impact of age of the company on performance of initial

TRANSCRIPT

Impact of age of the company on Performance of Initial Public

Offering (IPOs) in India

Dr. Srinivasa Rao Dokku

Assistant Professor,

Department of Business Administration, P.V.P. Siddhartha Institute of Technology,

Kanuru, Vijayawada Andhra Pradesh, India, 520 007.

Email: [email protected].

Dr. Rajesh C. Jampala

Professor& Head,

Department of Commerce and Business Administration,

P.B. Siddhartha College of Arts & Science, Vijayawada

Andhra Pradesh, India, 520 010., Email: [email protected].

Dr. P. Adi Lakshmi

Professor & Head,

Department of Business Administration, P.V.P. Siddhartha Institute of Technology,

Kanuru, Vijayawada, Andhra Pradesh, India, 520 007.

Email: [email protected].

Abstract:

Age could actually help firms become more efficient. Over time, firms discover what they are

good at and learn how to do things better. They specialize and find ways to standardize,

coordinate, and speed up their production processes, as well as to reduce costs and improve

quality. The previous findings of various researchers suggest that, there is significant relation

between age of the firm and aftermarket performance. This paper focuses on the evaluation of

price performance of IPOs up to a period of 36 months including the listing day. In this paper the

main emphasis is on the study of age of the company on after market performance of the selected

IPOs in short-run and as well as long-run. The paper presents fresh evidence on IPO

performance, i.e., short-run underpricing and long-run underperformance for 146 Indian IPOs

issued during the period 2007-2008.

Key words: Age, Returns, IPOs, Short-run, and Long-run

1. Introduction:

The age of the company could actually help firms become more efficient. Over time, firms

discover what they are good at and learn how to do things better They specialize and find ways

to standardize, coordinate, and speed up their production processes, as well as to reduce costs

and improve quality (Ericson and Pakes, 1995). Age of the firm defined in terms of years, is

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:946

one of the most popular proxies on company characteristics. High rank investment banks

generally choose companies with a longer operational history. Age of the IPO firm signals the

level of maturity of the company. In this study, age has been measured by the difference between

the date of incorporation and the date at which the company goes public.

A Shokand (2013), edited volume on “Long term performance of Indian IPOs” analyzed the

impact of firm age and its performance in stock market. Firm age at the time of IPO was

computed from the date of incorporation to the date of IPO, varied from less than one year to

over 98 years. Age of the firm is also one of the most important factors which affect the

performance of IPOs in long-term period. It is generally believed that there is a strong

relationship between the age and the long-run performance of IPOs. IPOs of companies, having

the age more than 50 years but less than or equal to 60 years were showing highest returns up to

the end of three months as compared to all other groups. These results were found to be

statistically significant at five percent level. Thereafter, IPOs having the age group above 60

years were indicating the maximum returns up to the end of the third year as compared to other

groups and the results were also found to be statistically significant at five percent level. The

study also highlighted the fact that returns of the group having age less than 10 years and age

group having age more than 10 years but less than or equal to 20 years were also showing

positive returns and most of their results were statistically significant at one percent level.

The age of the company is supposed to have an impact on the level of the underpricing after

initial public offering. First of all, companies of recent origin present a bigger uncertainty ex-ante

when compared to the established companies. It is due to the fact that the young companies may

be less followed by financial analysists because they may not have enough published historical

financial data. Second, the availability of the information about companies operating for several

years, contributes to reduce the asymmetry of information during the listing period

(Hensler(1997)). This uncertainty, as for the future prospects of the company, will be translated

by an increase of the underpricing(Bilson (2003)).

Ritter finds a positive monotone relationship between firm age and IPO aftermarket

performance, with the oldest category of firms (over 20 years) showing positive abnormal

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:947

returns. David T. Clark (2002) also finds common stock initial public offerings- In the

aggregate; the data shows a statistically significant correlation between firm age-at-IPO and post-

IPO excess returns. However, when the firms were disaggregated into technology and non-

technology panels, the data suggested that the relationship between age and returns is different

between the two categories. Among technology enterprises, very young firms outperformed

older firms, though the difference in return between the two age groups did not rise to a high

level of statistical significance. Their study also offers the alternative idea that the market may

have underestimated the unusually strong prospects of this group of young technology IPOs

relative to older technology firms. Non-technology firms, on the other hand, exhibited a positive

monotone correlation between firm age and excess holding period returns. A regression

confirmed this positive relationship, established at a high degree of statistical significance. The

average age of a firm going public during the 1990s was the lowest the market has witnessed

since the economic reforms in India. With a mean time from incorporation to public offering of

roughly ten years, the average 1990’s IPO was about one-third as old as a typical mid-20th

century IPO. According to Jovanovic and Roussea study in an efficient market, the aftermarket

price of an IPO will almost immediately reflect the growth potential of the firm, based on all

available information. Average risk-adjusted returns going forward should match the market,

regardless of the age-at-IPO of a firm.

This study examines the relationship between the age of firm at the time of IPO and long-run

aftermarket performance. In effect, the study will test the efficiency of the market with regard to

the IPO’s during the 2007 and 2008 period by measuring three-year holding period excess stock

returns relative to firm age-at-IPO.

2. Methodology and Sample

The study is an evaluation work on the impact of age of the firm on performance of IPOs in

India. In the early periods of financial reforms, especially since 1991 there were hardly any

restrictions on companies to go public and fixing premium. However, companies are expected to

provide justification in fixing premium on all their public issues. The sample consists of 146

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:948

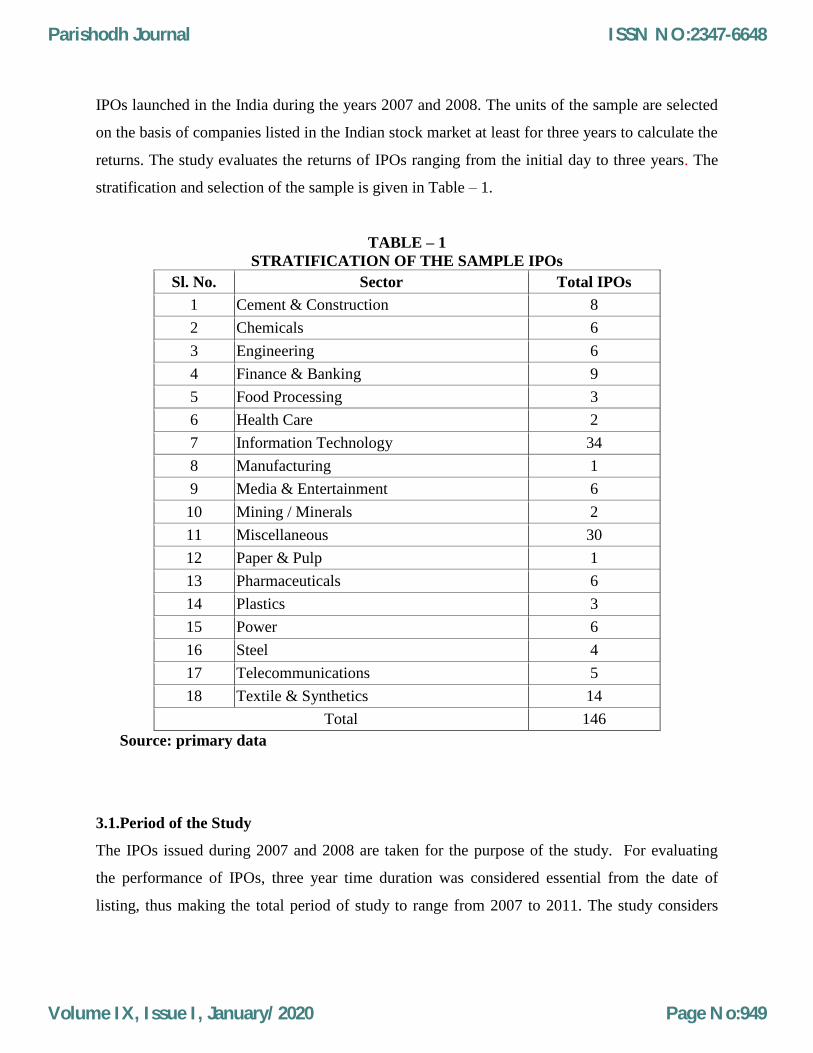

IPOs launched in the India during the years 2007 and 2008. The units of the sample are selected

on the basis of companies listed in the Indian stock market at least for three years to calculate the

returns. The study evaluates the returns of IPOs ranging from the initial day to three years. The

stratification and selection of the sample is given in Table – 1.

TABLE – 1

STRATIFICATION OF THE SAMPLE IPOs

Sl. No. Sector Total IPOs

1 Cement & Construction 8

2 Chemicals 6

3 Engineering 6

4 Finance & Banking 9

5 Food Processing 3

6 Health Care 2

7 Information Technology 34

8 Manufacturing 1

9 Media & Entertainment 6

10 Mining / Minerals 2

11 Miscellaneous 30

12 Paper & Pulp 1

13 Pharmaceuticals 6

14 Plastics 3

15 Power 6

16 Steel 4

17 Telecommunications 5

18 Textile & Synthetics 14

Total 146

Source: primary data

3.1.Period of the Study

The IPOs issued during 2007 and 2008 are taken for the purpose of the study. For evaluating

the performance of IPOs, three year time duration was considered essential from the date of

listing, thus making the total period of study to range from 2007 to 2011. The study considers

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:949

age of the company at the time of listing and returns at initial day, one month, one year, two

years and three year. The study identifies short-run as well as long-run performance.

3.2.Sources of Data

The sample used in this study consists of all Indian IPOs issued by firms which went public from

January 2007 to December, 2008. The prospectuses issued by firms were considered to collect

data prior to the listing which includes the offer price, issue details, dates of public issue, issue

amount, age of the firm, and financial information from balance sheets and income statements.

Moreover, the SEBI Fact book, an annual publication issued by the SEBI to disseminate

information to investors, is used to collect information on the main market indicators as well as

information pertaining to public issues. In addition, regular price histories were collected for

each sample firm through the period 2007-2013. The stock quotations were collected primarily

from moneycontrol.com, bseindia.com, yahoofinance.com and other relevant company websites

for analysis purpose.

Data analysis and interpretation

4. Descriptive Statistics of the sample companies

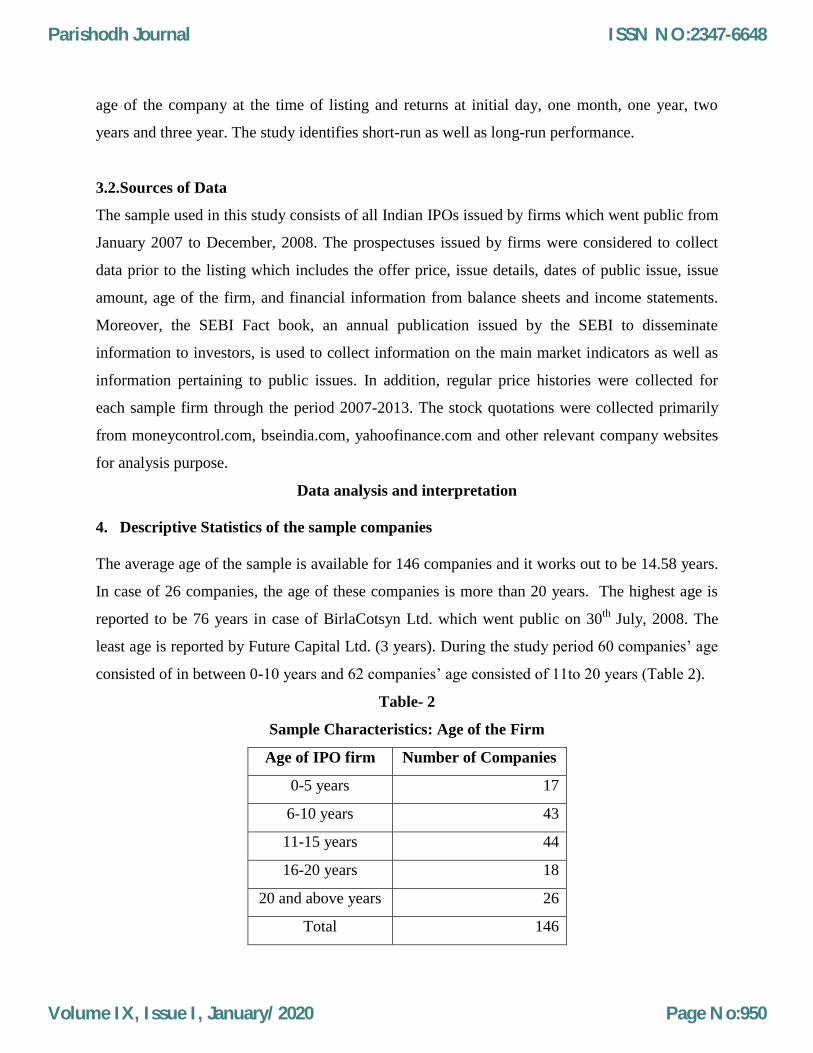

The average age of the sample is available for 146 companies and it works out to be 14.58 years.

In case of 26 companies, the age of these companies is more than 20 years. The highest age is

reported to be 76 years in case of BirlaCotsyn Ltd. which went public on 30th

July, 2008. The

least age is reported by Future Capital Ltd. (3 years). During the study period 60 companies’ age

consisted of in between 0-10 years and 62 companies’ age consisted of 11to 20 years (Table 2).

Table- 2

Sample Characteristics: Age of the Firm

Age of IPO firm Number of Companies

0-5 years 17

6-10 years 43

11-15 years 44

16-20 years 18

20 and above years 26

Total 146

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:950

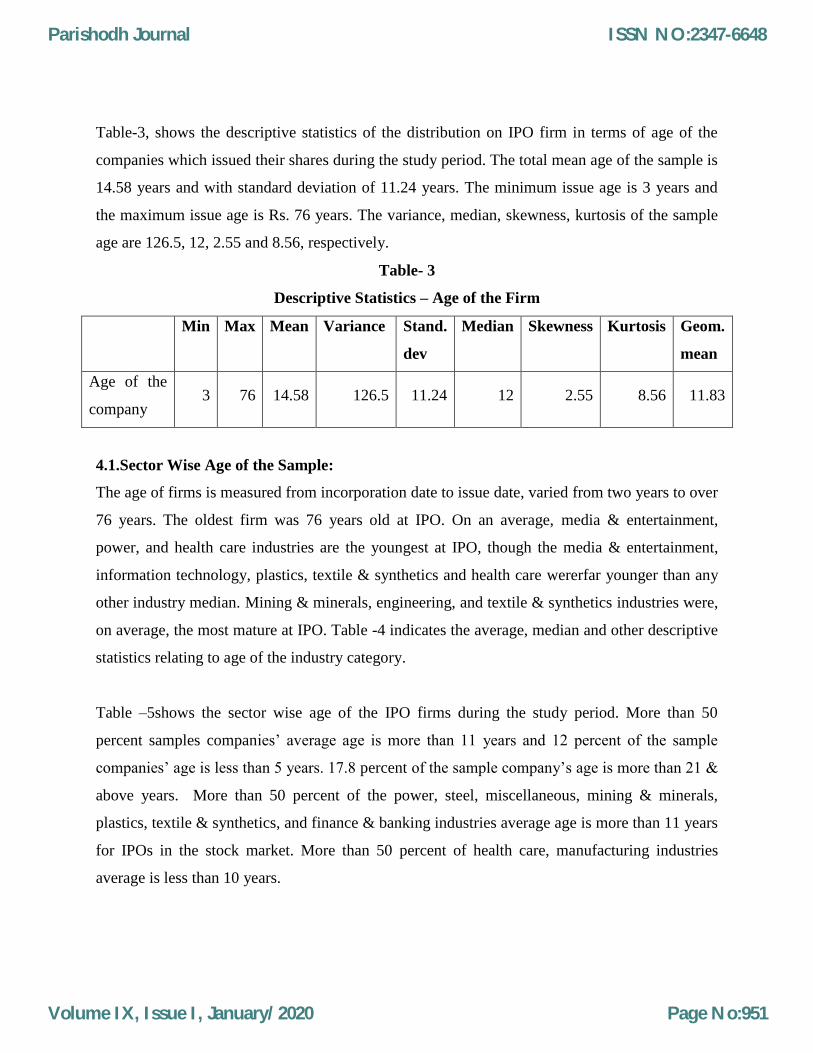

Table-3, shows the descriptive statistics of the distribution on IPO firm in terms of age of the

companies which issued their shares during the study period. The total mean age of the sample is

14.58 years and with standard deviation of 11.24 years. The minimum issue age is 3 years and

the maximum issue age is Rs. 76 years. The variance, median, skewness, kurtosis of the sample

age are 126.5, 12, 2.55 and 8.56, respectively.

Table- 3

Descriptive Statistics – Age of the Firm

Min Max Mean Variance Stand.

dev

Median Skewness Kurtosis Geom.

mean

Age of the

company 3 76 14.58 126.5 11.24 12 2.55 8.56 11.83

4.1.Sector Wise Age of the Sample:

The age of firms is measured from incorporation date to issue date, varied from two years to over

76 years. The oldest firm was 76 years old at IPO. On an average, media & entertainment,

power, and health care industries are the youngest at IPO, though the media & entertainment,

information technology, plastics, textile & synthetics and health care wererfar younger than any

other industry median. Mining & minerals, engineering, and textile & synthetics industries were,

on average, the most mature at IPO. Table -4 indicates the average, median and other descriptive

statistics relating to age of the industry category.

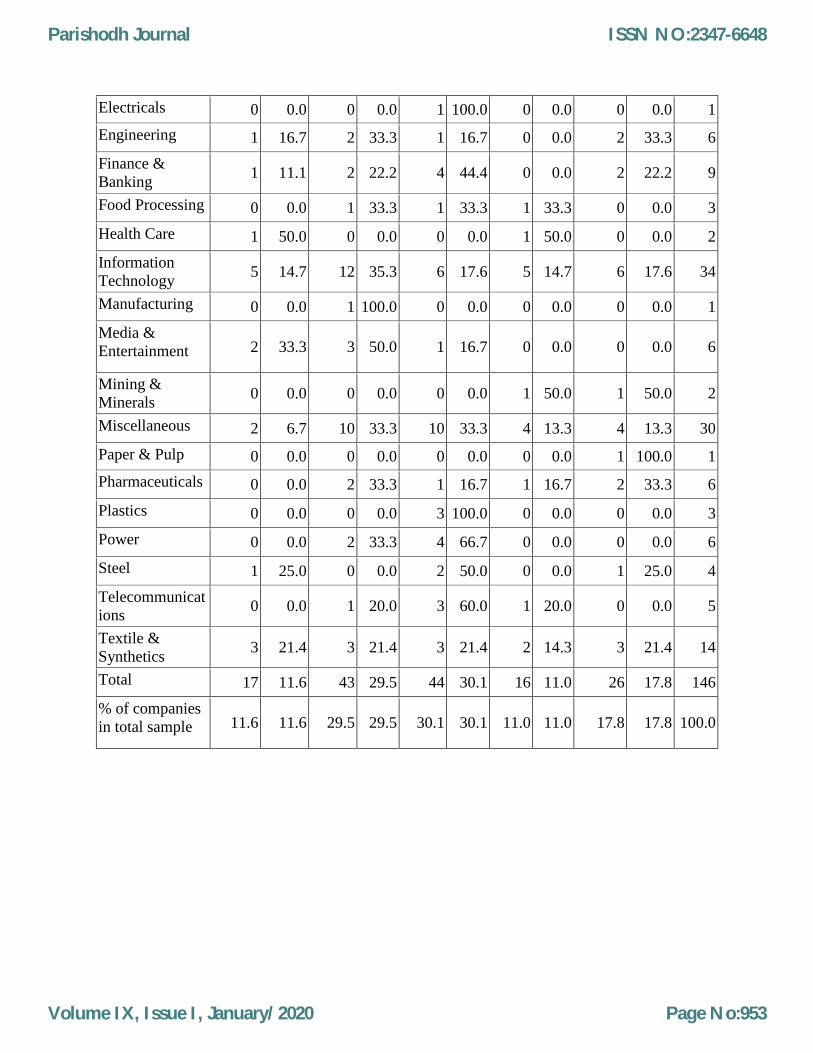

Table –5shows the sector wise age of the IPO firms during the study period. More than 50

percent samples companies’ average age is more than 11 years and 12 percent of the sample

companies’ age is less than 5 years. 17.8 percent of the sample company’s age is more than 21 &

above years. More than 50 percent of the power, steel, miscellaneous, mining & minerals,

plastics, textile & synthetics, and finance & banking industries average age is more than 11 years

for IPOs in the stock market. More than 50 percent of health care, manufacturing industries

average is less than 10 years.

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:951

Table- 4

Age Data by Industry (in Years)

Industry Total Min Max Mean Variance Stand.

dev Median Skewness Kurtosis

Geom.

mean

Cement &

Construction 8 8 23 12.75 38.5 6.20 10.5 1.21 -.28 11.66

Chemicals 5 5 19 20.8 318.2 7.9 12 1.20 1.00 15.42

Electricals 1 5 - - - - - - - -

Engineering 6 5 30 15.16 112.59 4.33 10.5 0.8 -1.67 12.32

Finance & Banking 9 2 39 14.11 119.11 3.63 12 1.69 3.27 10.84

Food Processing 3 7 18 12.33 30.33 5.50 12 0.271 -2.33 11.17

Health Care 2 4 18 11 98 9.89 11 0 -2.75 8.48

Information

Technology 34 4 57 15.11 159.25 12.61 10.5 1.91 3.46 11.72

Manufacturing 1 8 - - - - - - - -

Media &

Entertainment 6 6 13 7.33 10.66 3.26 6.5 1.15 1.10 6.79

Mining & Minerals 2 20 21 20.5 0.5 0.70 20.5 0 -2.75 20.49

Miscellaneous 30 4 31 13.46 50.53 7.10 12 1.34 1.52 11.92

Paper & Pulp 1 28 - - - - - - - -

Pharmaceuticals 6 7 30 17.33 85.46 9.24 15.5 0.39 -1.79 15.22

Plastics 3 11 13 11.66 1.33 1.15 11 1.73 -2.33 11.62

Power 6 6 13 10.33 9.06 3.01 12 -.94 -1.56 9.90

Steel 4 5 23 12.75 56.25 7.5 11.5 0.95 1.93 11.09

Telecommunications 5 9 19 13.4 13.3 3.64 13 0.75 1.62 13.01

Textile & Synthetics 14 4 76 19.78 474.48 21.78 11 1.97 3.41 12.98

Total 146 2 76 14.58 126.5 11.24 12 2.55 8.56 11.83

Table-5

Sector Wise Age of the Sample

Industry 2-5

years

% in

total

6-10

years

% in

total

11-15

years

% in

total

16-20

years

% in

total

21 &

above

years

% in

total Total

Cement &

Construction 0 0.0 4 50.0 2 25.0 0 0.0 2 25.0 8

Chemicals 1 20.0 0 0.0 2 40.0 0 0.0 2 40.0 5

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:952

Electricals 0 0.0 0 0.0 1 100.0 0 0.0 0 0.0 1

Engineering 1 16.7 2 33.3 1 16.7 0 0.0 2 33.3 6

Finance &

Banking 1 11.1 2 22.2 4 44.4 0 0.0 2 22.2 9

Food Processing 0 0.0 1 33.3 1 33.3 1 33.3 0 0.0 3

Health Care 1 50.0 0 0.0 0 0.0 1 50.0 0 0.0 2

Information

Technology 5 14.7 12 35.3 6 17.6 5 14.7 6 17.6 34

Manufacturing 0 0.0 1 100.0 0 0.0 0 0.0 0 0.0 1

Media &

Entertainment 2 33.3 3 50.0 1 16.7 0 0.0 0 0.0 6

Mining &

Minerals 0 0.0 0 0.0 0 0.0 1 50.0 1 50.0 2

Miscellaneous 2 6.7 10 33.3 10 33.3 4 13.3 4 13.3 30

Paper & Pulp 0 0.0 0 0.0 0 0.0 0 0.0 1 100.0 1

Pharmaceuticals 0 0.0 2 33.3 1 16.7 1 16.7 2 33.3 6

Plastics 0 0.0 0 0.0 3 100.0 0 0.0 0 0.0 3

Power 0 0.0 2 33.3 4 66.7 0 0.0 0 0.0 6

Steel 1 25.0 0 0.0 2 50.0 0 0.0 1 25.0 4

Telecommunicat

ions 0 0.0 1 20.0 3 60.0 1 20.0 0 0.0 5

Textile &

Synthetics 3 21.4 3 21.4 3 21.4 2 14.3 3 21.4 14

Total 17 11.6 43 29.5 44 30.1 16 11.0 26 17.8 146

% of companies

in total sample 11.6 11.6 29.5 29.5 30.1 30.1 11.0 11.0 17.8 17.8 100.0

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:953

Volume IX, Issue I, January/2020 Page No:922

4.2.IPOs Returns in Short Run and Long Run

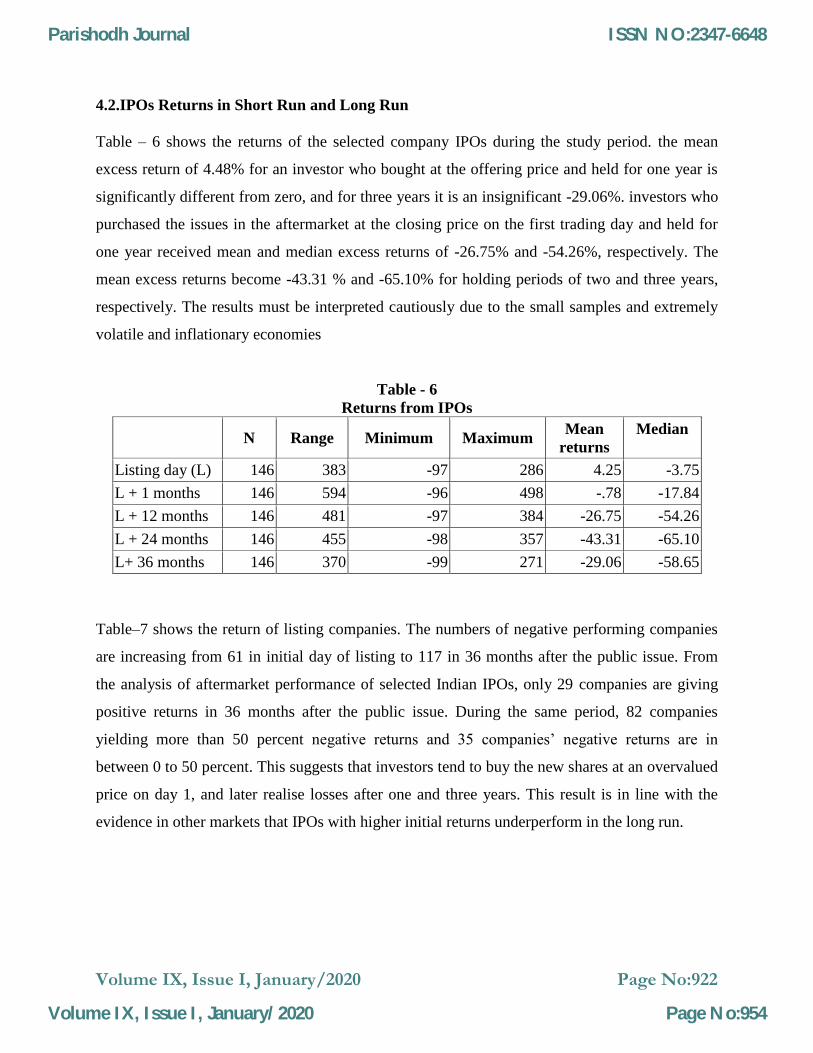

Table – 6 shows the returns of the selected company IPOs during the study period. the mean

excess return of 4.48% for an investor who bought at the offering price and held for one year is

significantly different from zero, and for three years it is an insignificant -29.06%. investors who

purchased the issues in the aftermarket at the closing price on the first trading day and held for

one year received mean and median excess returns of -26.75% and -54.26%, respectively. The

mean excess returns become -43.31 % and -65.10% for holding periods of two and three years,

respectively. The results must be interpreted cautiously due to the small samples and extremely

volatile and inflationary economies

Table - 6

Returns from IPOs

N Range Minimum Maximum Mean

returns

Median

Listing day (L) 146 383 -97 286 4.25 -3.75

L + 1 months 146 594 -96 498 -.78 -17.84

L + 12 months 146 481 -97 384 -26.75 -54.26

L + 24 months 146 455 -98 357 -43.31 -65.10

L+ 36 months 146 370 -99 271 -29.06 -58.65

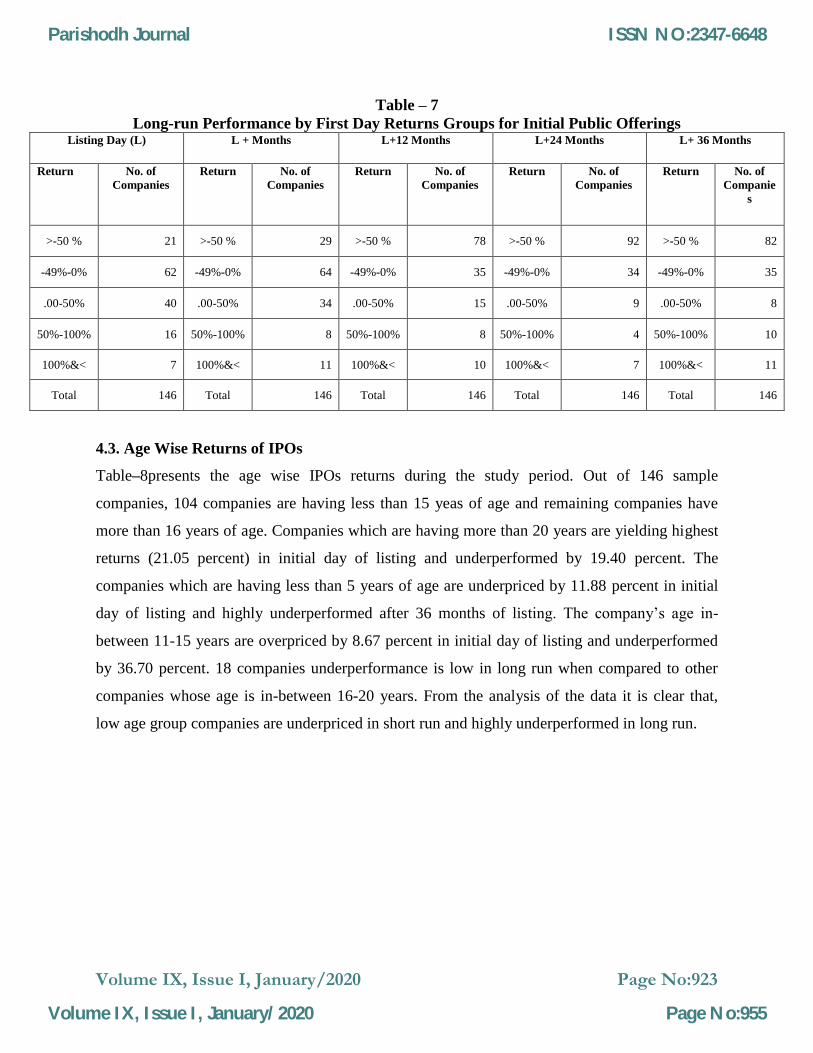

Table–7 shows the return of listing companies. The numbers of negative performing companies

are increasing from 61 in initial day of listing to 117 in 36 months after the public issue. From

the analysis of aftermarket performance of selected Indian IPOs, only 29 companies are giving

positive returns in 36 months after the public issue. During the same period, 82 companies

yielding more than 50 percent negative returns and 35 companies’ negative returns are in

between 0 to 50 percent. This suggests that investors tend to buy the new shares at an overvalued

price on day 1, and later realise losses after one and three years. This result is in line with the

evidence in other markets that IPOs with higher initial returns underperform in the long run.

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:954

Volume IX, Issue I, January/2020 Page No:923

Table – 7

Long-run Performance by First Day Returns Groups for Initial Public Offerings Listing Day (L) L + Months L+12 Months L+24 Months L+ 36 Months

Return No. of

Companies

Return No. of

Companies

Return No. of

Companies

Return No. of

Companies

Return No. of

Companie

s

>-50 % 21 >-50 % 29 >-50 % 78 >-50 % 92 >-50 % 82

-49%-0% 62 -49%-0% 64 -49%-0% 35 -49%-0% 34 -49%-0% 35

.00-50% 40 .00-50% 34 .00-50% 15 .00-50% 9 .00-50% 8

50%-100% 16 50%-100% 8 50%-100% 8 50%-100% 4 50%-100% 10

100%&< 7 100%&< 11 100%&< 10 100%&< 7 100%&< 11

Total 146 Total 146 Total 146 Total 146 Total 146

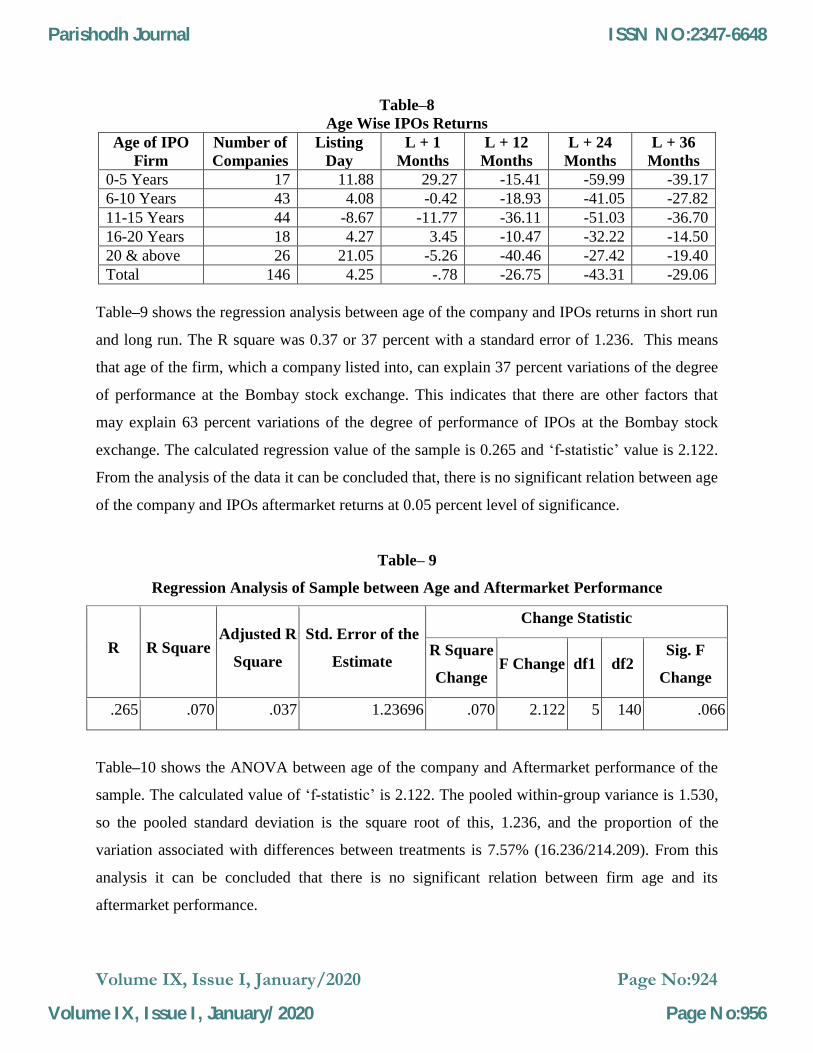

4.3. Age Wise Returns of IPOs

Table–8presents the age wise IPOs returns during the study period. Out of 146 sample

companies, 104 companies are having less than 15 yeas of age and remaining companies have

more than 16 years of age. Companies which are having more than 20 years are yielding highest

returns (21.05 percent) in initial day of listing and underperformed by 19.40 percent. The

companies which are having less than 5 years of age are underpriced by 11.88 percent in initial

day of listing and highly underperformed after 36 months of listing. The company’s age in-

between 11-15 years are overpriced by 8.67 percent in initial day of listing and underperformed

by 36.70 percent. 18 companies underperformance is low in long run when compared to other

companies whose age is in-between 16-20 years. From the analysis of the data it is clear that,

low age group companies are underpriced in short run and highly underperformed in long run.

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:955

Volume IX, Issue I, January/2020 Page No:924

Table–8

Age Wise IPOs Returns

Age of IPO

Firm

Number of

Companies

Listing

Day

L + 1

Months

L + 12

Months

L + 24

Months

L + 36

Months

0-5 Years 17 11.88 29.27 -15.41 -59.99 -39.17

6-10 Years 43 4.08 -0.42 -18.93 -41.05 -27.82

11-15 Years 44 -8.67 -11.77 -36.11 -51.03 -36.70

16-20 Years 18 4.27 3.45 -10.47 -32.22 -14.50

20 & above 26 21.05 -5.26 -40.46 -27.42 -19.40

Total 146 4.25 -.78 -26.75 -43.31 -29.06

Table–9 shows the regression analysis between age of the company and IPOs returns in short run

and long run. The R square was 0.37 or 37 percent with a standard error of 1.236. This means

that age of the firm, which a company listed into, can explain 37 percent variations of the degree

of performance at the Bombay stock exchange. This indicates that there are other factors that

may explain 63 percent variations of the degree of performance of IPOs at the Bombay stock

exchange. The calculated regression value of the sample is 0.265 and ‘f-statistic’ value is 2.122.

From the analysis of the data it can be concluded that, there is no significant relation between age

of the company and IPOs aftermarket returns at 0.05 percent level of significance.

Table– 9

Regression Analysis of Sample between Age and Aftermarket Performance

R R Square Adjusted R

Square

Std. Error of the

Estimate

Change Statistic

R Square

Change F Change df1 df2

Sig. F

Change

.265 .070 .037 1.23696 .070 2.122 5 140 .066

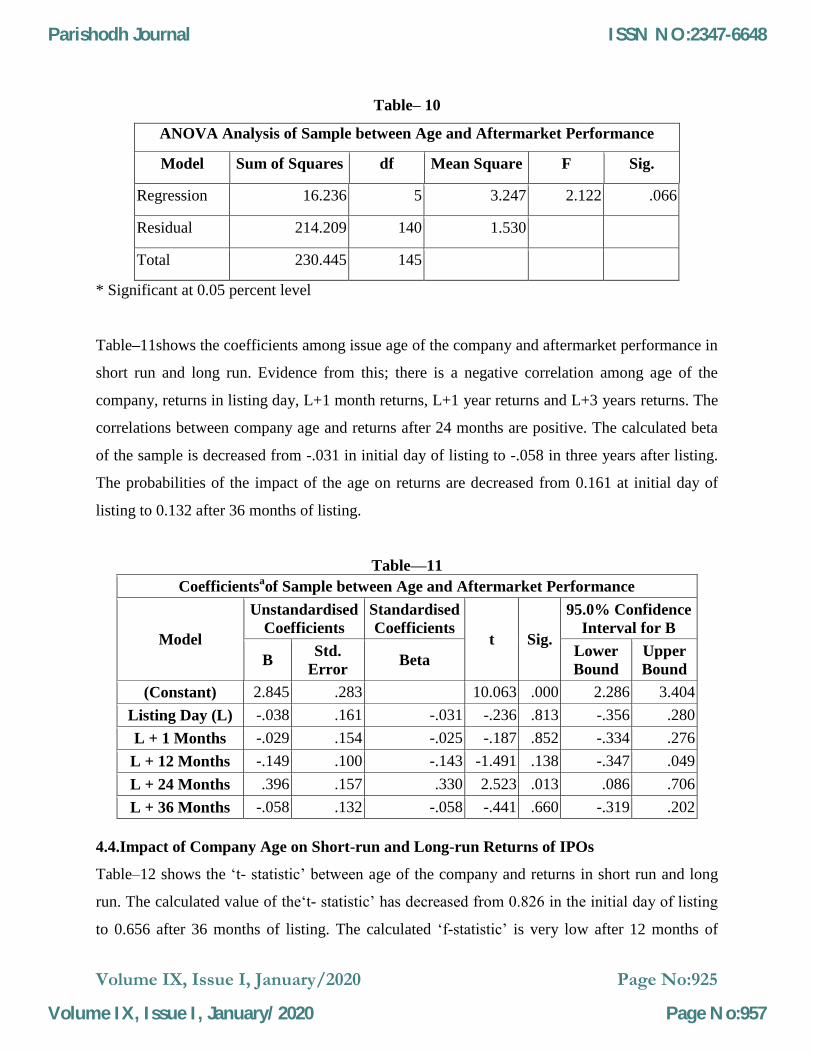

Table–10 shows the ANOVA between age of the company and Aftermarket performance of the

sample. The calculated value of ‘f-statistic’ is 2.122. The pooled within-group variance is 1.530,

so the pooled standard deviation is the square root of this, 1.236, and the proportion of the

variation associated with differences between treatments is 7.57% (16.236/214.209). From this

analysis it can be concluded that there is no significant relation between firm age and its

aftermarket performance.

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:956

Volume IX, Issue I, January/2020 Page No:925

Table– 10

ANOVA Analysis of Sample between Age and Aftermarket Performance

Model Sum of Squares df Mean Square F Sig.

Regression 16.236 5 3.247 2.122 .066

Residual 214.209 140 1.530

Total 230.445 145

* Significant at 0.05 percent level

Table–11shows the coefficients among issue age of the company and aftermarket performance in

short run and long run. Evidence from this; there is a negative correlation among age of the

company, returns in listing day, L+1 month returns, L+1 year returns and L+3 years returns. The

correlations between company age and returns after 24 months are positive. The calculated beta

of the sample is decreased from -.031 in initial day of listing to -.058 in three years after listing.

The probabilities of the impact of the age on returns are decreased from 0.161 at initial day of

listing to 0.132 after 36 months of listing.

Table—11

Coefficientsaof Sample between Age and Aftermarket Performance

Model

Unstandardised

Coefficients

Standardised

Coefficients t Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

(Constant) 2.845 .283 10.063 .000 2.286 3.404

Listing Day (L) -.038 .161 -.031 -.236 .813 -.356 .280

L + 1 Months -.029 .154 -.025 -.187 .852 -.334 .276

L + 12 Months -.149 .100 -.143 -1.491 .138 -.347 .049

L + 24 Months .396 .157 .330 2.523 .013 .086 .706

L + 36 Months -.058 .132 -.058 -.441 .660 -.319 .202

4.4.Impact of Company Age on Short-run and Long-run Returns of IPOs

Table–12 shows the ‘t- statistic’ between age of the company and returns in short run and long

run. The calculated value of the‘t- statistic’ has decreased from 0.826 in the initial day of listing

to 0.656 after 36 months of listing. The calculated ‘f-statistic’ is very low after 12 months of

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:957

Volume IX, Issue I, January/2020 Page No:926

listing and high after 24 months of listing. From the analysis of the data it can be concluded that

there is no significant relation between age of the company and aftermarket returns of the sample

in short run as well as long run at 0.05 percent level of significance.

Table –12

Company Age and Returns in Short Run and Long Run

ANOVA

Sum of

Squares df

Mean

Square F Sig.

Listing Day (L)

Between Groups 3.531 4 .883 .836 .505

Within Groups 148.962 141 1.056

Total 152.493 145

L + 1 Months

Between Groups 1.672 4 .418 .342 .849

Within Groups 172.355 141 1.222

Total 174.027 145

L + 12 Months

Between Groups 1.628 4 .407 .271 .896

Within Groups 211.393 141 1.499

Total 213.021 145

L + 24 Months

Between Groups 8.379 4 2.095 1.948 .106

Within Groups 151.649 141 1.076

Total 160.027 145

L + 36 Months

Between Groups 4.127 4 1.032 .656 .624

Within Groups 221.853 141 1.573

Total 225.979 145

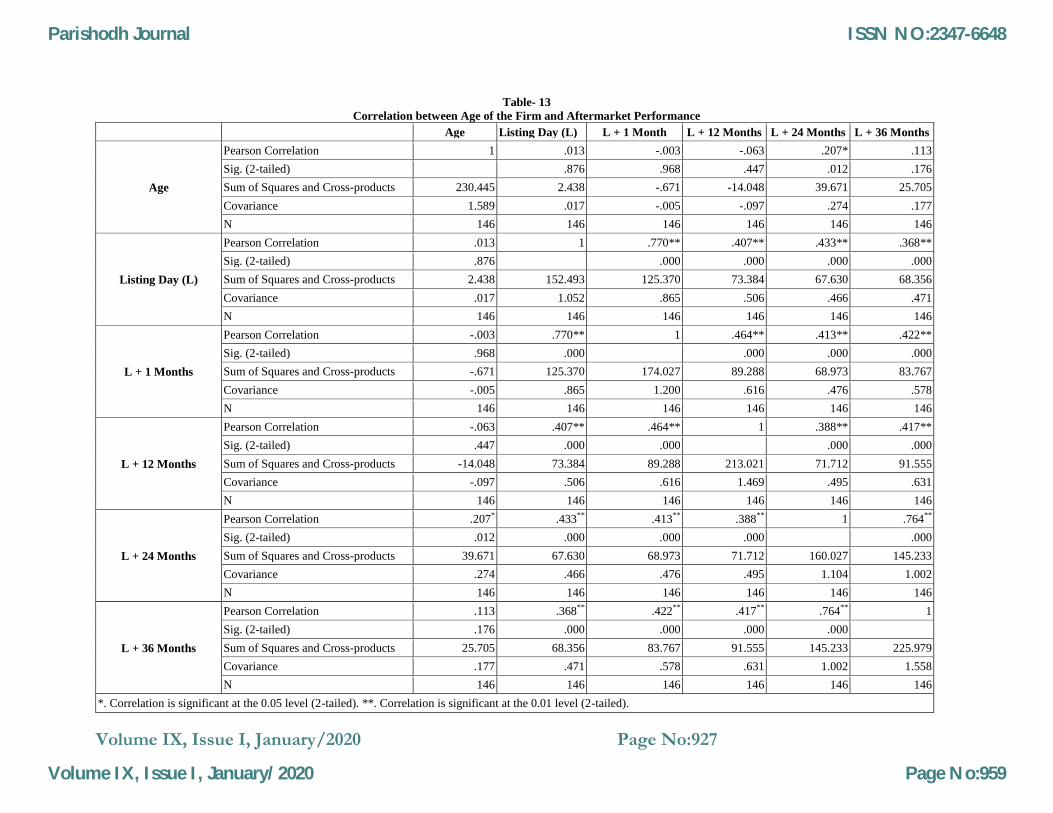

4.5.Correlation between Age of the Firms and Market performance

Table–13 shows the correlation between sample IPOs aftermarket returns and market age of the

company. The correlation is increased from 0.013 in initial day of listing to 0.113 after 36

months of listing. The IPOs returns are negatively correlated with age of the company at 1st

month & 12 months after returns. Age of the company and returns of the IPOs are positively

correlated in initial day of listing and long run (after 24 months of listing). The table-6.29 also

shows that there is a high correlation between listing day returns and one month aftermarket

returns. From the analysis of the data, the results are statistically insignificant correlation

between firm age-at-IPO and returns in short run and long run.

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:958

Volume IX, Issue I, January/2020 Page No:927

Table- 13

Correlation between Age of the Firm and Aftermarket Performance

Age Listing Day (L) L + 1 Month L + 12 Months L + 24 Months L + 36 Months

Age

Pearson Correlation 1 .013 -.003 -.063 .207* .113

Sig. (2-tailed) .876 .968 .447 .012 .176

Sum of Squares and Cross-products 230.445 2.438 -.671 -14.048 39.671 25.705

Covariance 1.589 .017 -.005 -.097 .274 .177

N 146 146 146 146 146 146

Listing Day (L)

Pearson Correlation .013 1 .770** .407** .433** .368**

Sig. (2-tailed) .876 .000 .000 .000 .000

Sum of Squares and Cross-products 2.438 152.493 125.370 73.384 67.630 68.356

Covariance .017 1.052 .865 .506 .466 .471

N 146 146 146 146 146 146

L + 1 Months

Pearson Correlation -.003 .770** 1 .464** .413** .422**

Sig. (2-tailed) .968 .000 .000 .000 .000

Sum of Squares and Cross-products -.671 125.370 174.027 89.288 68.973 83.767

Covariance -.005 .865 1.200 .616 .476 .578

N 146 146 146 146 146 146

L + 12 Months

Pearson Correlation -.063 .407** .464** 1 .388** .417**

Sig. (2-tailed) .447 .000 .000 .000 .000

Sum of Squares and Cross-products -14.048 73.384 89.288 213.021 71.712 91.555

Covariance -.097 .506 .616 1.469 .495 .631

N 146 146 146 146 146 146

L + 24 Months

Pearson Correlation .207* .433** .413** .388** 1 .764**

Sig. (2-tailed) .012 .000 .000 .000 .000

Sum of Squares and Cross-products 39.671 67.630 68.973 71.712 160.027 145.233

Covariance .274 .466 .476 .495 1.104 1.002

N 146 146 146 146 146 146

L + 36 Months

Pearson Correlation .113 .368** .422** .417** .764** 1

Sig. (2-tailed) .176 .000 .000 .000 .000

Sum of Squares and Cross-products 25.705 68.356 83.767 91.555 145.233 225.979

Covariance .177 .471 .578 .631 1.002 1.558

N 146 146 146 146 146 146

*. Correlation is significant at the 0.05 level (2-tailed). **. Correlation is significant at the 0.01 level (2-tailed).

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:959

Volume IX, Issue I, January/2020 Page No:928

5. Conclusion:

This article examines earned returns and allocation details of more than146 new offerings (Initial

Public Offering, IPO) from companies that wentpublic in India during the period 2007 to 2008.

This study finds that theaverage underpricing of equity IPOs decreased significantly from 4.25

per cent in initial day of listing to -29.06 per cent after three years of listing. The study also finds

the correlation between age of the company and returns varies from .013 initial day of listing to

.113 after 36 months of listing. The calculated value of ‘f-statistic’varies from .505 in initial day

of listing to .624 after 36 months of listing. From the analysis of data it can be concluded that

there is no significant relation between IPOs returns and age of the company during the period at

0.05 percent level of significance. The study concluded that ‘The age of the firm has significant

impact on short-run and long-run performance of the IPOs’ in the study period.

6. References:

1. A Shokand (2013), “long term performance of Indian IPOs” http:// shodhganga. inflibnet.

ac. in / bitstream.

2. BilsonJournal of Finance, “Age on Aftermarket Stock Performance Vol. 32. No. 4.1977,

pp1151-1168.

3. Block, Stanley and Majorie Stanley. "The Financial Characteristics and Price

Movement Patterns of Companies Approaching the Unseasoned Securities Market in the

late 1972s", Financial Management, Vol.9, No.4, 1989, pp.30-36.

4. Business Line “SEBI eases minimum public issue size to 10 pc” Business Line, December

23, 2000

5. Claudio Loderer and UrsWaelchli “Firm age and performance”, Journal of Financial

Economics September 27, 2009, Vol.87, Page No. 329-356.

6. David T. Clark “A Study of the Relationship Between Firm Age-at-IPO and Aftermarket

Stock Performance” The Leonard N. Stern School of Business, NBER Working Paper Series,

2010.

7. Dr. Rajesh C. Jamapala, Dr. P. Adi Lakshmi and Mr. D. SrinivasaRao (2013) “A Study on

Performance of Initial Public Offerings (IPOs) in India during 2007-2011”, Management

Today, Vol. 2, No.3, July, 2012, Page 12-26.

8. Ericson, R., Pakes, A., (1995), “Markov-perfect industry dynamics: A framework for

empirical work”. Review of Economic Studies, Volume. 62, page No. 53-82.

9. Finn, Frank J. and Ron Higham. "The Performance of Unseasoned New Equity Issues-

cum-Stock Exchange Listings in Australia", Journal of Banking and Finance, 1988, Vol.11,

No.3, pp.333-352.

10. Hensler “impact of fundamental on IPOs” Correlated trading and returns. Journal of Finance

63, 885–920

11. Ibbotson, R., (1975), « Price performance of commun stock new issues », Journal of

Financial Economics, Vol. 2, pp. 235-272.

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:960

Volume IX, Issue I, January/2020 Page No:929

12. Jovanovic, Boyan& Peter L. Rousseau. 2001. “Why Wait? A Century of Life Before IPO.”

NBER Working Paper Series.

13. Manu Kaushik , “All fall down” Business Today, June 26, 2011.

14. Mario Levis. "The Long-Run Performance of Initial Public Offerings: The UK Experience

1980-1988", Financial Management, Vol. 22, No. 1, 1993, pp 28-41.

15. Reilly, Frank K. "New Issues Revisited,” Financial Management, Vol. 6, No. 4, 1977,

pp28-42.

16. ReenaAggarwal, Ricardo Leal, Leonardo Hernandez (2011), “The Aftermarket Performance

of Initial Public Offerings in Latin America” Financial Management, Vol. 22, No. 1 (Spring,

1993), pp. 42-53.

17. Ritter, J.R. "The Choice between Firm Commitment and Best Efforts Contracts,”

Unpublished Working Paper, University of Michigan, Ann Arbor, 1991.

18. Rock, K. "Why New Issues are underpriced?" Journal of Financial Economics, Vol. 15, Nos.

1/2, January/February 1986, pp 187-212.

19. SeshadevSahoo and PrabinaRajib (2010), “After Market Pricing Performance of Initial

Public Offerings (IPOs): Indian IPO Market 2002-2006” VIKALPA, Volume 35, No. 4,

October – December 2010.

Parishodh Journal

Volume IX, Issue I, January/2020

ISSN NO:2347-6648

Page No:961