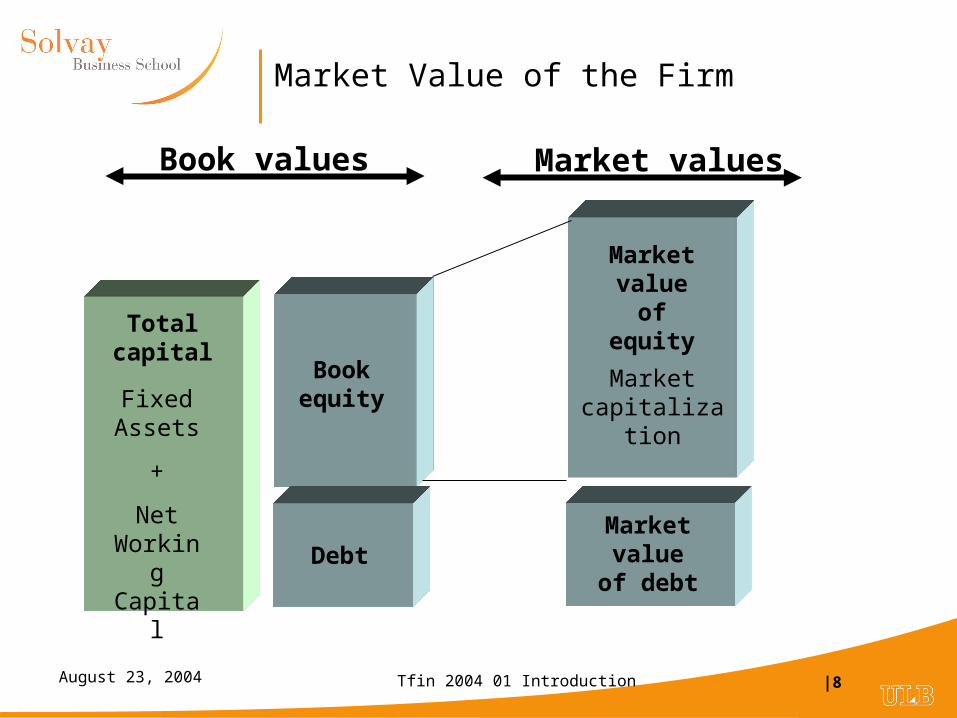

Market Value of the Firm

Total capital

Fixed Assets

+

Net Working Capital

Book equity

Debt

Book values Market values

Market value of equity

Market value of

debt

Market capitalization

Tfin 2004 01 Introduction |9August 23, 2004

Value creation

• Market value added (MVA)• = Market value of the firm’s capital – Total capital employed

• VALUE CREATION : 2 strategies• Strategy 1

• Buy assets at a cost lower than the value of the future revenues– real assets– financial assets

• Strategy 2• Sell financial assets for a price higher than the value of future

payments

Market value of equity + Market value of debt

Stockholders’ equity + Financial debt

Tfin 2004 01 Introduction |10August 23, 2004

Example: Microsoft (MSFT)

• Balance sheet - 30 June 2004

• (billion USD)

• Cash 49

• WCR -8

• Fixed assets 20

• Total assets 61

• Stockholders’ equity 61

• Income statement

• Revenue 32

• Net Income 10

• WCR = Working Capital Requirement

• Source: http://finance.yahoo.com

• Market Value -1 Sept. 2004

• Market cap 297

• Enterprise value 248

• MVA 236

Tfin 2004 01 Introduction |11August 23, 2004

The Cost of Capital

• The firm can always give cash back to the shareholders

• Capital employed by the firm has an opportunity cost

• The opportunity cost of capital is the expected rate of return offered by equivalent investments in the capital market

• The weighted average cost of capital (WACC) is the (weighted) average of the cost of equity and of the cost of debt

Project Cash

StockholderInvestment opportunities in capital markets

?

Tfin 2004 01 Introduction |12August 23, 2004

Stockholders’ problem

equity rs'Stockholde

IncomeNet ROE

InvestmentInitial

GainCapitalDivr

1

Capital marketCompany

ROEReturn on Equity

rExpected return

Tfin 2004 01 Introduction |13August 23, 2004

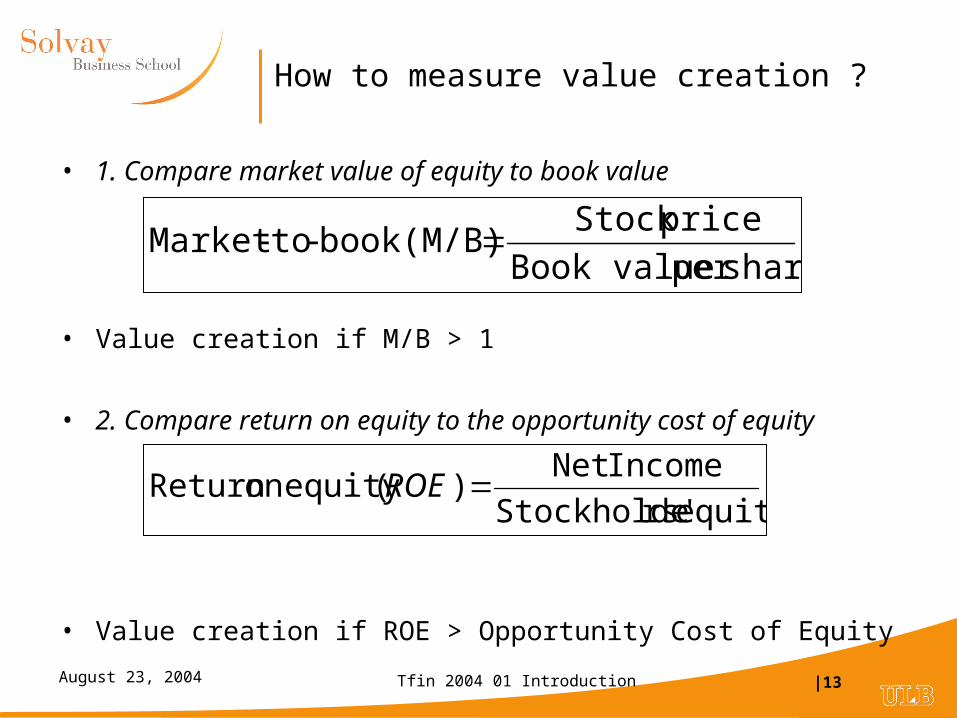

How to measure value creation ?

• 1. Compare market value of equity to book value

• Value creation if M/B > 1

• 2. Compare return on equity to the opportunity cost of equity

• Value creation if ROE > Opportunity Cost of Equity

shareper Book value

priceStock book(M/B)-to-Market

equity rs'Stockholde

IncomeNet )(equity on Return ROE

Tfin 2004 01 Introduction |14August 23, 2004

Value creation: Example

• Data:

• Book value of equity = € 10 b

• Net income = € 2 b / year

• Cost of equity r = 10%

• Return on equity ROE = 2 / 10 = 20% > 10%

• Market value of equity = NI / r = 2 / 10% = € 20 b

• Market value added: MVA = 20 – 10 = €10 b

• Market to Book M/B = 20 / 10 = 2

Tfin 2004 01 Introduction |15August 23, 2004

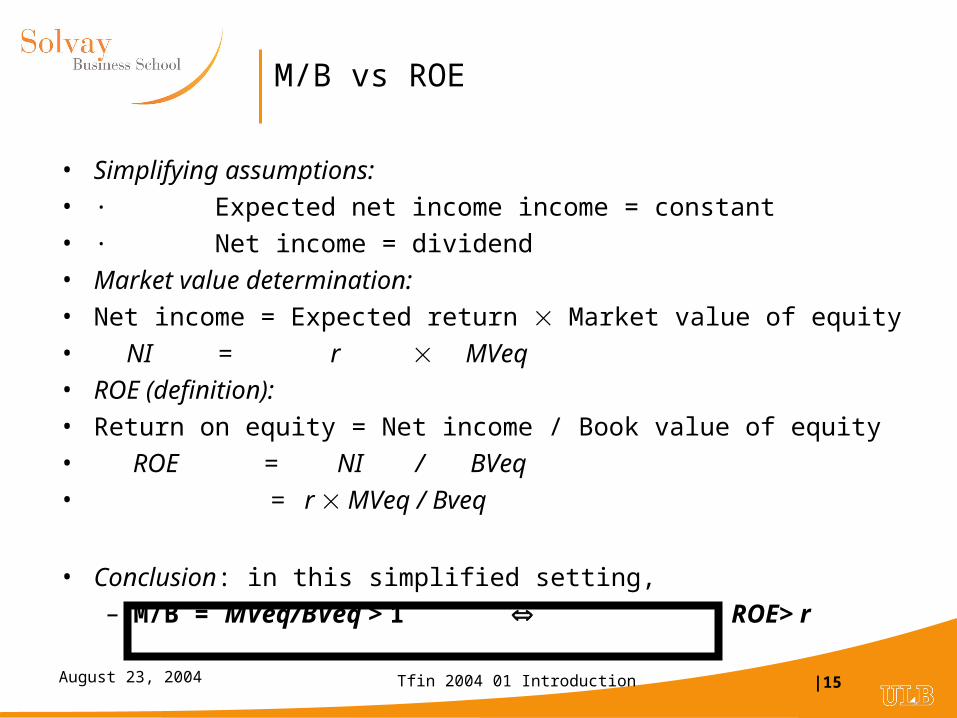

M/B vs ROE

• Simplifying assumptions:

• · Expected net income income = constant

• · Net income = dividend

• Market value determination:

• Net income = Expected return Market value of equity

• NI = r MVeq

• ROE (definition):

• Return on equity = Net income / Book value of equity

• ROE = NI / BVeq

• = r MVeq / Bveq

• Conclusion: in this simplified setting,

– M/B = MVeq/BVeq > 1 ROE> r

Tfin 2004 01 Introduction |16August 23, 2004

The Top Companies 2004

Mkt Value$ bil.

Price/Book

ROE%

1 GE US 328 4.3 21.62 Microsoft US 284 4.0 10.63 Exxon US 284 3.1 21.64 Pfizer US 270 3.9 2.15 Wal-Mart US 241 5.6 20.36 Citigroup US 239 2.4 19.17 BP UK 193 2.6 14.18 American Intl US 191 2.5 13.29 Intel US 185 4.8 16.810 Royal Dutch NL/UK 175 2.3 17.311 Bank of America US 170 2.5 22.312 Johnson & J. US 165 5.8 26.713 HSBC Hold. UK 163 2.1 16.0

Source:Business Week, July 14 2003

Tfin 2004 01 Introduction |17August 23, 2004

Drivers of ROE

• PROFITABILITY (du Pont system)

• Three determinants :

Equity

Assets

Assets

Sales

Sales

Net IncomeROE

EquityBook

IncomeNet ROE

Financial Leverage

Asset Turnover

Profit Margin

•Microsoft - 2004 US$ bil.•Net Income 10•Sales 32•Assets 61•Book equity 61

16.4%

31.0% 0.52 1.00

Tfin 2004 01 Introduction |18August 23, 2004

Example

Wal-Mart Vodafone Total

US UK F

Rank 5 14 24

MktValue 241,187 159,150 122,945

M/ B 5.6 0.7 3.5

P/ E 27 15 14

Sales 258,681 61,259 127,796

Profi t 8,861 11,364 8,968

Assets 104,912 269,754 97,647

ROE 20.20% 17.80% 24.10%

Profi t margin 3.43% 18.55% 7.02%

Turnover 2.47 0.23 1.31

Leverage 2.39 4.23 2.62

Source: Business Week July 26, 2004

Foundations of Finance

Tfin 2004 01 Introduction |20August 23, 2004

Theory of finance

• A young science

• Finance has been around for many centuries, of course…

• Main problem: calculation!!

• Imagine having to calculate the future value of 1 euro invested for 13 years when the annual interest rate is 4.35% (with annual compounding):

Future value = (1.0435)13

• A nightmare…..

• This problem disappeared after WWII with the development of computers.

• Now we have calculators and spreadsheets….

• We also have large data bases

Tfin 2004 01 Introduction |21August 23, 2004

Irving Fisher

• Finance has its roots in economics

• Irving Fisher laid the foundations of modern theory of finance.

• Takes into account the time dimension of financial decisions

• Main ideas:

• Decisions should based on present value

• Net Present Value (NPV): a measure of additional wealth

• With perfect capital markets: independent of preferences

Tfin 2004 01 Introduction |22August 23, 2004

Present value: 1 period, certainty

• Perfect capital market

• Interest rate: r

• Future cash flow C1

• Present value:

• or: r

CCPV

1)( 1

1

PV(C1) = DF1 C1

Interpretation: DF1 = discount factor

price of 1€ to be received in one year

price of unit zero coupon

with r

DF

1

11

Tfin 2004 01 Introduction |23August 23, 2004

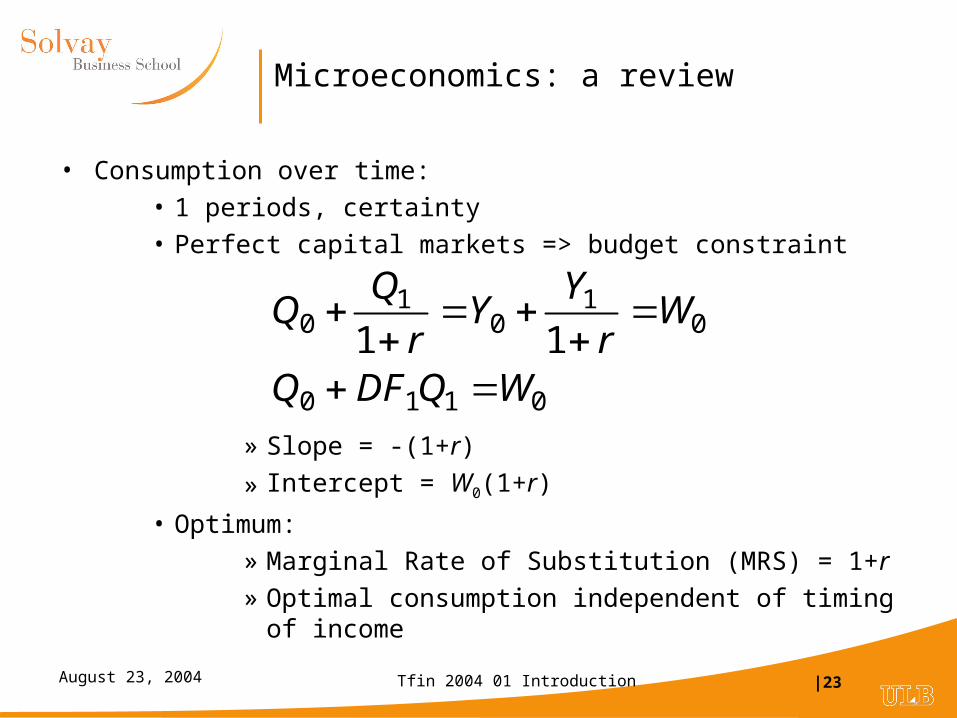

Microeconomics: a review

• Consumption over time:

• 1 periods, certainty

• Perfect capital markets => budget constraint

» Slope = -(1+r)

» Intercept = W0(1+r)

• Optimum:

» Marginal Rate of Substitution (MRS) = 1+r

» Optimal consumption independent of timing of income

0110

01

01

0 11WQDFQ

Wr

YY

r

Tfin 2004 01 Introduction |24August 23, 2004

Economic foundations of net present value

100

105

200Euros now

Euros next year

50

165

Slope = - (1 + r) = - (1 + 5%)

I. Fisher 1907, J. Hirshleifer 1958

Perfect capital markets

Separate investment decisions from consumption decisions

157.5

52.5

150

Tfin 2004 01 Introduction |25August 23, 2004

Net Present Value

NPV = -I + DF1 C1

Consider investment project:

Initial cost: I

Future cash flow: C1

Budget constraint with project:

NPVWCYvIYQvQ )()( 1110110

Tfin 2004 01 Introduction |26August 23, 2004

Economic foundations of net present value

100

105

200Euros now

Euros next year

50

165

207

NPV

Slope = - (1 + r) = - (1 + 5%)

-50

I. Fisher 1907, J. Hirshleifer 1958

Perfect capital markets

Separate investment decisions from consumption decisions

Tfin 2004 01 Introduction |27August 23, 2004

Entreprise Value Maximisation

0

Investment

Euros today

Euros next year

NPV

Investment opportunities

Market value of company

Numerical example!!!

Tfin 2004 01 Introduction |28August 23, 2004

Uncertainty: 1952 – 1973- the Golden Years

• 1952: Harry Markowitz*

– Portfolio selection in a mean –variance framework

• 1953: Kenneth Arrow*

– Complete markets and the law of one price

• 1958: Franco Modigliani* and Merton Miller*

– Value of company independant of financial structure

• 1963: Paul Samuelson* and Eugene Fama

– Efficient market hypothesis

• 1964: Bill Sharpe* and John Lintner

– Capital Asset Price Model

• 1973: Myron Scholes*, Fisher Black and Robert Merton*

– Option pricing model

Tfin 2004 01 Introduction |29August 23, 2004

1 period, uncertainty

• 2 possible states of the economy: prosperity and depression

• 2 financial assets: one riskless bond and one stock

Current price

Prosperity Depression

Bond v 1 1

Stock S SP SD

States Price P D Expected returnsProbability 0.5 0.5Bond 0.9524 1 1 5.00%Stock 50 100 25 25.00%

Tfin 2004 01 Introduction |30August 23, 2004

Contingent claims

• Consider 2 securities that pay 1€ in one state and 0€ in the other state.

• They are named: contingent claims, Arrow Debreu securities, states prices

Current Price

Prosperity Depression

CC prosperity vP 1 0

CC depression vD 0 1

Tfin 2004 01 Introduction |31August 23, 2004

Computing state prices

• Financial assets can be viewed as packages of financial claims.

• Law of one price:

v1 = vP 1 + vD 1

S = vP SP + vD SD

• Complete markets: # securities ≥ # states

• Solve equations for find vP and vD

DP

PD

DP

DP

SS

SSvv

SS

SvSv

1

1

Tfin 2004 01 Introduction |32August 23, 2004

Example

States Price P D Expected returnsProbability 0.5 0.5Bond 0.9524 1 1 5.00%Stock 50 100 25 25.00%

Contingent claimsCC P 0.3492 1 0CC D 0.6032 0 1

Project -50 120 40 80.00

Tfin 2004 01 Introduction |33August 23, 2004

Capital budgeting under uncertainty

• Consider the following investment project:

• Initial cost: I

• Future cash flows: CP or CD depending on state of the world.

• How do we compute the NPV for this project?

• NPV of project

• A straightforward extension of previous formula.

DDPP CvCvINPV

Tfin 2004 01 Introduction |34August 23, 2004

Example

States Price P D Expected returnsProbability 0.5 0.5Bond 0.9524 1 1 5.00%Stock 50 100 25 25.00%

Contingent claimsCC P 0.3492 1 0CC D 0.6032 0 1

Project -50 120 40 80.00

Present values 41.90 24.13NPV 16.03

Tfin 2004 01 Introduction |35August 23, 2004

References

• Corporate finance textbooks (MBA level)

– Brealey, Richard and Steward Myers, Principles of Corporate Finance, xth edition, McGraw-Hill 2000

– Ross, Stephen A., Randolph W. Westerfield and Jeffrey F. Jaffe, Corporate Finance, 6th edition, McGraw-Hill Irwin 2002

– Damorada, Aswath, Corporate Finance: Theory and Practice, Wiley 1997

• Ouvrages de référence en français:

– Bodie, Z. et Merton, R. Finance (édition française dirigée par C. Thibierge) Pearson education 2000

• Corporate finance texts for executives

– Bertoneche, Marc and Rory Knight, Financial Performance, Butterworth Heinemann 2001

– Hawawini, Gabriel and Claude Viallet, Finance for Executives: Managing for Value Creation, South-Western College Publishing, 1999