dia 2015_sales

TRANSCRIPT

1

Agenda

Marek PodstawaBoD Member

Downstream – Sales

22

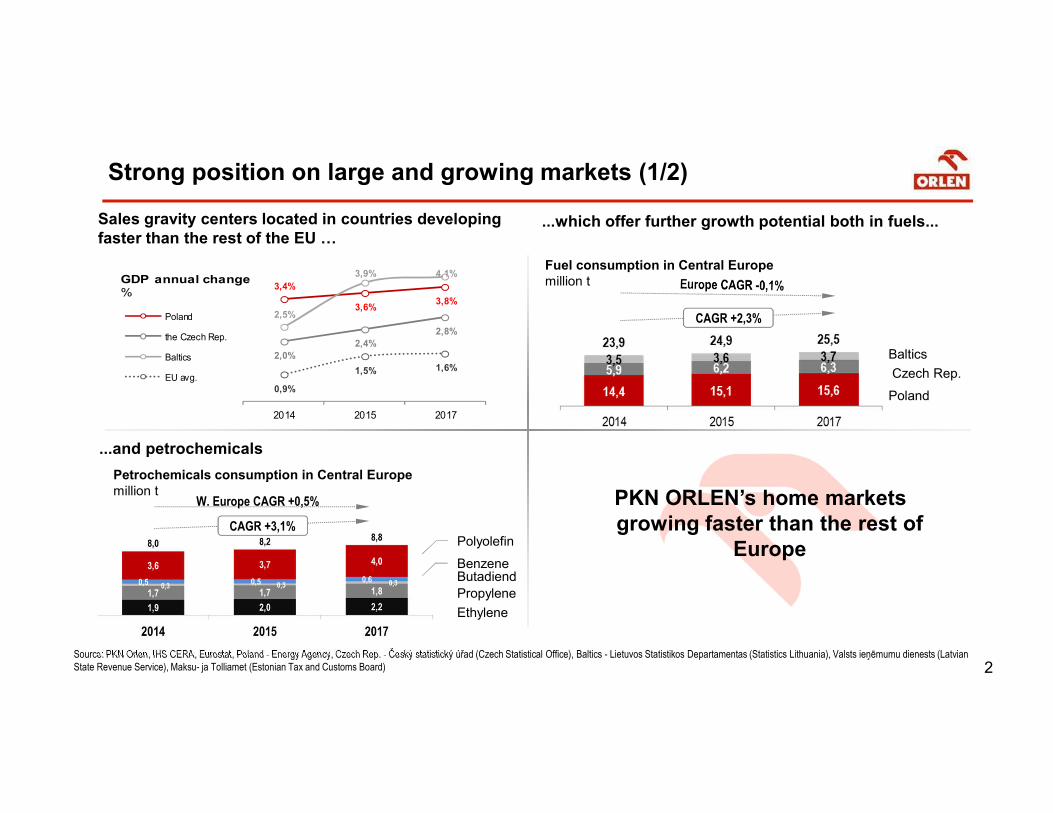

Strong position on large and growing markets (1/2)

Sales gravity centers located in countries developing faster than the rest of the EU …

Source: PKN Orlen, IHS CERA, Eurostat, Poland - Energy Agency, Czech Rep. - Český statistický úřad (Czech Statistical Office), Baltics - Lietuvos Statistikos Departamentas (Statistics Lithuania), Valsts ieņēmumu dienests (Latvian State Revenue Service), Maksu- ja Tolliamet (Estonian Tax and Customs Board)

Czech Rep.

...which offer further growth potential both in fuels...

CAGR +2,3%

Fuel consumption in Central Europemillion t

Poland

Baltics

...and petrochemicals

Petrochemicals consumption in Central Europemillion t

Ethylene

Polyolefin

BenzeneButadiend

Propylene

CAGR +3,1%

W. Europe CAGR +0,5% PKN ORLEN’s home marketsgrowing faster than the rest of

Europe

3,4%

3,6%3,8%

2,0%

2,4%

2,8%

2,5%

3,9% 4,1%

0,9%

1,5% 1,6%

2014 2015 2017

GDP annual change%

Poland

the Czech Rep.

Baltics

EU avg.

3

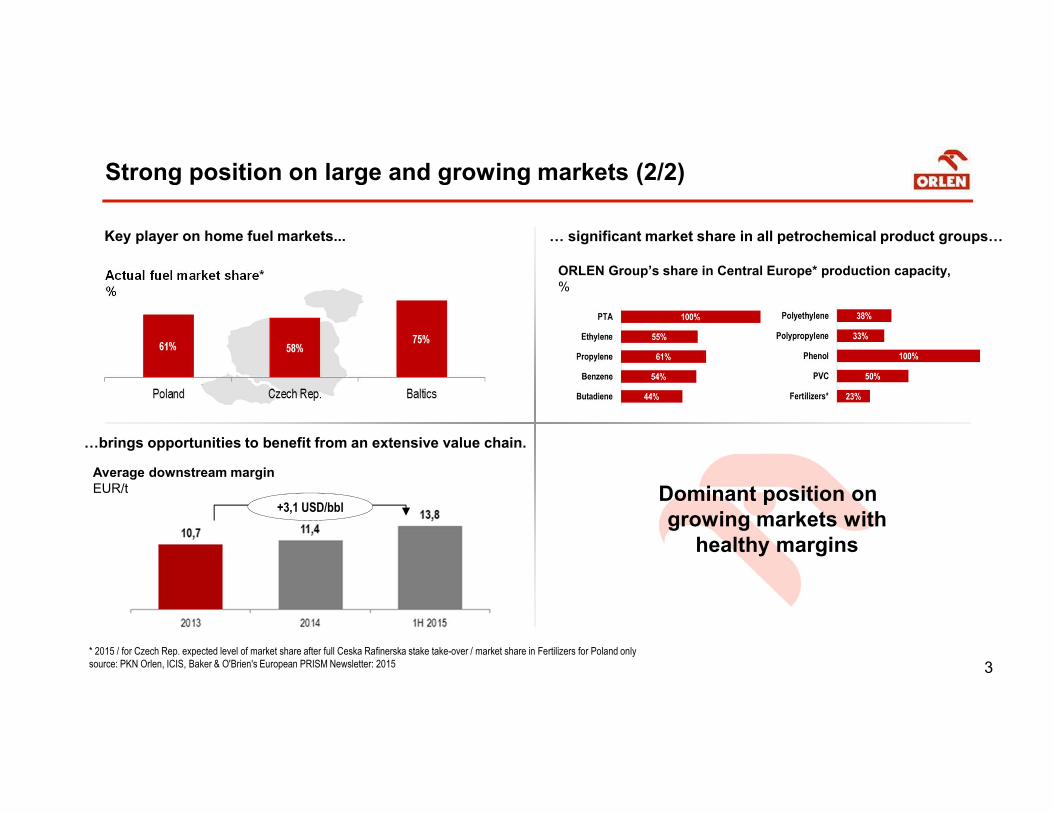

Strong position on large and growing markets (2/2)

* 2015 / for Czech Rep. expected level of market share after full Ceska Rafinerska stake take-over / market share in Fertilizers for Poland onlysource: PKN Orlen, ICIS, Baker & O'Brien's European PRISM Newsletter: 2015

Key player on home fuel markets... … significant market share in all petrochemical product groups…

…brings opportunities to benefit from an extensive value chain.

Actual fuel market share* %

+3,1 USD/bblDominant position on growing markets with

healthy margins

ORLEN Group’s share in Central Europe* production capacity, %

Average downstream marginEUR/t

44

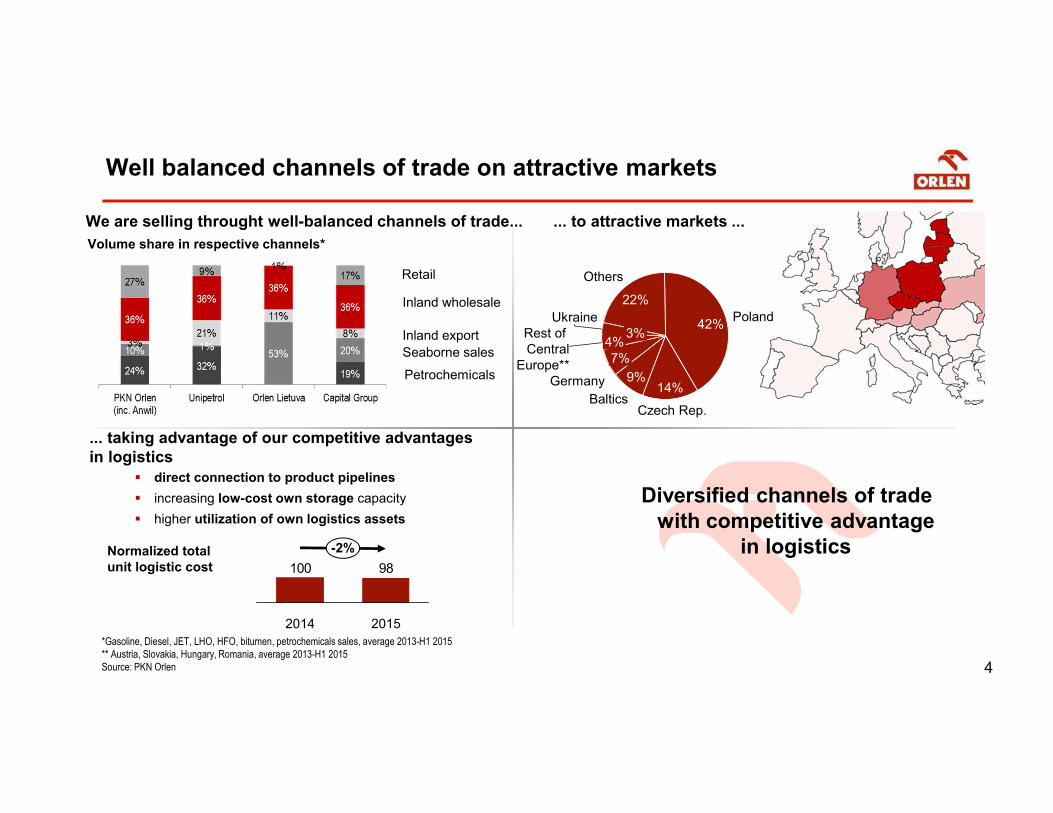

Well balanced channels of trade on attractive markets

... to attractive markets ...

Volume share in respective channels*

We are selling throught well-balanced channels of trade...

... taking advantage of our competitive advantagesin logistics

direct connection to product pipelines

increasing low-cost own storage capacity

higher utilization of own logistics assets

Normalized total unit logistic cost

*Gasoline, Diesel, JET, LHO, HFO, bitumen, petrochemicals sales, average 2013-H1 2015** Austria, Slovakia, Hungary, Romania, average 2013-H1 2015Source: PKN Orlen

98100

-2%

20152014

Retail

Inland wholesale

Inland export

Seaborne sales

Petrochemicals

Diversified channels of trade with competitive advantage

in logistics

7%

Baltics

9%

Czech Rep.

14%

Poland42%

Others

22%

Ukraine3%

Germany

4%Rest of Central

Europe**

55

Modern management culture

CUSTOMERS

INNOVATION

EFFECTIVENESS

PEOPLE

HEALTH & SAFETY

Experienced, well trained and highly motivated team

„Top Employer” according to sales managers of the largest Polish companies

Emphasis on customer relationship

Supply quality and reliability

Unique product offer

New business models for fuels, petrochemicals, lubricants and bitumen sales

Cost discipline

Systematic improvement of sales organization efficiency

Continuous focus on safety and environmental performance

6

Key strategic directions:Capture value on growing Central European markets

Development of trading competences;

Expansion to attractive, neighbouring markets;

Capture higher demand from diminishing grey zone.

Fuel marketing

Continuous business development and extension of value chain;

Diversification of product portfolio and customer base;

Volume increase and maintenance of unit margins.

Petrochemicals

Systematic enhancement of competitive advantage through growing elasticity, service quality and cost optimization;

Divestment of non-strategic assets;

Use of synergies with key infrastructure operators through alliances and strategic partnerships.

Logistics

7

Retail

Marek PodstawaBoD Member

8

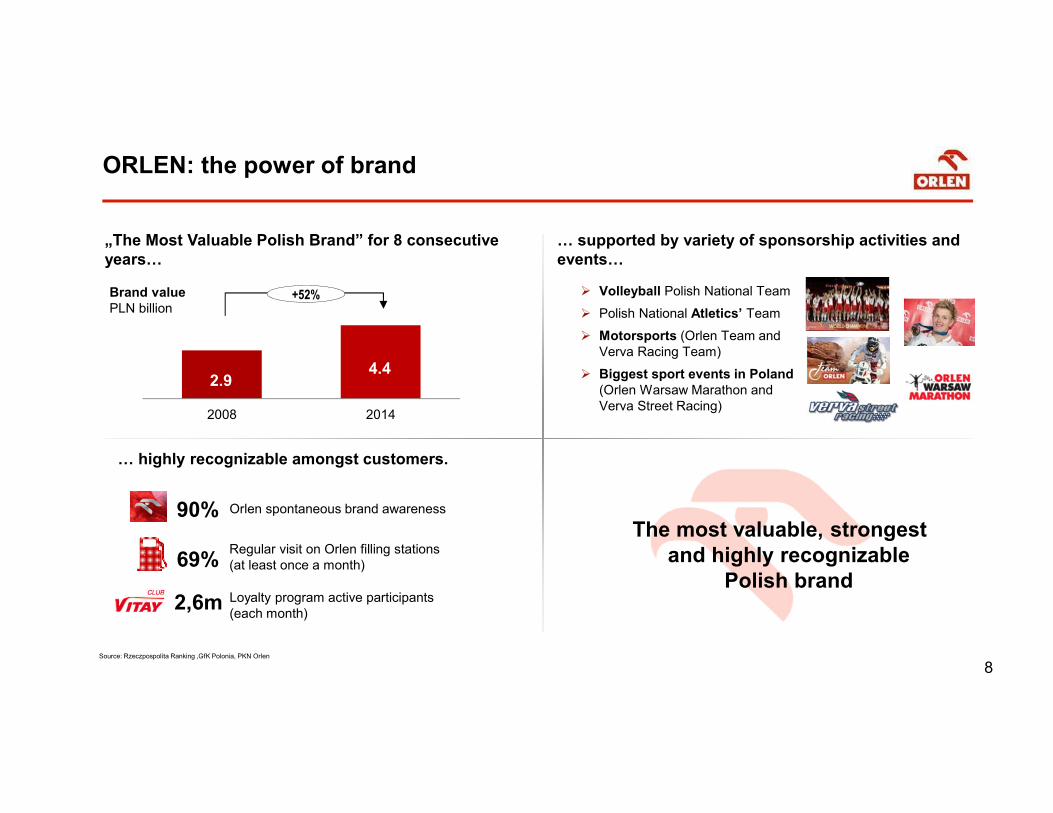

ORLEN: the power of brand

„The Most Valuable Polish Brand” for 8 consecutive years…

2.94.4

2008 2014

+52%Brand valuePLN billion

The most valuable, strongestand highly recognizable

Polish brand

Regular visit on Orlen filling stations(at least once a month)

Orlen spontaneous brand awareness

90% 96%

… highly recognizable amongst customers.

90%

69%

2,6m Loyalty program active participants(each month)

Source: Rzeczpospolita Ranking ,GfK Polonia, PKN Orlen

… supported by variety of sponsorship activities and events…

Volleyball Polish National Team

Polish National Atletics’ Team

Motorsports (Orlen Team and Verva Racing Team)

Biggest sport events in Poland (Orlen Warsaw Marathon and Verva Street Racing)

9

Volume per sitemln liters

EBITDAPLN million

Nonfuel margin index; 2014 =100

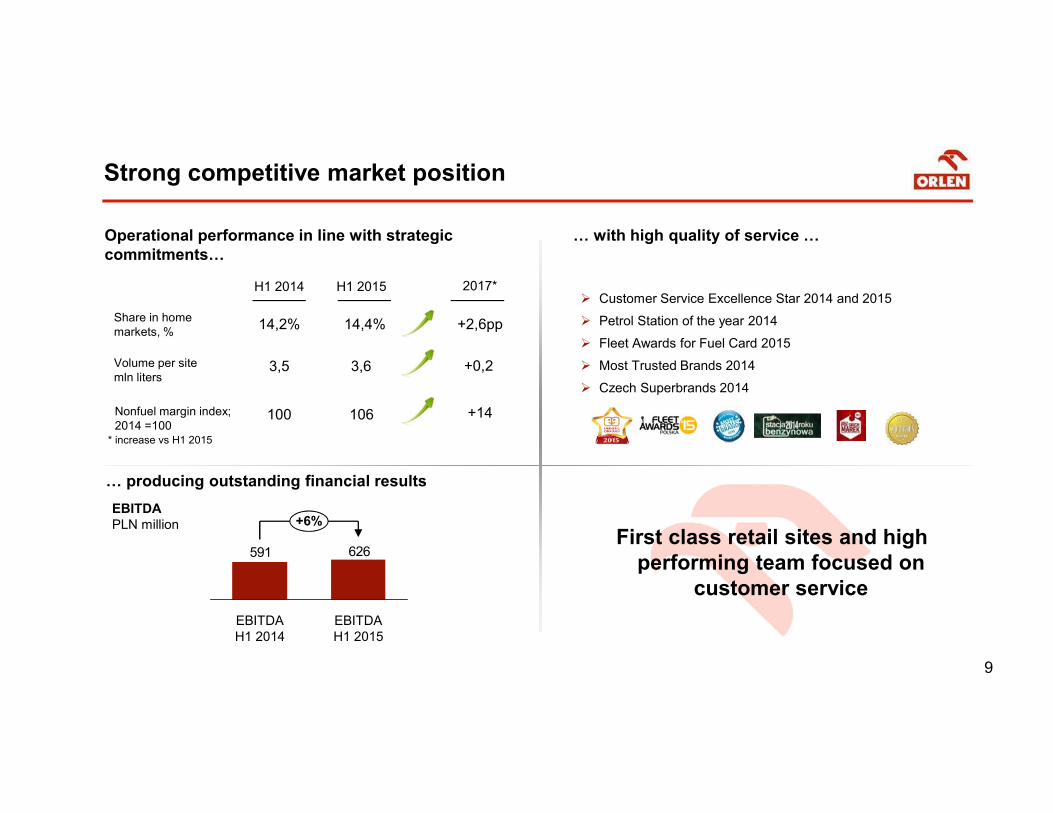

Strong competitive market position

Customer Service Excellence Star 2014 and 2015

Petrol Station of the year 2014

Fleet Awards for Fuel Card 2015

Most Trusted Brands 2014

Czech Superbrands 2014

Operational performance in line with strategic commitments…

… producing outstanding financial results

… with high quality of service …

3,6

106

H1 2015 2017*

+0,2

H1 2014

3,5

100 +14

First class retail sites and high performing team focused on

customer service

Share in home markets, %

14,2% 14,4% +2,6pp

* increase vs H1 2015

626591

EBITDAH1 2015

EBITDAH1 2014

+6%

10

+15%

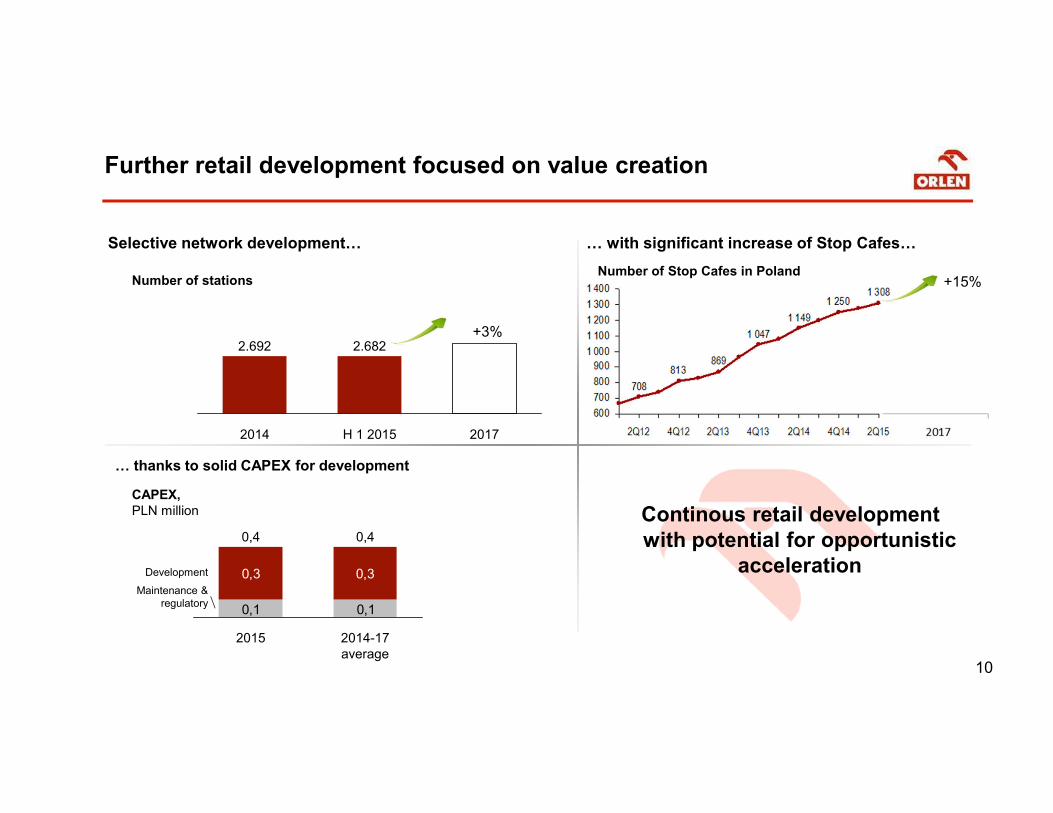

Further retail development focused on value creation

Number of Stop Cafes in Poland

CAPEX, PLN million

Selective network development…

… thanks to solid CAPEX for development

Number of stations

… with significant increase of Stop Cafes…

Continous retail development with potential for opportunistic

acceleration

+3%

0,3 0,3

0,10,1

2014-17average

Development

Maintenance ®ulatory

0,4 0,4

2015

2014 2017

2.692

H 1 2015

2.682

11

Key strategic directions:From a solid product supplier to customer experience provider

Fuel … … store …

… food …

Core competence

High quality of fuels and services

Increasing market efficiency

‚Must have’ for a filling station

Convenience and fast shopping

Store formats adjusted to market needs

Response to changing lifestyle and eating habits

Innovative products tailored to local preferences

Rapid development

… experience