mémoire présenté le : srxuo¶rewhqwlrqgx 'lso

TRANSCRIPT

Mémoire présenté le :

pour l’obtention du Diplôme Universitaire d’actuariat de l’ISFA

et l’admission à l’Institut des Actuaires

Par : SAYAH Mabelle

Titre Comparing standardized and internal models in computing the interest rate risk capital charge in a bank’s trading book

Confidentialité : NON OUI (Durée : 1 an 2 ans)

Les signataires s’engagent à respecter la confidentialité indiquée ci-dessus

Membre présents du jury de l’Institut

des Actuaires signature

Entreprise :

Nom :

Signature :

Membres présents du jury de l’ISFA Directeur de mémoire en entreprise :

Nom : ROBERT Christian

Signature :

Invité :

Nom :

Signature :

Autorisation de publication et de mise

en ligne sur un site de diffusion de

documents actuariels (après expiration

de l’éventuel délai de confidentialité)

Signature du responsable entreprise

Secrétariat : DRIGUZZI Christine Signature du candidat

Bibliothèque : BARTOLO Patricia

Contents

Introduction 5

I Banking Risk Management Function 10

1 Banks 101.1 Objectives and roles . . . . . . . . . . . . . . . . . . . . . . . 101.2 Balance Sheet Composition . . . . . . . . . . . . . . . . . . . 101.3 Banking vs trading book . . . . . . . . . . . . . . . . . . . . . 14

2 Financial Risk Management 142.1 Market Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.2 Credit Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.3 Operational Risk . . . . . . . . . . . . . . . . . . . . . . . . . 152.4 Liquidity Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

3 Basel implementation 153.1 Basel I . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153.2 Basel II . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153.3 Basel III . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

4 On the interest rate risk in the trading book 164.1 Definition of the interest rate risk . . . . . . . . . . . . . . . . 164.2 Net interest income (NII) . . . . . . . . . . . . . . . . . . . . . 174.3 General Interest rate risk in the trading book . . . . . . . . . 174.4 Basel III perception (January 2016) . . . . . . . . . . . . . . . 17

4.4.1 SBA impact on banks . . . . . . . . . . . . . . . . . . 19

II Tools and Models used 20

1 Yield Curves 201.1 Introduction to yield curves . . . . . . . . . . . . . . . . . . . 201.2 Term structure estimation models . . . . . . . . . . . . . . . . 201.3 Yield curves across central banks . . . . . . . . . . . . . . . . 211.4 Different methodologies . . . . . . . . . . . . . . . . . . . . . . 23

1.4.1 Nelson Siegel method . . . . . . . . . . . . . . . . . . . 241.4.2 Dynamic Nelson Siegel . . . . . . . . . . . . . . . . . . 24

2 Statistical tools 252.1 PCA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 252.2 ICA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

3 Econometrical tools 273.1 GARCH(p,q) model specification . . . . . . . . . . . . . . . . 273.2 Different GARCH Models . . . . . . . . . . . . . . . . . . . . 29

4 Forecasting models 294.1 Constant Conditional Correlation models . . . . . . . . . . . . 304.2 Dynamic Conditional Correlation models . . . . . . . . . . . . 304.3 CCC vs DCC . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

5 Sensitivity Based approach (SBA) 325.1 Introducing the approach . . . . . . . . . . . . . . . . . . . . . 325.2 Implementation reasons . . . . . . . . . . . . . . . . . . . . . 325.3 Computational steps . . . . . . . . . . . . . . . . . . . . . . . 325.4 Hypothetical example . . . . . . . . . . . . . . . . . . . . . . . 34

6 Risk measures 356.1 Value at risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

6.1.1 Different VaRs . . . . . . . . . . . . . . . . . . . . . . 366.2 Expected Shortfall . . . . . . . . . . . . . . . . . . . . . . . . 376.3 VaR vs ES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

7 Value at Risk Backtesting Methods 397.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . 397.2 Backtesting strategies . . . . . . . . . . . . . . . . . . . . . . . 41

7.2.1 Frequency Based Tests . . . . . . . . . . . . . . . . . . 417.2.2 Magnitude Based Tests . . . . . . . . . . . . . . . . . . 427.2.3 Independence Tests . . . . . . . . . . . . . . . . . . . . 427.2.4 Duration Based Tests . . . . . . . . . . . . . . . . . . . 437.2.5 Martingale Difference Based Tests . . . . . . . . . . . . 437.2.6 Regression models Based Tests . . . . . . . . . . . . . 447.2.7 Loss function Based Tests . . . . . . . . . . . . . . . . 45

7.3 Practical Issues . . . . . . . . . . . . . . . . . . . . . . . . . . 457.4 Remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

III Numerical Application 47

3

1 Data used 471.1 Data statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

2 Portfolios’ duration and capital requirements 492.1 Single currency portfolios . . . . . . . . . . . . . . . . . . . . . 502.2 Multiple currencies portfolios . . . . . . . . . . . . . . . . . . 58

3 Backtesting Results 63

IV Conclusion 64

V References 67

VI Appendices 72

4

IntroductionCommercial banks are a key component of today’s financial and economicsystem. Banks allocate funds from depositors to borrowers, convert maturi-ties, and provide financial products. These services among others enhancesthe efficiency of the overall economy. Given this crucial role, adequate regu-lations should apply to monitor banks risks.

Since its first issuance in 1988, Basel has been the main banking regula-tion authority initializing with some main credit risk rules. In 1996, themarket amendment was issued setting the basic standards regarding tradingassets and the value at risk computation methodology. It also divided therisk into market and credit risk; market risk being divided between equity,interest rate, foreign exchange, commodity, and option risk with a standard-ized capital computation approach treating each asset class separately. In2006, Basel II came along with more ’personalised’ approaches such as Inter-nal Rating Based (IRB) for credit risk, internal models for Over The Counter(OTC) derivatives exposure along with the introduction of the operationalrisk charge.

However these regulations did not prevent major crisis hitting the inter-national market causing huge losses in different sectors (cf. Baptistab et al.(2012)). As a response to this shortage, Basel 2.5 was created beginning2011 as a response adding more capital to the trading book (especially onthe poorly modeled products). Basel 2.5 additions target the stressed VaRconcept, the incremental risk charge and few new standard rules regardingthe banking book.

In 2013, after a thorough observation of the consequences of the crisis andthe attempt for correction made by 2.5, Basel III was introduced. The mainfunctions of this issuance are: increasing capital for counterpart exposures,tightening the definition of the bank’s capital, adding buffer for liquidity andintroducing a new leverage ratio (cf. BCBS (2014)). In parallel, increasingthe trading book capital requirement under Basel 2.5 was required follow-ing the crisis and was not well designed: the calculation remains non-risksensitive and highly conservative, and differences in model approval persistbetween jurisdictions (cf. Babel (2012))

As a result, in May 2012 the Basel Committee published a ConsultativePaper on a ’Fundamental Review of the Trading Book’ (FRTB) to improve

5

this framework, then in December 2014, ”Fundamental review of the tradingbook: outstanding issues”, and its comments March 2015,the BCBS exposedthe weaknesses of Basel’s previous approaches. It suggested some majorchanges to the trading book to be implemented by 2018: scope and approvalprocess (boundary of the trading book, desk level model approval, modeltesting, model independent assessment tool), modeling Issues (stressed ex-pected shortfall, liquidity adjustments, diversification, default and migrationrisk, and non-modelable risk factors), and new standard rules for capitalcharges computation.

The standard rule suggested by the FRTB is based on sensitivities, henceit is called the ”Sensitivity based approach” (SBA): it was implemented asthe ’homogeneous’ method for capital charge computation across all banks.The SBA is based on percentages and correlations between different matu-rities and currencies (cf. BCBS (2015)). The existing standard rules poorlyreflected hedging or diversification thus inflating the trading book capitallevel. The SBA is simple yet risk sensitive which is already a big improve-ment. SBA is a standardized method that reflects the risk resulting from:Interest rate, credit spread, equity, commodity, foreign exchange, options riskand default.

Comparing regulatory approaches, an obvious contrast between Basel andSolvency is noted: Solvency II has a similar three pillar structure as Basel’sAccords. The capital requirements are described under the first pillar andrefer to all types of risks: an insurance is exposed to: market risk (inter-est rate risks, equity risk, property risk, spread risk, concentration risk andcurrency risk) and counterpart default risk. Both frameworks take diversi-fication effects into account and use square root formulas. However, theseaggregation approaches are applied at different levels: a considerably strongerrisk differentiation is shown under Basel III. For example, the SBA equityrisk distinguishes 10 risk categories in order to assign the risk weights, incontrast to one single shock for all listed equities under Solvency II. Underthe interest rate risk, SBA is Basel’s III approach whereas in solvency II ashocked scenarios based computation sets the capital charge (cf. LAAS andSiegel (2015)).

Seemingly, the SBA has several add-ons regarding sensitivity and diversify-ing considerations however it still has some issues (specifying the coefficients)and details concerning the aggregations that need to be tweaked; for instancethe figure under the square root is sometimes negative (cf. ISDA (2015)).In this dissertation, we aim to focus on the suggested standard rule by the

6

FRTB in order to compare it with other econometric models to find an equiv-alent capital charge computation technique with few additional details suchas time horizon and confidence level for a given capital. Among the differentrisk modulations, we chose to focus on the interpretation of the interest raterisk capital charge calculation.

According to Oxford Dictionary of Economics, interest rate is defined as”The charge made for the loan of financial capital expressed as a proportionof the loan”. More formally, Basel Committee on Banking Supervision (cf.BCBS (2004)) indicated that interest rate risk (IRR) is the exposure of abank’s financial condition to adverse movements in interest rate.

The sound IRR management conducted by Basel Committee on BankingSupervision had been the source on which analysts rely to evaluate the ac-tivities of bank’s risk management of interest rate (cf. BCBS (2004)). Inthe guideline, the committee offers four basic elements of IRR: appropriateboard oversight, comprehensive internal controls, adequate policies and ap-propriate risk measure. The SBA falls under this forth element in modelingthe interest rate risk in the trading book.

Our aim in this work is to understand the computation of the interest raterisk in banks based on BASEL’s III approach. However, the SBA remainsrelatively vague and the choices of its coefficient and correlation parametersare not robustly detailed and documented. Hence, studying the interest raterisk from an econometric point of view in order to compare and contrast theresults is critical and highly important.

Based on different central banks approaches for term structure interest rate,we selected few econometric models. The main idea was to reduce the di-mensions of the database, study the dynamics of these ’reduced’ factors andthen conclude on the wider data range dynamic. We introduce the methodsused to derive capital requirement and compare them with SBA’s in orderto conclude on some equivalence between them.

Having this objective in mind, the structure of the work is as follows: Westarted by modeling each interest rate curve on a stand-alone maturity basisusing a Generalized Auto regressive Conditional Heteroskedasticity (GARCH)approach. It is worth noting that by doing so, we dropped a crucial infor-mation which is the strong correlation between these maturities, however weneeded this phase as a starting point and a comparison threshold. Modelingthe volatility of term structures using GARCH processes has become a cur-

7

rent practice due to its numerous advantages relative to alternative models.GARCH-methods are a way of investigating how a function of past returns, ina specific financial series, should be constructed and mapped onto the secondmoment (cf. Hull (2000)). Proposed by Engle (1982) and then generalized byBollerslev (1986), GARCH models explain high frequency financial data se-ries through the auto regressive conditional heteroskedasticity and can modelsimultaneously conditional mean and conditional variance (cf. Edison andLiang, 1999). Two parameters for orders could be used in order to optimizethe results of the tests regarding GARCH coefficients convergence. However,in practice, low orders are more frequently used. The first-order (p=q=1)GARCH model (cf. Taylor (1986)) has become the most popular GARCHmodel.

Secondly, we introduced the component approaches starting with the Prin-cipal component analysis (PCA) which is one of the multivariate analysistechniques usually used for correlation studies, data reduction and efficiencyassessment (cf. Levieuge et al. (2010)). This method incorporates the inter-dependence between term structures maturities: it considers the correlatedcurves and generates new non-correlated variables. Each factor is related toa loading and a cumulative variance defining the variance explained by eachone of the new variables. PCA creates the same number of term structuresincluded in the model however, we need to choose the reduced number offactors that we want to handle. In this work, we chose to cover 98% of thevariance, by considering two or three factors. Using a GARCH model, weonly project the chosen factors and not the loadings; then we re-create theentire data from the projected factors and previously observed loadings.

Thirdly, we introduced the implementation of the Independent componentanalysis (ICA): it provides a mechanism of decomposing a given signal intostatistically independent components. PCA uses only second order statisti-cal information however, ICA uses higher order (kurtosis) for separating thesignals which permits more conclusive results in financial data (cf. Comon(1994)). A drawback in the ICA is its inability to indicate the data variancecoverage for each factor, therefore the modeler has to define the number offactors to be considered; in this dissertation we chose to include three ICAfactors.

Regarding the last approach, a factor model is suggested: the Dynamic Nel-son Siegel. No GARCH processes are used, instead a mix of Nelson Siegelestimation and Autoregressive Integrated Moving Average (ARIMA) pro-cesses projection are put in practice. Yield curve factor models, such as

8

Nelson-Siegel (1988), its dynamic version (cf. Diebold and Li (2006)) and itsarbitrage-free counterpart proposed by Christensen, Diebold and Rudebusch(2011), have been extensively applied to forecast bond yields. We used theDynamic Nelson Siegel due to its flexibility in representation especially forthe long term projection. By fitting the curves, projecting the factors usingDiebold method and the loadings employing an ARIMA process, we are ableto reconstruct the curves from which we concluded the capital requirement.

The capital charge using the previously mentioned methods, except SBA,can be computed on a certain confidence level basis and for a given timehorizon; therefore comparing these methods to SBA would determine a com-mon time horizon and confidence level, reaching the purpose of this work.We start by explaining in details the procedure of the SBA, the correlationbetween the duration of the portfolios and the capital charge required by thisprocedure then compare the methods using different approaches. These latterwill be based on bonds portfolios denoted in: euros, dollars and Turkish lirafrom the French, German, US and Turkish governments yields respectively,for maturities between 1 month and 30 years.

9

Part I

Banking Risk ManagementFunction

1 Banks

1.1 Objectives and roles

Banking is about managing different risks and making the most profit outof it. The skills that banks use to balance their numerous assets and lia-bilities reflect the risk exposure and the expected returns. Nowadays, com-mercial banks are becoming more complex including different instrumentsin their portfolio and expanding their work circle. In addition regulatoryrequirements have been adding strict restrictions and requirements in orderto reevaluate the risk management tasks. This might induce that they aremore able to withstand the business fluctuation and risks, however, recentevents showed that this might not be the case.

Based on the recent crises, in a systemic sense, the financial sector is be-coming more risky. Indeed, if numerous banks invest in similar positions orfollow parallel strategies the whole sector becomes more exposed. In orderto explain how to handle the entire banking risk, compute it and minimizeit, a certain full comprehension of a commercial bank portfolio should be intitle.

1.2 Balance Sheet Composition

To begin with, let us demonstrate the components of its balance sheet andbriefly explain each:

10

Table 1: Standard bank’s balance sheetASSETS LIABILITIES

Cash and central bank Central bankFixed income Loans: Reg. & MultiLat.Dev.Bks

Equities Banks and Financial Inst.Banks & financial Institutions Due to Parent and Subsidiaries

Affiliated Banks & Financial Institutions Customer DepositsLoans & Advances - customers Public Sector Deposits

Acceptances Certificate of DepositsInvestments Fiduciary term DepositsOther assets Acceptances

Long Term Sub. DebtOther payables

Other Liabilities

Assets:

1. Fixed income:

• Eurobonds: bonds denoted in foreign currency

• T-bills, T-notes: local currency (central bank & government)

• Central bank CDs

• Corporate Bonds: with other banks (small proportion)

These are liquid products with a fixed rate (a unique bond has a float-ing rate, however it is a small proportion of the portfolio). The Eu-robonds having a maturity more than one year are traded, thereforewe have a secondary market for these items. In case of a local crisis,the Eurobonds portfolio would induce a liquidity problem because theThe government would not present cash in exchange of these bondsknowing that such action would result in a depreciation of the localcurrency and the imbalance of the local to foreign currencies parity.However, this is not the case for the T-bills; this product is not tradedbetween banks therefore they do not have a secondary market, everytrade would be based in the primary market. In result, in time of cri-sis the T-bills would be sold to the government therefore they won’tinduce any liquidity problem in contrast with the Eurobonds. We con-clude that we have a certain problem in the liquidity for the dollar helditems, therefore we cover it in the money market.

11

2. Money Market: This item is included in the assets and liabilities, butis mainly covered in the assets part including all kinds of currencies(LBP, USD, EURO, JPY...). Mainly, the placements are divided uponthree categories relatively to the counterpart of each: affiliated, non-affiliated and the central bank. The purpose of this money marketshare is, as previously mentioned, covering the liquidity in case of alocal crisis (mainly due to the foreign currency held Eurobonds). Onthe assets part we have:

• Nostro: current account with another foreign bank: this is a coston the bank because, when a client beholds money in the bank, wetake a certain proportion of the amount and place it in a Nostroaccount presenting a low interest rate. Therefore, I am losingin term of interest rate however gaining in terms of covering theliquidity risk.

• Loan: Blocked account with a foreign bank

• Loan term: Blocked account with a foreign bank having an amor-tization option at the banks blocked accounts with the centralbank are included here (secret repo agreement for ten years).

• Central bank reserve: in local and foreign currencies

• Subordinated debt: it mainly include the main entity debt to otherentities, it is another category of debt with a priority of collectingmoney in case of failure or bankruptcy.

• Reverse Repo: loans given to financial institution, paying low in-terest rate and receiving collateral for guarantee (ex: collateralcovering 120% of the loan amount in CDs), they are qualified asover collateralized products.

3. Loans

• Corporate and Commercial loans

– Term loan: x amount on n years, payments divided over theyears

– Overdraft: a certain fixed amount but the client has the lib-erty to choose when and how much money to spend condi-tioned by the reimbursement of the amount

– Post financing: corporate having different payments with clientsbut in need of money right away, the bank provide the liquid-ity and get to be the recipient of the clients bills (with acertain profit margin)

12

– Syndicated loan: a loan divided between different banks

• Retail

– Personal

– Car

– Home: divided between the banks proportion and the housingservice (provided by the government)

– Credit card

– Educational

– Others

It is important to note what a SUBSIDIED loan is: a loan in-cluding a proportion held by the government such as the housingloan.

Liabilities:

1. Deposits:

• Demand

• Term

• Credit linked deposit: using a number of deposits we buy a bond,with the same maturity as the deposits, the coupons of the bondare distributed on the depositors and an additional commission isretained by the bank.

2. Money Market:

• Vostro: another bank places money in our portfolio

• Deposit: idem as the loan but reversely

• Deposit term: idem as the loan term but reversely

• Deposit fiduciaries: deposits from affiliated banks on which wepay interests (rather than them paying in their home country ahigher rate)

3. Sub debt: When we need to increase the capital, the investors give thebank a loan, the bank pays them the coupons from the benefits. Inthat way, we increase the capital from the investors.

13

1.3 Banking vs trading book

Trading and banking book are accounting terms that categories instrumentsin a bank: Based on the purpose the bank is holding this product, a decisionis made whether it is in the banking or the trading book. We note that thedistinction between these two books is rather ambiguous in some cases, toconfirm, some financial institutions have used this to juggle products betweenthis or that book in order to reduce the capital charge or enhance the capitaladequacy ratio.

The trading book, as its name shows, refers to all assets held by the bankand that are regularly traded, it is required to be marked to market daily.

The banking book however, is the assets that the bank is supposed to holduntil maturity. It is not marked to market.

2 Financial Risk Management

Financial risk management has known a large boost over the last decades dueto consecutive crisis that emphasis the crucial need of having a robust riskmanagement function. Corporations need to manage their risk rather thanavoiding them: quantitative approaches have been widely adopted howevera full reliance on these figures without considering the exogenous conditionsa financial institution is exposed to would not be very representative.

In banks, financial risk is divided between several types: market, credit,operational and more recently liquidity. Briefly, we introduce each type:

2.1 Market Risk

This risk is due to market prices movement: stock prices, FX rates, interestrates, commodity prices or credit spreads. It is this, overly studied risk, thatled to the birth of the value-at-risk concept.

2.2 Credit Risk

The credit risk is related to a counterpart: this latter might not be ableto fulfill his contractual obligations: as default or just devaluation of therequired amount. The key aspect in this type is the probability of defaultand the exposure at default.

14

2.3 Operational Risk

Operational risk is divided between sources: people, systems and externalevents. An employee fraud, an ATM malfunction or a civil war fit in the op-erational risk category. This is the most hard to quantify type of risks whichleads to the use of more qualitative techniques, score cards and professionalsassessments.

2.4 Liquidity Risk

Liquidity risk represent the risk that a transaction cannot be executed onthe market due to the illiquidity of the underlying or size of the transactionsor the risk of not being able to fund payments. This risk gained the notationof the ’death risk’ in 2008 crisis once liquidity is missing it’s a vicious circlenot only for the concerned institutions but for the whole system.

3 Basel implementation

3.1 Basel I

In 1988, Basel was created in his first version in order to unify the interna-tional banking system (cf. BIS).

It divided the required capital into two tiers: tier I (Core capital) and TierII (Supplementary capital).

The tier I consists shareholders equity, held stocks and all declared reserveswhereas tier II includes gains and long-term maturing debts. The Capitalcharge is divided between two risk typologies: Market risks (interest rates,fx, equity derivatives) and credit risk (including default risk).

3.2 Basel II

Basel II implemented the minimal capital adequacy ratio which is the capitalheld to the assets for an 8% figure. The risks acknowledged became three:the operational risk was added. Plus, under Basel II internal approachessuch as the internal ratings-based approach were recognized. This new Baselversion is more risk sensitive and more representative of the risk mitigationadvantages therefore it was seen as an improvement to the previous Baselaccord until enormous financial crisis such as the Sub-crime crisis in 2008.

15

3.3 Basel III

Basel III was created in an attempt to improve capacity of absorbing shocksdue to the rise of the instability in the financial markets, improve risk man-agement and strengthen transparency among banks: it increases the marketrisk requirement, adjusts the credit risk computation and adds disclosures tobe provided regularly. Basel III also added two main concepts: the liquidityratio and leverage ratio.

4 On the interest rate risk in the trading

book

4.1 Definition of the interest rate risk

Previous studies show that the market risk factor dominates in term of sta-tistical significance on the entire portfolio risk, therefore we chose to managethe interest rate risk in order to get a broader view on the consolidated risk(cf. Schuermann (2010)).

P.S: A careful analysis of the portfolio risk suggests that the use of fewfactors accounting for the largest proportion of returns will underestimatethe risk, adding to that leaving out factors with high expected return willguide to misleading results as well (cf. Kambhu, Rodriguez). A banks inter-est rate risk reflects the extent to which its financial condition is affected bychanges in market interest rates. There are two different ways of thinkingabout such effects. The first approach focuses on the impact of changes inmarket interest rates on the value of bank assets, liabilities and off-balancesheet positions (potentially including those that are not marked to marketfor reporting purposes). The second approach focuses on the implications ofmovements in market rates for the future cash flows that the bank will ob-tain. Since the present discounted value of the banks cash flows must equalthe economic value of the bank, these two approaches are consistent and bothcan be useful (cf. BIS paper (2010)).

To assess directly the extent detailed information about a number of possiblesources of interest rate risk is needed. Clearly, one would need to understandthe mechanism of the bank and the detailed characteristics of each prod-uct: pricing assets and liabilities, including repricing periods and base rates,the likelihood that bank customers would choose to repay loans or withdrawfunds early as a result of changes in market rates, the interest sensitivity of

16

fee income and off-balance sheet exposures...

In addition to being very complex, the feasibility of this study depends onthe availability of the data therefore we try to choose an alternative way byresorting to well-chosen benchmarks. A universally used tool to measure thiskind of risk is the NII, net interest income.

4.2 Net interest income (NII)

The net interest income of a bank is defined as the excess of interest receivedover interest paid (cf. Hull (2012)).

Net interest income = interest revenue - interest expense

• Daily computed

• Deposits basis: 365 days

• Loans basis: 360 days

• Calculation for each product and then aggregated

• The change of NII for a giving change in rate: the computation is onlyaffected by the items that matures within this year or the floating itemswhich rates can change during this one year.

4.3 General Interest rate risk in the trading book

In the trading book, two different notations are assigned to the interest raterisk: the general aspect and the specific genre.

Simply, the general interest rate risk is the risk arising from general mar-ket movements Such as fluctuations in interest rate levels or equity priceschanges on the market; whereas specific interest rate risk is the risk relatedto the credit quality of issuers.

4.4 Basel III perception (January 2016)

In December 2014 Basel Committee issued its third consultative paper onoutstanding issues related to the fundamental review of trading book capitalrequirements. Recognizing the significant operational burden posed by cer-tain features of the proposed framework, including the revised standardizedapproach (cashflows needed) , several alternative treatments were tested in

17

the 2014 QIS and will be further assessed through a follow-up QIS in early2015. This document sets:

• the treatment of internal risk transfers of equity risk and interest raterisk between the banking book and the trading book

• a sensitivities-based methodology in the revised standardized approach

• a simpler method for incorporating the concept of liquidity horizons inthe internal models approach

Three main objectives for the revised standardized approach:

1. The approach must provide a method for calculating capital require-ments for banks with a level of trading activity that does not requiresophisticated measurement of market risk.

2. It provides a fallback in the event that a bank’s internal model isdeemed inadequate, including the potential use as an add-on or floorto an internal models-based charge.

3. The approach should facilitate consistent and comparable reporting ofmarket risk across banks and jurisdictions.

A previous consultative paper proposed a cash flow-based method which re-quired banks to decompose financial instruments into their constituent cashflows and then discount each cash flow using the risk-free curve for each cur-rency plus the credit spread of each instrument. Banks had many constraintsand issues regarding this method (data wise), therefore following these con-cerns, the Committee agreed on a sensitivity-based approach (SBA) as analternative to cash flow-based calculations for the standardized approach.

This new method would require banks to use price and rate sensitivities thatare more likely to be available in their systems as inputs into the differentasset class treatments. The use of sensitivities thus reduces the implementa-tion cost of the revised standardized approach.

The standardized approach trading book capital requirement is the sum of:

The linear (delta and Vega) risk and curvature requirements for the generalinterest rate risk (GIRR) capital charge, Credit Spread Risk (non-securitisations),CSR (securitisation non-correlation trading portfolio), Equity capital charge,Commodity capital charge, FX risks and additional requirements for defaultrisk (non-securitizations), default risk (securitization non-correlation trading

18

portfolio) and default risk (correlation trading portfolio).

In the following, we are discussing the SBA for the GIRR in the tradingbook.

4.4.1 SBA impact on banks

in a study led by BCBS (cf. BCBS (2015))based on a sample of 44 banks thatprovided usable data for the study and assumed that the proposed marketrisk framework was fully in force as of 31 December 2014; the results showthe following: market risk capital charges would produce a 4.7% increase inthe overall Basel III minimum capital requirement. When the bank with thelargest value of market risk-weighted assets is excluded from the sample, thechange in total market risk capital charges leads to a 2.3% increase in overallBasel III minimum regulatory capital. Compared with the current marketrisk framework, the proposed standard would result in a weighted averageincrease of 74% in aggregate market risk capital. When measured as a simpleaverage, the increase in the total market risk capital requirement is 41%. Forthe median bank in the same sample, the capital increase is 18%. Comparedwith the current internally modelled approaches for market risk, the capitalrequirement under the proposed internally modelled approaches would resultin an increase of 54%. For the median bank, the capital requirement underthe proposed internally modelled approaches is 13% higher. Compared withthe current standardised approach for market risk, the capital requirementunder the proposed standardised approach is 128% higher. For the medianbank, the capital requirement under the proposed standardised approach is51% higher.

19

Part II

Tools and Models used

1 Yield Curves

1.1 Introduction to yield curves

The relationship between the yields of default-free zero coupon bonds andtheir length to maturity is defined as the term structure of interest rates andis shown pictorially in the yield curve. This relation can be used for riskmanagement and has an important role in pricing fixed-income securitiesand interest rate derivatives, as well as other financial assets. Because of itsnumerous uses, an accurate estimate of the term structure has constituted amajor question in the empirical literature in economics and finance.

There are two distinct approaches to estimate the term structure of interestrates: the equilibrium models and the statistical techniques. Examples of thefirst approach include Vasicek (1977), Dothan (1978), Brenan and Schwartz(1979), Cox and Ingersoll Ross (1985) and Dufie and Kan (1996).

1.2 Term structure estimation models

Term Structure static models are usually spot rate models that weaves to-gether zero yields of different maturities as they are observed in the market.Major criticism of static spot rate models are adjustments and data overfitting. These models simply calculate the interest rate that fits the observedprice.

The first step in any financial scenario aiming to measure risk, anticipatefuturistic losses, gain or returns is the construction of an appropriate inter-est rate model especially when the existing yield curve is insufficient and lackof precision. A wide variety of models is available for long and short term;yet not a single model has proven to be worthy and valuable for all kindsof application, different purposes and different approaches. There is a veryimportant issue to consider when choosing among different models related tothe background, data and concept of the model: equilibrium and arbitragefree models(cf. Chen et al. (2010)).

20

Arbitrage free models Arbitrage-free structure projects future interestrates based on the historical yield curve. Therefore, the new anticipatedprices respect the non arbitrage concept and are useful for pricing deriva-tives. In this approach, we consider that individual agents are risk-neutraland have no preferences reaching by that a ’theoretical’ partial equilibrium(cf. Damino, Fabio (2000)). The no-arbitrage approach is an exact fit tothe observed market yield. Some of these models include: Hull and White,CIR++ and Karasinki’s extended model.

Equilibrium models In contrast with the no arbitrage methods, the gen-eral equilibrium model allows the investor’s risk preference to enroll in pricingthe instruments, in that kind of assumptions a more realistic equilibrium isreached. Equilibrium models typically begin with an assumption for theshort term interest rate behavior, which are usually derived from more gen-eral assumptions such as state variable or any significant factor that describethe overall economy. Using these assumptions, the model can determine thelong term behavior based on the possible paths (cf. Longstaff (1989)). Thesemodels are fairly easy to use however, they generate yield curve inconsistentwith the current market prices. In addition, the market price of risk used inthese models is very hard to obtain. Some of these models include: Vasicek,CIR, Dothan and exponential Vasicek.

1.3 Yield curves across central banks

Most central banks use either the Nelson-Siegel or the extended version sug-gested by Svensson. Exceptions are Canada, Japan, Sweden, the UnitedKingdom, and the United States of America which all apply variants of thesmoothing splines method. They employ government bonds in the estima-tions since they carry no default risk.

21

Rudy J. DACCACHE PhD Thesis

Appendix 1.B- Yield Curve Models in Cen-tral Banks

Table 1.7: Yield Curve Models in Central Banks

Centra Bank EstimationMethod

Minimised Er-ror

Availability(BIS)

Belgium Svensson orNelson-Siegel

Weighted Prices up to 16 years

Canada Merrill LynchExponentialSpline

Weighted Prices up to 30 years

Finland Nelson-Siegel Weighted Prices up to 12 yearsFrance Svensson or

Nelson-SiegelWeighted Prices up to 10 years

Germany Svensson Yields up to 10 yearsItaly Nelson-Siegel Weighted Prices up to 30 yearsJapan Smoothing

SplinesPrices up to 10 years

Norway Svensson Yields up to 10 yearsSpain Svensson Weighted Prices up to 10 yearsSweeden Smoothing

Splines andSvensson

Yields up to 10 years

Switzerland Svensson Yields up to 30 yearsUK VRP Yields up to 30 yearsUSA Smoothing

SplinesWeighted Pricesor Prices

up to 10 years

40

Table 2: Yield Curve methodologies across central banks

22

1.4 Different methodologies

noMo

del Na

meSte

psEqu

ation

Advant

ages

Disadv

antage

s

1Sup

er Bell

(Bootst

raping

)extr

acting t

he zero

-coupo

n and fo

rward i

nterest

rates

using an

OLS re

gressio

n to fit

a par yie

ld curv

e from

exis

ting bo

nd em

ploying

bootst

rapping

to der

ive zero

-coupo

n rates

For les

s than o

ne year

Cubic In

terpolat

ion1. T

he mode

l is not c

oncept

ually di

fficult.

2. The m

odel is p

arame

trized a

nalytica

lly and i

s thus s

traight

forward

to solv

e.1. le

ngthy p

rocess

2. focu

ses exc

lusively

on YTM

rather

than o

n the ac

tual ca

sh flow

s of the

underly

ing bon

ds.3. n

ot enou

gh flexi

bility

2Nel

son-Sie

gel Con

vert th

e bond p

rices to

forwar

d rates

(using F

ama-b

liss me

thod)

Conver

t to zer

o yields

1.The av

erage y

ield cur

ve is in

creasin

g and co

ncave.

2.Coul

d assum

e a var

iety of

shapes

(sloping

upward

, sloping

downw

ard, hu

mped o

r inver

sely hum

ped).

3.Yield

dynam

ics are p

ersisten

t (\beta

_1) and

less pe

rsisten

t (weak

er for \

beta_2

).4.Th

e short

end is m

ore vol

atile th

an the l

ong end

(short

end dep

ends on

\beta_

1 and \b

eta_2 w

hereas

the lon

g end

depend

s only o

n \beta

_1).

5.Long r

ates ar

e more

persist

ent tha

n short

rates (lo

ng end d

epends

on \be

ta_1 o

nly).

non line

ar estim

ation fo

r the la

mbda f

actor

3Sm

ith- Wi

lsonGoi

ng from

the ob

served Z

C on th

e mark

et, Com

pute ot

her ma

turities

ZC via

interpo

lation an

d extrap

olation

using a

long U

ltimate

Forwar

Rate

1.perfe

ct fit o

f the es

timate

d term

structu

re to th

e liquid

marke

t data

2.base

d on so

lving a

linear s

ystem o

f equat

ions an

alytical

ly. This

is an ad

vantag

e comp

ared to

metho

ds that

are bas

ed on m

inimizin

g sums

of leas

t squar

e deviat

ions, a

s the

se are s

uscept

ible to

“catast

rophic”

jumps w

hen the

least-sq

uares f

it jump

s from o

ne set o

f param

eters t

o anoth

er set o

f quite d

ifferen

t values

.3.In

this m

ethod

the ult

imate f

orward

rate w

ill be re

ached a

sympto

tically.

1.The pa

ramete

r alpha

has to

be chos

en outsi

de the m

odel. Th

us, in g

eneral,

expert

judgm

ent wo

uld be n

eeded t

o assess

this

input p

arame

ter for

each cu

rrency a

ndeac

h point

in time

separa

tely.

2.The pr

ice mig

ht be ne

gative.

4Nel

son-Sie

gel Sve

nsson

Conver

t the bo

nd price

s to for

ward ra

tes(usi

ng Fam

a-bliss

metho

d)Con

vert to

zero yi

eldsmo

re flexi

ble with

the cur

ve move

ments

estima

tion err

ors lea

ds to fu

rther de

viation

6Me

rrill Lyn

ch Expo

nential

spline

Specifie

s a fun

ctional

form for

the dis

count f

unction

a zero c

oupon

interest

rate fu

nction

is deriv

ed from

this

latter

1. high

flexibili

ty2. m

akes no

underly

ing eco

nomic a

ssump

tions

No assu

mption

s regar

ding infl

ation, f

uture

econom

ic grow

th, and

the dyn

amics o

f the sh

ort rate

over tim

e

7Sm

oothing

splines

assume

a linea

r funct

ionmin

imise th

e distan

ce betw

een est

imatet

and ob

served

data

1. Com

putatio

nal spe

d 2. c

larity in

control

ling cur

vature

behavio

rnot

easy to

progra

m

Model

s for co

nstruc

ting yie

ld curv

es

P

1

0, 1exp

1exp

exp

Table 3: Yield curves constuction methods

23

1.4.1 Nelson Siegel method

The interest rate curve is essential for pricing, hedging and evaluating aportfolio. Various curve fitting spline methods have been introduced suchas quadratic and cubic splines (McCulloch (1971, 1975)), exponential splines(Vasicek and Fong (1982)), B splines (Shea (1984))... However, these meth-ods were criticized for not being too representative of the economic situations.Therefore, Nelson and Siegel (1987) and Svensson (1994, 1996) suggestedparametric curves that are flexible enough to describe the large frame of thefinancial conditions in a static method overview.

Nelson Siegel method consists of estimating three parameters using the max-imum likelihood process or OLS to rebuild the yield curve (cf. Siegel andNelson (1988)): the three Nelson-Siegel components have a clear interpreta-tion as short, medium and long-term components. These labels are the resultof each element’s contribution to the yield curve.

y(τ) = β1 + β21−e−λτλτ

+ β31−e−λτλτ−e−λτ

Where β1 > 0, β1 + β2 > 0 and λ > 0 The Nelson Siegel model is extensivelyused by central banks and monetary policy makers (ex: Bank of InternationalSettlements (2005), European Central Bank (2008)).

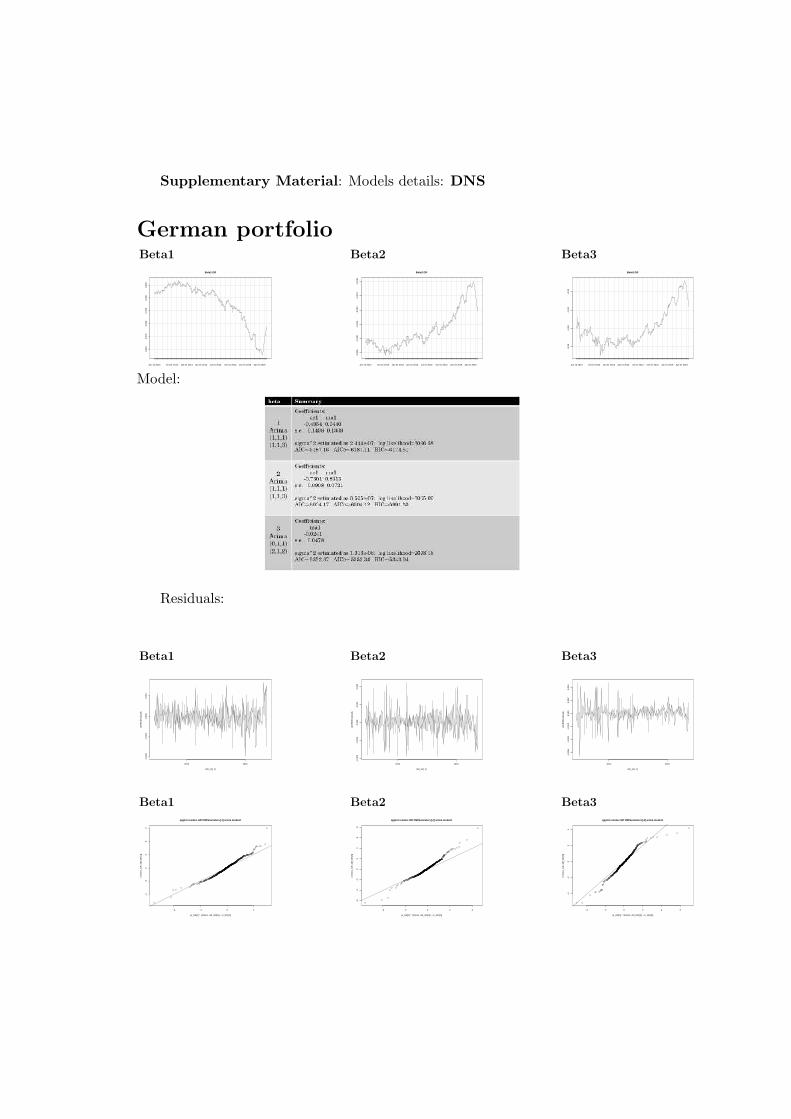

1.4.2 Dynamic Nelson Siegel

As a development to the traditional fitting approach, Diebold and Li (2006)introduce the Dynamic Nelson-Siegel (DNS) model by estimating the classi-cal formula with time-varying factors and model them using autoregressivespecifications projecting therefore the yield curves by adding dynamism tothe parameters.Diebold and Li (2006) interpret β1t, β2tandβ3t as the slope, curvature andlevel of the curve. This method shows very encouraging results especially ona long time horizon.

yt(τ) = β1t + β2t1−e−λtτλtτ

+ β3t1−e−λtτλtτ−e−λtτ

Our chosen approach in this work is to fit the yield curves using the tra-ditional Nelson Siegel and to project it afterwards: estimating the differentyields using the Nelson Siegel function in R, R-package: YieldCurve, project-ing the betas computed using adequate ARIMA processes (based on best-fitapproach); maintaining the loadings as calculated historically, rebuilding theprojected yields based on Diebold and Li’s dynamic approach. Having theprojected yields, a new portfolio evaluating could be placed, a value at riskand therefore a capital charge is computed.

24

2 Statistical tools

2.1 PCA

The principal component method summarizes the numerous factors affectinga system by a few uncorrelated variables, called principal components, whichprovide a description of the systems dynamics.

Principal component analysis is a process used to reduce the dimension ofthe data (cf. Jackson (1991)): This is useful in extracting a visual represen-tation i.e. by reducing the considered dimensions to a much more compactones enabling the researcher to represent visually the points. PCA trans-forms a number of starting points to a much reduced one using optimizationcriteria. Used criteria might be, among others, minimization of the mean-square error in data compression or finding mutually orthogonal directionsin the data explaining a maximal variance.

This reduction in dimensionality is particularly useful in finance, since assetprices are affected by thousands of economic variables that are difficult totranslate into a rigorous price model therefore this technique is commonlyapplied in banks to interest rate markets to describe the yield curves behaviorto be used for scenario analysis and risk estimation (cf. Nath, Dalvi (2013)).

The benenefits of PCA may be divided into: risk estimation, risk report-ing and scenario analysis. This method allow a new representation of thesame data however with a much more compact distribution that retains thesame characteristics. It helps understanding the dynamics and the shifts ofthe curves. The chosen model has to explain at least 95% of the variation andinclude the fewest components possible. For factor analysis to be efficient, itis important that an appropriate sample size should be used (cf. Novosyolov,Scatchkov (2009)).

To apply the principal component analysis, p vectors representing the weightsor loadings will be considered such as: wk = (w1, . . . , wp)k . These lattersmap each row vector xi of X to a new vector of principal component scoresti = (t1, .., tp)i , given by tki = xi.wk.

Therefore instead of having 15 yield curves with different maturities, usingthe PCA process we reduce it to a number of principle factors that representmore than 98% of our data. Having these factors (in most cases 2 or 3) weproject them on a one year basis using GARCH models and choose their

25

parameters based on the previously mentioned details. After rebuilding thefifteen maturities using the projected factors and the previously computedloadings, we generate the VaR and capital charge of our portfolios using thesame way selected in the previous methodology for the capital charge com-putation. This process adds the correlation between different maturities andshows the interdependency between all tenors even when the portfolio doesnot include the entirety of maturities.

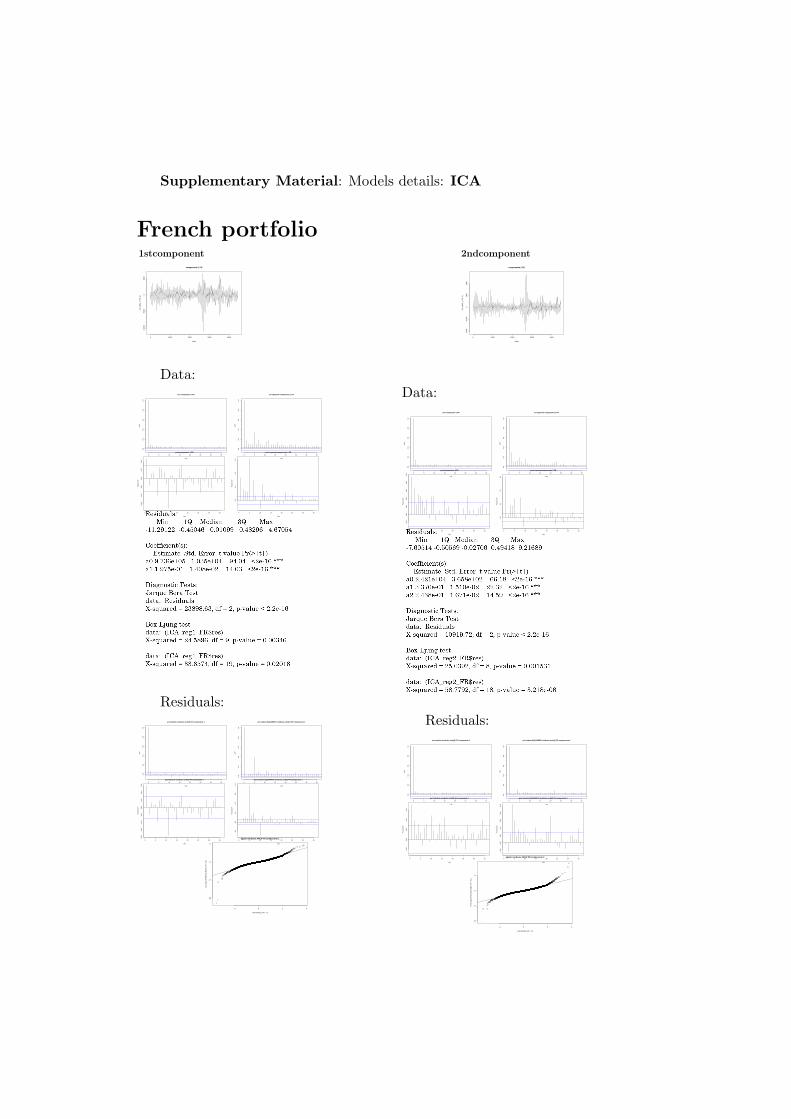

2.2 ICA

Independent components analysis, (cf. Comon (1994)), is another methodto reduce dimensions that has the same functionality as PCA except for thedifference in the determination of the components and the loadings: In PCA,the aim is to find vectors that best explain the variance of the data whereas inICA the kurtosis is in focus. The latent variables are assumed non-Gaussianand mutually independent(cf. Bugli (2007), Burgos (2013)).

ICA could be used in different fields such as digital imaging, stocks databases,economic indicators, geologic measurements or even psychometric indicators.Initially, the process was mostly used to ‘un-mix’ several signals: differentwaves recorded at the same time, two time series interfering for a certainprocess, underwater signals. . . (cf. Amari (1996), Bell (1995)). In this ICAmethod follows the same process as PCA’s: ICA to the full data panel,GARCH projection, rebuilding of the data, determining the VaR, capital re-quirement computation.

ICA is a data processing technique that aims to transform a certain setof data to another reduced, linear functions of statistically independent com-ponent variables:Having an m−dimensional vector xt = (x1t, x2t, . . . , xmt) , using the ICAmethod we generate a matrix A and another set of vector st verifying thefollowing:

xt = A ∗ st

Having A is a m ∗ n matrix with elements that explains the effect (weight)of st on our original data xt, and st a n−vector with mutually independentcomponents.

Again this model includes correlation as well as GARCH estimations howeverit is an add-on to the previous method due to the following: ICA does not

26

assume the non-correlation of the factors instead it supposes the indepen-dence, such that the normality of the data is not a must; on the contrary,non-Gaussian factors have an added-value.

3 Econometrical tools

3.1 GARCH(p,q) model specification

ARCH methods were introduced by Engle in 1982 (cf. Engle (1982)) thengeneralized by Bollerslev in 1986 (cf. Bollerslev and Tim (1986,2008)) as aconditional variance prediction model, especially useful when the volatilityof the financial data is the main issue.

Let Xt denote a real-time stochastic process and σt its conditional variance;GARCH (p, q) process is given by:

Xt|σt N(0, σ|t2)

σ2t = α0 +

∑pi=1 αiX

2t−i +

∑qj=1 βjσt−j(4)

Where p > 0, q > 0, α0 > 0, αi > 0 and βj > 0∀i, j

The GARCH approach has been used in modeling financial time series, test fi-nancial theories and interpret key features of a given data in a time-dependentmatter.

In our bonds portfolio we consider government yield curves with maturitiesranging from 3 months to 30 years, compute the return and apply GARCHmodels for each maturity.

The orders of a GARCH process play a major role in determining the re-sults: q can be based on model selection tests such as the auto correlationfunction of the squared residuals; however with large q, estimation errormight increase. Finding both p and q parameters can be facilitated throughtime series testing.

In our work GARCH models are determined on the basis of coefficients signif-icance and Jarque Berra test (cf. Bollerslev (2008)): skewness and kurtosisare used for constructing Jarque Berra’s test statistic to find whether thecoefficients of skewness and excess kurtosis are jointly null (cf. Jarque andBera (1981)).

27

When estimating GARCH models, computer-based softwares have to beused. Different softwares have different functionalities, drawbacks and fea-tures. Several works present these GARCH estimating software packages andcompare them (cf. Brooks et al. (2003)). In our work, the ’tseries’ R-packageis used to estimate these models.

We start by estimating the GARCH process for each maturity, after hav-ing adequately selected the parameters. Since the projection requires initialvalues for each yield curve, we adopted the traditional way of having the lastobserved yield as the first data point of projection and the volatility as thehistorically observed volatility for each curve. We project for one year, fixinga year as 252 days, using Monte Carlo simulations then extract the value atrisk for different confidence levels from 95% to 99.9 %. The capital chargepercentage was computed on a mean relative figure basis, i.e. the mean of allsimulations is extracted of the VaR and divided again by the mean (10,000simulations were in order).

28

3.2 Different GARCH Models

Table 4: Different GARCH models

4 Forecasting models

Projecting time series relies mostly on the volatility of the considered data.The correlation is a critical point to tackle too which led to different ap-proaches in forecasting models: non-conditional modals, constant conditionalcorrelation and dynamic conditional correlations approach.

29

4.1 Constant Conditional Correlation models

Model where time-varying covariances are proportional to the conditionalstandard deviation

In the CCC model the conditional covariance matrix consists of two com-ponents that are estimated separately: sample correlations and the diagonalmatrix of time-varying volatilities.

Advantages of a CCC model:

• Guarantees the positive definiteness of the co-variance matrix forecast

• Simple model, easy to implement

• Since we obtain a diagonal matrix for volatilities, we can estimate eachvolatility separately.

Disadvantages of a CCC model:

• The assumption of correlations being constant over time is at odds withthe vast amount of empirical evidence supporting nonlinear dependence

4.2 Dynamic Conditional Correlation models

DCC model is an extension of the the CCC model that corrects the latter’smain defect: constant correlations. Such models let the correlation matrixbe time dependent.

Advantages of a DCC model:

• Large covariance matrices can be consistently estimated using DCCtwo-step estimation technique without requiring too much computa-tional power.

Disadvantages of a DCC model:

• This method implies that the conditional correlations of all assets aredriven by the same underlying dynamics which is often an unrealisticassumption.

30

4.3 CCC vs DCC

Author

year

Title

Publica

tionCCC

DCC

1Ext

reme

Value

Theory

EVTF. X

. Diebo

ldT.

Schuer

mann

J. D.

Strough

air199

8Pitf

alls and

Oppor

tunitie

s in t

he Use

of Ext

reme

Value

Theory

in Risk

Manag

ement

Journa

l of

Risk

Finance

, 1 (Wi

nter

2000),

30-36.

comput

ation o

f the r

are

events

' proba

bility of

occ

urence

Estima

tes ext

reme q

uantile

s and

probab

ilities b

y fitting

a mo

del to

the em

pirical

surviva

l fun

ction o

f a set

of data

using

only th

e extrem

e event

data

rather t

han all

of it.

1. Selec

t a thre

shold u

2. Fit th

e excee

dent da

ta of th

is thre

shold y

={y1,y2

,…,yn} t

o a gen

eralise

d Pare

to distr

ibution

GPD for

a sam

ple of n

esceed

ing dat

a points

maxim

um like

lihood

for esti

mating

s and

eAlt

ernativ

e estim

ators

are av

ailable

(meth

od of

mome

nts, H

ill,or o

ther)

daily re

turns of

the

Nikkei

225 ma

rket

index f

or the

period

from

07 Jan

uary 19

70 to 1

7 Augu

st 2010

~ it foc

cusses

on the

'critica

l' par

t ~ r

easona

ble fun

ctions a

re gen

erated

that ar

e well s

uited

for the

tail fit

tings an

d esti

mation

s

~ conve

rgence

of (Ma

ximum

Likelih

ood) es

timate

d par

amete

rs is no

t guara

nteed.

~ M

ight req

uire Mo

nte Ca

rlo sim

ulations

when

applied

to por

tfolios.

~ Pa

rametri

c bootst

rappin

g could

be con

sidered

, but

is com

putatio

nally ex

pensive

.~ W

orks on

ly with

very lo

w prob

ability q

uantile

2His

torical

Simulat

ion

VaRHS-

VaRDow

d K.

2002

Measu

ring Ma

rket Ri

skChi

chester

: Joh

n Wiley

& S

onssup

posedl

y norma

l dist

ribution

sord

ered Lo

ss and

Profit

observ

ations

choose

the cor

respond

ant

quantil

eno

calculat

ion ne

eded

(P&L)^(

number

of obs

ervatio

ns * con

fidence

level)

no esti

mation

neede

d1000

given

P&L~ fa

st com

putatio

n~ ea

sy imp

liment

ation

~ Only

allows

us to e

stimate

VaRs a

t discre

te con

fidence

interv

als det

ermine

d by th

e size o

f our

data se

t~ P

oor app

roxima

tions of

small q

uantile

s

3Filt

ered

historic

al sim

ulation

VaR

FHS-Va

RBar

one-Ad

esi G.,

Gianno

poulos

K. and

Vosper

L.

2002

Backte

sting D

erivativ

e Por

tfolios

with Fi

ltered

Histori

cal Sim

ulation

(FHS)

Europe

an Fina

ncial

Manag

eme

nt, Vol

. 8, nº 1

, pp. 31

-58

time-v

arying

volatilit

iesimp

rovem

ent of

the HS

me

thod

Using t

he HS

Garch m

odels a

re fitte

d resi

duals a

re filte

redretu

rns are

regene

rated

doing s

o on m

ultiple

passes

resu

lts in a

VaR com

putatio

n

1. GARC

H mode

l on his

torical

data

2. Para

meters

comput

ation

3. Norm

alize th

e residu

als4. C

omput

e the fo

recasti

ng volat

ility5. C

omput

e the st

ock for

ecast

1) 3) 4) 5)

based

on the

hist

orical d

ata, ga

rch

param

eters a

re esti

mated

Germa

n Bund

, BTP,

Long G

ilt, Eur

omark

, 3 m

onth sw

iss inte

rest rat

es con

tracts

4 jan 1

996 un

til 12

novem

ber 199

7

~ takes

into ac

count c

hanges

in pas

t volati

lities

~ reduc

ed num

ber of

assum

ptions a

bout th

e future

pric

es

~ not e

nough a

ttention

to ext

reme o

bserva

tions

~ negle

cts tim

e-vary

ing cor

relation

s

4Gen

eralize

d dyn

amic

GDCC

C. M. Ha

fner

Philip a

nd H.

Franse

s200

3A G

enerali

zed Dy

namic

Conditi

onal Co

rrelatio

n Mo

del for

Many A

sset

Return

s

Econom

etric In

stitute

Rep

ort EI

2003–1

8larg

e num

ber of

assets

returns

(co

rrelatio

n sensit

ivity)

Genera

lize the

DCC m

odel by

allo

wing an

assest-

specific

vola

tility

It does

so by i

ndexing

one o

f the

ARMA

param

eters t

o the

asset

1. On h

istorica

l data e

stimate

Garch

mo

del2. B

uild a d

iagonal

matrix

with th

e var

iances e

stimate

d3. C

omput

e an int

ermedia

te matri

x4. C

alculate

the con

ditionn

al cova

riance

matrix

5. Appl

y Garc

h using

this m

atrix

quasi m

aximum

like

lihood

18 Germ

an stoc

k retu

rns (DA

X) and

25 UK

stocks

in the

FTSE

7800 (x

2) retr

uns

observ

ations

~ allow

s for as

set-spe

cific

hetero

geneity

in the

correla

tion

structu

re~ fl

exibility

gain fo

r the

dynam

ics of t

he cor

relation

s

~ no as

ymptoti

c propr

eties

~ quick

ly incre

asing di

mensio

ns

5Con

ditionn

al aut

oregre

ssive va

lue at

riskCaV

iarEng

le R. an

d Ma

nganel

li S. 200

4(19

9 9)

CAViaR

: Condi

tional

Autore

gressiv

e Value

at Risk

by Reg

ression

Qua

ntiles

Journa

l of

Busine

ss &

Econom

ic Sta

tistics,

Vol

. 22, nº

4, p

p. 367-

381

to capt

ure lev

erage e

ffects

and oth

er nonl

inear

charact

eristics

of the

financ

ial retu

rn

Instead

of mo

deling

the wh

ole

distribu

tion, we

model

the

quantil

e direc

tly

Choose

the app

roach f

or the f

unction

f :1. A

daptive

2. Prop

ortiona

l symm

etric ad

aptive

3. Sym

metric

absolut

e value

4. Asym

metric

absolu

te value

5. Assy

metric

slope

6. Indi

rect GA

RCH(1,1

)

genetic

algorit

hm to

optimi

ze a no

n-diff

erentia

ble

object

ive fun

ction

(cannot

be op

timized

usin

g tradit

ional

estima

tion me

thods)

3392 d

aily pri

ces fro

m Dat

astream

for Ge

neral

Motors

, IBM a

nd S&P

500

From A

pril 7, 1

986 to

April 7,

1999

(includ

ing the

crash o

f the 19

87)

~ ability

to ada

pt to n

ew risk

environ

ments

~ diffic

ulties c

hoosing

the app

roprait

e CaVi

aR mo

del (un

less usi

ng diffe

rent te

sts)

6Dyn

amic

Additiv

e Qua

ntile

DAQC. G

ouriero

ux and

J. Jasia

k200

6Dyn

amic q

uantile

model

sManus

cript

, Univer

sity

of Toro

ntouni

variate

return

scom

putatio

n of Va

RIt is

an imp

rovem

ent to

the

quantil

e mode

ls that

incopor

ates dy

namic e

ffects

1. Choo

se the

quantil

e funct

ion2. A

ppliyin

g the es

timatio

n meth

od,

we get

the par

amete

rs3. S

imulate

future

values

Optimi

zation

criterio

n bas

ed on

the inv

erse

KLIC me

thod

Stock r

eturn f

rom

Toront

o Stock

exchan

ge247

daily o

bserva

tions

Betwee

n octo

ber 20

02 and

octobe

r 2003

~ easy e

stimable

~ ensur

es the

monot

onicity

of con

ditinal

quantil

e estim

ates

(in opp

osition

with p

reviou

s mo

dels)

~ many

tests r

ecomm

ended

in orde

r to cho

ose

the ade

quate q

uantile

functio

n

7Qua

ntile

Factor

Model

QFMC. G

ouriero

ux and

J. Jasia

k200

6Dyn

amic q

uantile

model

sManus

cript

, Univer

sity

of Toro

nto

Dynam

ics of c

ross-se

ctional

distribu

tions of

return

sind

ividiual

incom

escor

porate

ratings

It is an

improv

ement

to the

qua

ntile m

odels th

at inco

porate

s dynam

ic effec

ts for

a panel

frame

work

1. Facto

r analys

is to de

termine

K2. E

stimate

the qu

antiles

(kalma

n filte

r)3. C

omput

e the m

odel of

the fac

tors

(AR)

4. Get t

he qua

ntile

where F

are fac

tors (po

sitif) an

d Q are

the qu

antiles

Kalman f

ilter

Log-like

lihood

optimi

zation

40 larg

est sto

cks tra

ded

on the

TSX247

daily o

bserva

tions

Betwee

n octo

ber 20

02 and

octobe

r 2003

~ prese

rves th

e orde

ring of

succes

sive qu

antiles

~ idd o

n the p

ast ass

umptio

ns

8Gen

eralise

d Smo

oth

transitio

n con

ditiona

l cor

relation

GSTCC

T. Shio

hama,

M. Hal

lin, D.

Vereda

s and

M. Tan

iguchi

2010

Dynam

ic portf

olio

optimi

zation

using

genera

lized d

ynamic

con

ditiona

l het

eroske

dastic f

actor

model

s

J. Japan

Sta

tist. So

c. Vol

. 40 No

. 1 14

5–166

large p

anels o

f financ

ial time

seri

es

The aim

is find

ing the

perfec

t ass

ets allo

cation

via wor

king

on the

idiosyn

cratic p

art of t

he risk

, and n

ot the

return a

s a who

le

1. Extra

ct the

idiosyn

cratic

compon

ents

2. Com

pute th

e VaR

of each

com

ponent

3. C

onstruc

t the p

ortfolio

by min

imising

the Va

R (with

respect

to the

weight

s)

1)

where

is th

e comm

on fact

or, is

the

idiosyn

cratic c

ompon

ent and

the m

ean of

2) Dete

rmine t

he num

ber of

commo

n shock

(for th

e idiosy

ncratic

com

ponent

, using

Hallin a

nd Las

ka (200

7) proc

edure

3) Reco

nstruc

t estim

ators f

or each

compon

ent

4) Assu

me tha

t

wher

e H is t

he con

ditionn

al cova

riance

matrix

and z w

hite no

ise idd

5) Appl

y multi

variate

GARCH

on the

idiosyn

cratic p

art to g

et the

correla

tions (D

CC or C

CC) ?

Hallan

and Lis

ka com

mon sh

ock fac

tor esti

mator

daily re

turns of

the

Tokyo s

tock ex

change

from Jan

uary 4,

2001

to Jun

e 29, 20

07 159

7 days

33

indust

ries

~ few r

estrictio

ns on th

e data

(on

ly seco

nd ord

er stat

ionnar

ity)

~ since

the idio

syncrat

ic com

ponent

s are n

ot obs

erved,

they ha

ve to b

e estim

ated an

d henc

e the

results

may be

affect

ed by t

he cho

ice of t

he mo

del

9Dyn

amic

Factor

Model

DFM-Va

RS.A

ramont

e,M.

Rodrigu

ezy

and J. W

u201

2Dyn

amic fa

ctor Va

lue-at-

Risk for

large

hetero

skedas

tic portf

olioshttp

://ssrn

.com

/abstra

ct=184

5846

applied

to por

tfolios

with ti

me-

varying

weight

s

Capturi

ng the

time-v

arying

volatilit

ies and

correla

tions of

a larg

e num

ber of

financia

l var

iables t

hrough

other l

atent

factors

to red

uce siz

e for an

ade

quate V

aR esti

mation

1. Appl

y a com

ponent

decom

positio

n to

the ret

urns (t

o reduc

e the si

ze and

work

on late

nt facto

rs)2. T

he volat

ility of

the ret

urn is m

odelled

3. Q

is mode

lled as

a DCC

specific

ation

4. Fore

cast th

e return

s using

the DC

C par

amete

rs

1) 2) 3) 4)

whe

re A,H,Q

and z a

re defin

ed in th

e DCC

model

six step

s estim

ation

proced

ure de

tailed

in the

relativ

e pape

r

daily re

turns on

the

stocks i

n CRSP

that

commo

nly trad

e on the

NYS

E, AME

X, and

NASDAQ

non-mi

ssing re

turns on

all t

rading

days (2

007-

2009)

~ well r

eprese

ntative

in case

of syst

ematic

risk~ co

mputa

tional e

fficien

cy~ d

o not a

llow for

foreca

sting m

odels th

at are

non-lin

ear

10Ind

epende

nt Com

ponent

ana

lysis

GARCH

model

ICA-

GARCH

D. Xu an

d T.

S. Wirja

nto201

4On

the Co

mputa

tion of

Large P

ortfolio

's VaRs

und

er Multi

variate

GARCH

Vol

atility

not

publish

edlarg

e num

ber of

assets

portfol

ios tha

t are

charact

erized

by nonl

inearit

y and

nonno

rmality

Model

ing a m

ultivar

iate

GARCH

compos

ition u

sing a

linear c

ombin

ation o

f sever

al uni

variate

GARCH

model

s using

the ICA

decom

positio

n

1. Appl

y the IC

A techn

ique to

the

multiv

ariate a

sset re

turns da

ta2. F

it the G

ARCH m

odel to

each IC

3. G

enerate

the res

ultinng

foreca

sted

returns

1) 2) 3)

severa

l estim

ation

algorith

ms for

the ICA

pro

cess

tests fo

r IC's

indepe

ndence

~ 1st p

ortfolio

: 6 cur

rency e

xchang

e rates

~ 2nd p

ortfolio

: 4 stoc

k ind

ices (Ja

n 1998

to Dec

200

5) ~ 3

rd portf

olio: 18

ind

ividual

stocks

traded

in the

New Y

ork Sto

ck Exc

hange (

NYSE)

~ comp

utation

ally tra

ctable

metho

d~ m

ore sta

ble tha

n othe

r~ ex

plain th

e non-

gaussia

n beh

aviour o

f financ

ial data

compar

able mo

dels

~ Garch

model

s only a

re sens

itive to

thema

gnitude

of the

excess

of retu

rns and

not to

the

sign o

f this e

xcess o

f return

Inconve

nients

Idea

VaR cal

culation

steps

noMo

del Na

meSho

rtSou

rceTyp

eAdv

antage

sSui

table f

or Con

ditionn

al Non

-con

ditionn

alEqu

ation

Estima

tions

Applica

tions

~

0,

√1,

∀2

1√

1

1

,,

,,

,

;

,,

,

,

,,

χ

ϵ

/

/ ∗

∗ = A

/

~ 0,

1 ,

,

Table 5: Different forecasting methodologies

5 Sensitivity Based approach (SBA)

5.1 Introducing the approach

This new method would require banks to use prices and rate sensitivitiesin order to compute their capital charge. This revised (sensitivity-based)standardized approach would capture more granular or complex risk factorsacross different asset classes in the trading book (cf. BCBS (2015)).

It builds on the standardized framework tested in the trading book QISconducted in the second half of 2014 (cf. Basel (2014)).

The proposed methodology covers the delta and optionality risk: generalinterest rate risk, credit spread risk of non-securitization and securitizationexposures, equity, commodity and FX risk.

Vega and curvature risk measurements are under development in order tomeasure the sensitivity of the value of an option with respect to a modifica-tion in volatility and the rate of change of delta.

5.2 Implementation reasons

• The approach must provide a method for calculating capital require-ments for banks with a level of trading activity that does not requiresophisticated measurement of market risk.

• It provides a fall back in the event that a bank′s internal model isdeemed inadequate, including the potential use as add-on or floor toan internal model-based charge.

• The approach should facilitate consistent and comparable reporting ofmarket risk across banks and jurisdictions.

5.3 Computational steps

We first compute the net sensitivity of the bond (relative 1 bps change)and multiply it by its corresponding risk weight in order to get the weightedsensitivity. We note that for each maturity a different risk weight is allocatedbased on a matrix provided by the Basel committee. For each currency, the’average’ is computed as the square root of the sum of squared single weightedsensitivities and double products of these latter weighted by given, maturitybased, correlation coefficients. Aggregation on a portfolio level is another

sum of the squared capital charges computed for each currency plus thedouble products weighted by a factor of 0.5 fixed by Basel. The method isas follows:

1. Get the observed yield and price on the market.

2. Compute the net sensitivity of each instrument and recalculate theprice.